ID : MRU_ 432077 | Date : Dec, 2025 | Pages : 242 | Region : Global | Publisher : MRU

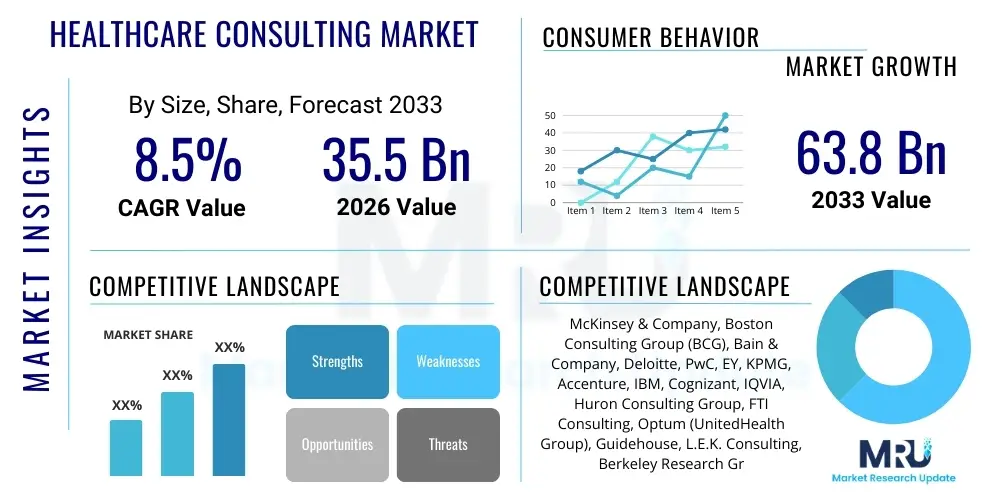

The Healthcare Consulting Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 8.5% between 2026 and 2033. The market is estimated at USD 35.5 Billion in 2026 and is projected to reach USD 63.8 Billion by the end of the forecast period in 2033.

The Healthcare Consulting Market encompasses advisory and implementation services provided to healthcare providers, payers, pharmaceutical companies, and biotechnology firms to improve efficiency, navigate regulatory landscapes, optimize operational performance, and adapt to technological disruption. This market is fundamentally driven by the global shift towards value-based care models, which necessitate complex operational restructuring and strategic planning. Consultants assist organizations in managing rising healthcare costs, integrating digital health solutions, ensuring compliance with evolving regulations like HIPAA and GDPR, and enhancing patient outcomes through clinical process optimization. The complexity inherent in modern healthcare systems, coupled with persistent financial pressures and the mandate for digital transformation, solidify the critical role of specialized consulting services across the entire healthcare ecosystem.

The core product offerings in this sector span a broad range, including strategic planning, financial management, operational efficiency improvements, clinical performance enhancement, and technology integration, particularly in electronic health records (EHR) and interoperability solutions. Major applications involve mergers and acquisitions (M&A) due diligence, population health management implementation, revenue cycle management (RCM) optimization, and enterprise resource planning (ERP) system deployment. Key benefits derived by clients include reduced operating expenses, improved utilization rates, successful digital transformation journeys, enhanced compliance posture, and clearer strategic direction for long-term growth and competitiveness. These services enable healthcare entities to remain resilient in a highly dynamic and constrained operating environment.

Driving factors for sustained market expansion include the rapid advancements in digital health technologies, such as telemedicine and remote monitoring, which require expert guidance for successful adoption and scalability. Furthermore, the aging global population contributes to an increased demand for complex healthcare services, amplifying the need for consultants skilled in resource allocation and capacity planning. The increasing scrutiny over pharmaceutical pricing and drug development efficiency necessitates specialized strategic consulting for biotech and pharma industries. Moreover, the inherent regulatory volatility and the perpetual need for risk management across all segments of the healthcare industry ensure a consistent demand for expert consulting services, positioning the market for robust and sustained growth throughout the forecast period.

