ID : MRU_ 434576 | Date : Dec, 2025 | Pages : 258 | Region : Global | Publisher : MRU

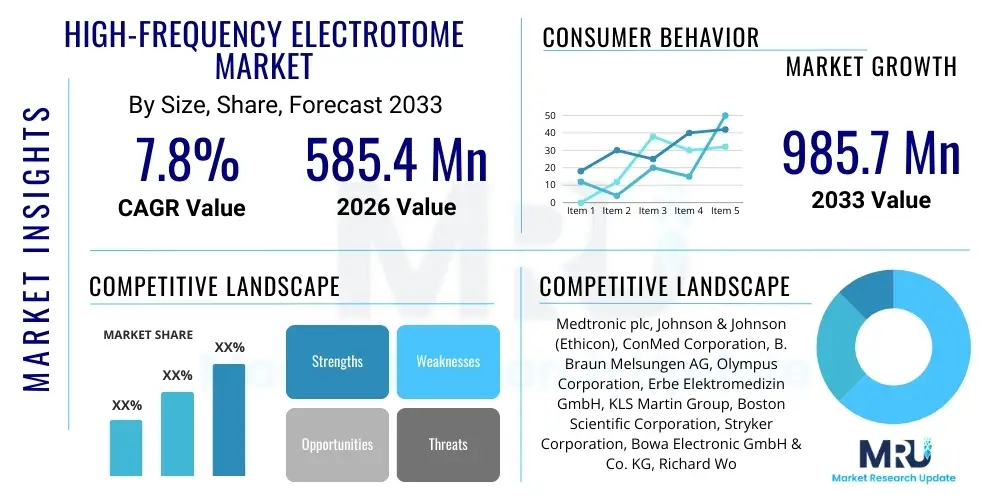

The High-Frequency Electrotome Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 7.8% between 2026 and 2033. The market is estimated at $585.4 Million USD in 2026 and is projected to reach $985.7 Million USD by the end of the forecast period in 2033.

The High-Frequency Electrotome Market encompasses devices utilizing high-frequency alternating current to perform surgical functions such as cutting, coagulation, desiccation, and fulguration of biological tissue. These sophisticated medical devices are fundamental tools in modern operating rooms, enabling precise, controlled, and often minimally invasive surgical procedures across various specialties. Electrotomes function by converting electrical energy into heat at the surgical site, allowing for simultaneous cutting and hemostasis, thereby reducing blood loss and accelerating recovery times compared to traditional scalpel surgery. The versatility and efficiency of these devices have secured their widespread adoption in hospitals, ambulatory surgical centers, and specialized clinics globally, driving consistent market expansion.

Major applications for high-frequency electrotomes span crucial medical disciplines, including general surgery, gynecology, cardiology, dermatology, and neurosurgery. In general surgery, they are indispensable for procedures like appendectomies and cholecystectomies. Their application in minimally invasive surgery (MIS), particularly laparoscopy and endoscopy, represents a significant growth segment, as these techniques demand precise energy delivery in confined anatomical spaces. The key benefits driving adoption include reduced patient trauma, decreased length of hospital stay, lower risk of infection, and improved cosmetic outcomes. These factors align strongly with global healthcare trends emphasizing value-based care and efficiency improvement.

Market growth is primarily driven by several critical factors: the rising global incidence of chronic diseases requiring surgical intervention, the accelerating trend toward adopting minimally invasive surgical techniques, and continuous technological advancements leading to the development of more advanced, safer, and multi-functional electrotome units. Furthermore, increased healthcare spending in developing economies and a growing elderly population prone to surgical conditions also contribute significantly to the expanding demand for high-frequency electrotomes. Regulatory clearances facilitating the rapid introduction of new generations of electrosurgical units, integrated with features like tissue monitoring and intelligent feedback systems, further solidify the market's positive trajectory.

The High-Frequency Electrotome Market is characterized by robust growth driven by technological integration and the pervasive shift towards minimally invasive procedures globally. Business trends indicate strong emphasis on developing advanced energy platforms that integrate multiple functions, such as bipolar and monopolar modes, with sophisticated safety mechanisms like automatic power adjustment based on tissue impedance. Key market participants are focusing on strategic collaborations, mergers, and acquisitions to broaden their product portfolios and geographical reach, particularly targeting emerging markets in Asia Pacific where healthcare infrastructure is rapidly developing. Furthermore, the increasing demand for specialized, portable units suitable for ambulatory surgical centers is a defining commercial trend, alongside a commitment to reusable and sustainable device components.

