ID : MRU_ 432013 | Date : Dec, 2025 | Pages : 258 | Region : Global | Publisher : MRU

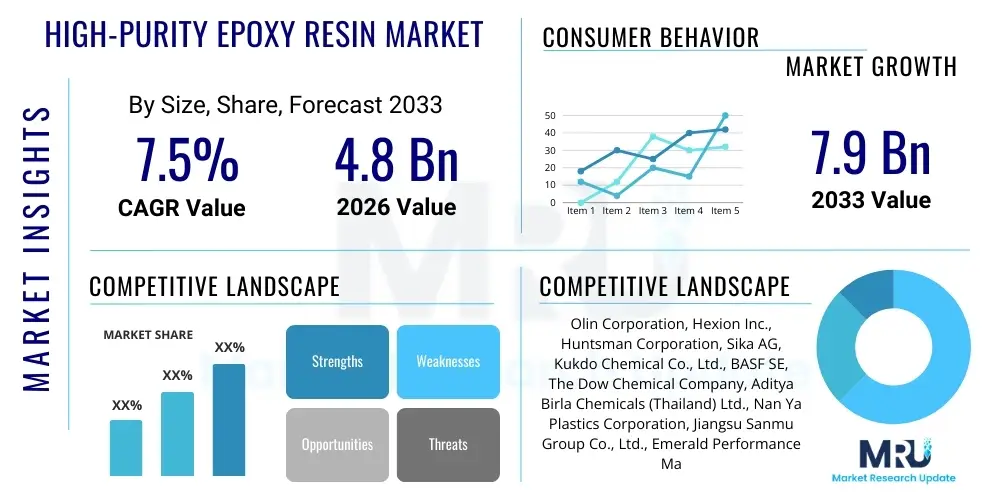

The High-Purity Epoxy Resin Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 7.5% between 2026 and 2033. The market is estimated at USD 4.8 Billion in 2026 and is projected to reach USD 7.9 Billion by the end of the forecast period in 2033.

High-purity epoxy resins are specialized, thermosetting polymers characterized by extremely low levels of ionic impurities, halides, and volatile organic compounds (VOCs). This stringent compositional control is essential because even trace impurities can significantly degrade the performance and longevity of sensitive electronic components, particularly semiconductors, integrated circuits (ICs), and light-emitting diodes (LEDs). These resins are critical in advanced packaging, microelectronics encapsulation, and high-performance composites where dielectric strength, thermal stability, and low coefficient of thermal expansion (CTE) are paramount. The market expansion is intrinsically linked to the global acceleration in semiconductor manufacturing, the proliferation of 5G technology, and the stringent demands from the aerospace and automotive sectors for materials that can withstand extreme operational environments.

The primary function of high-purity epoxy resins involves providing mechanical protection, electrical insulation, and hermetic sealing for delicate electronic components. Their superior adhesion to various substrates, excellent resistance to moisture and chemicals, and ability to maintain structural integrity under thermal cycling make them irreplaceable in applications such as molding compounds, die-attach adhesives, and glob-top coatings. The production process for these resins involves highly controlled synthesis and purification steps, often leveraging advanced chromatography and filtration technologies to achieve the required purity standards, typically measured in parts per million (ppm) or even parts per billion (ppb) for critical impurities like sodium, potassium, and chloride ions. This focus on material integrity differentiates this specialized market segment from the general epoxy resin market.

Driving factors for sustained market growth include the miniaturization trend in consumer electronics, which necessitates advanced encapsulation materials, and the rapid expansion of electric vehicles (EVs), requiring highly reliable power electronics and battery management systems insulated with ultra-pure dielectric materials. Furthermore, the increasing complexity of data centers and server infrastructure mandates the use of materials that ensure high-frequency signal integrity and prevent electrochemical corrosion over long operational lifespans. The critical benefits offered by these resins—such as enhanced reliability, extended device life, and improved thermal management—justify the premium pricing and fuel continuous innovation in resin formulations tailored for specific technological nodes and harsh environment performance requirements.

