ID : MRU_ 437310 | Date : Dec, 2025 | Pages : 249 | Region : Global | Publisher : MRU

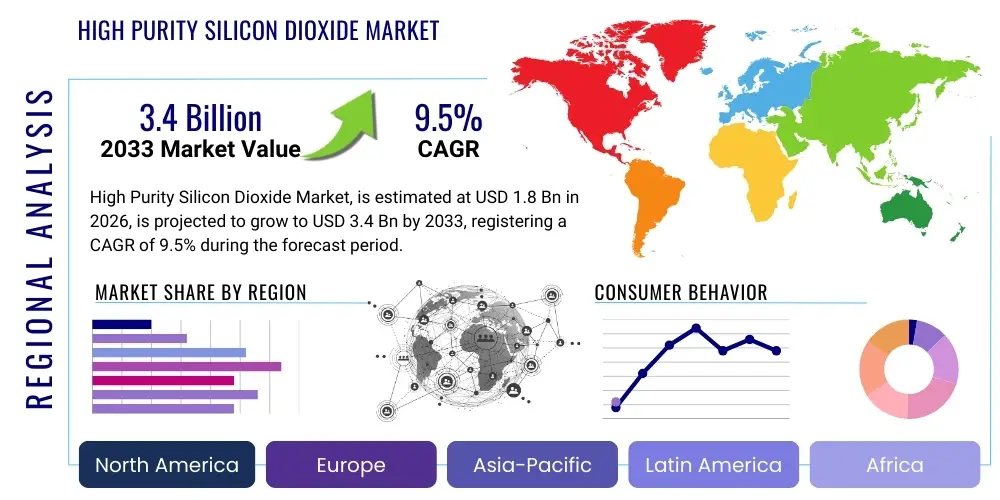

The High Purity Silicon Dioxide Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 9.5% between 2026 and 2033. The market is estimated at USD 1.8 Billion in 2026 and is projected to reach USD 3.4 Billion by the end of the forecast period in 2033. This substantial expansion is fundamentally driven by the relentless demand from high-tech industries, particularly semiconductors, advanced optics, and specialized solar photovoltaic applications, all of which require silicon dioxide materials with minimal metallic impurities and defect concentrations.

The exceptional growth trajectory reflects the accelerating globalization of advanced manufacturing capabilities, especially in Asia Pacific, where significant investments are being made in fabrication plants (fabs) and sophisticated optical component production. High Purity Silicon Dioxide (HPSD) serves as a critical enabling material in these sectors, providing essential properties like excellent electrical insulation, high thermal stability, and superior optical transmission. As device geometries shrink in semiconductor chips (e.g., transitioning to 3nm and 2nm nodes) and data transmission speeds increase, the tolerance for impurities in raw materials like HPSD diminishes, thereby elevating the value and complexity of purification processes and driving market revenue growth.

The High Purity Silicon Dioxide Market encompasses the production and supply of silicon dioxide (SiO2) characterized by exceptionally low levels of metallic and non-metallic contaminants, often measured in parts per billion (ppb) or parts per trillion (ppt). This specialized material, distinct from commodity-grade silica, is foundational to modern microelectronics and photonics. High purity requirements are mandated because even trace impurities can significantly degrade the performance, reliability, and lifespan of highly sensitive components, such as transistors, optical fibers, and complex lithography systems. Key methods for achieving this purity include advanced chemical synthesis, purification of natural quartz (fused silica), and sophisticated deposition techniques like Chemical Vapor Deposition (CVD) or Flame Hydrolysis. The primary product forms include fused silica glass, high-purity silica powder, and synthetic amorphous silica, each tailored for specific industrial applications.

Major applications of HPSD are heavily concentrated in the electronics industry, where it is utilized as an insulating layer, passivation layer, and dielectric material in Integrated Circuits (ICs). In the optical sector, HPSD is indispensable for manufacturing preforms for optical fibers, critical components in telecommunications infrastructure, owing to its superior transparency and low attenuation characteristics. Furthermore, its use extends to specialized crucibles and furnace components required for silicon wafer growth and high-temperature processing in semiconductor and solar manufacturing, where material stability and purity are paramount to avoid contaminating the processed wafers. The intrinsic benefits of HPSD—including high dielectric strength, low thermal expansion, and resistance to chemical etching—make it irreplaceable in these demanding environments, driving consistent market demand.

