ID : MRU_ 434582 | Date : Dec, 2025 | Pages : 253 | Region : Global | Publisher : MRU

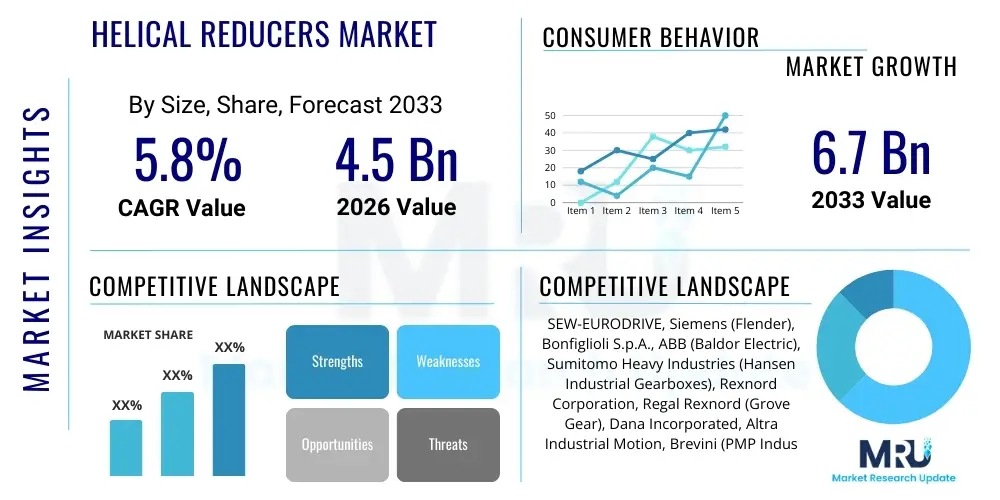

The Helical Reducers Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 5.8% between 2026 and 2033. The market is estimated at USD 4.5 Billion in 2026 and is projected to reach USD 6.7 Billion by the end of the forecast period in 2033.

Helical reducers, integral components of power transmission systems, are mechanical devices designed to decrease the input rotational speed while simultaneously increasing the output torque. These reducers utilize helical gears, which feature teeth cut at an angle to the gear axis. This angled design allows for greater tooth contact area and gradual meshing, resulting in significantly smoother, quieter operation, and superior load-carrying capacity compared to traditional spur gears. The high efficiency, reliability, and compact nature of helical reducers make them indispensable across various heavy and precision industries, driving demand in sectors prioritizing operational stability and energy efficiency.

The primary function of helical reducers is to optimize the energy input from a motor to meet the specific speed and torque requirements of machinery. Their inherent design provides numerous benefits, including reduced vibration, longer operational life, and minimal maintenance needs, translating directly into lower total cost of ownership (TCO) for industrial end-users. Key applications span a wide industrial spectrum, including sophisticated manufacturing environments, bulk material handling in mining and ports, fluid movement in chemical processing, and precise motion control in robotics and machine tools. The demand is intrinsically linked to global industrialization rates and capital expenditure in infrastructure projects.

Driving factors propelling market expansion include the rapid implementation of Industry 4.0 principles, necessitating precise and durable power transmission solutions. Furthermore, stringent global regulations promoting energy conservation are accelerating the adoption of high-efficiency helical gearboxes over less efficient alternatives. The continuous trend toward automation and miniaturization in manufacturing requires compact, high-torque density reducers, which helical designs are uniquely positioned to provide, ensuring sustained market growth throughout the forecast period. Expansion in construction, logistics, and automotive manufacturing heavily influences the procurement cycles for these critical components.

The Helical Reducers Market is characterized by robust growth, driven primarily by accelerating industrial automation trends globally and significant capital investments in modernizing aging infrastructure, particularly across Asia Pacific (APAC). Business trends indicate a strong focus on modular designs and customization, allowing manufacturers to serve a diverse range of application-specific needs, particularly in high-precision sectors like aerospace and robotics. Key players are increasingly engaging in strategic mergers and acquisitions to consolidate market share, enhance technological capabilities, and expand their regional distribution networks. Sustainability is emerging as a critical competitive factor, with companies investing in R&D to produce reducers utilizing lighter, more durable materials that also boast enhanced energy efficiency ratings.

