ID : MRU_ 436106 | Date : Dec, 2025 | Pages : 251 | Region : Global | Publisher : MRU

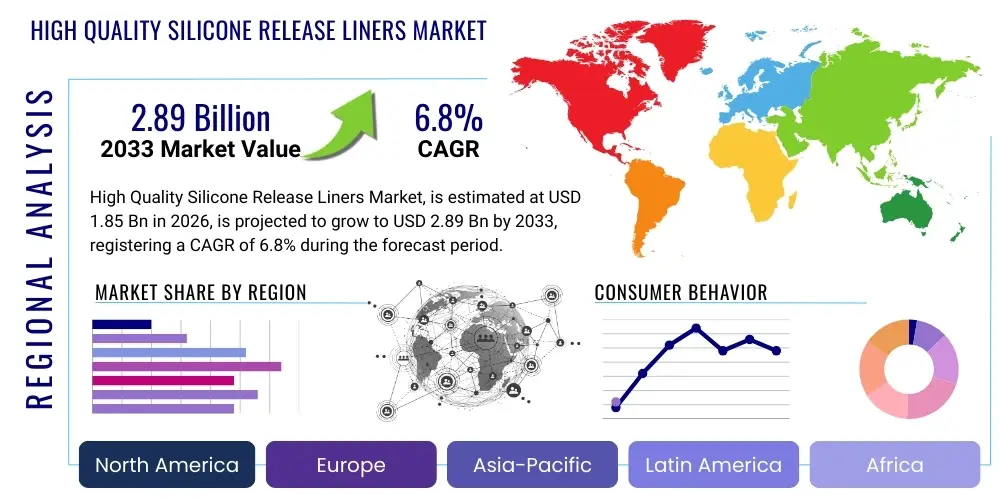

The High Quality Silicone Release Liners Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2026 and 2033. The market is estimated at $1.85 Billion in 2026 and is projected to reach $2.89 Billion by the end of the forecast period in 2033.

The High Quality Silicone Release Liners Market encompasses advanced materials utilized to protect adhesive surfaces until they are ready for application. These liners consist primarily of a substrate—such as film (PET, PP, PE) or specialty papers (Glassine, CCK, SCK)—coated with a finely tuned silicone release agent. High quality in this context refers to precision manufacturing, consistent release characteristics (peel force), low extractables, and superior barrier properties necessary for demanding applications like medical diagnostics, high-performance tapes, aerospace composites, and multilayer electronic assemblies. The demand for flawless, residue-free surfaces in mission-critical applications mandates the use of these specialized, high-tolerance liners, driving market expansion particularly in regulated and high-value industrial sectors. These products are crucial intermediaries, ensuring the integrity and functionality of sensitive adhesive systems across various stages of manufacturing and end-use.

The primary function of these silicone release liners is to offer controlled differential release characteristics, allowing the liner to be removed smoothly without compromising the adhesive layer or leaving behind silicone residue, which is critical in industries such as electronics and wound care. Major applications include protective films for displays, sophisticated medical transdermal patches, release sheets for prepregs in composite manufacturing (e.g., carbon fiber), and high-speed automatic labeling systems. The increasing complexity of modern adhesives, often requiring ultra-light release forces and exceptional dimensional stability, directly fuels the need for technologically superior release liners. Furthermore, the push towards sustainability is encouraging innovation in using thinner film substrates and developing solvent-less silicone curing chemistries, offering environmental benefits alongside performance improvements.

Key benefits derived from utilizing high quality silicone release liners include maintaining the adhesive performance over extended periods, providing mechanical protection during handling and transportation, and facilitating streamlined, high-speed automated application processes. Driving factors for market growth include the robust expansion of the global medical and healthcare sectors, particularly in advanced wound dressings and wearable medical devices; the surging demand for lightweight composite materials in automotive and aerospace industries; and the continuous proliferation of sophisticated electronic devices requiring specialized temporary protective films. The necessity for reliable, consistent performance in demanding industrial environments ensures sustained investment and growth within this highly specialized segment of the packaging and industrial materials market.

The High Quality Silicone Release Liners Market is experiencing robust growth fueled by accelerated demand from niche, high-value end-use sectors, predominantly healthcare and advanced manufacturing. Business trends indicate a strong focus on sustainable product development, shifting from solvent-based toward UV and thermal solvent-less silicone curing technologies to meet stringent environmental regulations and reduce volatile organic compound (VOC) emissions. Furthermore, strategic consolidations and investments in high-precision coating assets are defining the competitive landscape, emphasizing consistency and scalability. Regional trends show Asia Pacific leading both consumption and production growth, driven by rapid industrialization, particularly in electronics and electric vehicle battery manufacturing, where precise release characteristics are paramount. North America and Europe maintain stable demand, focusing heavily on medical-grade and pharmaceutical applications, adhering to strict quality standards and traceability requirements.

