ID : MRU_ 433635 | Date : Dec, 2025 | Pages : 258 | Region : Global | Publisher : MRU

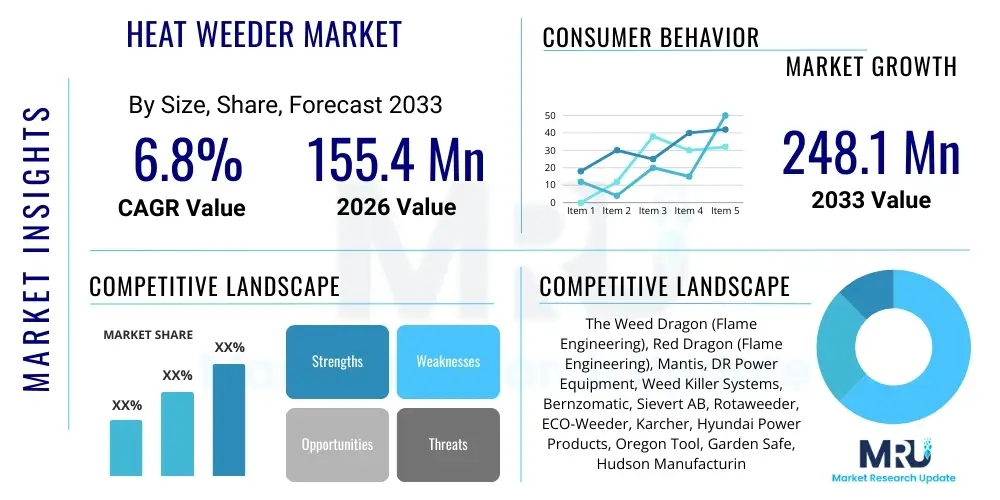

The Heat Weeder Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2026 and 2033. The market is estimated at USD 155.4 Million in 2026 and is projected to reach USD 248.1 Million by the end of the forecast period in 2033.

The Heat Weeder Market encompasses devices designed to eliminate unwanted vegetation (weeds) through the application of intense heat, typically generated by propane, butane, or electricity, which causes the rapid thermal destruction of plant cells. Unlike chemical herbicides, heat weeding offers an organic, environmentally friendly alternative for weed management, appealing strongly to consumers and commercial entities focused on sustainable practices. The market includes various product designs, ranging from small handheld torches suitable for residential use and spot weeding to large, trolley-mounted or tractor-pulled systems utilized in commercial agriculture and municipal landscaping for large-scale operations.

Key applications of heat weeders span across diverse sectors, including commercial agriculture (for row crops and vineyards), specialized horticulture (nurseries and greenhouses), public landscaping (parks, pathways, and sports fields), and utility infrastructure management (railway tracks and pavement cracks). The increasing global scrutiny on the use of glyphosate and other chemical herbicides, driven by environmental regulations and health concerns, serves as a primary catalyst for the adoption of thermal weeding solutions. Furthermore, the efficiency gains in targeted weed control and the ability to operate effectively in varying weather conditions contribute significantly to their growing appeal.

The market benefits from several intrinsic factors, including the rising consumer preference for organic food products, which mandates chemical-free farming techniques. Technological advancements leading to more fuel-efficient and ergonomically designed thermal weeders, coupled with increasing governmental support for organic farming subsidies in developed economies, are driving heightened market penetration. The major driving factors, therefore, center around environmental mandates, consumer demand for chemical-free produce, and continuous product innovation focusing on portability and operational efficiency in large-scale weed suppression.

The Heat Weeder Market is experiencing robust growth fueled by stringent environmental policies restricting chemical herbicide use and a pronounced global shift towards organic and sustainable agricultural practices. Business trends indicate a strong move towards diversification, with manufacturers investing heavily in developing electric heat weeder models to cater to urban landscaping and greenhouse operations where noise and emissions are critical factors. Commercial agricultural demand remains high for high-capacity, propane-fueled units designed for inter-row weeding, maximizing efficiency while minimizing soil disturbance. Key market participants are focusing on strategic partnerships with agricultural equipment distributors and specialized horticultural suppliers to enhance product visibility and streamline the supply chain, particularly in North America and Europe.

