ID : MRU_ 432495 | Date : Dec, 2025 | Pages : 249 | Region : Global | Publisher : MRU

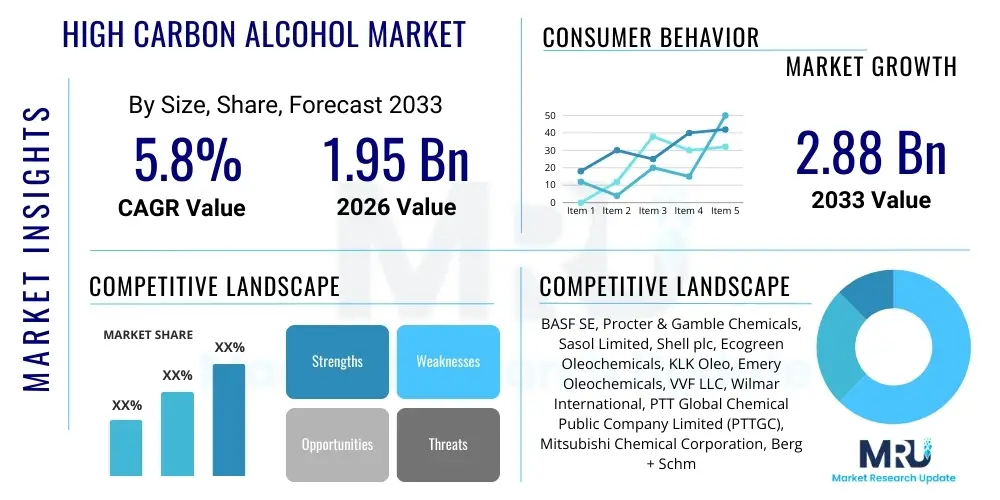

The High Carbon Alcohol Market, encompassing fatty alcohols with chain lengths typically from C12 up to C20 and higher, is experiencing substantial expansion driven by increased demand across key industrial and consumer sectors. This category of alcohols, crucial for manufacturing surfactants, detergents, plasticizers, and high-performance lubricants, is projected to grow at a Compound Annual Growth Rate (CAGR) of 5.8% between 2026 and 2033. The market is estimated at $1.95 Billion USD in 2026 and is projected to reach $2.88 Billion USD by the end of the forecast period in 2033.

High Carbon Alcohols, also known as long-chain fatty alcohols, are linear, primary alcohols derived either from natural sources (oleochemicals like coconut or palm kernel oil) or synthetic routes (petrochemicals). Products include Lauryl Alcohol (C12), Myristyl Alcohol (C14), Cetyl Alcohol (C16), and Stearyl Alcohol (C18), distinguished by their high molecular weight and amphiphilic nature. These alcohols are fundamental building blocks due to their dual functionality: a long hydrophobic carbon chain and a polar hydroxyl group, making them effective emulsifiers, stabilizers, and viscosity modifiers in complex chemical formulations. Their inherent properties, such as low toxicity and high biodegradability, particularly for naturally derived variants, position them as essential ingredients in the transition toward sustainable chemistry.

The primary applications of high carbon alcohols are vast, spanning household, industrial, and specialized sectors. In the detergent and personal care industry, they serve as precursors for producing alcohol sulfates and alcohol ethoxylates, which are key anionic and non-ionic surfactants necessary for cleaning efficiency and foaming properties. Furthermore, in the cosmetics sector, they are valued for their emollient and thickening capabilities, widely used in creams, lotions, and hair conditioners. Industrially, high carbon alcohols are indispensable in manufacturing plasticizers (phthalate alternatives), specialty lubricants, and anti-foaming agents, enhancing the performance and stability of various polymer and fluid systems.

The market is predominantly driven by surging consumer demand for mild, performance-oriented personal care products and the global trend favoring bio-based ingredients. Regulatory pressures in regions like Europe and North America, advocating for the phasing out of traditional petrochemical-based surfactants in favor of readily biodegradable oleochemical derivatives, further accelerate market growth. Additionally, the rapid industrialization and urbanization across the Asia Pacific region, leading to increased consumption of detergents, cleaning agents, and construction chemicals, provides substantial impetus to the production and consumption of high carbon alcohols globally.