Regionally, North America and Europe maintain dominance, attributed to high healthcare expenditure, established clinical adoption protocols, and the early availability of cutting-edge technology. However, the Asia Pacific region is anticipated to demonstrate the highest growth rate during the forecast period due to burgeoning medical tourism, rapid urbanization, rising disposable incomes, and governments’ initiatives to improve access to surgical care. Latin America and the Middle East and Africa are also showing promising signs of acceleration, fueled by foreign investments in hospital infrastructure and increasing awareness regarding advanced surgical tools. Regional variations in regulatory approval processes and reimbursement policies significantly influence the market structure and competitive dynamics across these geographies.

Segmentation trends reveal that the use of Bipolar Electrotomes is gaining substantial traction over Monopolar Electrotomes, primarily due to their superior safety profile, reduced risk of unintended burns, and specific advantages in sensitive areas like neurosurgery and gynecology. In terms of application, general surgery and obstetrics/gynecology remain the largest segments, but specialized areas like cardiology and ophthalmology are demonstrating high incremental opportunities. Furthermore, end-user segmentation highlights that Hospitals continue to be the primary revenue generators, but the rapid proliferation of Ambulatory Surgical Centers (ASCs) is reshaping distribution strategies, necessitating the development of cost-effective, high-performance compact systems suitable for outpatient settings.

Common user questions regarding AI's impact on high-frequency electrotomes center on themes such as enhanced precision, automation of critical settings, predictive maintenance, and improved surgical training. Users frequently inquire about whether AI can automatically adjust the power output of the electrotome in real-time based on immediate tissue impedance monitoring, thereby minimizing the risk of thermal injury to surrounding healthy tissue. There is significant interest in AI algorithms that can analyze surgical video feeds to provide contextual guidance to the surgeon, or even automate simple, repetitive cutting and coagulation tasks within robotic surgical systems. Concerns often revolve around the regulatory hurdles for AI-driven devices, data privacy of surgical recordings, and the potential displacement of skilled surgical assistants due to increased automation.

The integration of Artificial Intelligence (AI) and Machine Learning (ML) into high-frequency electrotomes is poised to revolutionize electrosurgery by transforming devices from passive energy generators into intelligent surgical assistants. AI algorithms are increasingly being used to interpret continuous streams of data—including tissue temperature, electrical impedance, and visual feedback—to optimize the energy delivery parameters in milliseconds. This real-time optimization capability ensures maximum efficacy for cutting and coagulation while drastically reducing collateral tissue damage and charring. This shift moves the technology toward truly personalized surgery, where the device adapts instantly to the unique characteristics and pathology of the patient’s tissue, significantly improving patient safety and procedural outcomes.

Furthermore, AI-powered systems are impacting the operational and maintenance aspects of the market. Predictive maintenance models analyze usage patterns and internal diagnostics of electrotome units to forecast potential hardware failures, allowing for proactive servicing and minimizing costly downtime in operating rooms. In the future, AI will likely enable advanced feedback loops in robotic-assisted electrosurgery, allowing robots to perform complex tasks with higher stability and precision than human hands. This integration promises to elevate the standards of electrosurgical practice, driving innovation towards safer, more predictable surgical procedures across all major disciplines utilizing high-frequency energy.

The High-Frequency Electrotome Market is shaped by a powerful confluence of drivers, restraints, and opportunities. The principal driver is the surging global preference for minimally invasive surgical procedures, which inherently rely on the precision and immediate hemostasis capabilities of modern electrotomes. This is coupled with the growing incidence of chronic conditions—such as cardiovascular diseases, various cancers, and gastrointestinal disorders—that require surgical intervention, thereby expanding the potential patient pool. Technological advancement acts as a significant amplifying force, particularly the shift toward safer bipolar and integrated energy platforms, which address historical concerns regarding patient safety and thermal injury. These drivers collectively ensure a sustained and elevated demand for high-quality electrosurgical equipment worldwide.

Despite strong drivers, the market faces notable restraints. High capital investment required for acquiring advanced electrosurgical units, especially those integrated with robotic systems, poses a barrier to entry for smaller hospitals and healthcare facilities in developing regions. Furthermore, the persistent risk associated with unintended burns and potential complications arising from improper use or device malfunction necessitates stringent training protocols and adds complexity to clinical deployment. Another significant restraint is the increasingly rigorous regulatory environment in mature markets like the U.S. and E.U., which often lengthens the time-to-market for new innovations and increases development costs, slowing the pace of widespread adoption of cutting-edge technologies.