The High-Purity Epoxy Resin Market demonstrates robust growth driven primarily by escalating demand from the semiconductor and advanced electronics industries. Business trends indicate a strong focus on strategic partnerships between resin manufacturers and electronic device original equipment manufacturers (OEMs) to co-develop customized formulations, particularly low-stress, high-Tg (glass transition temperature) resins suitable for complex 3D stacking and advanced chip packaging techniques like flip-chip and wafer-level packaging. Companies are heavily investing in Asia Pacific, specifically in Taiwan, South Korea, and China, due to these regions serving as the global manufacturing hub for electronic components and integrated circuits, leading to intense capacity expansion and technological competition among key players focused on reducing metallic ion contamination levels. This competitive landscape favors suppliers who can consistently meet ultra-high purity specifications and offer scalable production processes.

Regionally, Asia Pacific maintains undisputed market leadership, fueled by government initiatives supporting domestic semiconductor fabrication (fabs) and the massive consumer base for electronics. North America and Europe, while having lower production volumes compared to APAC, exhibit strong demand for high-purity resins in niche, high-value sectors such as defense, aerospace, and high-reliability medical devices, where material qualification and traceability are rigorous. European market dynamics are also influenced by stringent environmental regulations, prompting research into bio-based or solvent-free high-purity epoxy systems. Latin America and MEA currently represent smaller market shares, but increasing foreign investment in telecommunications infrastructure and renewable energy projects suggests potential long-term growth, particularly for protective coatings in demanding environments.

Segmentation analysis highlights that the liquid resin segment dominates based on volume, utilized extensively in potting and casting applications, though the molding compound segment is expected to show the highest growth rate due to its critical role in advanced IC encapsulation. Application-wise, the semiconductor and electronic components segment remains the largest and fastest-growing, reflecting the relentless global demand for microprocessors, memory chips, and sensors required across virtually all modern technologies. Furthermore, the increasing adoption of wide-bandgap semiconductors (like SiC and GaN) in power electronics necessitates new, extremely high-purity epoxy formulations capable of handling higher operating temperatures and electrical fields, driving segment innovation and value capture across the supply chain.

Common user questions regarding the impact of Artificial Intelligence (AI) on the High-Purity Epoxy Resin market frequently center on how AI can enhance material discovery, optimize complex manufacturing processes, and improve quality control to meet ultra-high purity demands. Users are keen to understand if AI can accelerate the identification of novel curing agents or resin formulations that offer specific properties (e.g., lower CTE or higher breakdown voltage) necessary for next-generation chips and advanced packaging, thus shortening R&D cycles. Furthermore, inquiries often revolve around AI's ability to predict and prevent batch contamination in production lines, ensuring consistent output purity, and optimizing predictive maintenance for expensive synthesis reactors, thereby reducing downtime and increasing overall manufacturing efficiency. The consensus expectation is that AI will primarily serve as a powerful tool for accelerating innovation and ensuring stringent quality compliance, mitigating the high risks associated with material failure in critical electronic applications.

The dynamics of the High-Purity Epoxy Resin Market are shaped by a complex interplay of strong technological drivers and persistent structural constraints, amplified by significant opportunity spaces inherent in global technological shifts. Key drivers include the exponential growth in global semiconductor fabrication capacity, particularly in advanced nodes requiring superior encapsulation materials, and the rapid electrification of the automotive sector, demanding highly reliable power modules. Conversely, the market is restrained by the high capital expenditure required for establishing and maintaining ultra-clean manufacturing environments, the inherent volatility and dependence on petroleum-derived raw material prices (like Bisphenol A), and the exceptionally long and rigorous qualification cycles imposed by major electronic OEMs, which inhibit market entry and rapid product iteration. Opportunities arise from the development of high-performance epoxy systems for extreme environments, such as deep-sea cabling and high-altitude avionics, and the growing focus on sustainable, bio-based epoxy alternatives that maintain the required purity standards.

