ID : MRU_ 434824 | Date : Dec, 2025 | Pages : 251 | Region : Global | Publisher : MRU

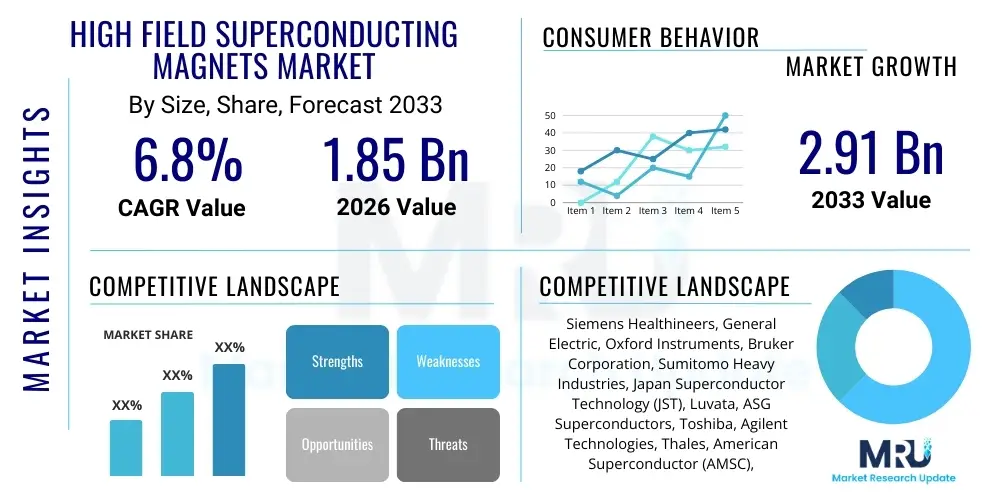

The High Field Superconducting Magnets Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2026 and 2033. The market is estimated at $1.85 Billion in 2026 and is projected to reach $2.91 Billion by the end of the forecast period in 2033.

High field superconducting magnets are advanced technological devices utilizing coils of superconducting wire to generate extremely powerful magnetic fields, significantly higher than those achievable with conventional electromagnets. These magnets operate at cryogenic temperatures, allowing the wires to conduct electricity with zero resistance, thereby maintaining immense field strengths efficiently and stably. The core principle hinges on materials transitioning into a superconducting state below a critical temperature, enabling groundbreaking applications across scientific research, medical diagnostics, and advanced industrial processes. These systems are crucial for achieving ultra-high resolution in Magnetic Resonance Imaging (MRI) and Nuclear Magnetic Resonance (NMR) spectroscopy, which form the diagnostic backbone of modern medicine and materials science, respectively.

The primary driver for this market expansion is the continuous demand for higher field strengths in medical imaging and fundamental physics research. Higher field MRI systems (7T and above) offer enhanced clarity and spatial resolution, facilitating earlier and more precise diagnosis of neurological and oncological conditions. Simultaneously, large-scale scientific infrastructure, such as particle accelerators (like the LHC at CERN) and experimental fusion reactors (like ITER), rely exclusively on highly robust, high-field superconducting magnets to steer particle beams or confine plasma. The efficiency and power density offered by these specialized magnets are unmatched by traditional technologies, cementing their essential role in next-generation technological endeavors.

Key applications span across several critical sectors. In healthcare, they are foundational for clinical and research MRI scanners, offering non-invasive diagnostic capabilities. In research and development, they are integral to advanced spectroscopy, high-energy physics, and materials testing, driving innovation in quantum computing and material design. Furthermore, the development of High-Temperature Superconducting (HTS) materials is opening new avenues for applications in energy sectors, particularly in efficient power transmission, high-speed rail (maglev), and advanced magnetic separation techniques used in industrial purification processes. The overall benefit provided by these magnets is the ability to sustain extremely intense, stable magnetic fields required for complex scientific and industrial operations efficiently.

The High Field Superconducting Magnets market demonstrates robust growth, primarily driven by accelerated investments in advanced medical diagnostics and large-scale public and private funding for high-energy physics research. Current business trends indicate a strong shift towards the commercialization of 7 Tesla (T) MRI systems and the increasing adoption of High-Temperature Superconducting (HTS) technology, which promises lower cooling costs and greater operational flexibility compared to traditional Low-Temperature Superconducting (LTS) magnets. Strategic collaborations between academic research institutions and commercial manufacturers are intensifying, focusing on developing more compact and powerful magnet designs, particularly those leveraging rare-earth barium copper oxide (REBCO) wires. The industry is also witnessing significant merger and acquisition activity aimed at consolidating technological expertise and expanding regional distribution networks, especially in rapidly industrializing economies where healthcare infrastructure investment is soaring.