Regionally, Europe leads the market in terms of regulatory push and adoption rate, particularly due to the comprehensive implementation of policies promoting ecological pest control methods in countries like Germany and France. The Asia Pacific region, while currently lagging in infrastructure for specialized thermal weeding equipment, is projected to exhibit the highest growth trajectory, driven by the rapid modernization of agriculture, particularly in China and India, and increasing governmental initiatives supporting organic certification. North America maintains a mature but steady growth rate, largely underpinned by the substantial commercial landscaping sector and high residential interest in chemical-free lawn maintenance.

Segment trends reveal that the Propane Heat Weeder segment dominates the market share due to its power, portability, and suitability for large-scale outdoor applications. However, the Electric Heat Weeder segment is anticipated to register the fastest CAGR, driven by advancements in battery technology, making high-powered electric units viable for professional use. The commercial farms and municipal services end-user segments are critical revenue generators, requiring durable, industrial-grade equipment capable of continuous heavy-duty operation. Furthermore, the increasing acceptance of thermal weeding in niche applications, such as railway infrastructure maintenance and specialized crop production (e.g., asparagus, onions), contributes significantly to overall segment expansion.

Common user questions regarding the impact of AI on the Heat Weeder Market primarily revolve around how automation and precision agriculture technologies can optimize thermal weeding efficiency. Users frequently ask about the integration of computer vision systems for selective weeding, the viability of autonomous thermal weeding robots, and how predictive analytics can determine optimal weeding schedules based on real-time environmental data and weed growth patterns. Key themes center on reducing operational costs, minimizing fuel consumption in propane models through targeted application, and ensuring that AI-driven solutions maintain the core benefit of chemical-free weed control while achieving parity or superiority in efficiency compared to conventional methods. Users are concerned about the high initial investment required for such sophisticated systems and the necessary regulatory framework for deploying autonomous agricultural machinery.

The convergence of Artificial Intelligence and thermal weeding technology is poised to revolutionize the precision and scalability of these chemical-free methods. AI-powered thermal weeders utilize advanced computer vision and machine learning algorithms to accurately distinguish between cash crops and weeds, allowing for highly localized and instantaneous application of heat. This targeted approach dramatically reduces the energy expenditure—especially crucial for propane and electric units—while ensuring minimal thermal stress or damage to desirable plants. The integration moves the technology beyond broad application towards true selective weed control, overcoming one of the historical limitations of purely manual or generic thermal systems.

Furthermore, AI algorithms are crucial for optimizing fleet management and predictive maintenance for commercial thermal weeding operations. By analyzing telemetry data, fuel consumption rates, and equipment stress points, AI systems can schedule maintenance preemptively, minimizing downtime during peak growing seasons. The deployment of fully autonomous heat weeding robots, guided by GPS, LiDAR, and AI decision-making processes, will be a significant future trend, particularly in large-scale organic farms. These autonomous units can operate 24/7, offering substantial labor savings and consistent weed management quality, ultimately solidifying the competitive position of thermal weeding against mechanized or chemical alternatives.

The dynamics of the Heat Weeder Market are shaped by a complex interplay of Drivers, Restraints, and Opportunities, which collectively constitute the Impact Forces influencing industry trajectory. The primary driver is the global regulatory shift away from conventional chemical pesticides, exemplified by increasing bans or severe restrictions on substances like glyphosate across major economies, thereby creating an immediate and substantial need for viable, non-chemical alternatives. This driver is powerfully reinforced by escalating consumer demand for organic, residue-free produce, compelling agricultural producers to adopt sustainable weeding methods. The combination of environmental stewardship mandates and shifting consumer preferences forms a strong foundational demand structure for thermal weeding solutions.

However, the market faces significant restraints, notably the relatively high initial capital investment required for professional-grade thermal weeding equipment compared to conventional sprayers. Furthermore, the operational speed of thermal weeding can be slower than chemical application in very large fields, potentially limiting its adoption in highly commoditized, conventional farming operations focused purely on speed and cost minimization. A persistent concern, particularly in regions prone to drought or extreme heat, is the perceived fire risk associated with open-flame systems, necessitating stringent safety protocols and specialized training for operators, which acts as a practical barrier to entry for some smaller users.

