ID : MRU_ 436535 | Date : Dec, 2025 | Pages : 248 | Region : Global | Publisher : MRU

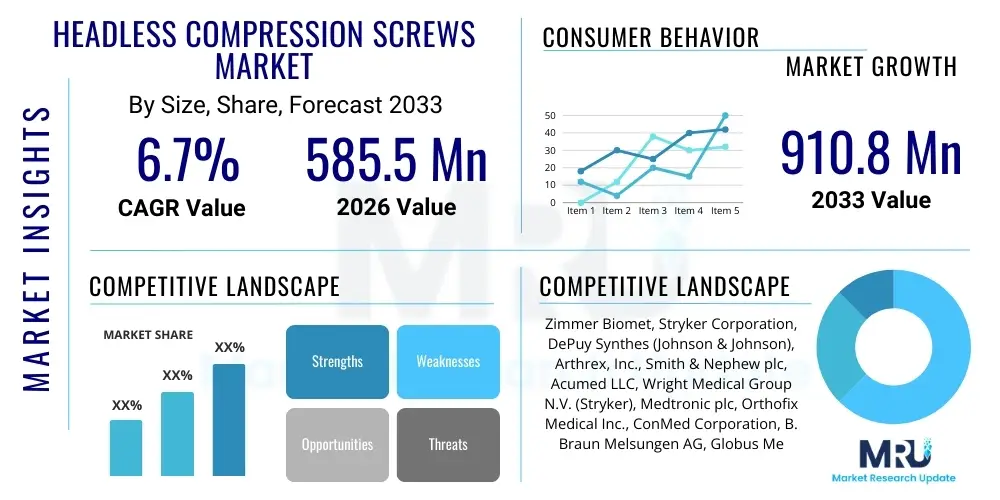

The Headless Compression Screws Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.7% between 2026 and 2033. The market is estimated at USD 585.5 Million in 2026 and is projected to reach USD 910.8 Million by the end of the forecast period in 2033.

The Headless Compression Screws Market encompasses the manufacturing, distribution, and utilization of specialized orthopedic implants designed primarily for fracture fixation in small bone anatomy, notably in the foot, ankle, hand, and wrist. These screws are characterized by their fully buried design, lacking a traditional screw head, which minimizes soft tissue irritation and allows for better articulation and joint mobility post-surgery. The inherent design utilizes a differential thread pitch between the proximal and distal ends of the screw, generating controlled compression across the fracture site as the screw is fully seated, promoting primary bone healing and stability. This mechanism makes them indispensable in treating intra-articular fractures, osteotomies, and arthrodesis procedures where anatomical contours and minimal hardware prominence are critical to successful patient outcomes.

The core product technology centers on cannulated systems, which allow the surgeon to precisely guide the screw over a K-wire, enhancing accuracy, reducing surgical invasiveness, and minimizing operative time. Major applications span complex trauma care, reconstructive surgery, and elective orthopedic procedures. Benefits include superior cosmetic outcomes, reduced risk of secondary surgery for hardware removal (due to reduced impingement), and enhanced mechanical stability for specific fixation patterns. Driving factors underpinning market expansion include the global increase in incidence of sports-related injuries and trauma, the rising prevalence of degenerative joint diseases necessitating arthrodesis, and the sustained demographic shift toward an aging population, which is more susceptible to fragility fractures requiring specialized fixation devices.

Furthermore, continuous innovation in biomaterials, particularly the shift toward advanced titanium alloys and, increasingly, bioresorbable polymers, is enhancing screw performance characteristics such as biocompatibility and load-bearing capacity. The market is also heavily influenced by advancements in surgical techniques, especially the proliferation of minimally invasive surgery (MIS). Headless compression screws are optimally suited for MIS approaches due to their slender profile and precise deployment mechanisms, appealing to both surgeons seeking reduced operational trauma and patients desiring faster recovery times and less scarring. Regulatory standards governing implant safety and efficacy, while rigorous, also drive manufacturers to invest heavily in clinical trials supporting the superior performance and long-term viability of these devices in small bone surgery.