The market is primarily driven by the exponential growth of data centers, the rollout of 5G and 6G networks requiring high-capacity fiber optic cables, and the continuous innovation within semiconductor technology (Moore's Law). Increased government and private investment in advanced manufacturing capabilities, particularly in regions aiming for technological self-sufficiency, further fuels market expansion. The shift towards higher-performance computing, artificial intelligence processing, and the proliferation of IoT devices necessitates increasingly complex and dense ICs, which, in turn, heighten the demand for ultra-high purity materials like HPSD to maintain yield and reliability targets.

The High Purity Silicon Dioxide market is entering a robust growth phase, principally propelled by structural shifts in global technology production and increasing stringency regarding material quality in microelectronics. Business trends indicate a strong movement towards vertical integration among key players, securing control over specialized purification technologies and raw quartz sourcing to ensure supply chain stability and maintain competitive advantage in purity standards. Strategic partnerships between HPSD suppliers and large-scale semiconductor foundries (fabs) are becoming common, focusing on co-development of materials suited for extreme ultraviolet (EUV) lithography and advanced deposition processes. Geographical market dominance is shifting further toward the Asia Pacific region, primarily driven by massive government and corporate capital expenditure directed toward semiconductor manufacturing capacity expansion in Taiwan, South Korea, and China.

Segment trends highlight the exceptional growth within the fused silica glass segment, specifically utilized in optical preforms and deep UV optics components. Simultaneously, the market for high-purity silica powders, essential for chemical mechanical planarization (CMP) slurries and specialty fillers, is also expanding due to increased semiconductor wafer processing volumes. The demand for synthetic HPSD derived from silane or synthetic quartz is outpacing natural quartz derivatives, reflecting the industry’s preference for materials that offer greater control over chemical composition and defect structure, though often at a higher cost. These segmented trends underscore the market’s bifurcation: while traditional electronics still use significant volumes, the steepest growth lies in ultra-specialized, high-value applications demanding the highest purity levels achievable.

Regional analysis confirms that Asia Pacific holds the largest market share and exhibits the highest growth potential, directly correlating with its status as the global hub for semiconductor and advanced consumer electronics production. North America and Europe, while representing mature markets, maintain significant influence through specialized R&D and manufacturing of highly complex components, such as EUV masks and precision optical systems. Investment activities in these Western regions are often focused on technological innovation and supply chain resilience rather than purely volume expansion. This global investment strategy ensures that the HPSD market remains globally competitive, highly localized around major technology manufacturing clusters, and intensely focused on continuous improvement in material science.

User queries regarding AI's impact on the High Purity Silicon Dioxide market generally center on three main themes: the increased demand for high-performance computing hardware required to run AI models, the role of AI in optimizing HPSD production processes, and the potential for AI-driven material discovery. Users are concerned about how AI's rapid growth will strain the supply of critical materials necessary for advanced processors (GPUs, TPUs), many of which rely heavily on HPSD for insulating layers and packaging. There is also significant curiosity about whether AI algorithms can be deployed in quality control to rapidly identify trace impurities in HPSD materials, thereby improving manufacturing yields and lowering costs. Expectations are high that AI will accelerate the iteration cycles in R&D, potentially leading to novel, high-purity materials or more efficient synthetic routes, which could dramatically alter the competitive landscape of the market.

The most immediate and significant impact of Artificial Intelligence on the HPSD market is the surge in demand for semiconductor components integral to AI infrastructure, such as advanced logic chips and specialized memory. These chips, used in data centers and edge devices for running complex AI models, require denser transistor integration and superior thermal management, directly translating into a heightened need for ultra-pure dielectrics and encapsulation materials, largely supplied by HPSD manufacturers. The relentless pursuit of higher computational speed necessitates increasingly sophisticated wafer fabrication processes, demanding higher-quality HPSD products to ensure the integrity and reliability of sub-nanometer circuitry.