Segment trends reveal that film-based liners, particularly Polyethylene Terephthalate (PET) and specialized polyolefins, are gaining traction over traditional paper substrates in applications demanding superior dimensional stability, strength, and transparency, such as flexible electronics and specialized tapes. Within the silicone type segment, solvent-less technologies are becoming the standard, displacing older solvent-based systems due to operational efficiencies and regulatory pressures. The application segment growth is primarily propelled by advanced tapes, including double-sided and specialty mounting tapes, and the high-growth composites industry, which requires wide-width, heat-resistant liners for prepreg manufacturing. Manufacturers are increasingly differentiating their offerings based on technical support, customizability of release levels (easy, medium, tight), and compliance documentation.

The market outlook remains positive, underpinned by continuous technological evolution aimed at achieving ultra-light, residue-free release mechanisms essential for next-generation products. Challenges such as fluctuating raw material costs (especially silicon metal) and the need for high capital expenditure for new coating lines are being offset by the high profitability associated with specialized, high-quality offerings. Companies are focusing their research and development efforts on improving barrier properties, enhancing recyclability of the substrates, and integrating smart manufacturing processes, including AI-driven quality checks, to minimize variation and maintain high throughput. This ensures that the market structure remains highly dependent on technical expertise and product consistency, favoring established players with comprehensive portfolios and robust quality management systems.

User inquiries frequently center on how Artificial Intelligence (AI) and Machine Learning (ML) can optimize complex manufacturing processes inherent in high-quality release liner production, specifically focusing on defect detection, material waste reduction, and predictive maintenance of high-speed coating lines. Users also show keen interest in AI's role in optimizing supply chain logistics—managing volatile raw material costs (silicone, substrate papers/films) and predicting demand fluctuations across diverse end-use sectors like medical adhesives and automotive composites. Key concerns revolve around the implementation costs of AI systems and the need for specialized data infrastructure to handle proprietary process data, particularly regarding confidential silicone formulations and coating parameters. The overarching expectation is that AI integration will lead to unprecedented quality consistency and cost efficiency, fundamentally reshaping the competitive landscape among major producers, ensuring tighter specifications required by high-end consumers.

The primary area of AI integration is in quality assurance and process control. High-quality silicone release liners demand micron-level precision regarding coat weight, curing temperature, and web tension. Traditional optical inspection systems can identify defects, but AI-powered vision systems, utilizing deep learning algorithms, can classify subtle flaws in real-time—such as pinholes, voids, or minor inconsistencies in the silicone layer—that are often missed by conventional methods. This ability to instantly adjust process parameters based on defect prediction minimizes waste of expensive raw materials, improving yield rates dramatically. Furthermore, AI models are being deployed to manage the complex, non-linear relationships between curing kinetics, catalyst loading, and line speed, ensuring optimal cross-linking density and consistent release profiles batch after batch, which is paramount for medical and electronic applications.

Beyond the factory floor, AI is transforming material procurement and strategic sourcing. Given the dependency on silicon metal and specific polymers for substrates, which are subject to significant price volatility and supply chain disruption, ML algorithms are used for granular forecasting and risk analysis. These models integrate macroeconomic data, commodity exchange prices, and historical internal consumption patterns to provide predictive insights, allowing procurement teams to optimize inventory levels and hedge against cost increases. This strategic use of AI enhances operational resilience, ensuring steady supply even during periods of geopolitical uncertainty or unforeseen logistical bottlenecks, thereby safeguarding production capacity for high-margin products.

The market dynamics for High Quality Silicone Release Liners are governed by a robust interplay of driving forces centered on industrial modernization and high-tech application growth, balanced against significant constraints relating to manufacturing complexity and cost volatility. The primary drivers include the exponential expansion of the electric vehicle (EV) sector, which requires specialized release liners for battery thermal management adhesives and structural components, and the burgeoning global healthcare market, especially for sophisticated transdermal drug delivery systems and advanced wound care. Opportunities arise from the transition to sustainable, bio-based substrates and the commercialization of specialized liners capable of handling extremely thin film adhesives used in flexible electronics. Restraints primarily involve the high capital investment required for state-of-the-art coating equipment, stringent regulatory hurdles (especially for medical-grade products), and the fluctuating global prices of key inputs, notably silicone polymers and specialized paper pulp or PET films. These forces collectively shape the competitive strategy, pushing manufacturers towards high-precision, vertically integrated operations.