The Healthcare Consulting Market is undergoing a rapid evolution characterized by significant business trends centered on digital transformation and market consolidation. Major consulting firms are aggressively expanding their digital health capabilities, focusing heavily on data analytics, cybersecurity resilience, and the implementation of Artificial Intelligence (AI) to automate administrative functions and enhance clinical decision support. The shift toward value-based contracts is forcing healthcare systems to reorganize service delivery, thereby fueling demand for operational and strategic consulting services aimed at cost reduction and quality improvement. Furthermore, merger and acquisition activity among healthcare providers and payers requires substantial consulting support for due diligence, integration planning, and post-merger synergy realization, dominating the high-value consulting segment.

Regionally, North America remains the largest market due to its mature healthcare infrastructure, complex payer-provider relationships, and high expenditure on specialized services, particularly in regulatory compliance and IT implementation. However, the Asia Pacific (APAC) region is projected to exhibit the highest growth rate, driven by escalating healthcare spending, increasing adoption of Western standards of care, and government initiatives aimed at modernizing healthcare infrastructure. European markets maintain stable growth, primarily focused on optimizing universal healthcare systems through efficiency programs and digital modernization efforts mandated by national health services. These regional dynamics highlight a globally fragmented but increasingly interconnected market where consulting methodologies must be tailored to specific economic and regulatory contexts.

In terms of segment trends, the Strategy Consulting segment holds the largest market share, driven by organizations seeking guidance on navigating pricing pressures, market entry strategies, and competitive positioning. Simultaneously, the Digital Consulting segment is experiencing the fastest growth, propelled by the urgent requirement for providers and pharmaceutical companies to leverage cloud computing, implement advanced data governance frameworks, and integrate patient-facing digital tools. End-user demand is heavily concentrated in pharmaceutical and biotech companies, which utilize consulting services for clinical trial optimization, supply chain restructuring, and ensuring market access compliance, followed closely by hospitals and provider systems focusing on revenue cycle and clinical pathway efficiency.

Common user questions regarding AI's impact on Healthcare Consulting predominantly revolve around themes of efficiency, necessity of human expertise, and data governance challenges. Users frequently question whether AI-powered tools, such as predictive models for patient flow or automated regulatory compliance checkers, will reduce the need for traditional operational consulting, focusing on the potential displacement of human consultants involved in data processing and basic analysis. Conversely, there is significant inquiry into how consulting firms must adapt their service offerings—specifically, what expertise is required to advise clients on selecting, integrating, and scaling complex AI solutions ethically and effectively, particularly concerning patient data privacy and algorithmic bias. The key themes summarized indicate a collective expectation that AI will transition consulting focus from operational delivery to strategic implementation, risk mitigation, and sophisticated interpretation of AI-generated insights, fundamentally elevating the role of the consultant to a high-level strategic advisor.

The market dynamics are governed by powerful drivers, systemic restraints, and evolving opportunities, all of which collectively constitute the core impact forces shaping market expansion. A primary driver is the pervasive governmental pressure worldwide to control escalating healthcare costs, mandating providers and payers to seek external consulting expertise for operational streamlining, efficiency improvements, and the transition to value-based payment models. Complementing this is the rapid pace of technological innovation, particularly in digital health (telemedicine, remote monitoring, and EMR optimization), which necessitates expert guidance for effective integration and change management within complex healthcare organizations. These drivers establish a foundational requirement for specialized knowledge that internal corporate resources often lack, ensuring sustained demand for external consultants.

Despite robust drivers, several restraints pose significant challenges to market growth. The high cost associated with premium consulting services often acts as a deterrent, especially for smaller hospitals or healthcare providers operating on tight margins, forcing them to prioritize immediate needs over long-term strategic projects. Furthermore, concerns regarding data privacy, security, and the necessity of navigating complex regulatory frameworks (such as HIPAA in the US and GDPR in Europe) require consultants to possess highly specialized knowledge, increasing the complexity and execution risk of projects. Internal resistance to change within conservative healthcare organizations, coupled with skepticism regarding the tangible return on investment (ROI) from large consulting engagements, often slows the decision-making and deployment timelines for consulting projects.

