ID : MRU_ 438889 | Date : Dec, 2025 | Pages : 248 | Region : Global | Publisher : MRU

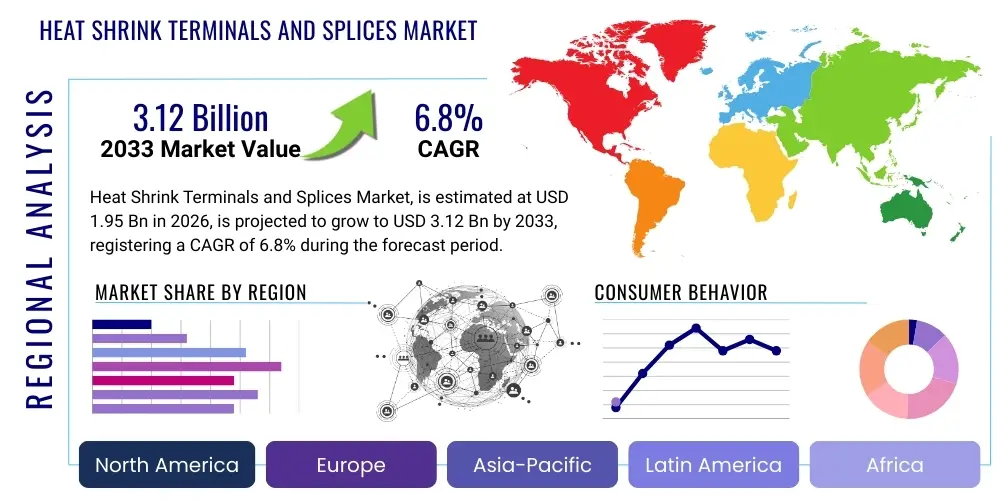

The Heat Shrink Terminals and Splices Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2026 and 2033. The market is estimated at USD 1.95 Billion in 2026 and is projected to reach USD 3.12 Billion by the end of the forecast period in 2033. This consistent growth trajectory is primarily underpinned by increasing infrastructural development across emerging economies, coupled with stringent safety standards mandating robust, environmentally sealed electrical connections in critical applications such as automotive, aerospace, and renewable energy installations. The enhanced reliability and superior insulation properties offered by heat shrink technology over traditional methods are driving adoption across various industrial sectors seeking long-term performance and reduced maintenance costs.

The market expansion is also significantly influenced by the accelerating transition towards electric vehicles (EVs) and the massive investment in smart grid infrastructure globally. Heat shrink products are integral components in high-voltage battery connection systems in EVs and are essential for protecting sensitive electronic circuits from moisture, vibration, and chemical exposure, ensuring system integrity and longevity. Furthermore, the rising deployment of decentralized energy resources, particularly solar and wind farms, necessitates durable and weather-resistant splicing and termination solutions, further solidifying the market's robust financial outlook through 2033.

The Heat Shrink Terminals and Splices Market encompasses specialized electrical components designed to provide a secure, insulated, and environmentally sealed connection between conductors. These products, typically fabricated from cross-linked polyolefin or other robust polymer materials, utilize heat to contract or shrink tightly around the wire connection, creating a permanent, waterproof, and strain-relieving seal. This superior method of protection is vital for maintaining electrical system reliability in harsh operating conditions, mitigating risks associated with moisture ingress, corrosion, abrasion, and mechanical stress, which are common failure points for unprotected connections.

Major applications for heat shrink terminals and splices span a multitude of industries, including automotive manufacturing, where they are essential for wiring harness protection; aerospace and defense, ensuring critical electronic reliability under extreme thermal and mechanical loads; telecommunications, for underground cable splicing; and industrial machinery and control systems, requiring durable connectivity. The core benefits driving their adoption include exceptional dielectric strength, rapid installation compared to molding or potting compounds, and the ability to conform tightly to irregular shapes, guaranteeing a consistent seal regardless of the conductor geometry. These advantages position heat shrink technology as a preferred solution for high-performance electrical installations where safety and longevity are paramount.

Key driving factors propelling the market include the global expansion of automotive production, particularly focusing on hybrid and electric powertrains which require highly reliable insulation for high-voltage circuits. Additionally, regulatory pressures for enhanced safety standards in construction and industrial sectors globally mandate the use of sealed connections to prevent electrical hazards. The increasing complexity of modern electronic systems, requiring miniaturization and enhanced protection, further fuels demand for high-quality, adhesive-lined heat shrink products that offer superior sealing capabilities compared to standard crimp connections alone.