The Headless Compression Screws Market is characterized by robust, sustainable growth fueled by continuous technological refinements in orthopedic trauma and reconstructive surgery. Business trends indicate a strong focus on system simplification, offering comprehensive tray solutions that cater to varying anatomical requirements, from 2.0 mm screws for hand trauma to larger diameter screws for hindfoot fusions. Market leaders are strategically engaging in mergers and acquisitions to consolidate intellectual property related to proprietary threading technologies and material science, aiming to capture niche segments, such as pediatric orthopedics and specialized podiatric surgery. Furthermore, the rising adoption of volume-based procurement strategies by major hospital systems is intensifying competitive pricing pressures, necessitating efficiency gains throughout the manufacturing value chain, particularly concerning titanium alloy processing and sterilization protocols.

Regionally, North America maintains its position as the dominant market, primarily driven by established reimbursement frameworks, high patient awareness regarding advanced orthopedic treatments, and the pervasive presence of key market players and specialized trauma centers. However, the Asia Pacific (APAC) region is projected to exhibit the highest CAGR during the forecast period. This accelerated growth in APAC is attributed to rapidly improving healthcare infrastructure in countries such as China and India, increasing governmental expenditure on healthcare access, and the burgeoning trend of medical tourism for complex orthopedic procedures. European markets demonstrate stable growth, characterized by strong clinical acceptance of innovative fixation systems and rigorous safety standards imposed by regulatory bodies like the European Medicines Agency (EMA), favoring established, clinically proven products.

Segment trends reveal that the Application segment—specifically Foot & Ankle surgery—represents the largest revenue contributor due to the high incidence of associated fractures and the complexity of tarsal and metatarsal fusions requiring precise compression. In terms of product material, Titanium alloys continue to dominate due to their optimal strength-to-weight ratio and inert biocompatibility. However, the bioresorbable screws segment, though smaller, is gaining significant traction, particularly in pediatric applications and cases where permanent hardware retention is undesirable, signaling a key area for future R&D investment and market disruption. The shift towards Ambulatory Surgical Centers (ASCs) as primary locations for elective orthopedic procedures is also a key macroeconomic trend influencing distribution strategies and packaging requirements.

Common user questions regarding AI's impact on the Headless Compression Screws Market frequently revolve around its potential to enhance surgical precision, automate inventory management, and personalize implant selection. Users are keen to understand how machine learning (ML) algorithms can assist in pre-operative planning, specifically in optimizing screw trajectories and determining the ideal screw length and diameter based on complex CT or MRI imaging data, thereby minimizing complications and improving fixation rigidity. A secondary, yet crucial, area of inquiry concerns the use of predictive analytics for supply chain logistics, ensuring that specialized screw sizes and instrumentation sets are available precisely when needed in trauma situations, reducing administrative burdens and operational costs for hospitals. There is also significant interest in the application of deep learning models to correlate specific fracture patterns with optimal surgical outcomes achieved using headless compression screws, potentially leading to new, evidence-based surgical protocols and product design enhancements.

The integration of AI is transforming the pre-operative workflow. AI-powered imaging analysis tools can automatically segment bone structures and simulate the mechanical stress distribution across the fracture site, providing surgeons with crucial data to select the most appropriate implant and insertion angle before entering the operating room. This level of predictive modeling significantly reduces variability in surgical outcomes, a key benefit in complex intra-articular fractures. Furthermore, AI systems are beginning to be incorporated into robotic surgical assistants, guiding the precise drilling and insertion of K-wires, which is fundamental to the subsequent placement of cannulated headless screws. This augmentation enhances the accuracy of minimally invasive procedures, reducing fluoroscopy time and improving overall surgical efficacy, thus validating the premium pricing often associated with high-end headless screw systems.

Beyond the surgical theatre, AI is profoundly influencing the commercial and manufacturing sectors of the market. Manufacturers are leveraging AI for quality control by analyzing microscopic material flaws during production, ensuring the highest standards of mechanical integrity for the screws. On the business side, predictive demand forecasting based on seasonal injury patterns, regional demographic data, and historical sales trends allows companies to optimize production schedules and reduce inventory obsolescence. This enhanced efficiency throughout the value chain contributes directly to maintaining stable product supply, particularly for specialty screws required for rare or complex orthopedic conditions. The overall expectation is that AI will standardize complex procedures, democratize access to high-precision surgery, and accelerate the development cycle of next-generation screw designs.