Regional trends highlight APAC as the dominant and fastest-growing market, fuelled by massive industrial expansion, particularly in China, India, and Southeast Asian nations, where urbanization and manufacturing capacity are rapidly scaling. North America and Europe maintain a mature market status, characterized by demand for high-end, IoT-enabled, smart reducers that support predictive maintenance strategies within advanced manufacturing facilities. Government initiatives supporting infrastructure development, such as modernized railway systems and renewable energy projects (wind and solar), are also significantly impacting regional procurement volumes, favoring heavy-duty, reliable helical solutions.

Segmentation trends indicate that the market for parallel shaft helical reducers currently holds the largest revenue share, owing to their versatility and widespread use in high-power applications, including mining and heavy machinery. However, the market for bevel helical reducers is anticipated to demonstrate the highest Compound Annual Growth Rate (CAGR), driven by their compact geometry and ability to transmit power at right angles, making them ideal for space-constrained industrial setups and material handling systems. Furthermore, there is a pronounced shift towards high-torque capacity reducers, reflecting the increasing size and power requirements of modern industrial equipment across heavy-duty sectors.

Common user inquiries concerning the influence of Artificial Intelligence (AI) on the Helical Reducers Market typically revolve around how AI can enhance the operational lifespan and reduce downtime of gear systems, given their mechanical nature and susceptibility to wear. Users are keenly interested in predictive maintenance frameworks enabled by AI, wanting to understand if sensor data coupled with machine learning algorithms can accurately forecast component failure before it occurs, thereby optimizing maintenance schedules and inventory management for spare parts. Furthermore, there is growing curiosity regarding AI's role in the design and material selection process, particularly concerning the automated optimization of gear geometry for maximum efficiency and reduced noise, addressing long-standing challenges in mechanical engineering. Key expectations center on achieving unprecedented levels of efficiency and reliability through intelligent monitoring and adaptive operational controls.

The Helical Reducers Market is fundamentally shaped by several distinct dynamics encompassing Drivers, Restraints, Opportunities, and broader Impact Forces. Primary drivers include the global push towards industrial automation, particularly manifested in the adoption of high-performance machinery across discrete manufacturing and process industries. The necessity for high-efficiency power transmission systems that minimize energy loss aligns perfectly with global energy conservation mandates, ensuring steady demand for helical units. Concurrently, large-scale infrastructure projects in developing economies, focusing on modernizing transportation and utility sectors, necessitate durable and high-torque gear solutions, further fueling market expansion. These drivers create a foundational demand structure impervious to minor economic fluctuations, prioritizing long-term operational resilience.

However, the market faces significant restraints, notably the relatively high initial capital investment required for high-precision, helical gearboxes compared to simpler speed reducers. Furthermore, the complexity involved in the precise manufacturing and demanding maintenance schedules for larger, multi-stage helical units can deter smaller enterprises. The cyclical nature of capital expenditure in heavy industries also introduces volatility; economic downturns often lead to delayed investments in new machinery, temporarily impacting market growth rates. Overcoming these restraints involves demonstrating the superior Total Cost of Ownership (TCO) derived from enhanced longevity and efficiency.

Opportunities abound through technological advancements, including the development of modular and compact helical designs suitable for integration into robotic systems and mobile equipment. The proliferation of IoT and sensing technology offers a lucrative avenue for market players to differentiate their products by offering 'smart' helical reducers capable of seamless integration into digital factory ecosystems. Impact forces influencing the market trajectory include rapid technological change, particularly in additive manufacturing (3D printing) of custom gear components, and intensifying competitive pressures leading to pricing consolidation. Regulatory standards related to noise levels, efficiency ratings (like IE efficiency classes), and safety protocols also continuously shape product design and manufacturing processes globally.