Furthermore, AI and machine learning are being integrated into the manufacturing process of HPSD itself. Predictive maintenance systems and real-time process control, powered by AI, enable manufacturers to fine-tune reaction parameters during synthesis or purification, maximizing output purity and minimizing batch variations. By analyzing vast datasets derived from spectroscopic analysis and quality control checks, AI models can detect subtle deviations indicating contamination earlier than traditional methods, resulting in improved operational efficiency and reduced waste. This adoption of smart manufacturing practices is crucial for meeting the stringent purity requirements demanded by next-generation chip makers.

The dynamics of the High Purity Silicon Dioxide market are governed by a critical interplay of strong technological drivers, significant regulatory restraints, and immense potential opportunities rooted in emerging technologies. The primary driving force is the foundational role HPSD plays in enabling Moore's Law, specifically the requirement for higher dielectric constants and lower leakage currents in scaled-down transistor architectures. Restraints largely involve the high capital intensity and complexity associated with achieving and maintaining ultra-high purity standards (especially removing trace metals like alkali ions) and the concentrated nature of the raw material supply chain. Opportunities are particularly rich in innovative applications, such as specialized materials for quantum computing components and the rapidly expanding market for high-bandwidth passive optical networking (PON) infrastructure, demanding next-generation optical fibers.

Drivers: The global rollout of 5G and fiber-to-the-home (FTTH) networks is a major driver, necessitating vast quantities of high-purity fused silica for optical fiber production. Furthermore, the persistent push for miniaturization and enhanced performance in microelectronic devices mandates the use of increasingly pure SiO2 films as gate oxides and inter-level dielectrics. The shift towards advanced packaging techniques, such as 3D integration and wafer-level packaging, also relies heavily on specialized HPSD formulations for thermal management and insulation. The semiconductor industry’s capital expenditure, particularly the construction of new fabrication plants globally, directly correlates with increased HPSD consumption, as initial tooling and ongoing process materials heavily rely on ultra-pure silica derivatives.

Restraints: The market faces significant hurdles due to the extremely high energy consumption and technological complexity inherent in the purification processes (e.g., thermal treatment, chlorination, and plasma etching). The cost of raw materials, particularly high-grade natural quartz, and the intellectual property controlling advanced synthetic methods, create high barriers to entry, leading to an oligopolistic market structure. Moreover, stringent regulatory standards related to environmental impact and worker safety in chemical processing facilities, combined with the difficulty of scaling ultra-high purity production without introducing defects, pose substantial constraints on rapid market expansion.

Opportunities: Emerging high-growth areas present lucrative opportunities. The development of advanced lithography techniques, particularly EUV, demands extremely high-purity synthetic fused silica for critical lens, mirror, and mask substrates, offering premium pricing potential. The increasing adoption of solar energy components, which require high-purity quartz crucibles for melting silicon feedstock, provides a steady, expanding demand base. Furthermore, R&D focused on alternative synthesis methods, such as sol-gel processes for specialized HPSD powders used in advanced coatings and biomedical applications, offers diversification prospects beyond traditional electronics and optics.

The High Purity Silicon Dioxide market is systematically segmented based on product type, application, and end-use industry, reflecting the diverse purity requirements and functional roles of the material across various technological domains. Product segmentation distinguishes between the physical form and origin, encompassing synthetic derivatives (offering superior control over impurity levels) and refined natural quartz (providing a cost-effective solution for less demanding applications). Application segmentation highlights the material's critical function, ranging from insulating layers in ICs to structural components in laboratory equipment. End-use segmentation clearly defines the primary consuming industries, dominated by electronics, followed by optics and solar energy, each imposing unique purity and form requirements on the suppliers.

The value chain for High Purity Silicon Dioxide begins with rigorous upstream activities involving the extraction and selection of high-grade quartz ore or the sourcing of precursor chemicals like silanes and silicon tetrachloride. For natural quartz, the initial purification steps, including acid washing and flotation, are critical to reduce major contaminants. For synthetic HPSD, the production process, often involving flame hydrolysis or vapor deposition, represents the most capital-intensive and technologically sensitive stage, as purity must be guaranteed at the atomic level. This upstream control over raw material quality and initial synthesis dictates the final achievable purity and, consequently, the market application for the finished product.