The global High Carbon Alcohol market is characterized by a significant transition toward sustainability, marked by heightened investment in oleochemical production capacity, particularly in Southeast Asia where feedstock (palm and coconut oils) is abundant. Business trends indicate strong vertical integration strategies among key players, spanning from feedstock processing to final surfactant production, aimed at controlling supply chain volatility and ensuring quality consistency. Companies are focusing heavily on developing specialty, ultra-high purity grades of C16 and C18 alcohols to cater to the stringent requirements of the pharmaceutical and high-end cosmetics sectors, driving premiumization within the market structure. The competitive landscape is intensely focused on patenting novel, non-traditional synthesis routes to mitigate risks associated with fluctuating agricultural commodity prices and geopolitical supply disruptions affecting crude oil.

Regional dynamics highlight Asia Pacific (APAC) as the dominant and fastest-growing market, propelled by massive population growth, expanding middle-class disposable income, and the consequential boom in the textile, home care, and automotive industries. Regulatory environments in Europe are pivotal, driving the adoption of bio-based high carbon alcohols through mandates promoting sustainable chemical use, thereby positioning the continent as a leader in technological innovation for green chemistry. North America maintains strong demand, primarily fueled by advanced industrial applications, including high-performance lubricants and sophisticated polymer additives, alongside robust consumer market penetration for bio-derived personal care items. These varying regional demands necessitate flexible manufacturing and tailored product portfolios from market participants.

Segment-wise, the Surfactants and Detergents application segment remains the largest consumer of high carbon alcohols, utilizing C12-C14 alcohols extensively for their excellent foaming and cleaning properties. However, the Lubricants and Metalworking Fluids segment is projected to exhibit the highest CAGR, spurred by the need for biodegradable, high-temperature resistant synthetic lubricants in the automotive and aerospace sectors. The segment analysis by source reveals a strong preference shift toward natural/oleochemical-based alcohols over synthetic/petrochemical variants, although petrochemical alcohols continue to dominate specialized, high-purity industrial niches due to their consistent isomer distribution and scalability advantages. This trend underscores the duality of the market, balancing environmental concerns with rigorous industrial performance specifications.

Common user inquiries regarding AI in the High Carbon Alcohol market center on how artificial intelligence can stabilize volatile feedstock supply chains, optimize complex manufacturing processes, and accelerate the discovery of novel bio-based precursors for long-chain alcohols. Users frequently ask about AI's role in predictive quality control, especially concerning the purity and chain-length distribution of fatty alcohols derived from natural oils, which inherently exhibit greater variability than petrochemical sources. Key expectations revolve around using machine learning algorithms to model and predict the impact of environmental factors (e.g., climate change affecting palm harvests) on raw material pricing and availability, enabling manufacturers to implement dynamic procurement strategies. Furthermore, there is significant interest in AI-driven formulation design, where algorithms can rapidly test thousands of potential high carbon alcohol derivatives (e.g., ethoxylates, esters) to identify the optimal chemical structure for specific end-user performance requirements, such as enhanced detergency at low temperatures or improved skin mildness.

The integration of AI and machine learning (ML) is fundamentally changing the operational efficiency and research trajectory within the High Carbon Alcohol industry. AI models are being deployed to analyze vast datasets related to chemical kinetics, catalyst performance, and reactor conditions in synthesis plants. This allows for real-time process optimization, minimizing energy consumption during the hydrogenation and distillation stages, crucial steps in producing high carbon alcohols. Predictive maintenance, another major application, leverages sensor data from plant equipment to forecast potential failures, significantly reducing unplanned downtime and maintaining the capital utilization rate of expensive hydrogenation reactors. This technological enhancement leads to higher yield rates and reduced operational costs, directly impacting the market’s bottom line and improving competitiveness, particularly for producers reliant on continuous flow processes.

In the realm of sustainability and R&D, AI is instrumental in accelerating the development of next-generation bio-alcohols. ML algorithms are used to analyze genomic and metabolic pathways of microorganisms, identifying viable strains for the fermentation of high carbon precursors from non-food biomass, such as algae or agricultural waste. This bio-engineering approach, guided by AI, aims to overcome the current dependence on traditional edible oils, offering a more resilient and environmentally friendly sourcing alternative. By quickly iterating through enzyme design and fermentation protocol adjustments, AI drastically cuts the time needed to bring scalable, sustainable high carbon alcohol production technologies to commercial viability, ensuring the market can meet future demands for certified sustainable ingredients.