The Helical Reducers Market is extensively segmented based on several key operational and structural parameters, allowing for detailed analysis of demand patterns across different industrial verticals. The core segmentation often involves classifying reducers based on the axis arrangement (parallel shaft, bevel helical, or worm helical), which dictates the application environment and space constraints. Further differentiation is achieved through power output (low, medium, high), torque capacity, and the number of reduction stages (single, double, or triple), directly correlating to the machinery's operational requirements. This granular approach is vital for market players to tailor their product portfolios accurately to meet the exacting specifications of end-user industries such as mining, construction, food & beverage, and power generation, ensuring targeted marketing and distribution strategies.

The value chain for the Helical Reducers Market begins with upstream activities focused on securing high-quality raw materials, predominantly steel alloys (e.g., chrome-nickel steel) essential for gear and shaft manufacturing, and high-grade cast iron or aluminum for the housing. This stage demands rigorous quality control, as the mechanical properties of the final product depend heavily on the metallurgy. Key activities in the upstream sector include forging, casting, and precision machining of blank gear components. Efficient material procurement and hedging against volatility in commodity prices are critical factors determining the overall cost structure and competitive positioning of manufacturers.

The midstream phase encompasses the core manufacturing processes: gear cutting (hobbing, shaping), heat treatment (carburizing, nitriding) to enhance surface hardness and wear resistance, and highly precise gear grinding to achieve the required tolerance and efficiency levels. Assembly, rigorous quality testing, and certification (e.g., ISO, AGMA standards) follow. Manufacturers often invest heavily in advanced CNC machinery and clean room assembly environments to ensure the superior reliability and low noise characteristics expected of helical reducers. Efficient logistics and optimized manufacturing footprints are essential in this capital-intensive phase.

Downstream activities involve the distribution channel, which utilizes both direct sales to large Original Equipment Manufacturers (OEMs) and indirect sales through a network of specialized distributors and authorized service providers focusing on the aftermarket segment. Direct channels are preferred for high-volume, custom orders, especially in heavy industries. Indirect channels leverage regional distributors for reach, immediate availability of standard units, and local technical support. End-users (potential customers) are diverse industrial sectors such as mining, construction, and power generation, where performance, longevity, and post-sales service are paramount considerations when selecting a supplier.

Potential customers for helical reducers span the entire global industrial landscape, characterized by operations requiring robust, efficient, and precise control over speed and torque. The primary end-users are large-scale industrial operators and equipment manufacturers (OEMs) who integrate these components into their final products. The construction and infrastructure sectors represent a massive purchasing base, utilizing helical reducers in heavy machinery like mixers, cranes, and concrete pumps, where high load capacity and reliability are non-negotiable. Similarly, the global material handling industry, encompassing vast networks of conveyor systems, automated storage and retrieval systems (AS/RS), and hoisting equipment in ports and warehouses, relies heavily on helical reduction units for operational efficiency and throughput.

The mining and metallurgy sector is a cornerstone customer group, consistently demanding the largest and most durable reducers for applications such as crushers, ball mills, and excavators, operating under extreme conditions of dust, heat, and continuous heavy load. The sheer scale and criticality of operations in mining dictate a preference for premium, high-torque capacity reducers, often driving customized solution requirements. Furthermore, the renewable energy sector, particularly wind power generation, requires specialized helical reducers for yaw and pitch control mechanisms, ensuring precise alignment of turbine blades. This customer segment is experiencing accelerated growth, driven by global climate mandates and investments in green energy infrastructure.

The food and beverage industry, pharmaceutical manufacturing, and the packaging sector also constitute significant customer bases, albeit often requiring smaller, highly hygienic, and often stainless steel-housed helical reducers. These applications prioritize smooth operation, washdown capabilities, and compliance with stringent sanitation standards. The common thread among all potential customers is the need for dependable mechanical power transmission that minimizes energy consumption and maximizes operational uptime, making the selection of a helical reducer supplier a strategic decision based on reliability, efficiency ratings, and long-term service capability.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 4.5 Billion |