Impact forces significantly affecting market evolution include the intense rivalry among a limited number of specialized global chemical manufacturers, which necessitates continuous investment in proprietary purification technologies to maintain a competitive edge. The bargaining power of major end-users, primarily large semiconductor foundries and advanced packaging houses, is exceptionally high due to the critical nature of the material, meaning pricing power often remains constrained by stringent qualification and second-sourcing demands. Furthermore, the threat of substitution, while currently low due to the unique combination of electrical, mechanical, and thermal properties offered by high-purity epoxies, is monitored through the emergence of high-performance polyimides and silicone-based encapsulants in certain flexible electronics applications. Regulatory forces, particularly concerning hazardous substance control (e.g., RoHS, REACH), continually impact formulation choices and require proactive adaptation by manufacturers, influencing raw material selection and production location decisions.

In summary, the market's trajectory is strongly positive, largely dictated by macro-economic trends in digitalization and electrification. However, profitability remains sensitive to commodity price fluctuations and the high barrier to entry imposed by the demand for pristine material quality. Strategic success in this market relies on vertically integrated supply chains, proprietary purification intellectual property, and establishing long-term, deep collaborative relationships with Tier 1 electronics manufacturers to ensure early-stage involvement in next-generation product development, securing premium pricing and long-term contracts. The balance between meeting aggressive capacity expansion demands and maintaining zero-defect purity specifications represents the core operational challenge for industry participants moving forward.

The High-Purity Epoxy Resin Market is comprehensively segmented based on its chemical structure, physical form, application, and end-use industry, reflecting the diverse and highly specific requirements across different technological domains. The segmentation by type is crucial, distinguishing standard Bisphenol A derivatives from advanced systems like Bisphenol F, multifunctional epoxies (e.g., novolac types), and specialized cycloaliphatic epoxies, each offering tailored properties concerning heat resistance, chemical stability, and dielectric performance. By physical form, the market is divided into liquid, solid, and semi-solid (e.g., paste) formats, directly impacting the ease and method of application, such as dispensing, molding, or coating. The critical application segment covers areas from semiconductor encapsulation, which demands the highest purity levels, to advanced composite fabrication, where mechanical strength and thermal resilience are prioritized. Analyzing these segments provides a clear map of where technological growth and investment are concentrated, particularly highlighting the pivot towards materials compatible with high-density, multi-layer electronic assemblies.

The value chain for high-purity epoxy resins is characterized by high integration and rigorous quality control at every stage, starting from the upstream procurement of specialized chemical precursors. Upstream analysis focuses on key raw materials such as Epichlorohydrin (ECH) and various Bisphenols (A, F), which are high-volume commodity chemicals but must be sourced in grades amenable to ultra-purification. Given that the final resin purity is highly dependent on the initial quality and consistency of these precursors, suppliers often operate specialized purification facilities to minimize impurities before the synthesis stage. The intermediate manufacturing step involves the reaction and subsequent rigorous purification processes, which include distillation, solvent extraction, and advanced ion-exchange chromatography, representing the highest value-add stage and often relying on proprietary technology held by major chemical firms. Pricing pressures are often exerted at the raw material level, but the premium for the final high-purity product ensures substantial margin retention at the manufacturing level due to the high barrier to entry related to quality assurance.

Downstream analysis highlights the critical role of formulators and compounders who take the base high-purity resin and blend it with fillers (e.g., silica), curing agents, accelerators, and performance additives to create application-specific materials like molding compounds or liquid encapsulants. These formulators must maintain ultra-clean room conditions to prevent secondary contamination during compounding, adhering to strict cleanroom protocols (e.g., ISO Class 7 or 8). The distribution channel for these specialized materials is often direct or through highly trained technical distributors who can provide application support and ensure materials are handled correctly (e.g., maintaining specific temperature and moisture conditions) during transit and storage. Direct distribution dominates sales to Tier 1 semiconductor manufacturers, facilitating immediate technical feedback and joint qualification efforts, essential in this reliability-sensitive market.