The High Carbon Alcohol market is shaped by a confluence of influential factors, notably the growing global awareness and regulatory push toward sustainable and bio-based chemistry (Driver). This momentum is frequently counterbalanced by the significant volatility in feedstock pricing, particularly for crude oil and agricultural commodities like palm kernel oil, which introduce uncertainty into production costs (Restraint). However, the continuous innovation in fermentation and enzymatic synthesis technologies presents a pivotal Opportunity to diversify sourcing away from traditional agricultural and petrochemical dependence, offering long-term stability and environmental benefits. These elements collectively generate powerful impact forces, where the mandatory shift towards high biodegradability (Impact Force) compels manufacturers to prioritize natural sources, even if they incur higher operational complexity and fluctuating costs, ultimately reshaping investment decisions across the industry value chain.

Key drivers include the burgeoning demand for sophisticated personal care products and high-efficacy laundry detergents, especially across developing economies, directly translating into increased consumption of alcohol ethoxylates and sulfates. Furthermore, the stringent safety and environmental regulations in developed nations necessitate the replacement of conventional, potentially harmful chemical additives with milder, high-carbon alcohol derivatives in industrial applications, such as coatings, adhesives, and sealants. The versatility of high carbon alcohols as intermediates allows them to service a rapidly diversifying range of specialized niche markets, including enhanced oil recovery chemicals and specialty agricultural formulations, providing consistent demand expansion independent of the core consumer goods sectors.

The primary restraints, besides feedstock price fluctuations, involve the intensive capital expenditure required for setting up large-scale hydrogenation and purification facilities, creating substantial entry barriers for new market entrants. Additionally, the sustainability debate surrounding palm oil cultivation, a major source for oleochemical high carbon alcohols, poses reputational risks and demands complex certification processes (e.g., RSPO), which can limit supply and complicate procurement. Conversely, the market is rife with opportunities stemming from technological advancements in catalysis, enabling more selective and cost-effective production of specific carbon chain lengths (e.g., pure C14 or C16), which command premium pricing in niche applications. The accelerating trend towards bio-plasticizers as a substitute for traditional phthalates offers a significant, untapped growth vector for medium-to-high carbon alcohol derivatives.

The High Carbon Alcohol market is segmented based on source, type, and application, reflecting the diverse range of end-user requirements and the underlying chemical processes used in their manufacture. The source segmentation (Natural vs. Synthetic) highlights the crucial industry divergence driven by sustainability goals, while the type segmentation (C12-C14, C16-C18, C20+) categorizes products based on their physical and chemical properties, which dictate suitability for specific uses (e.g., shorter chains for detergents, longer chains for lubricants). The application segmentation illustrates the breadth of market penetration, with household cleaning and industrial fluids consuming the majority of the volume, though specialty chemical uses are driving value growth. Understanding these segments is vital for strategic market positioning and resource allocation, enabling companies to focus R&D efforts where demand is highest and margins are most attractive.

The value chain for High Carbon Alcohols begins with complex upstream analysis, focusing heavily on the reliable and sustainable sourcing of feedstocks. For natural alcohols, this involves securing certified sustainable palm kernel or coconut oil from plantations, necessitating robust relationships with major commodity suppliers and strict adherence to sustainability certifications like RSPO. For synthetic alcohols, the upstream phase relies on access to petrochemical intermediates, typically ethylene or linear alpha olefins, sourced from major crude oil refiners and cracking facilities. The volatility and global distribution of these raw materials introduce significant risk management challenges at the upstream level, prompting companies to dual-source when possible to ensure supply continuity and cost optimization, a critical strategic imperative in this market.

The core manufacturing stage involves specialized chemical processing, including high-pressure hydrogenation of fatty acids or olefins, followed by detailed fractional distillation to separate the resulting alcohol mixture into commercial-grade chain-length cuts (e.g., C12, C16). Midstream efficiency is directly dependent on the performance of proprietary catalysts and the energy efficiency of distillation columns. High purity and precise chain-length distribution are paramount, as even minor variations can significantly affect the performance of derived products, such as surfactants or emollients. This stage requires substantial capital investment and deep technical expertise, making it the most value-adding segment in the chain and a critical focus area for process optimization and proprietary technology protection.