The Heat Shrink Terminals and Splices Market is characterized by robust growth driven by significant advancements in material science and escalating demand from high-reliability sectors. Business trends indicate a strong move towards specialty products, specifically dual-wall, adhesive-lined terminals that offer enhanced environmental sealing, addressing the critical needs of marine, automotive under-hood, and outdoor infrastructure applications. Strategic expansions and vertical integration among key manufacturers are focusing on securing raw material supplies (polymer resins and cross-linking agents) and optimizing production efficiency to meet the rising volume demands, particularly from Asian Pacific automotive OEMs and large-scale renewable energy project developers. Furthermore, the market is experiencing consolidation, with leading players acquiring niche providers possessing advanced material technologies, aiming to bolster their product portfolios and capture specialized industry segments requiring specific flame-retardant or chemical-resistant properties.

Regional trends highlight Asia Pacific (APAC) as the fastest-growing region, fueled by massive government investments in infrastructure, rapid urbanization, and the region's dominance in global electronics and electric vehicle manufacturing. North America and Europe maintain substantial market shares due to stringent quality regulations and high adoption rates in demanding industries like aerospace and defense, alongside significant ongoing smart grid modernization projects. Segment trends reveal that the 'Splices' segment is witnessing faster growth than 'Terminals' due to the growing need for reliable cable repair and extension solutions in vast, decentralized networks such as those found in telecommunications and utility distribution systems. In terms of end-use, the Automotive sector remains the largest consumer, but the Energy and Utility sector is projected to exhibit the highest CAGR as the global energy transition accelerates, requiring durable connections for solar PV systems, wind turbines, and energy storage infrastructure.

Overall, the market is pivoting towards performance and durability, with a discernible preference for solutions that offer compliance with international standards (like UL, CSA, RoHS) and ease of installation. Manufacturers are also focusing on offering complete kits and user-friendly tools to simplify field installation and reduce application errors, thereby appealing to maintenance, repair, and overhaul (MRO) operations globally. This comprehensive focus on high-reliability, material innovation, and geographical expansion underscores a healthy and dynamically evolving market landscape poised for sustained expansion throughout the forecast period driven by global electrification mandates.

User inquiries regarding the impact of Artificial Intelligence (AI) on the Heat Shrink Terminals and Splices Market primarily center on optimizing manufacturing processes, enhancing quality assurance, and predicting equipment failure in end-use applications. Common questions include: "How can AI optimize the cross-linking process for polyolefin?", "Will AI-driven robotics replace manual heat application?", and "Can AI predict the lifespan and potential failure of a splice connection in a harsh environment?". These inquiries reflect a market expectation that AI will transition the industry from traditional quality control methods to highly precise, predictive manufacturing, enhancing the consistency and reliability of the final product while reducing waste materials and cycle times. The main concern revolves around integrating complex sensor technology into traditional manufacturing lines and the requisite data infrastructure investment needed to leverage predictive analytics effectively.

The key theme emerging from this analysis is that AI's primary influence will not be on the component itself, but on the ecosystem surrounding its production and deployment. AI and Machine Learning (ML) are being leveraged to refine polymer formulations, specifically optimizing the melt index and shrink ratio predictability during the cross-linking stage, ensuring uniformity across large batches. In the realm of quality control, computer vision systems powered by AI are automating the inspection of crimp dimensions and heat shrink uniformity post-application, significantly improving flaw detection rates compared to manual or traditional automated inspection systems. This shift towards AI-enhanced quality and efficiency ensures that heat shrink products maintain the rigorous standards required by high-stakes applications such as aerospace and medical device manufacturing.

Furthermore, within end-use sectors like utility infrastructure and aerospace, AI-driven predictive maintenance platforms are utilizing data gathered from smart sensors on critical cable systems. While the heat shrink component is passive, its successful application is critical. AI algorithms analyze environmental data (temperature fluctuations, humidity, vibration levels) alongside electrical load data to predict the degradation rate of cable insulation and connections, thus indirectly driving the demand for superior-quality, verifiable heat shrink components. This predictive capability increases the value proposition of premium, durable heat shrink products by incorporating them into a wider, AI-managed reliability framework, compelling users to invest in highest-specification sealing solutions to maximize system uptime and operational lifespan.

