ID : MRU_ 436628 | Date : Dec, 2025 | Pages : 257 | Region : Global | Publisher : MRU

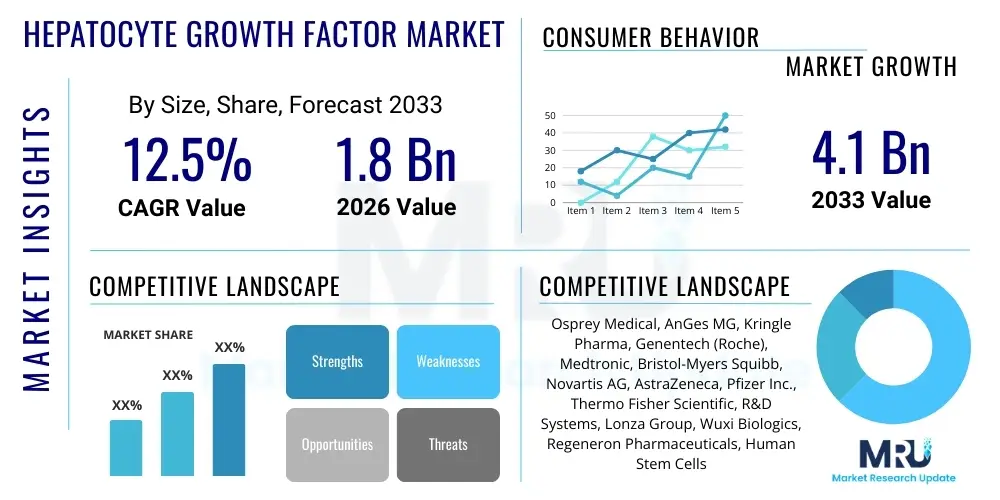

The Hepatocyte Growth Factor Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 12.5% between 2026 and 2033. The market is estimated at USD 1.8 Billion in 2026 and is projected to reach USD 4.1 Billion by the end of the forecast period in 2033.

The Hepatocyte Growth Factor (HGF) Market encompasses the research, development, production, and commercialization of therapeutic agents utilizing HGF or its analogues for treating various chronic and acute conditions. HGF, also known as Scatter Factor (SF), is a pleiotropic cytokine that primarily acts on epithelial, endothelial, and hematopoietic cells. Its biological function is mediated through the c-Met receptor, playing crucial roles in embryonic development, tissue regeneration, angiogenesis, and anti-fibrotic processes. This inherent capability to stimulate cellular proliferation and migration positions HGF as a critical target for regenerative medicine, particularly in conditions involving severe tissue damage, such as critical limb ischemia, myocardial infarction, and chronic kidney disease.

The market growth is fundamentally driven by the increasing global prevalence of chronic diseases, particularly cardiovascular disorders and diabetes, which lead to significant tissue and organ damage. HGF therapies offer a promising alternative to conventional treatments by focusing on restoring native physiological function rather than merely managing symptoms. Current commercial products and pipeline candidates span several therapeutic modalities, including recombinant HGF protein injections and gene therapies designed to enhance endogenous HGF expression at the site of injury. The product description of therapeutic HGF emphasizes its multifaceted regenerative capabilities—acting as a potent mitogen for hepatocytes and certain epithelial cells, and exhibiting powerful anti-apoptotic and anti-inflammatory effects.

Major applications of HGF therapies are concentrated within cardiology (for treating ischemic heart failure and peripheral artery disease), nephrology (addressing renal fibrosis and acute kidney injury), and dermatological wound healing (especially in non-healing diabetic ulcers). The primary benefits derived from successful HGF application include enhanced vascularization, accelerated tissue repair, reduction of fibrotic scarring, and improved overall organ function. Driving factors propelling this market include advancements in gene delivery systems, increased investment in biotechnology R&D focused on regenerative biology, supportive regulatory frameworks for orphan drug designations in regenerative medicine, and growing evidence from late-stage clinical trials confirming HGF's efficacy in achieving clinical endpoints that conventional therapies often fail to address.