The efficiency of the distribution system, both direct and indirect, is paramount, especially for materials with limited shelf life or stringent storage requirements. Indirect channels, typically involving specialized distributors, serve smaller OEMs and local assembly houses but require rigorous inventory management to prevent material aging or contamination. The ultimate success in the downstream market is defined by qualification approvals; once a resin formulation is qualified by a major semiconductor fab for a specific process (e.g., wire bonding or flip-chip underfill), the relationship often becomes long-term, creating sticky demand. Therefore, strategic efforts are concentrated on achieving qualification early in the product development cycle of high-volume electronics, making the technical support and responsiveness of the supplier a key differentiating factor in the overall value proposition.

The potential customers for High-Purity Epoxy Resins are primarily concentrated within industries where electronic reliability, thermal management, and dielectric integrity are non-negotiable operational requirements. The largest segment of buyers comprises semiconductor manufacturers (Foundries, IDMs) and outsourced semiconductor assembly and test (OSAT) companies, which use these resins extensively for chip encapsulation, protection of integrated circuits, and advanced device packaging. These customers demand resins with extremely low ionic content (often <5 ppm), excellent crack resistance, and superior adhesion under thermal cycling to ensure the reliability of components used in high-performance computing, mobile devices, and data centers. Procurement decisions in this sector are driven less by cost and more by qualification status, long-term supply agreements, and the supplier's capacity for rapid technical iteration to meet evolving packaging standards.

Another significant customer base resides within the aerospace and defense sector, including manufacturers of avionics, missile guidance systems, and satellite communication equipment. Here, the resins are used for structural bonding of composite parts and for potting critical electronic assemblies that must operate reliably under conditions of extreme temperature variation, high vibration, and exposure to aggressive chemicals or radiation. The qualification periods are typically the longest in this sector, requiring exhaustive testing and stringent documentation, emphasizing the need for suppliers to demonstrate robust quality control systems and long-term material consistency. Additionally, the growing electric vehicle (EV) industry, particularly component suppliers manufacturing battery management systems (BMS), power inverters, and charging infrastructure, represents a rapidly expanding buyer segment demanding high-thermal-stability epoxy materials for efficient heat dissipation and electrical isolation of high-voltage components.

Furthermore, medical device manufacturers, particularly those producing implantable devices, diagnostic equipment, and surgical instruments, rely on high-purity epoxies for biocompatible encapsulation and robust sealing. The inherent purity minimizes the risk of leaching toxic substances or causing corrosion, which is vital for patient safety and device longevity. Lastly, specialized electrical equipment manufacturers focusing on high-voltage transformers, switchgear, and renewable energy components (wind turbine pitch control systems, solar panel junction boxes) purchase these resins for their exceptional dielectric properties and resistance to environmental degradation. In all these critical end-use applications, the customers are seeking long-term partners capable of delivering consistently certified materials tailored to complex, demanding functional requirements, making technical collaboration a core component of the buyer-supplier relationship.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 4.8 Billion |