Opportunities within the Healthcare Consulting Market are abundant, primarily stemming from untapped potential in emerging economies in Asia Pacific and Latin America, where healthcare infrastructure development is accelerating rapidly, demanding advisory services for capacity building and digitalization. The growing integration of personalized medicine, genomics, and advanced diagnostics presents a new frontier for consultants specializing in clinical strategy, research organization, and patient engagement pathways. Moreover, the increasing focus on cybersecurity consulting within healthcare is a critical, high-growth opportunity, as providers become increasingly reliant on interconnected digital systems that are vulnerable to sophisticated cyber threats. These opportunities allow consulting firms to diversify their service portfolios and penetrate nascent high-value niches, mitigating the impact of existing restraints and fostering long-term market vitality.

The Healthcare Consulting Market is comprehensively segmented based on the type of service offered, the specific end-users requiring the expertise, and the functional area within the client organization being addressed. This segmentation provides clarity on the diverse needs of the market, ranging from high-level strategic planning to detailed technological implementation and ongoing operational optimization. The service types reflect the evolution of healthcare needs, moving beyond traditional operational reviews to encompass sophisticated digital and financial advisory roles. Understanding these distinct segments is crucial for consulting firms to align their core competencies with the most pressing client demands and prevailing industry trends, facilitating highly targeted and effective service delivery across the complex healthcare ecosystem.

The primary segment drivers vary significantly. For instance, the demand within the Pharmaceutical and Biotechnology segment is driven heavily by clinical trial optimization, regulatory strategy for novel therapies, and commercialization planning, focusing on specialized scientific and regulatory knowledge. Conversely, the demand from hospitals and provider systems often centers on enhancing revenue cycle management (RCM) efficiency, optimizing bed utilization, and achieving compliance with quality metrics, emphasizing operational and financial acumen. The increasing prevalence of complex integrated delivery networks (IDNs) further drives demand for integrated consulting solutions that span multiple segments, requiring expertise in organizational structure, governance, and seamless technology integration across diverse entities within a unified healthcare system.

The fastest-growing segments are centered around technology adoption. Digital Consulting, encompassing services related to cloud migration, data analytics implementation, and telehealth strategy, is witnessing unprecedented growth due to the industry’s accelerated push toward virtualization and data-driven decision-making following recent global health crises. Similarly, the IT Consulting sub-segment focused on Electronic Health Record (EHR) optimization and interoperability solutions remains robust, driven by regulatory mandates and the necessity for healthcare organizations to extract maximum value from their expensive IT investments. This technological shift underlines the market's trajectory towards data-centric, high-value consulting engagements.

The value chain for the Healthcare Consulting Market begins with Upstream Analysis, which focuses primarily on the acquisition and development of human capital and proprietary intellectual property (IP). Key upstream activities include intensive talent recruitment, particularly securing experts with clinical, regulatory, and specialized technological backgrounds (e.g., AI/ML engineers). Furthermore, the development of proprietary methodologies, benchmarking databases, and specialized diagnostic tools represents significant capital investment at this stage, establishing the foundation for differentiated service delivery. The quality and depth of this foundational expertise and IP directly dictate the firm's ability to tackle complex, high-value engagements and command premium pricing in the marketplace.

Midstream analysis focuses on the efficient execution and delivery of consulting engagements. This involves project management, data gathering and analysis, solution design, and client interaction. Effective project execution requires rigorous quality control processes, sophisticated analytical capabilities to interpret complex healthcare data sets (Big Data analytics), and the ability to tailor generalized methodologies to specific client contexts. The integration of modern project management tools and collaborative platforms enhances communication and transparency, crucial for maintaining client trust and ensuring that defined objectives—such as RCM improvements or clinical pathway optimization—are met accurately and on schedule, transforming raw expertise into actionable recommendations.