The dynamics of the Headless Compression Screws Market are complex, driven by escalating demand for superior fracture fixation technologies, yet constrained by economic barriers and stringent regulatory pathways. The primary drivers include the global increase in age-related degenerative conditions and trauma incidence, leading to a higher volume of orthopedic surgeries, coupled with the proven efficacy of headless screws in achieving stable, internal compression, particularly in delicate small bones. However, the market faces significant restraints, chiefly the high initial cost of specialized implants and associated sterile instrument trays, which can strain hospital budgets, especially in developing economies. Moreover, the need for highly skilled orthopedic surgeons proficient in advanced minimally invasive cannulated techniques acts as a logistical bottleneck, limiting adoption in regions with nascent surgical training programs. Opportunities abound in the development of customized implants using additive manufacturing (3D printing) and the expansion into untapped emerging markets across Asia and Latin America, where demand for advanced trauma care is accelerating faster than infrastructural development.

The industry's competitive landscape is strongly shaped by Porter's Five Forces. The Threat of New Entrants is moderate; while manufacturing precision requires substantial capital investment and regulatory hurdles are high, the potential for disruptive technologies (like bioresorbable or 3D-printed screws) remains attractive to smaller, innovation-focused startups. The Bargaining Power of Buyers (Hospitals and Group Purchasing Organizations or GPOs) is significant, particularly in mature markets like North America and Western Europe, where consolidation leads to high-volume procurement contracts demanding price concessions. GPOs leverage volume to pressure manufacturers, necessitating robust cost efficiency measures across the supply chain. Conversely, the Bargaining Power of Suppliers of specialized raw materials, primarily medical-grade titanium and high-performance polymers, is moderate to high, as these materials require rigorous certification and specialized refinement processes, limiting the supplier base.

The Threat of Substitutes is moderate. While conventional screw fixation (headed screws, pins, and plates) remains viable for many fractures, the distinct benefits of headless compression (minimal soft tissue irritation and superior interfragmentary compression) limit direct substitution, especially for intra-articular or joint fusion procedures. However, external fixation methods and advanced plating systems occasionally serve as alternatives for certain complex fractures. Competitive Rivalry among existing players is intense, characterized by continuous intellectual property disputes, rapid product iteration (e.g., variable thread pitch optimization, new coating technologies), and aggressive marketing centered on clinical evidence and superior surgical instrumentation sets. Companies heavily invest in surgeon education and training programs to establish brand loyalty, making incremental product differentiation a core strategic imperative in maintaining market share in this technically demanding sector.

The Headless Compression Screws Market is comprehensively segmented based on critical factors including Product Type (standard vs. variable pitch), Diameter (mini, small, standard), Material (Titanium, Stainless Steel, Bioresorbable), Application (Foot & Ankle, Hand & Wrist, Others), and End-User (Hospitals, Ambulatory Surgical Centers, Orthopedic Clinics). This granular segmentation is essential for manufacturers to tailor their product offerings and marketing strategies to specific surgical needs and facility types. The diameter segmentation is particularly important, as orthopedic trauma spans a wide range of bone sizes, requiring screw diameters ranging from sub-2.0 mm systems for phalanges to over 4.0 mm systems for ankle fusions. The market’s evolution is driven primarily by the Application segment, where the complexity and increasing volume of foot and ankle surgeries demand specialized, robust fixation solutions that headless screws effectively provide.

Material segmentation reveals the strategic shift within the industry. While conventional stainless steel provides adequate structural integrity at lower cost, titanium alloys are overwhelmingly preferred due to superior biocompatibility, reduced artifact generation in post-operative imaging (MRI/CT), and better osseointegration properties. The burgeoning bioresorbable segment, utilizing polymers like PLLA (Poly-L-Lactide) or PLGA (Poly-Lactide-co-Glycolide), represents the future of specialized fixation, particularly appealing in pediatric cases or in scenarios where permanent implants might cause long-term stiffness or future hardware-related discomfort. These segments require distinct manufacturing processes and substantial research investment to ensure mechanical strength is maintained until sufficient bone healing is achieved, after which the material gradually degrades and is absorbed by the body.