The dynamics of the Heat Shrink Terminals and Splices Market are shaped by a complex interplay of Drivers, Restraints, and Opportunities (DRO). The primary drivers include the escalating global demand for electrical insulation solutions in harsh environments, driven particularly by the explosive growth in the electric vehicle (EV) sector, which requires millions of reliable, sealed connections for high-voltage battery packs and wiring harnesses. Further impetus comes from significant global investments in telecommunication network expansion (5G rollouts) and modernization of aging power grid infrastructure, both of which require high-performance, weather-proof cable connectivity solutions. The enhanced safety features, including superior fire resistance and mechanical protection offered by heat shrink materials, also align perfectly with increasingly stringent industry regulations, pushing widespread adoption over alternatives like electrical tape or standard plastic caps.

However, the market faces notable restraints. Fluctuations in the cost and supply chain volatility of raw materials, primarily specialized polymer resins such as polyolefin and fluoropolymers, pose a constant challenge to profit margins and pricing stability. Furthermore, the reliance on heat application for successful installation can be a limiting factor; improper heating or the lack of specialized tooling in field installations can compromise the integrity of the seal, leading to premature connection failure, which necessitates user education and specialized training. Another restraint comes from emerging alternative technologies, such as cold shrink systems, which offer comparable environmental sealing without requiring external heat sources, particularly gaining traction in explosive or hazardous environments where heat sources are restricted.

Opportunities for market growth are vast and often intersect with global macro-economic trends. The most significant opportunity lies in the rapid development of renewable energy infrastructure, including utility-scale solar farms and offshore wind installations, which demand extremely durable and UV-resistant sealing solutions for thousands of exposed connections. There is also a substantial opportunity in developing specialized, miniaturized heat shrink components for wearable technology, medical devices, and complex consumer electronics where space constraints are critical. Impact forces, therefore, lean heavily towards the drivers, as global electrification and mandatory safety compliance in high-growth sectors continually outweigh the challenges related to material costs and competitive alternatives, ensuring a net positive market trajectory.

The Heat Shrink Terminals and Splices Market is segmented comprehensively based on product type, material, conductor size, end-use application, and geographical region, allowing for detailed market targeting and strategic decision-making. The primary segmentation by product type distinguishes between terminals (used for connection to a single point, such as a busbar or equipment stud) and splices (used to join two or more conductors permanently). Material segmentation is crucial, differentiating between standard polyolefin, high-performance fluoropolymers (like PTFE or PVDF) used in high-temperature or chemical-resistant applications, and specialized elastomers.

Further granularity is achieved through end-use application segmentation, which delineates demand across critical industries. The automotive sector dominates due to complex internal wiring needs, followed closely by the energy and utility sector, which utilizes large diameter heat shrink tubing for medium and high-voltage cable terminations and repairs. The performance criteria, such as dielectric strength, UV resistance, and operational temperature range, significantly influence the selection within each segment. The shift towards higher voltage systems in EVs and industrial machinery is compelling manufacturers to innovate specialized components that can handle increased electrical stress while maintaining superior environmental protection, driving premiumization across high-specification segments.

The value chain for the Heat Shrink Terminals and Splices Market commences with the upstream segment, dominated by raw material suppliers providing specialized polymer resins, specifically cross-linked polyolefin, PTFE, and custom fluoropolymers, along with metallic components (copper and brass) used for the terminal and splice barrels. Stability and pricing of these materials directly influence manufacturing costs. Manufacturers in the intermediate stage engage in complex processes including compounding, extrusion, cross-linking (often via electron beam or chemical methods), and final forming, coupled with the assembly of metallic terminals and the integration of specialized adhesive liners. Efficiency in this stage, particularly minimizing material waste during the high-temperature cross-linking process, is a crucial determinant of competitive advantage.

The downstream analysis focuses on the distribution channels and end-user engagement. Distribution is multifaceted, involving both direct sales to large volume Original Equipment Manufacturers (OEMs) in the automotive and aerospace sectors, and indirect sales through specialized electrical distributors, industrial supply houses, and global retail channels catering to Maintenance, Repair, and Operations (MRO) markets. Direct sales typically handle highly customized, high-specification products requiring dedicated technical support, ensuring stringent compliance. Indirect channels, conversely, focus on inventory breadth and geographical reach, serving smaller manufacturers and field service teams that require readily available standard sizes and kits for repair work and smaller-scale projects.