Opportunities in this market are abundant, primarily focused on untapped geographical areas and product specialization. Emerging economies, characterized by improving healthcare infrastructure and expanding access to insurance, present substantial growth prospects for both established and local manufacturers. Furthermore, there is a clear opportunity for market players to develop specialized electrotome accessories and consumables tailored for niche areas such as pediatric surgery and aesthetic dermatology, where unique tissue properties demand specific energy delivery profiles. The move towards establishing standardized protocols for electrosurgical safety and training also provides manufacturers an opportunity to partner with educational institutions, cementing brand loyalty and driving the adoption of their latest devices. These forces, including technological innovation and demographic shifts, exert a cumulative impact on market dynamics, ensuring steady evolution and competitive intensity.

The High-Frequency Electrotome Market is extensively segmented based on key functional characteristics, operational mode, application type, and the end-user base, providing a granular view of market dynamics. Segmentation is crucial for strategic analysis, revealing differential growth rates and adoption patterns across distinct product categories and clinical settings. The primary categorization by technology distinguishes between Monopolar and Bipolar units, reflecting the evolution toward safer and more specialized energy delivery. Further segmentation by application highlights the dominant surgical specialties driving demand, while end-user categorization illustrates the evolving landscape of surgical sites, moving beyond traditional hospitals to embrace specialized ambulatory centers and clinics. This detailed structural breakdown allows companies to tailor their R&D and marketing efforts to the most promising and rapidly expanding segments of the global market.

The value chain for the High-Frequency Electrotome Market begins with the upstream suppliers, focusing primarily on high-precision electronic components, sophisticated microprocessors, specialized materials (e.g., medical-grade plastics and stainless steel for instruments), and advanced power supply units. Critical elements at this stage involve ensuring the highest quality of semiconductor components necessary for generating stable, high-frequency currents, and securing reliable supply chains for specialized ceramic and metal alloys used in surgical tips and electrodes. Manufacturers are highly dependent on these specialized upstream providers, making supply chain resilience and cost management significant factors influencing final product pricing and availability. Optimization in this phase often involves strategic long-term contracts and diversification of material sourcing.

The core of the value chain involves the manufacturing and assembly phase, where extensive R&D efforts are focused on improving safety features, integrating digital technologies (like tissue monitoring), and miniaturization of generators. Companies invest heavily in obtaining necessary regulatory approvals (e.g., FDA clearance, CE Marking) which significantly adds value and credibility to the product. Following manufacturing, the distribution phase involves a complex network. Direct distribution is common for high-value generators, involving specialized sales representatives who provide technical training and maintenance support directly to major hospital systems and large purchasing organizations. This approach ensures control over the quality of installation and after-sales service, critical for maintaining high performance standards.

Conversely, indirect distribution utilizes medical device distributors, wholesalers, and third-party logistics providers, particularly for high-volume consumables and accessories like disposable electrodes and pencils. This method is crucial for reaching smaller clinics, ambulatory surgical centers, and international markets where manufacturers may lack a direct physical presence. Downstream analysis focuses on the end-users—hospitals, ASCs, and specialized clinics—who rely heavily on prompt maintenance, technical support, and continuous clinical education provided by the manufacturer or authorized distributors. The final stage involves post-market surveillance and feedback loops, which inform future product iterations, completing a cyclical value chain heavily weighted toward precision manufacturing, rigorous regulatory compliance, and robust technical support services.

The primary and largest segment of potential customers for high-frequency electrotomes consists of large acute care Hospitals and integrated health systems globally. These institutions perform the vast majority of complex and high-volume surgical procedures, including general surgery, complex cardiovascular interventions, and neurosurgical operations, requiring high-end, multi-functional electrosurgical generators and specialized accessories. Hospitals are driven by the need for superior patient safety standards, efficiency in the operating room, and equipment reliability, making them the target audience for premium, high-specification devices that offer advanced features like tissue feedback control and integrated smoke evacuation systems. Purchasing decisions in this segment are often centralized and involve clinical staff, procurement departments, and value analysis committees, emphasizing total cost of ownership (TCO) alongside clinical efficacy.

A rapidly expanding segment of potential customers includes Ambulatory Surgical Centers (ASCs) and specialized Outpatient Clinics. ASCs focus on scheduled, less complex procedures that allow patients to return home the same day, such as endoscopy, minor orthopedic surgeries, and cosmetic procedures. This customer base seeks portable, easy-to-use, and cost-effective electrosurgical units that do not compromise on safety or performance. Their buying criteria often prioritize small footprints, intuitive interfaces, and low maintenance costs, driving demand for specialized compact electrotomes suitable for high-throughput, standardized procedures. As healthcare shifts towards outpatient settings for cost efficiency, ASCs represent a critical area for market penetration, requiring tailored product offerings and streamlined service contracts.