Opportunities for growth are abundant, particularly through technological enhancements, such as developing high-capacity, rechargeable electric thermal weeders that eliminate fuel handling logistics and fire risk, making them ideal for urban and indoor farming environments. Another significant opportunity lies in expanding market penetration into municipal services and infrastructure maintenance (roads, railways), where preventing chemical runoff is paramount. The increasing focus on integrated pest management (IPM) strategies also positions heat weeding as a valuable, rotational tool alongside mechanical and biological controls. The overall impact forces are strongly positive, driven by the irreversible global trend toward sustainability, though manufacturers must proactively address cost and operational efficiency restraints through innovation to fully capitalize on the market potential.

The Heat Weeder Market is segmented based on Type, Application, End-User, and Distribution Channel, reflecting the diverse needs of various stakeholders ranging from residential gardeners to large-scale commercial agricultural enterprises. Analyzing these segments provides crucial insights into product development focus areas and regional consumption patterns. The segmentation by Type, distinguishing between propane, butane, and electric models, is particularly important as it dictates performance characteristics, operational cost structures, and environmental impact. Propane models currently dominate due to their power and durability for outdoor applications, while electric models are rapidly gaining traction in controlled environment agriculture and residential markets due to zero localized emissions and ease of use.

Application-wise, the market sees robust demand from traditional agriculture, driven by the need for chemical-free inter-row weeding in organic crops. Concurrently, the horticulture and landscaping segments are crucial, focusing on precision tools for delicate tasks around ornamental plants and maintaining weed-free public spaces without chemical leaching. The End-User analysis clearly delineates the demand profiles, with Commercial Farms prioritizing high throughput and durability, while Residential Users prioritize safety, ergonomics, and accessibility. Understanding these varied demands allows manufacturers to tailor product portfolios effectively, ensuring that both industrial-grade solutions and consumer-friendly devices are adequately represented in the market offering.

Furthermore, the segmentation by Distribution Channel highlights the evolving sales landscape. Traditional hardware stores and specialized agricultural equipment dealers (Offline Retail) remain critical for professional users who require consultation and maintenance services. However, the rise of e-commerce (Online Retail) provides extensive reach for smaller, consumer-focused models, offering competitive pricing and convenience, which is increasingly influencing purchasing decisions, especially among residential and small landscaping businesses seeking immediate product access and comparative reviews.

The Value Chain for the Heat Weeder Market begins with upstream activities involving the sourcing of core components, primarily specialized metals for burners and nozzles, advanced heating elements (for electric models), and high-pressure regulators and hoses for propane systems. Critical suppliers include metal fabricators, industrial gas component manufacturers, and battery technology providers. Efficiency in this stage is paramount, as the durability and safety of the final product depend heavily on the quality and certification of these specialized inputs. Manufacturers strive for vertical integration or long-term contracts with reliable suppliers to mitigate supply chain disruptions and ensure cost-effective component acquisition, particularly for high-volume units.

The middle segment focuses on manufacturing, assembly, and quality assurance. This stage involves complex engineering to ensure optimal combustion efficiency (in propane models) and ergonomic design. Companies often invest heavily in research and development to enhance fuel efficiency, reduce weight, and improve operator safety features, such as integrated ignition systems and flame control mechanisms. After manufacturing, the products move through the distribution channels. Direct distribution is common for high-value, industrial-grade equipment sold directly to large commercial farms or municipal clients, often involving specialized training and maintenance contracts.

Downstream activities predominantly involve the complex distribution network, which is bifurcated into indirect and direct channels. Indirect distribution utilizes online retailers, mass-market hardware stores, and regional agricultural equipment dealers, catering mainly to residential and small to medium-sized enterprises (SMEs). This indirect network requires robust logistics and inventory management. The final stage involves end-user utilization and post-sales support, including warranty services and spare parts availability, which are vital for maintaining customer satisfaction and brand loyalty, especially given the rugged nature of the equipment and its use in harsh outdoor environments.

The Heat Weeder Market primarily targets several distinct groups of end-users who share a common need for effective, non-chemical weed control solutions, driven either by regulatory requirements, consumer demand, or environmental ethos. The most significant segment comprises Commercial Farms, particularly those engaged in organic production of high-value crops (e.g., vegetables, fruits, herbs) where chemical residue is strictly prohibited and thermal weeding provides an excellent alternative to labor-intensive manual weeding. These buyers prioritize high-capacity, durable, and tractor-mountable solutions capable of covering extensive acreage efficiently and reliably during critical growth phases.