| Market Forecast in 2033 | USD 7.9 Billion |

| Growth Rate | 7.5% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Olin Corporation, Hexion Inc., Huntsman Corporation, Sika AG, Kukdo Chemical Co., Ltd., BASF SE, The Dow Chemical Company, Aditya Birla Chemicals (Thailand) Ltd., Nan Ya Plastics Corporation, Jiangsu Sanmu Group Co., Ltd., Emerald Performance Materials LLC, Chang Chun Group, Mitsubishi Chemical Corporation, Sumitomo Bakelite Co., Ltd., DIC Corporation, Shin-Etsu Chemical Co., Ltd., Nagase ChemteX Corporation, Wuxi Tianyuan Resin Co., Ltd., Epoxies, Etc., Atul Ltd. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technology landscape governing the High-Purity Epoxy Resin Market is highly advanced and focuses predominantly on achieving two critical objectives: maximizing purity and engineering advanced functional properties. Key technological advancements revolve around purification techniques, where sophisticated methods such as fractional distillation under high vacuum, membrane filtration, and proprietary ion-exchange resin columns are employed to systematically remove ionic contaminants, halide ions, and trace transition metals down to the ppb level. This intense focus on purification is necessary to meet the demanding specifications of advanced semiconductor packaging where ionic impurities can induce electrochemical migration, leading to device failure. Furthermore, continuous process monitoring technologies, including real-time spectroscopic analysis and advanced chromatography, are integrated into production lines to ensure batch-to-batch consistency and rapid detection of minute deviations from the required purity profile, setting a high technological entry barrier for new competitors.

Beyond purity, significant technological innovation is dedicated to formulating resins with specialized performance characteristics. This includes the development of low-stress epoxy molding compounds (EMCs) featuring reduced coefficient of thermal expansion (CTE) to minimize stress on delicate silicon dies during thermal cycling, particularly crucial for large dies and complex 3D chip stacks. Another critical area is the formulation of high-Tg (glass transition temperature) resins capable of operating reliably in high-power applications, such as power inverters in EVs, where temperatures can exceed 175°C. This often involves using modified Bisphenol F or epoxy novolac chemistries, coupled with high-functionality curing agents, to create a highly cross-linked polymer network that retains mechanical integrity and low dielectric loss at elevated temperatures and frequencies. The incorporation of nano-fillers and specialized coupling agents is also growing to enhance thermal conductivity while maintaining low viscosity for efficient processing.

The emerging technological focus includes the transition towards developing bio-based or renewable epoxy resin systems that meet high-purity standards, addressing growing sustainability mandates without compromising performance. Research efforts are targeting precursor chemicals derived from biomass (e.g., vegetable oils or lignin) to replace conventional petroleum-based Bisphenol A and F. Additionally, rapid curing technologies, such as UV-assisted or cationic polymerization systems, are gaining traction, especially in high-throughput manufacturing environments like wafer-level packaging, reducing processing time and increasing production throughput while maintaining dimensional stability and stress mitigation. The confluence of ultra-purification science, advanced materials engineering, and process automation defines the cutting-edge of the high-purity epoxy resin technology landscape, continually pushing the boundaries of material capability to enable smaller, faster, and more reliable electronic devices.

The primary driver is the rapid global expansion of the semiconductor and microelectronics industries, particularly the shift towards advanced, high-density packaging (3D stacking, flip-chip) which demands materials with extremely low ionic impurities (often less than 5 ppm) to ensure device reliability, thermal stability, and long operational life, mitigating failure risks.

Purity is strictly defined by the maximum permissible concentration of critical ionic contaminants (like chloride, sodium, and potassium ions) and organic volatiles, typically measured in parts per million (ppm) or parts per billion (ppb). Measurement relies on advanced analytical techniques such as Ion Chromatography (IC) and ICP-MS (Inductively Coupled Plasma Mass Spectrometry) to ensure compliance with industry standards and customer specifications.

The Semiconductors and Electronics industry holds the largest market share, utilizing these resins extensively for critical applications including molding compounds for integrated circuits, die-attach adhesives, and encapsulation/potting of sensitive components vital for computing and communication devices.

The main challenges involve maintaining zero-defect purity during large-scale synthesis and compounding, managing high capital costs associated with ultra-clean manufacturing facilities, sourcing consistently high-grade precursors, and navigating lengthy and expensive qualification processes imposed by major electronics manufacturers.

The EV sector significantly impacts the market by driving demand for high-thermal-stability, high-dielectric strength epoxy resins essential for insulating and protecting high-voltage power electronics (inverters, converters) and battery management systems (BMS) against thermal runaway and electrical failures, ensuring reliable vehicle performance.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.