The Hepatocyte Growth Factor market is poised for robust expansion, reflecting significant shifts in biopharmaceutical business models toward highly specific, regenerative protein and gene therapies. Business trends are characterized by substantial merger and acquisition activity among specialty biopharma firms and large pharmaceutical companies seeking to integrate novel HGF delivery platforms, particularly in cardiovascular and renal therapeutic areas. High research expenditure in North America and Europe, coupled with accelerated regulatory pathways like Fast Track designation, are compressing development timelines. Segment trends show that the application segment, particularly cardiovascular diseases (myocardial repair and chronic ischemia), dominates the market due to the high mortality and morbidity associated with these conditions and the demonstrated potent angiogenic effects of HGF. Gene therapy delivery methods are projected to exhibit the highest Compound Annual Growth Rate, driven by the advantage of sustained local HGF expression compared to repeated protein injections.

From a regional perspective, North America maintains the largest market share, attributable to mature healthcare infrastructure, significant governmental and private funding for biotechnology research, and a high volume of ongoing Phase II and Phase III clinical trials involving HGF-based products. However, the Asia Pacific region, led by China and Japan, is emerging as the fastest-growing market. This acceleration is fueled by favorable local regulatory approvals for regenerative medicines (particularly in Japan), the increasing prevalence of diabetes leading to severe peripheral vascular complications, and proactive government investments in biopharma manufacturing capabilities. The European market, while growing steadily, faces fragmentation due to varied national reimbursement policies, although collaborative European research initiatives are boosting early-stage development.

Overall, the market dynamic is shifting from foundational research to commercial readiness. Key market participants are focusing intensely on optimizing manufacturing yields for recombinant HGF and developing scalable, safe viral and non-viral vectors for gene delivery. The primary constraint remains the high cost associated with manufacturing biopharmaceuticals and the complex logistics of clinical application. Strategic partnerships between academic institutions, Contract Development and Manufacturing Organizations (CDMOs), and commercial entities are vital for overcoming these barriers and successfully translating preclinical success into viable commercial products that address unmet medical needs globally.

User inquiries regarding AI's influence on the Hepatocyte Growth Factor market frequently center on three key areas: accelerating target identification and validation related to the c-Met pathway, optimizing the design and stability of recombinant HGF protein variants, and refining patient stratification for clinical trials to maximize therapeutic efficacy. Users are concerned with how AI can minimize the high failure rates common in regenerative medicine trials and whether machine learning algorithms can predict patient response based on genetic or disease biomarkers. Key expectations involve AI reducing the time and cost associated with drug discovery, enhancing personalized dosing regimens for protein therapies, and improving the selection criteria for gene therapy candidates, thereby accelerating the path to market approval and reducing risks associated with large-scale biomanufacturing variability.

The Hepatocyte Growth Factor market is propelled by significant clinical successes in regenerative medicine (Driver), yet simultaneously constrained by formidable manufacturing complexity and regulatory scrutiny of gene therapy vectors (Restraint). The market possesses substantial opportunities arising from the exploration of HGF in new indications, specifically neurodegenerative and pulmonary disorders (Opportunity). These factors interact dynamically, shaping the competitive landscape. The primary impact forces influencing this market trajectory include the rapid pace of technological innovation in genetic engineering for enhanced HGF expression (Technological Force), the escalating global burden of chronic non-communicable diseases requiring regenerative intervention (Societal Force), and the necessity for robust intellectual property protection surrounding novel HGF derivatives and delivery methods (Legal Force). Balancing the need for rapid clinical translation with stringent safety requirements remains the central challenge for market participants, heavily influencing investment decisions and market entry strategies.

Drivers: The increasing prevalence of chronic lifestyle diseases such as diabetes leading to chronic wounds and peripheral artery disease drives demand for potent angiogenic and regenerative agents like HGF. Furthermore, the robust investment in gene therapy platforms, which can provide sustained HGF expression, significantly enhances therapeutic viability over traditional protein injection regimens. Positive outcomes from late-stage clinical trials, particularly in treating critical limb ischemia and post-myocardial infarction recovery, are instilling confidence among clinicians and investors, pushing these therapies closer to commercialization. The established mechanism of action of HGF through the c-Met receptor, confirmed in numerous preclinical models for tissue protection and repair, forms a strong scientific foundation for further therapeutic development.