Midstream activities involve processing the HPSD into specific forms—whether milling the powder, drawing fused silica into tubes, or manufacturing complex optical blanks and components. This stage includes precision machining, surface finishing, and advanced metrology to certify the material meets strict performance specifications, particularly for optical transmission and thermal stability. Distribution channels are highly specialized; due to the sensitive nature and high value of the product, direct sales and established, secure supply lines are preferred. Indirect channels, typically specialized chemical distributors, handle lower-volume or less critical applications, maintaining strict protocols to prevent contamination during handling and transport.

Downstream analysis focuses on integration into end-user manufacturing processes. In the semiconductor industry, HPSD materials are consumed in wafer fabrication, often requiring just-in-time delivery and technical support for integration into CVD or etching machines. For telecommunications, preforms are drawn into finished optical fiber. The reliance on direct sales ensures tight collaboration between HPSD producers and major consumers (e.g., semiconductor foundries, major fiber optic cable manufacturers) to address immediate performance issues and future material requirements based on evolving technological roadmaps (e.g., new lithography wavelengths or fiber designs).

The primary customers for High Purity Silicon Dioxide are large-scale manufacturers operating within highly regulated and technologically demanding industries where material integrity is non-negotiable. Leading semiconductor fabrication plants (fabs) represent the most critical customer segment, utilizing HPSD for nearly every step of the wafer processing cycle, from the crucibles used for crystal growth to the dielectric layers within the final chip structure. These customers seek materials certified to the highest purity standards (typically 5N to 7N purity) to maximize device yield and reliability, making supplier qualification processes extremely rigorous and long-term relationships essential.

Another major customer group consists of manufacturers in the optical and telecommunications sectors, specifically those producing fiber optic cables, specialty optics for scientific instrumentation, and components for high-power lasers. These customers demand specific optical properties, such as low hydroxyl content and excellent UV/IR transmission, which are critical for maximizing data transmission efficiency and component longevity. Additionally, large industrial enterprises involved in high-temperature material processing, such as specialized metallurgical and solar photovoltaic companies, require HPSD products, particularly high-purity quartz crucibles, for melting and processing silicon and other specialized metals under contamination-free conditions.

Finally, research institutions, advanced material developers, and manufacturers of complex measuring instruments (e.g., mass spectrometers, interferometers) also form a niche but highly valuable customer base. These organizations often require small volumes of bespoke, ultra-specialized HPSD forms tailored for experimental purposes or highly sensitive tooling, representing a segment that drives innovation and demands the forefront of material science capability from suppliers. The purchasing decision for all these segments is driven less by cost and predominantly by verified purity, consistency, and a strong history of supply chain resilience.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 1.8 Billion |

| Market Forecast in 2033 | USD 3.4 Billion |

| Growth Rate | CAGR 9.5% |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Shin-Etsu Chemical Co., Ltd., Heraeus Group, Momentive Technologies, Tosoh Corporation, Applied Materials Inc., Wacker Chemie AG, Cabot Corporation, Evonik Industries AG, The Quartz Corp., Unimin Corporation (Sibelco), China Glass Holdings Limited, Kropfmühl GmbH (AMG), Russian Quartz, Lianyungang High-Purity Quartz, Saint-Gobain S.A. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological landscape of the High Purity Silicon Dioxide market is defined by sophisticated purification and synthesis methods aimed at minimizing defect density and controlling trace metal contamination. A cornerstone technology is Flame Hydrolysis Deposition (FHD), primarily used for manufacturing synthetic fused silica preforms for optical fibers, where precise control over refractive index profiles and hydroxyl content is paramount. Another critical set of technologies involves Chemical Vapor Deposition (CVD) and Plasma-Enhanced CVD (PECVD), which utilize silane or TEOS (Tetraethyl orthosilicate) precursors to deposit ultra-pure, uniform SiO2 films onto semiconductor wafers, forming gate dielectrics and passivation layers. Advancements in PECVD systems, specifically those employing remote plasma technology, are crucial for achieving lower thermal budgets and higher film quality necessary for advanced node manufacturing.