Another crucial customer base includes Government Agencies and Municipalities responsible for maintaining public areas such as city parks, sidewalks, historical sites, and recreational facilities. These entities are increasingly mandated to minimize or eliminate chemical usage in public spaces to protect public health and local ecosystems, making thermal weeders an indispensable tool for urban maintenance. Their purchasing criteria often emphasize low noise levels (favoring electric models) and certified safety standards for public operation, coupled with longevity and low maintenance requirements for fleet management.

Furthermore, the residential market represents a vast pool of potential customers. These are typically environmentally conscious homeowners and small-plot gardeners seeking to manage weeds in their gardens, patios, and driveways without resorting to chemicals. For this segment, the primary purchasing drivers are ease of use, compact design, and affordability. Specialized buyers, such as Professional Landscapers, Horticultural Nurseries, and even Infrastructure Operators (like railway maintenance crews), also constitute significant customers, requiring robust, task-specific thermal tools to maintain complex or sensitive environments efficiently and sustainably.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 155.4 Million |

| Market Forecast in 2033 | USD 248.1 Million |

| Growth Rate | 6.8% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | The Weed Dragon (Flame Engineering), Red Dragon (Flame Engineering), Mantis, DR Power Equipment, Weed Killer Systems, Bernzomatic, Sievert AB, Rotaweeder, ECO-Weeder, Karcher, Hyundai Power Products, Oregon Tool, Garden Safe, Hudson Manufacturing, Matabi, Berthoud, Solo Sprayers, Gloria Haus und Garten, Agrifac Machinery, Weedtechnics |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological landscape of the Heat Weeder Market is defined by continuous innovation focused on enhancing safety, efficiency, and environmental compatibility. The core technologies revolve around combustion engineering and heat transfer mechanics. For propane-based systems, recent advancements focus on optimizing burner design to achieve higher temperatures with lower fuel consumption, moving towards highly efficient, enclosed-flame burners that minimize heat dissipation and improve operational safety by containing the flame. Furthermore, the integration of advanced pressure regulation systems ensures consistent heat output regardless of ambient temperature or fuel tank level, crucial for uniform weed control across large fields. Manufacturers are also incorporating lightweight, durable materials to improve the ergonomics of handheld units and the maneuverability of trolley-mounted systems.

A significant technological shift is occurring in the electric segment, driven by breakthroughs in Lithium-ion battery technology. Modern electric heat weeders now utilize high-capacity, high-density battery packs capable of delivering the sustained power necessary to generate effective thermal shock, making them viable for commercial landscaping tasks traditionally dominated by gas models. These electric units feature advanced temperature controls and rapid heat-up times, offering precise control over the thermal application. The elimination of fuel handling and exhaust emissions makes electric models the preferred technology for controlled environments like greenhouses, vertical farms, and densely populated urban areas where air quality and noise pollution are key concerns.

Looking forward, the technology landscape is increasingly integrating smart and automated features. This includes the use of sensor technology (like infrared sensors) to confirm the optimal application temperature and duration for maximum efficacy. Crucially, the deployment of AI and computer vision systems enables selective, robotic thermal weeding, representing the zenith of precision agriculture technology in this domain. These systems utilize sophisticated image recognition to target weeds only, dramatically increasing the efficiency of the application and marking the next evolution from broadcast or inter-row thermal application to individual plant treatment, thereby maximizing resource utilization and operational throughput.

The geographical analysis of the Heat Weeder Market reveals distinct adoption patterns and growth drivers across major regions, heavily influenced by local agricultural practices, regulatory environments, and consumer attitudes towards organic farming. Europe currently holds the dominant market share, driven primarily by the strong regulatory framework promoting sustainable agriculture and extensive governmental subsidies for non-chemical weed control methods. Countries such as Germany, the Netherlands, and France have been pioneers in restricting chemical herbicide usage, creating a high immediate demand for sophisticated thermal weeding solutions in both commercial farming and municipal infrastructure maintenance. The European market focuses heavily on technological refinement, favoring electric and high-efficiency propane models that comply with strict emission and safety standards. The mature organic sector across Western Europe guarantees sustained investment in these ecological tools.