Restraints: The primary restraint is the extremely high cost associated with the research, development, and complex biomanufacturing of recombinant HGF proteins and corresponding gene therapy vectors. Additionally, regulatory hurdles and the inherent safety concerns surrounding the long-term effects of sustained growth factor expression, particularly the potential for oncogenic risk due to HGF’s mitogenic properties, pose significant restrictions on clinical use. The challenge of achieving targeted delivery and maintaining therapeutic concentration at the injury site without systemic side effects also limits broad applicability. Furthermore, the competitive presence of alternative regenerative therapies, such as stem cell treatments and other growth factor approaches, fragments the market and increases the complexity of securing market share.

Opportunities: Significant market opportunities exist in expanding HGF applications beyond cardiovascular and renal indications into high-growth areas such as neuroregeneration (treating stroke or Parkinson's disease), hepatic failure, and ocular diseases where tissue repair is critical. The development of next-generation delivery technologies, including bio-scaffolds and encapsulated cell delivery systems, promises improved localized efficacy and reduced systemic toxicity. Furthermore, geographical expansion into emerging economies with rapidly improving healthcare infrastructure and high chronic disease burdens offers untapped potential for HGF therapeutics, assuming successful navigation of local regulatory landscapes and pricing pressures.

Impact Forces: The Intellectual Property landscape is intensely competitive, with numerous patents covering HGF sequences, formulations, and vectors, creating high entry barriers for new players. Healthcare policy and reimbursement mechanisms significantly impact the adoption rate, as HGF therapies are currently positioned as high-cost specialty treatments. The societal drive towards curative rather than palliative care methods strongly favors the adoption of regenerative therapies, putting pressure on healthcare providers to integrate advanced biopharmaceuticals. Technological advancements in CRISPR and synthetic biology are offering precision tools for modulating HGF expression, ensuring that the technology evolution remains a constant and powerful force influencing future market direction.

The Hepatocyte Growth Factor market is structurally segmented based on the type of product (recombinant protein or gene therapy), the primary application area, and the specific delivery mechanism utilized. Segmentation allows market stakeholders to focus resources on the most commercially viable therapeutic pathways and regions demonstrating high unmet medical need. The analysis highlights the critical shift toward gene therapy modalities, driven by the desire for durable, single-dose treatments capable of stimulating long-term endogenous HGF production, thereby circumventing the challenges associated with frequent protein injections and short half-lives. Application segmentation is crucial, with cardiovascular and chronic kidney diseases representing the most substantial current revenue streams due to the advanced stage of clinical trials in these areas and HGF's proven efficacy in promoting angiogenesis and nephron protection. Geographical segmentation confirms that clinical adoption and market maturity are highest in developed regions, while future growth is concentrated in emerging biopharma hubs.

The value chain for the Hepatocyte Growth Factor market is complex, beginning with upstream research and discovery, transitioning through intricate biomanufacturing, and culminating in highly regulated clinical distribution. Upstream analysis focuses intensely on basic scientific research, including target identification (c-Met receptor signaling) and preclinical testing of HGF constructs. Key activities include the selection and engineering of expression systems (e.g., mammalian cell lines, yeast, or bacteria) for recombinant protein production, and the development and optimization of viral vectors (like AAV or lentivirus) for gene therapy approaches. Collaboration between academic labs, biotechnology start-ups, and specialized Contract Research Organizations (CROs) is fundamental in this stage, driving innovation in protein stabilization and gene delivery efficiency. Intellectual property development and securing key patents define the success of this initial phase.

Midstream activities revolve around manufacturing and quality assurance. For recombinant protein, this involves large-scale fermentation/cell culture, complex purification (chromatography), and formulation to maintain biological activity. For gene therapies, vector production requires specialized expertise in biosafety and yield optimization, often handled by dedicated Contract Development and Manufacturing Organizations (CDMOs). Quality control is exceptionally rigorous, ensuring compliance with Current Good Manufacturing Practices (cGMP) and confirming the purity, potency, and sterility of the final product. Scalability remains a significant hurdle, as the clinical and eventual commercial demand for high-quality biologicals mandates robust, repeatable, and cost-effective production methods.

Downstream analysis covers clinical trials, regulatory approval, market access, and distribution. Distribution channels are highly specialized, often requiring cold chain logistics due to the sensitivity of biological products. Direct channels are common for high-cost, specialized therapies administered in hospital settings or specialty clinics, allowing manufacturers greater control over product integrity and patient services. Indirect channels, utilizing specialized third-party logistics providers (3PLs) and wholesalers, handle distribution to broader hospital networks. Regulatory approval, led by bodies such as the FDA and EMA, dictates market entry. Following approval, market access requires navigating complex payer landscapes and achieving favorable reimbursement status, a critical step given the typically high price point of HGF therapies. Effective distribution strategies must ensure timely delivery to the point of care while maintaining product efficacy and traceability, minimizing supply chain disruptions.