| Market Forecast in 2033 | USD 6.7 Billion |

| Growth Rate | 5.8% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | SEW-EURODRIVE, Siemens (Flender), Bonfiglioli S.p.A., ABB (Baldor Electric), Sumitomo Heavy Industries (Hansen Industrial Gearboxes), Rexnord Corporation, Regal Rexnord (Grove Gear), Dana Incorporated, Altra Industrial Motion, Brevini (PMP Industries), China High Speed Transmission Equipment Group (CHSTE), Tsubakimoto Chain Co., Nidec Corporation, David Brown Santasalo, Hangzhou Gearbox Group Co., Ltd., Elecon Engineering, Nord Drivesystems, Radicon (A Gearless & Hansen Company), Watt Drive (WEG Group), STM Spa |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological landscape of the Helical Reducers Market is rapidly evolving, driven by the demand for higher power density, quieter operation, and seamless digital integration. One of the most significant advancements is the proliferation of modular design principles. Modular reducers allow for easier customization, faster assembly, and reduced inventory holding costs for manufacturers and distributors. By standardizing input and output components, companies can quickly configure gearboxes to meet specific torque, speed, and mounting requirements across varied applications, dramatically improving time-to-market for end-users seeking specialized solutions.

Another crucial technological focus is on materials science and manufacturing precision. The adoption of advanced alloy steels, combined with sophisticated thermal treatments such as vacuum carburizing, is leading to gears with superior hardness, reduced wear, and extended service life, enabling higher torque transmission in smaller, lighter housings. Precision grinding techniques, often controlled by multi-axis CNC machines, are essential for minimizing tooth profile errors, which directly reduces operational noise and vibration. Furthermore, the development of specialized synthetic lubricants tailored for helical gears contributes significantly to maximizing efficiency and reducing thermal stress during high-speed, heavy-load operation.

The integration of Information Technology (IT) and Operational Technology (OT) is transforming helical reducers into 'smart' components. This involves embedding various sensors (vibration, temperature, oil quality, acoustic emission) within the gearbox casing. These sensors collect real-time operational data, which is processed via local controllers and often uploaded to cloud-based analytical platforms. This capability supports advanced predictive maintenance strategies, enabling operators to move away from time-based maintenance to condition-based maintenance, optimizing operational expenditure and virtually eliminating catastrophic failures. This convergence of mechanical engineering and digital technology is defining the next generation of power transmission systems.

APAC stands as the dominant market for helical reducers globally, exhibiting the highest growth rate during the forecast period. This dominance is intrinsically linked to the unprecedented scale of industrialization and infrastructure development across key economies such as China, India, and Indonesia. These nations are massive hubs for heavy manufacturing, including automotive, steel, cement, and bulk material handling, all of which rely heavily on high-torque, durable helical reducers. Government initiatives supporting massive investments in railway networks, ports, and smart city development further amplify the demand. Local manufacturers are rapidly gaining ground by focusing on cost-effective, high-volume production, while international players are expanding their manufacturing and distribution footprints within the region to capitalize on the soaring demand from OEMs.

The burgeoning renewable energy sector, particularly wind power installation in offshore and onshore sites in countries like China and India, requires robust helical gearboxes for turbine control systems, contributing significantly to market volume. Furthermore, the rapid adoption of automation and robotic systems in Southeast Asian manufacturing facilities, driven by rising labor costs and the push for higher quality output, fuels the demand for medium and high-precision helical reducers. Supply chain resilience and localized support services are critical competitive differentiators in this highly active and price-sensitive market environment.

North America represents a mature, high-value market characterized by demand for technologically advanced, high-efficiency, and smart helical reducers. The market growth here is less driven by capacity expansion and more by the replacement of older, less efficient units and the adoption of Industry 4.0 principles. Key sectors driving demand include oil and gas extraction, aerospace manufacturing, and automated warehousing and logistics. American manufacturers and end-users prioritize long-term reliability, minimal total cost of ownership (TCO), and advanced diagnostics capabilities, fostering a market environment conducive to premium, sensor-integrated products.