North America represents a mature market characterized by robust demand from both the large-scale commercial agricultural sector, particularly organic growers in California and the Midwest, and a highly active residential landscaping market. The adoption rate is steady, supported by state-level regulations limiting chemical use in parks and schools, such as those implemented in parts of Canada and the Northeastern US. The region exhibits high demand for durable, heavy-duty propane units optimized for efficiency across large row crops, alongside a burgeoning interest in electric, consumer-grade models for suburban use. Market growth here is closely tied to the expansion of organic acreage and the professionalization of landscaping services seeking chemical-free competitive advantages.

The Asia Pacific (APAC) region is projected to be the fastest-growing market over the forecast period. Although currently facing challenges related to initial equipment cost and fragmented landholdings, the region is undergoing rapid agricultural modernization. Governments in nations like China, India, and Australia are increasingly prioritizing food safety, environmental protection, and exporting organic produce, which necessitates the shift away from broad-spectrum chemical treatments. The market potential is immense, especially as local manufacturers begin to produce localized, affordable versions of heat weeding technology. Initial adoption is strong in high-value, protected horticulture and specialized cash crops, providing a gateway for wider adoption across staple crops in the coming decade.

Latin America and the Middle East & Africa (MEA) regions currently hold smaller market shares but offer significant long-term growth potential. In Latin America, countries such as Brazil and Argentina, major global agricultural exporters, are beginning to face environmental pressure and consumer scrutiny regarding pesticide use, prompting organic producers to explore thermal alternatives, particularly in coffee, sugar cane, and specialty vegetable production. The MEA region is characterized by varied climates and agricultural scales. Growth is nascent but expected to increase, particularly in high-income Gulf countries focusing on controlled environment agriculture (CEA) and sustainable urban landscaping, where electric heat weeders offer a precise, climate-independent solution. Furthermore, development aid programs promoting sustainable farming practices in certain African nations are beginning to introduce these non-chemical tools to smallholder farmers.

Heat weeders offer several key advantages: they are a 100% chemical-free solution, eliminating concerns about pesticide residue on crops and environmental contamination. They effectively target weeds resistant to chemical treatments and require no withdrawal period before harvest. This makes them essential for certified organic farming operations that must adhere to strict non-chemical standards, aligning with increasing consumer preference for sustainable and residue-free food products globally.

While the initial purchase price of high-capacity electric heat weeders may be higher due to advanced battery technology, their long-term operating costs are generally lower. Electric models eliminate the recurring expense of purchasing and transporting propane tanks, and electricity is typically a cheaper fuel source per unit of energy output than propane. Furthermore, electric systems often require less maintenance, reducing downtime and servicing costs, although battery replacement cycles must be factored into the total cost of ownership (TCO).

The primary safety consideration for propane heat weeders is minimizing the risk of accidental fires, particularly when operating near dry grasses, mulch, or flammable structures. Operators must ensure adequate clearance, maintain equipment in excellent working condition (checking hoses and connections for leaks), and have appropriate fire suppression tools readily available. Proper training regarding flame control and operation during periods of high fire danger is essential, mitigating risks associated with high temperatures and open flames required for effective thermal weeding.

Heat weeders are highly effective against annual weeds and the top growth of perennial weeds by instantly rupturing the plant's cell structure (thermal shock). However, deeply rooted perennial weeds may require multiple treatments, as the heat often does not penetrate sufficiently to kill the entire root system in a single pass. For perennials, repeated applications are necessary to deplete the root reserves over time, making integrated pest management strategies, combining heat with other controls, the most effective long-term solution.

Automation, particularly through AI-powered robotic heat weeder systems, is critical for future market growth by addressing the key limitation of operational speed. Autonomous thermal weeders equipped with computer vision can navigate fields, selectively identify, and precisely apply heat to weeds without human intervention, leading to significant reductions in labor costs and greatly increased operational efficiency. This integration positions thermal weeding as a scalable and economically competitive alternative to conventional high-speed chemical spraying methods for large commercial organic farms.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.