The downstream analysis focuses on distribution channels and end-user engagement. High Carbon Alcohols are primarily distributed through a mix of direct sales to large, integrated chemical companies (e.g., multinational detergent manufacturers) and indirect distribution via regional chemical distributors who handle smaller volumes and specialty customer needs. Direct distribution is common for bulk commodity grades, ensuring efficient large-scale delivery, while indirect channels cater to niche formulators in the cosmetics or specialty lubricant sectors. The final stage involves complex compounding and formulation by end-users, where the high carbon alcohols are transformed into final consumer or industrial products, such as anionic surfactants, non-ionic emulsifiers, or bio-based plasticizers, concluding the value transformation cycle.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | $1.95 Billion USD |

| Market Forecast in 2033 | $2.88 Billion USD |

| Growth Rate | 5.8% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | BASF SE, Procter & Gamble Chemicals, Sasol Limited, Shell plc, Ecogreen Oleochemicals, KLK Oleo, Emery Oleochemicals, VVF LLC, Wilmar International, PTT Global Chemical Public Company Limited (PTTGC), Mitsubishi Chemical Corporation, Berg + Schmidt GmbH & Co. KG, Musim Mas Group, Godrej Industries, Sinopec. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technology landscape for High Carbon Alcohols is segmented into traditional chemical synthesis and emerging biotechnological routes. Historically, the primary synthetic methods include the Ziegler process (converting ethylene into linear alpha olefins and subsequently to alcohols) and the OXO synthesis process (hydroformylation of olefins). These petrochemical routes offer high consistency and large economies of scale, making them the standard for synthetic high carbon alcohol production, particularly for C12 and C14 alcohols. However, the environmental footprint and dependence on fossil fuels are driving innovation toward cleaner chemical methods, such as enhanced catalytic systems that operate at lower pressures and temperatures, minimizing energy usage and byproduct formation during the critical hydrogenation stage of fatty acid conversion.

For naturally derived alcohols (oleochemicals), the key technologies center on the efficient and selective conversion of triglycerides (from palm, coconut, etc.) into fatty acids and subsequent hydrogenation. Modern processing employs high-pressure splitting and continuous hydrogenation reactors utilizing highly selective copper or nickel catalysts. Technological advancements here focus on improving the efficiency of fractional distillation columns using advanced packing materials and precise temperature control to achieve ultra-high purity cuts of specific chain lengths, such as cosmetic-grade Cetyl (C16) or Stearyl (C18) alcohols. Sustainability certification tracking via blockchain technology is also becoming a crucial, non-chemical technology, ensuring the provenance of the natural feedstock and maintaining regulatory compliance throughout the supply chain.

The most disruptive technological development is the advent of fermentation-based synthesis, leveraging synthetic biology. This involves genetically modifying yeasts or bacteria to convert inexpensive sugars (derived from biomass or waste) directly into long-chain fatty alcohols (C12 to C18), bypassing both the volatility of agricultural commodities and the dependence on crude oil. This bio-based approach, sometimes referred to as 'fermentative fatty alcohol production,' promises a highly sustainable, scalable, and environmentally friendly alternative. Although currently high in capital cost, the rapid optimization of fermentation yields and downstream purification processes positions this technology as the long-term strategic core for meeting the growing global demand for certified sustainable High Carbon Alcohols, potentially decoupling market stability from traditional feedstock pricing pressures.

Regional consumption patterns and production capabilities significantly influence the global High Carbon Alcohol market dynamics, with pronounced differences in feedstock preference and regulatory environment shaping local market characteristics.

Natural (oleochemical) high carbon alcohols are derived from renewable sources like palm or coconut oils and are favored for their high biodegradability, often used in personal care. Synthetic (petrochemical) alcohols are derived from crude oil intermediates (ethylene) and are valued for their high purity, consistency, and specific isomer distribution, crucial for specialized industrial applications.

The Surfactants and Detergents segment accounts for the largest volume consumption globally. High Carbon Alcohols, particularly C12-C14, are essential precursors for manufacturing anionic and non-ionic surfactants necessary for efficient cleaning and emulsification in household and industrial products.

Key growth drivers include the rising global demand for sustainable, bio-based chemical ingredients, stringent environmental regulations promoting biodegradability, and expanding consumption of personal care and home care products, especially in emerging economies like APAC.

Technological advancement is leading to the commercialization of sustainable sourcing via synthetic biology, where microorganisms are engineered to convert low-cost sugars into long-chain fatty alcohols through fermentation, aiming to reduce reliance on volatile palm/coconut oil and petrochemical feedstocks.

Asia Pacific (APAC) is projected to register the fastest growth rate, driven by significant production capacity (oleochemicals) and surging consumption across developing economies in the textile, detergent, and general industrial sectors.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.