End-User segmentation highlights the shifting point of care. While large hospitals and trauma centers remain the primary purchasers due to the volume of complex and emergency surgeries, Ambulatory Surgical Centers (ASCs) are rapidly increasing their purchasing power, especially for elective procedures like bunion corrections or non-complex hand surgeries. This shift necessitates changes in packaging and distribution strategies, focusing on smaller, highly optimized sterile kits suitable for rapid turnover in the ASC environment. Successful market players must therefore maintain diverse distribution channels capable of serving both high-volume hospital systems and efficiency-focused outpatient facilities, ensuring that the specific demands of each end-user group—whether high complexity (Hospitals) or high efficiency (ASCs)—are met with appropriate inventory and support services.

The value chain for the Headless Compression Screws Market is highly specialized and knowledge-intensive, beginning with the meticulous procurement of raw materials, primarily certified medical-grade titanium (Ti-6Al-4V) and stainless steel, or advanced bioresorbable polymers. The Upstream Analysis involves forging and machining, where precision engineering is paramount to ensure the required differential thread pitch and cannulation dimensions. Given the load-bearing requirements and minimal tolerance for defects, raw material quality checks, and sophisticated milling and turning operations define this stage. Manufacturers must adhere to rigorous ISO 13485 standards for medical device quality management systems. Strategic sourcing relationships are crucial here, as raw material availability and pricing fluctuations directly impact the final product cost and profitability, necessitating long-term contracts with specialized metal and polymer suppliers.

The core manufacturing and operational stage involves thread rolling, surface treatment (such as anodization for titanium), laser etching for identification, and ultimately, stringent cleaning and sterile packaging. This stage is capital-intensive, requiring specialized cleanroom facilities and validated sterilization processes (e.g., gamma irradiation or ethylene oxide). Direct and indirect distribution channels then move the finished, sterile products to end-users. Direct channels involve the manufacturer’s own sales force and regional stocking centers, facilitating direct negotiations with major hospital networks and trauma centers. This channel allows for greater control over inventory and faster technical support. Indirect channels utilize specialized medical device distributors or agents who handle logistics, inventory, and localized sales for smaller clinics and specialized regional surgical groups, especially beneficial in geographically dispersed or emerging markets.

The downstream analysis focuses on the interaction with end-users and post-market surveillance. Effective distribution requires not only the delivery of the implants but also the management and maintenance of the specialized, reusable instrumentation sets (trays and drivers) required for insertion. These instrument sets represent a significant capital investment and logistical challenge, requiring constant tracking, cleaning, and sterilization support. Post-market surveillance is critical for collecting real-world data on performance and potential complications, informing design iterations and satisfying regulatory reporting requirements. The entire value chain is therefore characterized by the necessity for flawless precision, stringent quality assurance at every step, and highly trained personnel capable of managing complex inventory logistics and clinical support.

The primary consumers and end-users of headless compression screws are orthopedic healthcare providers focusing on trauma, reconstructive surgery, and elective procedures involving small bones. The most significant customer segment comprises large academic hospitals and specialized trauma centers, which handle high volumes of complex fractures in the hand, wrist, foot, and ankle, often requiring urgent surgical intervention. These institutions require a broad portfolio of screw sizes and materials, robust inventory management, and 24/7 technical support, making them the most influential segment in terms of driving volume and establishing clinical standards. Procurement in this segment is often managed by Group Purchasing Organizations (GPOs), leading to price sensitivity but also rewarding long-term, high-volume supply contracts based on product reliability and clinical evidence.