The effectiveness of the distribution channel is heavily reliant on technical training provided to sales representatives, ensuring end-users correctly select and apply the heat shrink products for optimal performance. Given the critical nature of the seal, educating distributors on proper crimping techniques, heat source management, and material compatibility is essential. The increasing digitalization of industrial purchasing platforms is also transforming the downstream segment, making product specification data, installation videos, and technical documentation critical elements of a successful sales strategy, ensuring the high integrity and intended benefits of the heat shrink technology are fully realized by the global end-user base.

Potential customers for heat shrink terminals and splices are broadly categorized as industries requiring high-reliability, environmentally protected electrical connections, prioritizing longevity and system uptime over initial cost savings. The primary customer base resides within the Original Equipment Manufacturers (OEMs) across the transportation and heavy industry sectors. Specifically, major automotive manufacturers and their Tier 1 suppliers are voluminous buyers, particularly those involved in producing electric and hybrid vehicles, demanding terminals and splices capable of handling high thermal cycling and corrosive environments characteristic of battery systems and engine compartments. These buyers prioritize compliance with automotive standards like ISO/TS 16949 and require detailed traceability and consistent performance.

Another significant customer segment includes Utility and Energy providers, encompassing companies managing power transmission, distribution networks, and renewable energy installations (solar, wind). These entities act as key buyers for medium and high-voltage heat shrink cable accessories used for splicing, termination, and repair of underground and overhead cables. Their purchasing decisions are driven by product longevity (often requiring decades of reliable service) and resistance to UV exposure, moisture, and extreme temperatures, ensuring grid stability. Furthermore, military and aerospace contractors form a crucial high-value segment, purchasing specialized, lightweight, flame-retardant, and fluid-resistant heat shrink products for use in aircraft wiring, defense vehicles, and satellite communication systems, where absolute reliability under stress is non-negotiable. These customers are typically the end-users/buyers of premium, specialized product variants.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 1.95 Billion |

| Market Forecast in 2033 | USD 3.12 Billion |

| Growth Rate | 6.8% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | TE Connectivity, 3M Company, ABB Ltd., HellermannTyton, Panduit, Alpha Wire, Shawcor (DSG-Canusa), Molex, Amphenol, Raychem (TE Connectivity), Kroy, Inc., Sumitomo Electric, Lapp Group, Nelco Products, Connect-It, Weidmuller, Brady Corporation, Salipt, Shinagawa Electric Wire, and Interflex. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The Heat Shrink Terminals and Splices Market is underpinned by sophisticated polymer science, with the most crucial technology being the process of irradiation cross-linking. This process, typically involving electron beams or chemical accelerators, transforms standard thermoplastic polymers (like polyolefin) into a cross-linked thermoset structure. This transformation is pivotal because it enables the material to resist melting at high temperatures and introduces the "memory effect," allowing the material to shrink back to its original, irradiated shape when heat is applied. Continuous technological refinement focuses on achieving highly precise, uniform cross-linking across various thicknesses and shapes, ensuring consistent shrink ratios and superior physical properties, which are essential for high-performance applications like aerospace harnesses and high-voltage cable insulation sleeves.

A second major technological area involves the material composition, particularly the development of dual-wall tubing incorporating specialized internal adhesives. This adhesive-lining technology utilizes co-extrusion techniques to integrate a layer of heat-activated adhesive (often polyamide or ethylene vinyl acetate based) that melts and flows during the shrinking process. This molten adhesive fills voids, creating a 100% waterproof and corrosion-proof seal around the crimp barrel and wire insulation, significantly enhancing the environmental protection capabilities beyond what single-wall tubing can achieve. Current R&D efforts are focused on developing halogen-free, flame-retardant adhesive systems that meet stringent environmental and safety standards, particularly for rail transit and enclosed space applications, without compromising the sealing performance or flexibility of the final product.