The U.S. remains the largest contributor to regional revenue, with significant expenditure on modernizing manufacturing infrastructure and increasing automation levels in domestic industries. The stringent regulatory environment regarding energy efficiency mandates and worker safety also pushes continuous product improvement, favoring helical designs optimized for reduced noise and vibration. Maintenance and service contracts form a significant revenue stream for suppliers in this region, emphasizing the critical role of strong local technical support and efficient spare parts supply.

The European market is defined by a strong emphasis on precision engineering, compliance with strict environmental regulations, and a high concentration of specialized machinery manufacturers (OEMs). Germany, Italy, and the UK are core markets, focusing on advanced robotics, machine tools, and process industry applications (chemical, food and beverage). European demand is significantly influenced by the European Union’s energy efficiency directives, making high-efficiency helical gearboxes (often exceeding IE3 standards) mandatory for new installations.

Innovation is key in Europe, with substantial R&D investments focused on lightweight materials, modular architecture, and cyber-physical system integration. Manufacturers often collaborate closely with specialized OEMs to develop custom solutions for niche applications, ensuring products meet the stringent performance requirements of highly automated production lines. While the industrial base is mature, ongoing digitalization of manufacturing processes (Smart Factory initiatives) provides sustained opportunities for sophisticated helical reducer technologies, especially those supporting remote monitoring and predictive diagnostics across complex European supply chains.

The LAMEA region exhibits promising growth potential, driven primarily by large-scale commodity production and significant government investment in energy and transportation infrastructure. In Latin America, countries like Brazil and Mexico drive demand through mining, agriculture, and automotive production, requiring heavy-duty and robust helical reducers capable of operating reliably in harsh environments. The market often favors cost-effective and rugged designs over high-end smart features, although the trend towards automation is gradually shifting procurement strategies.

The Middle East market is dominated by the oil and gas sector and massive construction projects linked to national diversification strategies (e.g., Vision 2030 in Saudi Arabia). Helical reducers are vital in pumping stations, drilling rigs, and port logistics. Africa’s growth is anchored in mining and raw material processing, where reliability and low-maintenance solutions are highly valued due to operational challenges and dispersed industrial locations. These regions often rely heavily on international suppliers, necessitating strong partnerships with local distributors to ensure adequate technical support and service coverage across diverse geographies.

Helical reducers offer several distinct advantages, notably smoother and quieter operation due to the gradual meshing of angled teeth, enabling simultaneous contact between multiple teeth. This characteristic also provides superior load-carrying capacity and higher torque density, resulting in greater operational efficiency (typically 95-98%) and extended lifespan compared to less efficient alternatives like worm gear drives.

Industry 4.0 drives the integration of smart technologies, transforming reducers into cyber-physical systems. Modern helical reducers are often equipped with embedded sensors for vibration, temperature, and lubricant analysis, enabling predictive maintenance algorithms. This connectivity allows for real-time performance monitoring and optimized operational scheduling, reducing unplanned downtime and improving overall equipment effectiveness (OEE) in automated factories.

The material handling industry, including conveyors, cranes, hoists, and automated logistics systems, currently accounts for the largest share of the market. Helical reducers are critical in these applications due to their requirement for high reliability under continuous load, robust torque transmission, and precise speed control necessary for moving heavy or delicate items efficiently across large industrial facilities and ports.

The current trend focuses on high-strength, lightweight materials. For gear components, manufacturers utilize advanced alloy steels coupled with precise heat treatments (e.g., carbonitriding) to maximize hardness and durability. For casings, there is a growing adoption of lighter, high-grade cast iron or sometimes aluminum alloys, particularly in smaller units, to reduce overall machine weight while maintaining optimal rigidity and heat dissipation properties.

TCO calculation must extend beyond the initial purchase price to include factors such as energy efficiency over the lifespan (high efficiency leads to significant long-term savings), maintenance frequency and cost (related to reliability and design complexity), cost of downtime (prevented through predictive maintenance), and the lifespan of critical components like seals and bearings. High-quality, high-efficiency helical reducers often demonstrate a much lower TCO despite a higher initial investment.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.