The primary customers and end-users of Hepatocyte Growth Factor therapeutics are highly specialized entities within the healthcare ecosystem, focusing on regenerative medicine and treatment of refractory chronic diseases. The most significant segment comprises large specialized hospitals and academic medical centers that possess the infrastructure and clinical expertise required for administering advanced biological and gene therapies. These institutions frequently participate in clinical trials and serve as early adopters of novel treatments for conditions such as severe diabetic foot ulcers, acute kidney injury following surgery, and non-revascularizable critical limb ischemia (CLI). Their acquisition volume is high, driven by patient needs within specific departments like cardiology, nephrology, and vascular surgery.

Specialty clinics and dedicated regenerative medicine centers form another crucial customer base. These facilities focus on outpatient procedures and less severe forms of target diseases, often seeking less invasive, locally administered HGF products (e.g., injections for chronic wounds). These centers prioritize ease of administration, product stability, and demonstrated cost-effectiveness compared to complex surgical interventions. Research institutes and biotechnology companies also serve as key buyers, procuring recombinant HGF protein primarily for ongoing preclinical research, assay development, and optimizing novel delivery systems, fueling the market's innovation pipeline.

Furthermore, government and private payer organizations act as indirect but highly influential customers, as their decisions regarding inclusion in national formularies and reimbursement rates directly determine the accessibility and affordability of HGF therapies for the ultimate beneficiaries—the patients. Successful commercialization hinges on demonstrating compelling long-term clinical and economic benefits to these payers. The buyers, therefore, require extensive clinical evidence packages demonstrating superiority over existing standards of care, coupled with robust pharmacovigilance data to mitigate concerns regarding the potential long-term safety of growth factor modulation.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 1.8 Billion |

| Market Forecast in 2033 | USD 4.1 Billion |

| Growth Rate | 12.5% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Osprey Medical, AnGes MG, Kringle Pharma, Genentech (Roche), Medtronic, Bristol-Myers Squibb, Novartis AG, AstraZeneca, Pfizer Inc., Thermo Fisher Scientific, R&D Systems, Lonza Group, Wuxi Biologics, Regeneron Pharmaceuticals, Human Stem Cells Institute, F. Hoffmann-La Roche Ltd., Takeda Pharmaceutical Company Limited, Daiichi Sankyo Company, Limited, Bluebird Bio, Gilead Sciences |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological landscape surrounding the Hepatocyte Growth Factor market is rapidly evolving, driven primarily by innovations in biological manufacturing and targeted delivery systems. The core technology utilized for producing therapeutic-grade HGF involves recombinant DNA technology, requiring sophisticated bioprocesses to achieve high yield and purity of the complex protein structure. Advanced expression systems, including proprietary mammalian cell lines (like CHO cells), are critical for ensuring proper glycosylation and folding necessary for optimal biological activity. Furthermore, novel purification techniques, such as continuous chromatography and advanced filtration systems, are being implemented to reduce production costs and increase scalability, addressing a major constraint in the commercialization pathway for all biologics.

A major technological focus is the development of next-generation delivery vehicles, specifically for gene therapy applications. Adeno-Associated Virus (AAV) vectors remain the most widely used platform for delivering the HGF gene construct, but ongoing research is focused on developing non-viral alternatives (e.g., lipid nanoparticles or polymer-based delivery systems) to mitigate potential immunogenicity issues associated with viral vectors. Enhanced technologies are aimed at achieving cell-specific targeting—for instance, directing the HGF gene specifically to cardiomyocytes or endothelial cells post-myocardial infarction—to maximize local therapeutic effect while minimizing systemic exposure. The implementation of tissue engineering principles, involving the integration of HGF into bio-scaffolds or hydrogels, represents another key technological advancement for sustained, localized release in applications like chronic wound care and musculoskeletal repair.