Regionally, North America and Europe currently dominate the market due to established infrastructure in advanced medical research and the presence of major key players and large-scale research facilities (e.g., Fermilab, CERN). However, the Asia Pacific (APAC) region is projected to exhibit the highest Compound Annual Growth Rate (CAGR) during the forecast period. This accelerated growth in APAC is fueled by massive governmental expenditure on building advanced medical facilities in countries like China, India, and South Korea, coupled with significant national initiatives in nuclear fusion and particle physics. Latin America and the Middle East & Africa (MEA) represent emerging markets, with growth primarily concentrated in urban centers adopting high-end diagnostic equipment, though regulatory harmonization and infrastructure deficits pose moderate limitations to immediate widespread adoption.

In terms of segmentation, the healthcare application segment, driven by MRI and NMR demand, remains the largest revenue contributor. Nonetheless, the research and development segment, particularly fueled by international projects like fusion energy programs, is expected to exhibit faster growth due to the escalating demand for highly specialized, ultra-high field magnets (e.g., above 20T). Technology-wise, while LTS magnets (primarily utilizing NbTi and Nb3Sn) constitute the bulk of the market due to maturity and reliability, the HTS segment is gaining traction rapidly. HTS magnets are poised to disrupt the market by enabling operation at warmer temperatures, simplifying cryogenic systems, and potentially reducing the overall footprint and maintenance cost of future superconducting devices, thereby accelerating adoption in industrial settings previously inaccessible to superconducting technology.

Users frequently inquire how Artificial Intelligence (AI) and Machine Learning (ML) can optimize the design, manufacturing, and operational efficiency of high field superconducting magnets. Key user concerns revolve around reducing the complexity of magnetic field shimming processes, predicting magnet quench (failure) events, and optimizing cryogenic system performance. The expectation is that AI algorithms can significantly accelerate the R&D cycle for new superconducting materials by simulating complex material interactions and identifying optimal alloy compositions faster than traditional empirical methods. Furthermore, users anticipate that AI will enhance the reliability of clinical applications, particularly in MRI, by improving image reconstruction and compensating for magnetic field drift, thereby ensuring stable and precise diagnostic outcomes across long operational periods.

The integration of AI, specifically through advanced computational methods and predictive modeling, is revolutionizing the development and deployment of high field superconducting magnets. In the design phase, ML algorithms are employed to optimize coil winding geometries and minimize stray fields, reducing material waste and improving field homogeneity, which is crucial for high-resolution imaging and sensitive physics experiments. During operation, AI-powered predictive maintenance systems analyze real-time telemetry data—including temperature fluctuations, voltage transients, and pressure readings—to anticipate potential critical failures, such as quench events, allowing operators to intervene proactively and drastically enhancing system uptime and safety.

Furthermore, in the core application of MRI, deep learning models are fundamentally changing data acquisition and processing. AI facilitates rapid, low-signal MRI acquisition by denoising and reconstructing high-quality images from undersampled data, reducing scanning times and improving patient throughput. This optimization of the final diagnostic output indirectly drives the demand for the underlying high-field magnet technology, as clinicians seek systems that combine superior field strength with optimized operational intelligence. AI thus acts as a pivotal enabler, maximizing the utility and performance envelope of high field superconducting magnet infrastructure across all major end-user sectors.

The High Field Superconducting Magnets Market is profoundly influenced by a complex interplay of Drivers (D), Restraints (R), and Opportunities (O), which dictate market velocity and strategic investments. Key drivers include the escalating global demand for advanced medical imaging modalities, particularly ultra-high field MRI (7T and above), and robust, sustained governmental funding for large-scale physics research initiatives like fusion energy and particle colliders. These drivers collectively necessitate greater field strength and stability. Conversely, the market is constrained by significant capital investment required for procurement and installation, the high operational complexity associated with cryogenic systems (especially liquid helium reliance for LTS magnets), and inherent supply chain vulnerabilities regarding specialized raw materials like Niobium alloys. The high barrier to entry for new manufacturers due to stringent certification requirements and required intellectual property also limits competitive dynamism.

Opportunities in this sector are primarily centered on the commercialization of High-Temperature Superconducting (HTS) technology, which promises to mitigate the operational restraints associated with liquid helium cooling. HTS materials, such as YBCO and Bi-2223, can operate using less complex and more cost-effective cooling methods (like closed-cycle cryocoolers), opening doors for superconducting technology in industrial applications (e.g., magnetic separation, smart grid power transmission) where complexity and cost were previously prohibitive. Furthermore, the development of smaller, more mobile superconducting magnet systems for specialized applications, coupled with expansion into emerging economies with burgeoning healthcare infrastructure, represents significant long-term market growth potential.