The downstream component of the value chain involves the implementation, distribution, and long-term impact realization for the client. Distribution channels are typically direct, involving long-term strategic relationships managed through key account executives. However, indirect channels, such as partnerships with technology vendors (e.g., EHR providers) or specialized managed service organizations (MSOs), are becoming increasingly common for joint solutions delivery. Successful downstream activities include rigorous change management support, performance monitoring post-implementation, and continuous advisory services to sustain improvements. The long-term establishment of client trust and demonstrable return on investment (ROI) significantly influences repeat business and referral volume, concluding the value generation cycle.

The primary customers, or end-users, of healthcare consulting services are broadly categorized across the entire healthcare spectrum, segmented into providers, payers, and life sciences organizations, each possessing distinct operational and strategic needs. Hospitals and Integrated Delivery Networks (IDNs) represent a cornerstone of the demand pool, continuously seeking consulting expertise to manage operational bottlenecks, optimize patient throughput, comply with complex reimbursement models, and implement large-scale IT systems like advanced EHRs. The immediate and tangible impact of consulting services on revenue cycle performance and quality metrics makes these organizations consistent and high-volume consumers of consulting engagements, often driven by survival in competitive regional markets and adherence to quality reporting standards.

Pharmaceutical and Biotechnology Companies form another critical customer base, particularly relying on strategic consulting services for market access strategy, clinical trial optimization, regulatory filing preparation, and complex commercialization planning for novel drugs and therapies. Given the high-risk, high-reward nature of drug development and the intense scrutiny on pricing, these organizations require highly specialized consultants with deep scientific and regulatory acumen to navigate global market complexities and maximize product value. Furthermore, consulting services are crucial in assisting these firms with supply chain resilience and digital transformation initiatives that integrate R&D data platforms and manufacturing processes.

Payer organizations, comprising health insurance companies and government health agencies, actively utilize consulting services to redesign benefit packages, manage risk under value-based payment contracts, improve claims processing efficiency, and implement sophisticated population health management programs. Government agencies, including national health services and public health bodies, engage consultants for large-scale policy implementation, resource allocation studies, and infrastructure planning projects aimed at modernizing national health delivery systems. These varied customer segments collectively ensure a diversified and robust demand base for consulting expertise across financial, operational, and digital domains.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 35.5 Billion |

| Market Forecast in 2033 | USD 63.8 Billion |

| Growth Rate | CAGR 8.5% |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | McKinsey & Company, Boston Consulting Group (BCG), Bain & Company, Deloitte, PwC, EY, KPMG, Accenture, IBM, Cognizant, IQVIA, Huron Consulting Group, FTI Consulting, Optum (UnitedHealth Group), Guidehouse, L.E.K. Consulting, Berkeley Research Group, Premier Inc., ECG Management Consultants, AlixPartners. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technology landscape underpinning the Healthcare Consulting Market is characterized by the increasing adoption of sophisticated digital platforms designed to enhance efficiency, facilitate data-driven decision-making, and manage complex regulatory requirements. Central to this landscape are Big Data analytics and Business Intelligence (BI) tools, which consultants leverage to analyze vast amounts of clinical, financial, and operational data. These technologies are critical for identifying performance gaps, forecasting demand, optimizing resource allocation, and proving the efficacy of interventions like population health programs. The integration of advanced visualization tools allows consultants to translate complex data into actionable insights for client leadership, making analytical sophistication a core differentiator in modern consulting services.

Furthermore, cloud-based technology platforms are fundamentally reshaping service delivery. Cloud solutions provide secure, scalable environments necessary for hosting Electronic Health Record (EHR) systems, managing large clinical datasets, and facilitating remote consulting engagements, particularly relevant for telehealth and remote patient monitoring strategy implementation. Interoperability solutions, often leveraging Fast Healthcare Interoperability Resources (FHIR) standards, are another vital technological area where consultants provide expertise. As healthcare systems strive for seamless data exchange between disparate organizational units and external partners, consultants specializing in integration technology are essential for bridging legacy systems with modern digital infrastructure, ensuring compliance while maximizing data flow.