Other vital customer groups include specialized clinical centers focusing on fields like dermatology, cosmetology, and veterinary medicine, which utilize electrotomes for highly specific applications requiring fine control over coagulation and ablation depth. Academic and research institutions also constitute a smaller but crucial customer base, purchasing advanced units for training surgeons, conducting clinical trials, and developing novel surgical techniques. Manufacturers must address the diverse needs of these customer groups—from high-volume hospital purchasing to the individualized requirements of specialty clinics—by maintaining a broad portfolio that ranges from ultra-sophisticated integrated platforms to dedicated, single-purpose electrosurgical pencils and accessories.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | $585.4 Million USD |

| Market Forecast in 2033 | $985.7 Million USD |

| Growth Rate | 7.8% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Medtronic plc, Johnson & Johnson (Ethicon), ConMed Corporation, B. Braun Melsungen AG, Olympus Corporation, Erbe Elektromedizin GmbH, KLS Martin Group, Boston Scientific Corporation, Stryker Corporation, Bowa Electronic GmbH & Co. KG, Richard Wolf GmbH, Kirwan Surgical Products, Dentsply Sirona, AtriCure, Inc., Utah Medical Products, Inc., Smith & Nephew plc, OLYMPUS CORPORATION, DePuy Synthes (J&J), Sutter Medizintechnik GmbH |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technology landscape of the High-Frequency Electrotome Market is rapidly evolving, moving beyond basic monopolar cutting and coagulation towards highly sophisticated, integrated, and safer energy delivery systems. A primary technological focus is on enhancing tissue protection through advanced feedback control systems. Modern electrotomes incorporate microprocessors and sophisticated algorithms to continuously monitor tissue impedance during the procedure. This real-time monitoring allows the generator to automatically adjust power output, ensuring that only the minimum necessary energy is applied to achieve the desired surgical effect (cut or coagulation) while minimizing thermal spread to adjacent healthy tissue, thereby reducing the risk of unintended burns and improving patient recovery. This advancement is crucial for procedures involving delicate structures like nerves and major vessels.

Another dominant technological trend is the proliferation of Bipolar Electrosurgery, especially advanced vessel sealing technology. Traditional monopolar surgery requires the current to flow through the patient’s body to a grounding pad, creating potential risks. Bipolar devices, however, confine the current flow between two tips of an instrument (e.g., forceps), offering superior control and significantly enhanced safety, particularly in procedures where grounding pads cannot be effectively placed or where patients have implanted electronic devices. Vessel sealing technology builds upon this by employing precise combinations of pressure and controlled bipolar energy to permanently fuse tissue bundles and blood vessels up to 7mm in diameter, offering a robust, suture-less hemostasis method that increases procedural efficiency and reduces operating time across major surgical disciplines.

The future of the market is defined by the integration of electrosurgery with other complementary technologies, particularly robotic surgery systems and smoke evacuation technology. Electrosurgical units designed for robotic platforms require specialized, long, and flexible instruments capable of precise articulation and energy delivery commanded remotely by the surgeon. Furthermore, as awareness of surgical smoke hazards (containing viable viruses, cellular debris, and carcinogens) grows, the integration of high-efficiency smoke evacuation systems directly into the electrotome pencil or surgical suite is becoming standard. Manufacturers are prioritizing solutions that seamlessly manage smoke plume at the source without disrupting the surgical field, further driving innovation in combined safety and performance features within the comprehensive operating room environment.

Monopolar electrotomes pass current through the patient's body to a grounding pad, suitable for wide-area cutting and coagulation. Bipolar electrotomes confine the current between two tips of the instrument, offering highly localized energy delivery, superior safety, and reduced risk of remote burns, making them preferred for precise surgery and sensitive tissue.

General Surgery consistently drives the highest demand due to the essential use of electrosurgical units in common procedures like laparoscopy, coupled with high volume. However, specialized segments like Gynecology (especially vessel sealing) and Urology are demonstrating significant accelerated growth due to procedural advancements.

The global shift toward MIS is a primary market driver. MIS procedures rely critically on advanced high-frequency electrotomes for precise cutting and immediate hemostasis through small incisions, directly increasing the demand for sophisticated, specialized instruments and generators designed for laparoscopic and endoscopic use.

Modern units incorporate advanced safety features such as Automatic Return Monitoring (ARM) to ensure proper grounding pad contact, Tissue Impedance Monitoring to auto-adjust power output, and integrated smoke evacuation systems to protect surgical staff and optimize visualization during the procedure.

The Asia Pacific (APAC) region is forecasted to exhibit the fastest growth rate, driven by substantial government investments in healthcare infrastructure, increasing population access to surgical care, and the rising adoption of Western medical technology in countries such as China and India.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.