The impact forces within the market are predominantly technological and financial. The accelerating pace of scientific discovery mandates continuous innovation in magnet design, pushing the limits of current superconducting materials. Economically, the market is highly sensitive to public research budgets; geopolitical stability and government commitments to multi-billion dollar research projects (like the next generation of particle accelerators) directly determine the size and timing of major procurement cycles. Moreover, strict regulatory frameworks governing medical devices (FDA, CE Mark) exert strong downward pressure on R&D timelines and necessitate rigorous quality control, influencing both market entry and product deployment strategies across key regions.

The High Field Superconducting Magnets Market is primarily segmented based on the type of superconducting material (LTS vs. HTS), the level of magnetic field strength (low, high, ultra-high), the application domain (healthcare, research, energy), and the geographic region. This multi-faceted segmentation allows for a detailed analysis of market dynamics, revealing that while the traditional Low-Temperature Superconducting (LTS) segment currently dominates revenue due to established reliability and large installed base in MRI, the High-Temperature Superconducting (HTS) segment is poised for the most rapid growth driven by industrial adoption and reduced cooling requirements. Application segmentation highlights the consistent demand from the healthcare sector, counterbalanced by cyclical but high-value demands from fundamental research facilities.

Further breakdown by field strength shows a clear trend towards the higher end; ultra-high field magnets (above 7 Tesla) are seeing increasing investment driven by advanced neurological studies and materials science research, often requiring custom-engineered solutions. Geographically, market maturity dictates growth rates, with established markets focusing on replacement and upgrading existing infrastructure, while burgeoning markets, particularly in Asia Pacific, prioritize initial mass installation of diagnostic systems. Understanding these segment trends is crucial for stakeholders to align their product development and market penetration strategies, focusing on the convergence of HTS materials with ultra-high field requirements in specialized medical and research applications.

The value chain for high field superconducting magnets is highly specialized and complex, beginning with the critical upstream supply of raw materials. This upstream phase involves the mining and purification of rare earth metals (for HTS) and specific transition metals like Niobium and Titanium (for LTS). The subsequent stage involves the production of superconducting wire and cables, which is a highly technical process dominated by a few specialized manufacturers capable of drawing fine, complex composite filaments. Any disruption in the supply or pricing volatility of these precursor materials directly impacts the profitability and production cycle of magnet manufacturers. Reliability in the wire drawing process and maintaining stringent quality control over filament diameter and superconducting properties are foundational to the overall performance of the final magnet system.

The central phase of the value chain involves the design, winding, and integration of the superconducting coils into the final magnet system. This manufacturing process requires extreme precision engineering, advanced cryogenics integration, and sophisticated field mapping capabilities. Original Equipment Manufacturers (OEMs), who typically operate in highly controlled cleanroom environments, acquire the superconducting wire and incorporate complex cooling jackets, structural supports, and safety mechanisms (e.g., quench protection circuits). Distribution channels for these large, high-value systems are primarily direct; manufacturers usually negotiate sales, installation, and long-term maintenance contracts directly with major end-users such as large hospital networks, governmental research labs, or energy consortiums. Indirect channels, involving specialized engineering consultants or regional distributors, often facilitate sales, but the core technical support remains OEM-centric.

The downstream segment is defined by the installation, commissioning, maintenance, and eventual decommissioning of these long-lifecycle assets. Given the capital-intensive nature of superconducting magnets, after-sales service, including periodic cooling system maintenance (especially liquid helium refills) and software upgrades, represents a significant and stable revenue stream for OEMs. The primary end-users are clinical diagnostic centers (e.g., for MRI operation) and large scientific institutions. The interaction between the manufacturer and the end-user often extends over decades, solidifying the importance of reliable long-term support. Technological advancements, particularly in integrating cryogen-free cooling systems, are gradually simplifying the downstream maintenance process, potentially shifting the balance of value capture from continuous service toward the initial product sale and specialized system integration expertise.

The primary customers for high field superconducting magnets are institutions that require stable, high-intensity magnetic fields for advanced technical operations. The largest segment remains the healthcare sector, specifically major hospitals, private imaging clinics, and specialized diagnostic centers procuring high-field (3T to 7T) MRI systems for complex anatomical and functional imaging. These buyers prioritize system uptime, image quality, and regulatory compliance. The second significant customer base is the academic and governmental research community, including universities, national laboratories, and international scientific organizations involved in high-energy physics, plasma confinement (fusion reactors), quantum research, and materials science. These customers often demand custom-engineered, ultra-high field magnets (above 10T) to push the boundaries of fundamental research.