The second key customer segment is Ambulatory Surgical Centers (ASCs). ASCs focus predominantly on elective orthopedic procedures, such as forefoot corrections (e.g., bunionectomies) and non-complex hand surgeries, where the minimally invasive attributes and reduced tissue irritation of headless screws are highly valued for facilitating quick patient discharge. ASCs prioritize efficiency, cost-effectiveness, and streamlined inventory, preferring smaller, pre-packaged, single-use instrument kits over large, reusable trays. Manufacturers targeting ASCs must emphasize ease of use, competitive unit pricing, and distribution logistics that minimize inventory footprint. This segment is growing rapidly and represents a strategic pivot point for market share acquisition, driven by increasing preference among surgeons and patients for outpatient settings.

Finally, specialized orthopedic and podiatric clinics, often affiliated with larger health systems, represent a critical customer base for specific applications, particularly foot and ankle specialists who utilize these implants daily for osteotomies and fusions. These specialists often drive clinical adoption of new, highly specialized products based on published clinical data and technical advantages. Engaging key opinion leaders (KOLs) within these clinics is crucial for market penetration. The purchasing decisions in this segment are heavily influenced by clinical outcomes, surgeon preference, and the availability of dedicated educational resources and hands-on training provided by the manufacturer. Effective communication of clinical superiority and long-term patient benefits is essential to convert these specialists into brand loyal users.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 585.5 Million |

| Market Forecast in 2033 | USD 910.8 Million |

| Growth Rate | 6.7% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Zimmer Biomet, Stryker Corporation, DePuy Synthes (Johnson & Johnson), Arthrex, Inc., Smith & Nephew plc, Acumed LLC, Wright Medical Group N.V. (Stryker), Medtronic plc, Orthofix Medical Inc., ConMed Corporation, B. Braun Melsungen AG, Globus Medical Inc., DJO Global, Paragon 28, CrossRoads Extremity Systems, OsteoMed L.P., BioPro, Inc., Novastep, NextStep Arthropedix, Inion Oy. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technology landscape governing the Headless Compression Screws Market is characterized by continuous refinement aimed at improving insertion mechanics, enhancing compression dynamics, and expanding material biocompatibility. A fundamental technology is the advanced cannulated design, which utilizes specialized K-wires (guidewires) to precisely control screw placement, drastically improving accuracy in difficult anatomical locations like the scaphoid bone. Recent innovations focus on optimizing the differential thread pitch—the variation in pitch between the leading and trailing threads—to maximize interfragmentary compression with minimal effort and reduce the risk of stripping or overtightening. Furthermore, advancements in specialized driving mechanisms and self-retaining drivers minimize slippage during insertion, which is critical in hard bone structures where screw engagement is challenging.

Material science represents another crucial technological frontier. While conventional titanium alloys (Grade 5 Ti-6Al-4V) remain the gold standard, manufacturers are increasingly developing proprietary surface treatments, such as hydroxyapatite coatings, to promote faster and stronger bone integration (osseointegration). The emergence of PEEK (Polyetheretherketone) and, more significantly, fully bioresorbable polymers like PLLA/PLGA, offers fixation solutions that gradually transfer load back to the healing bone, potentially eliminating the long-term foreign body reaction risk and the need for expensive secondary removal surgeries. Although bioresorbable screws currently face challenges related to initial strength and predictable degradation rates, ongoing material engineering efforts are steadily overcoming these limitations, positioning them as a highly disruptive future technology, especially for younger, active patients.

Additive Manufacturing (3D Printing) is rapidly influencing the market, moving beyond prototyping into the direct production of surgical tooling and, increasingly, patient-specific implants. 3D printing allows for the creation of customized surgical guides that ensure perfect trajectory and depth during K-wire placement, substantially reducing intraoperative errors. Although direct 3D printing of standard compression screws is less common due to the high-volume nature of the product, the technology is pivotal in developing complex, anatomical-specific screw designs and instrumentation sets tailored for unique trauma cases. Integrating these digital planning and manufacturing technologies ensures that the resulting headless compression system maximizes stability and conforms precisely to the patient’s unique skeletal anatomy, driving demand for premium, high-value surgical systems.