For high-purity quartz crucibles and components derived from natural sources, the technology centers around advanced mineral processing and multi-stage purification. This includes specialized acid leaching, floatation, high-temperature chlorination, and vacuum sintering techniques designed to remove difficult-to-isolate contaminants like aluminum, titanium, and alkali metals, which are detrimental in high-temperature semiconductor processing. Continual innovation in metrology is equally important; technologies like Inductively Coupled Plasma Mass Spectrometry (ICP-MS) and Atomic Absorption Spectroscopy (AAS), alongside optical characterization methods, are constantly being refined to accurately measure impurities down to the sub-ppt level, providing the necessary quality assurance required by downstream users.

Future technological advancements are focused on developing solvent-free, environmentally benign synthesis routes and enhancing the circular economy through recycling. Research into laser-based purification and advanced crystallization methods aims to produce ultra-high purity materials with fewer structural defects than current conventional processes. Furthermore, there is significant ongoing research into modifying HPSD surfaces at the nanoscale using specialized coatings and treatments to improve adhesion, chemical resistance, and dielectric properties, essential for next-generation devices such as high-frequency integrated circuits and MEMS sensors. The integration of process analytical technology (PAT) leveraging AI also represents a technological shift, moving from post-process quality control to real-time, in-line defect management.

The regional dynamics of the High Purity Silicon Dioxide market are heavily skewed toward Asia Pacific (APAC), which stands as the global epicenter for high-tech manufacturing. APAC’s dominance is underpinned by massive investment in semiconductor foundries in regions such as Taiwan, South Korea, and mainland China, coupled with the world's largest consumer electronics manufacturing base. These regions drive demand not only for HPSD in IC fabrication but also for related applications, including advanced display panels and extensive fiber optic network deployment. The strategic governmental push for domestic semiconductor self-sufficiency further catalyzes demand for all upstream materials, including high-purity quartz and synthetic silica. Rapid urbanization and the deployment of 5G infrastructure throughout Southeast Asia also contribute significantly to the high growth rate observed in APAC.

North America holds a pivotal position in the high-end, specialty segment of the market, particularly in R&D and the production of complex optical systems, aerospace components, and advanced scientific instruments. While volume consumption might be lower than APAC, the region commands premium pricing for ultra-specialized HPSD used in sophisticated lithography systems (like EUV) and defense applications. Recent initiatives to revitalize domestic semiconductor manufacturing (e.g., through government acts) are expected to significantly boost internal consumption of HPSD materials over the forecast period, emphasizing supply chain security and domestic sourcing for critical materials.

Europe represents a mature market focusing heavily on optical communication, automotive electronics, and specialized industrial applications. European companies are global leaders in high-purity quartz component manufacturing, leveraging deep expertise in material science and precision engineering. The demand here is stable and high-value, driven by stringent quality requirements in industrial lasers, medical technology, and advanced telecommunication components. The MEA and Latin America regions currently constitute smaller market shares, but demand is growing, particularly fueled by infrastructure projects, expanding solar energy installations, and increasing foreign direct investment in localized assembly and manufacturing hubs.

The key differentiator is the impurity level; HPSD typically contains trace metals and alkali elements measured in parts per billion (ppb) or parts per trillion (ppt), whereas commodity silica is measured in parts per million (ppm). This ultra-low contamination is essential for semiconductor yields and critical optical clarity.

The Electronics and Semiconductors industry is the largest consumer. HPSD is critical for manufacturing ICs (as dielectrics, insulators), silicon wafer crucibles, and specialized components required for advanced photolithography processes, driving massive volume and value demand.

5G necessitates extensive deployment of high-capacity fiber optic networks and complex front-end modules in devices. This drives demand for ultra-pure fused silica for optical fiber preforms and high-quality dielectric layers in high-frequency semiconductor components required for 5G base stations and devices.

The main challenges involve achieving repeatable, consistent purity below the ppb level, effectively managing process contamination, and controlling the distribution of structural defects (like hydroxyl groups) during synthesis, particularly in high-volume production required for semiconductor manufacturing.

HPSD, specifically ultra-pure synthetic fused silica, is essential for fabricating the complex reticles (masks) and specialized optical components (mirrors and lenses) used in Extreme Ultraviolet (EUV) lithography tools. Its superior homogeneity and resistance to thermal expansion are crucial for the nanometer-scale precision required.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.