The application of bioinformatic tools and High-Throughput Screening (HTS) is fundamentally changing the way HGF-based therapies are developed. Computational biology assists in predicting the stability of HGF analogues and optimizing their receptor binding affinity to the c-Met receptor. Furthermore, continuous monitoring technologies in biomanufacturing, utilizing Process Analytical Technology (PAT), ensure real-time quality control and consistency across production batches, which is paramount for meeting rigorous regulatory standards. The integration of these advanced manufacturing and delivery technologies is essential for reducing the overall cost of goods and accelerating the clinical translation of potent HGF therapies, moving them from specialized academic trials into mainstream clinical practice.

North America, particularly the United States, commands the largest market share in the Hepatocyte Growth Factor market, driven by unparalleled R&D spending, the presence of major biopharmaceutical companies, and a streamlined regulatory process (e.g., Regenerative Medicine Advanced Therapy (RMAT) designation) that supports accelerated development. The robust ecosystem of academic research institutions and specialized venture capital funding ensures continuous innovation and rapid progression of HGF pipeline candidates through clinical phases. The high incidence of cardiovascular diseases and chronic kidney failure further contributes to the dominance of this region, creating a significant patient pool actively seeking advanced regenerative treatment options. Furthermore, sophisticated healthcare infrastructure allows for the successful integration and deployment of complex gene therapy procedures and high-cost biological treatments, supporting higher market valuations.

Europe represents a substantial and steadily growing market, primarily led by Germany, the UK, and France. Growth in this region is supported by government initiatives promoting biotech development and collaboration through centralized EU funding mechanisms. However, market adoption is often hindered by the decentralized nature of national health systems, which results in variability in pricing and reimbursement policies. The focus in Europe tends to be heavily centered on regulatory compliance with EMA guidelines and establishing cost-effectiveness data to satisfy national health technology assessment (HTA) bodies. Despite these hurdles, ongoing large-scale European clinical trials focusing on CLI and renal protection using HGF therapies demonstrate a strong commitment to adopting these regenerative solutions.

The Asia Pacific (APAC) region is projected to be the fastest-growing market during the forecast period. This rapid growth is spearheaded by favorable regulatory environments in Japan (which has a robust history of approving regenerative therapies early) and burgeoning investment in biotech infrastructure across China and South Korea. The rapidly expanding elderly population and the resulting increase in chronic diseases, particularly diabetes and related vascular complications, create a vast, underserved market. Local biopharmaceutical companies in APAC are increasingly entering into strategic partnerships with Western firms to gain access to HGF technology, simultaneously developing their own novel HGF analogues and delivery systems tailored to regional manufacturing capabilities and specific disease phenotypes prevalent in Asian populations. Latin America and the Middle East & Africa (MEA) represent nascent markets, characterized by improving healthcare spending and a rising awareness of regenerative medicine potential, primarily through imports and localized distribution agreements.

Hepatocyte Growth Factor (HGF) is a pleiotropic cytokine that binds to the c-Met receptor, acting as a potent mitogen, motogen, and morphogen. Its primary role in regenerative medicine is to stimulate angiogenesis (new blood vessel formation), promote tissue repair, inhibit fibrosis, and prevent apoptosis (cell death) in injured tissues, making it critical for cardiovascular, renal, and wound healing applications.

The largest therapeutic applications for HGF are concentrated in cardiovascular diseases, specifically Critical Limb Ischemia (CLI) and post-Myocardial Infarction (MI) repair, due to HGF's demonstrated ability to induce therapeutic angiogenesis and improve cardiac function post-ischemic injury. Chronic kidney disease (CKD) and non-healing diabetic foot ulcers also constitute major segments.

HGF gene therapy offers the advantage of sustained, localized expression of the HGF protein at the site of injury, typically requiring only a single administration. This contrasts sharply with recombinant protein delivery, which requires frequent injections due to the protein's short half-life, leading to better patient compliance and potentially superior long-term clinical outcomes.

The primary constraints include the high manufacturing complexity and associated cost of biological products and gene therapy vectors, leading to high treatment prices. Furthermore, ongoing regulatory scrutiny and clinical concerns regarding the long-term safety profile of sustained HGF expression, particularly the potential link to oncogenesis given its role as a mitogen, restrict broader clinical use.

AI is expected to significantly accelerate HGF development by optimizing the design of stable HGF protein variants, enhancing the specificity of gene therapy vectors, and improving clinical trial success rates through precision patient stratification. Machine learning helps identify optimal biomarkers for patient selection, paving the way for personalized regenerative medicine protocols.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.