Furthermore, innovation in terminal and splice manufacturing involves optimizing the metallic component design for compatibility with heat shrink technology. Advanced crimping technology ensures that the conductor receives maximum mechanical retention while maintaining optimal electrical conductivity, preventing internal heating or resistance issues. Manufacturers are developing materials specifically tailored for high-temperature applications (up to 150°C and beyond), utilizing high-grade fluoropolymers (e.g., PVDF) that maintain their structural integrity and dielectric strength when subjected to intense thermal stress, common in high-density electronic packaging and near-engine automotive environments. This integration of advanced polymer chemistry, material engineering, and mechanical design defines the competitive edge in the modern heat shrink market.

The regional analysis of the Heat Shrink Terminals and Splices Market reveals distinct drivers and maturity levels across key geographical areas. Asia Pacific (APAC) stands out as the primary growth engine, driven by rapid industrialization, massive investments in renewable energy infrastructure (particularly in China, India, and Southeast Asia), and the dominant position of the region in global automotive and electronics manufacturing. The swift adoption of Electric Vehicles (EVs) in nations like China is creating unprecedented demand for high-reliability components, ensuring that APAC is expected to exhibit the highest Compound Annual Growth Rate (CAGR) throughout the forecast period. Local governments' focus on smart city development and extensive high-speed rail projects further solidifies the need for durable electrical connections in complex, large-scale systems.

North America maintains a highly significant market share, characterized by its mature aerospace and defense sectors, which prioritize the highest performance specifications and regulatory compliance (such as MIL-SPEC standards). The ongoing massive grid modernization efforts across the U.S. and Canada, aimed at improving resilience and integrating decentralized energy sources, are propelling demand for medium and high- voltage heat shrink cable accessories. European markets, similarly mature, are heavily influenced by stringent environmental regulations (RoHS, REACH) and strong internal standardization, leading to high adoption rates of halogen-free and eco-friendly heat shrink solutions, especially in the construction, rail, and industrial automation segments across Germany, the UK, and France.

The Middle East and Africa (MEA) region is showing promising growth, primarily fueled by infrastructural projects in the Gulf Cooperation Council (GCC) countries, including oil and gas facility maintenance and large-scale utility expansions. Latin America presents a mixed picture, with Brazil and Mexico driving demand through their expanding automotive manufacturing base and energy sector development, albeit often facing economic volatility that can impact capital expenditure on new installations. Overall, the global distribution reflects a strong correlation between regional industrial output, regulatory mandates, and investment in sustainable, complex electrical systems.

Single-wall heat shrink tubing provides electrical insulation and mechanical protection, relying on the tight fit for sealing. Dual-wall (adhesive-lined) tubing includes an inner layer of adhesive that melts upon heating, flowing to fill gaps and creating a superior, moisture-proof environmental seal critical for outdoor, marine, and underground applications, offering enhanced strain relief and corrosion resistance.

EVs utilize high-voltage battery systems which require robust insulation that can withstand high temperatures, constant vibration, and exposure to corrosive battery chemicals. Heat shrink terminals and splices offer reliable, sealed connections that prevent short circuits and catastrophic failures, ensuring the long-term safety and performance integrity of the high-voltage wiring harness, a non-negotiable requirement for passenger safety.

For applications demanding resistance to extreme temperatures (above 125°C) or harsh chemicals (fuels, hydraulic fluids), specialized fluoropolymers like PTFE (Polytetrafluoroethylene), PVDF (Polyvinylidene fluoride), and FEP (Fluorinated ethylene propylene) are commonly used. These materials maintain excellent dielectric strength and structural integrity under conditions where standard polyolefin would soften or fail.

Improper installation, typically involving insufficient or excessive heat, compromises the seal. Insufficient heat prevents the material from shrinking fully or the adhesive from flowing, leading to moisture ingress and corrosion. Excessive heat can damage the wire insulation or weaken the metallic crimp barrel. Both scenarios drastically reduce the intended lifespan and reliability, potentially causing electrical faults or system shutdowns, necessitating comprehensive installer training.

The Asia Pacific (APAC) region is projected to register the fastest CAGR due to unparalleled growth in infrastructure spending, rapid urbanization, and its global leadership in Electric Vehicle (EV) production. Government mandates supporting renewable energy projects and the expansion of massive telecommunication networks (5G) further accelerate the demand for high-volume, reliable heat shrink solutions across manufacturing and utility sectors in countries like China and India.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.