A rapidly growing segment of potential customers includes industrial entities, particularly those engaged in energy and high-tech manufacturing. This incorporates electrical utilities and grid operators interested in superconducting fault current limiters and power cables for loss-less energy transmission. Furthermore, manufacturers requiring high-efficiency magnetic separation for mineral processing or water purification represent an emerging customer group, particularly as HTS technology lowers the barrier to entry for industrial implementation. Finally, the aerospace and defense sectors, while smaller volume purchasers, require high field magnets for specialized testing applications and potential military-grade devices, focusing heavily on reliability and robustness under demanding conditions.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | $1.85 Billion |

| Market Forecast in 2033 | $2.91 Billion |

| Growth Rate | 6.8% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Siemens Healthineers, General Electric, Oxford Instruments, Bruker Corporation, Sumitomo Heavy Industries, Japan Superconductor Technology (JST), Luvata, ASG Superconductors, Toshiba, Agilent Technologies, Thales, American Superconductor (AMSC), Cryomagnetics Inc., SuperPower Inc., HTS-110, Southwire Company, Furukawa Electric, Nexans, Superconducting Technology (STI), Quantum Design. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The High Field Superconducting Magnets market is characterized by intense technological competition centered on material science and cryogenic engineering. Currently, the landscape is dominated by Low-Temperature Superconducting (LTS) technology, primarily utilizing Niobium-Titanium (NbTi) and Niobium-Tin (Nb3Sn) alloys. NbTi is the workhorse for most clinical MRI systems (up to 3T and some 7T systems) due to its ductility, ease of manufacturing, and cost-effectiveness, requiring cooling to 4.2 Kelvin (liquid helium temperature). Nb3Sn, while brittle and harder to process, is necessary for achieving fields between 10T and 20T, crucial for advanced spectroscopy and large-scale physics experiments, offering superior performance but demanding sophisticated winding techniques and heat treatment processes.

The emerging technological frontier is High-Temperature Superconducting (HTS) magnets, utilizing materials like Bismuth Strontium Calcium Copper Oxide (Bi-2223) and Yttrium Barium Copper Oxide (YBCO or REBCO). Although "high temperature" is relative (typically operating above liquid nitrogen temperature or around 40-77K), these materials significantly simplify cryogenic requirements, allowing the use of cryocoolers instead of bulky, expensive liquid helium systems. HTS technology is pivotal for developing compact, cryogen-free high-field magnets (e.g., portable NMR devices or industrial magnetic separators) and is essential for ultra-high field systems (above 20T) where the performance limits of Nb3Sn are reached. The development of robust, economically viable HTS wire manufacturing processes remains a key challenge and a central focus of R&D investment.

Beyond the core superconducting materials, innovation is focused on enhancing system efficiency and stability. Advancements in persistent mode switches, which allow the magnet to operate without continuous power once the field is established, improve long-term stability crucial for research. Furthermore, sophisticated quench protection systems—utilizing passive and active components to safely dissipate stored energy during a failure event—are becoming smarter, often integrating AI for predictive analysis. The move towards cryogen-free magnet systems, leveraging high-efficiency pulse tube refrigerators and Gifford-McMahon cryocoolers, is a fundamental technological shift that is broadening the market accessibility of high field magnets to environments previously unsuitable due to infrastructure constraints or high liquid helium costs. This integration of advanced thermal management systems, combined with superior HTS materials, defines the next generation of commercially available superconducting magnet technology.

Geographic analysis reveals distinct market maturity and growth dynamics across different regions, influenced by localized investment in healthcare infrastructure, industrial policy, and fundamental research funding.

The primary driver is the accelerating need for higher spatial and spectral resolution in medical imaging (MRI/NMR) and fundamental scientific research, particularly in neurological studies, materials science, and high-energy physics projects, requiring field strengths exceeding 7 Tesla.

HTS technology, utilizing materials like YBCO, is crucial for developing cryogen-free magnet systems that operate at warmer temperatures (above 40K). This simplifies cooling, reduces reliance on expensive liquid helium, lowers operational costs, and expands market accessibility to industrial and mobile applications.

Key challenges include the high upfront capital cost, the complexity and expense of maintaining cryogenic infrastructure (especially liquid helium refill schedules for LTS magnets), and the risk of magnet quench (a sudden loss of superconductivity) which requires sophisticated safety and recovery procedures.

The Healthcare application segment, dominated by the widespread use of High Field Magnetic Resonance Imaging (MRI) systems for clinical diagnostics and anatomical studies, remains the largest revenue contributor to the superconducting magnets market.

The market is led by established regions, North America and Europe, due to advanced R&D and healthcare infrastructure. However, the Asia Pacific region is projected to register the highest growth rate, driven by massive public investments in new research facilities and expanding medical diagnostics access.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.