North America dominates the global Headless Compression Screws Market, primarily due to the highly sophisticated healthcare infrastructure, high expenditure on orthopedic R&D, and favorable reimbursement policies for advanced surgical procedures. The United States, in particular, drives the region's growth, characterized by a high incidence of sports injuries and an aging population with increasing demand for elective orthopedic procedures performed in both hospitals and a growing network of Ambulatory Surgical Centers (ASCs). The presence of major market leaders (e.g., Stryker, Zimmer Biomet, Arthrex) and their aggressive product development strategies, coupled with high awareness and acceptance among surgeons of advanced cannulated systems, solidifies its leading position. Regulatory standards, though strict (FDA approval), accelerate market adoption once efficacy is clinically validated, further cementing North America's status as a technological frontrunner and key revenue hub.

Europe represents the second-largest market, exhibiting steady and predictable growth. The market performance is largely influenced by the adoption rate in major Western European countries such as Germany, the UK, and France, which have established national healthcare systems prioritizing high-quality orthopedic care. Growth drivers include increasing road accidents and sports participation, coupled with a well-developed network of orthopedic specialists. European manufacturers often emphasize durability, material safety, and rigorous clinical data to comply with CE marking and local healthcare procurement requirements. Eastern European countries are showing faster, though smaller, growth rates as they upgrade their healthcare facilities and increase per capita healthcare spending, slowly transitioning from older fixation methods to modern headless compression technology.

Asia Pacific (APAC) is projected to be the fastest-growing region throughout the forecast period. This rapid expansion is driven by a confluence of factors: massive population size leading to a high absolute number of trauma cases, increasing disposable income allowing patients to access advanced private care, and significant investments by governments in developing medical infrastructure. Countries like China and India are focal points for growth, witnessing a surge in orthopedic patient volume and medical tourism. Local manufacturing is also scaling up, increasing competition and access to more affordable implant options, although premium products from multinational corporations still command significant market share due to perceived quality and clinical track record. The high demand for solutions in trauma and reconstructive foot and ankle surgery is fueling this rapid market uptake.

Latin America (LATAM) and the Middle East and Africa (MEA) represent emerging opportunities. In LATAM, countries like Brazil and Mexico are leading the adoption curve, driven by urbanization and rising incidence of high-energy trauma, although fragmented healthcare systems and varying reimbursement models present logistical challenges. The MEA region's growth is concentrated in the Gulf Cooperation Council (GCC) states (UAE, Saudi Arabia), where substantial government wealth is invested in state-of-the-art medical cities, attracting specialized surgical expertise and demanding premium orthopedic implants. However, political instability and limited access to advanced care in many African countries restrict overall regional growth, making MEA a strategically diverse market requiring localized approaches.

Headless compression screws are designed to be fully countersunk below the bone surface, eliminating potential soft tissue irritation, reducing the need for secondary hardware removal, and providing superior interfragmentary compression due crucial to the differential thread pitch mechanism for stable fracture healing, particularly critical in joints and small bone anatomy.

The Titanium Alloy segment, specifically Ti-6Al-4V, currently dominates the market. Titanium is preferred due to its high biocompatibility, excellent mechanical strength-to-weight ratio, inertness within the body, and minimal artifact distortion in post-operative MRI and CT scans compared to stainless steel.

MIS growth is a major driver, as headless compression screws, particularly those utilizing cannulated systems, are ideally suited for percutaneous and minimally invasive techniques. MIS reduces operative time, decreases patient morbidity, and allows for precise fixation over a guidewire, aligning perfectly with patient demands for faster recovery and reduced scarring.

Foot and Ankle Surgery holds the largest market share. The complex anatomy of the foot and ankle frequently requires precise compression for arthrodesis (joint fusion) and fixation of intra-articular fractures, making the low profile and strong compression capabilities of headless screws indispensable for successful clinical outcomes in this specialty.

Bioresorbable screws are a key growth opportunity, offering the potential to provide temporary fixation and compression while the bone heals, subsequently being absorbed by the body. This eliminates the need for removal surgery and is highly advantageous in pediatric cases and patients sensitive to permanent implants, though ongoing research focuses on improving their initial mechanical strength.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.