The rapid emergence of Artificial Intelligence (AI), Machine Learning (ML), and Robotic Process Automation (RPA) tools is transforming both the consulting process and the solutions offered to clients. RPA is deployed internally by consulting firms to automate repetitive data gathering and analysis tasks, speeding up project timelines and reducing costs. For clients, consultants are advising on the implementation of AI for predictive modeling (e.g., readmission risk, operational scheduling) and leveraging ML algorithms for clinical decision support systems. This technological pivot requires consulting firms to continuously upskill their workforce in computational science and ethical AI frameworks, ensuring they remain at the forefront of digital strategy advisory services.

North America currently dominates the global Healthcare Consulting Market, largely due to the presence of a mature and highly complex healthcare system characterized by fragmented payer-provider dynamics and significant private sector investment. The United States market is fueled by the continuous cycle of regulatory changes, notably surrounding reimbursement mechanisms and quality reporting standards, which mandates consistent reliance on external expertise for compliance and adaptation. High IT spending, substantial adoption rates of digital health technologies, and the persistent pressure to manage exorbitant healthcare costs further solidify North America's leadership. Key consulting activities center on managing large-scale IT migrations, maximizing revenue cycle performance, and guiding complex mergers and acquisitions within Integrated Delivery Networks (IDNs).

Europe represents the second-largest market, exhibiting stable growth influenced primarily by government-led initiatives aimed at optimizing universal healthcare systems. Consulting demand in European countries is often focused on improving operational efficiency, managing waiting times, restructuring regional health services, and implementing pan-European data protection regulations like GDPR. Countries such as the UK, Germany, and France utilize consulting services for large public sector projects involving digital transformation and clinical pathway standardization. The fragmented nature of national health policies across the continent necessitates highly localized consulting approaches tailored to specific socio-economic and political healthcare mandates.

Asia Pacific (APAC) is anticipated to be the fastest-growing region, driven by rapid economic development, increasing public and private healthcare expenditure, and substantial government efforts to modernize outdated infrastructure. Key drivers include the emergence of medical tourism hubs, expanding private insurance penetration, and the large-scale implementation of digital health initiatives to reach dispersed populations. Countries like China and India present vast opportunities for consulting services focused on hospital capacity building, supply chain resilience, and the establishment of advanced clinical research organizations (CROs). Investment in regulatory compliance and quality assurance systems to meet international standards is a significant and growing area of consulting engagement across the APAC region, reflecting a high potential for future market penetration.

Latin America and the Middle East & Africa (MEA) are emerging markets offering increasing opportunities, though growth is often more volatile and reliant on public sector funding or foreign direct investment. In Latin America, demand is centered on privatized healthcare systems requiring financial optimization and technology implementation. In the MEA region, particularly the Gulf Cooperation Council (GCC) countries, significant government spending on establishing world-class healthcare facilities drives demand for strategic planning and large-scale project management consulting. These regions require consultants capable of navigating unique local challenges, including resource constraints and specific cultural factors influencing healthcare delivery models.

The key growth drivers are the mandated transition toward value-based care models, accelerating adoption of digital health technologies (telemedicine, AI), increasing complexity of regulatory and compliance requirements, and persistent pressure on healthcare providers to manage escalating operational costs efficiently.

The Digital Consulting segment, which includes services related to cloud migration, data analytics, cybersecurity, and telehealth strategy implementation, is anticipated to record the fastest growth due to the industry's widespread digital transformation agenda.

AI is shifting consulting focus from manual data analysis to strategic advisory regarding ethical AI deployment, risk mitigation, and the effective integration of predictive models for operational efficiency and clinical decision support, creating new high-value service lines.

Major restraints include the high initial cost of engaging premium consulting firms, significant internal resistance to organizational change within traditional healthcare entities, and paramount concerns regarding patient data security and privacy compliance (e.g., navigating HIPAA and GDPR).

North America, particularly the United States, holds the largest market share, driven by its complex reimbursement landscape, high private sector investment in healthcare IT, and persistent need for external expertise to manage regulatory changes and consolidation activities.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.