Impact forces dictate the strategic priorities for market participants. Technological sophistication acts as a multiplier, favoring companies that can consistently deliver ultra-light and differential release coatings. The regulatory environment, particularly the ISO 13485 standard for medical devices, heavily impacts market access and investment decisions, pushing quality control to the forefront. Furthermore, competitive intensity compels firms to continuously innovate, offering bespoke solutions rather than standardized products. The increasing focus on circular economy principles and recyclability mandates research into release liners that are easier to de-siliconize or manufactured from recycled content, significantly impacting long-term product development cycles. These external and internal pressures ensure that only highly specialized, technically proficient companies can thrive in the high-quality segment.

Specific market pressures related to sustainability have intensified the pursuit of solvent-less silicone systems, minimizing the environmental footprint associated with manufacturing. While this transition presents an opportunity for technological leadership, it also necessitates substantial retooling of older production facilities, acting as a short-term financial restraint. The high performance demands from key end-users, such as aerospace and automotive prepreg manufacturers, necessitate liners with exceptional thermal stability and minimal contamination risk, which limits the number of qualified suppliers. Successfully managing the high barrier to entry—encompassing technical expertise, capital investment, and rigorous qualification processes—is crucial for firms aiming to capitalize on the sustained, high-margin growth characterizing this specialized sector.

The High Quality Silicone Release Liners Market is meticulously segmented based on substrate material, silicone coating technology, specific application, and the ultimate end-use industry, reflecting the diverse and specialized requirements of its consumers. This granular segmentation is essential as the required release performance (peel strength, stability, residue content) varies dramatically depending on whether the liner is used for medical tapes, automotive paints protection films, or composite prepregs. The differentiation between film and paper substrates is particularly significant, with films dominating high-dimensional stability applications, while specialty papers retain market share in labeling and standard tape contexts. Understanding these segments allows manufacturers to tailor their production assets and marketing strategies to address specific high-value niches effectively.

Segmentation by silicone chemistry—solvent-less, solvent-based, and emulsion—reflects the evolution of manufacturing technology and regulatory compliance. Solvent-less systems, favored for their environmental advantages and high-speed applicability, are rapidly becoming the dominant technology, especially in new installations. The application segmentation highlights key growth vectors, with advanced wound dressings and high-temperature industrial tapes showing above-average growth rates. Furthermore, the segmentation by end-use industry, particularly the rise of sophisticated sectors like electric mobility and flexible electronics, dictates the specifications for heat resistance, surface smoothness, and optical clarity required from the release liners.

Each segment presents unique technical hurdles and market opportunities. For instance, the medical segment demands biocompatibility and extremely tight control over extractable compounds, leading to higher average selling prices (ASPs). Conversely, the standard label and graphic arts segments, while requiring high throughput, are generally more price-sensitive but offer larger volume potential. The overall segmentation structure confirms that high quality is not a singular concept but a spectrum of specialized performance attributes customized to meet the exacting demands of modern industrial processes, emphasizing precision engineering at every layer of the product construction.

The value chain for high quality silicone release liners is complex, starting with the upstream sourcing of specialized raw materials and extending through highly technical coating processes to diverse downstream converters and end-users. Upstream analysis focuses on the procurement of silicone polymers (polydimethylsiloxanes) and their corresponding catalysts, sourced from major chemical and specialty silicone manufacturers. Concurrently, specialized substrates—including high-density PET films, solvent-free cured papers (CCK, SCK), or proprietary polyolefin blends—are sourced from paper mills or polymer film extruders. The quality and purity of these raw inputs are critical, directly impacting the final release properties and the potential for contamination, particularly in medical and electronics applications. Price volatility and supply concentration in these raw material markets present significant margin risks for coaters.

The midstream involves the core manufacturing process: the precision application and curing of the silicone layer onto the substrate. This stage demands sophisticated, high-speed coating machinery and proprietary formulations to achieve specified coat weights and release values. Manufacturers invest heavily in in-house R&D to optimize curing processes (thermal, UV, e-beam) and minimize silicone migration. Distribution channels are typically dual: direct sales to large, specialized converters or integrated end-users (e.g., medical device manufacturers) for bespoke, high-volume orders, and indirect distribution through specialized regional distributors or agents for smaller volume or general-purpose products. The direct channel offers greater control over quality assurance and technical support, which is critical for high-quality product lines.

Downstream analysis centers on the customers—the pressure-sensitive adhesive (PSA) converters, label manufacturers, and industrial users who combine the release liner with adhesive and face stock to create the final product. The performance of the release liner directly affects the converter’s processing efficiency (die-cutting, laminating). End-users demand stringent technical documentation, traceability, and batch consistency, especially in regulated industries like aerospace and healthcare. The value chain is characterized by strong partnerships and technical collaboration between silicone coaters and high-end users, aimed at co-developing liners perfectly matched to new adhesive chemistries and processing speeds, thereby securing long-term contracts and sustaining high margins in this highly technical market segment.

Potential customers for High Quality Silicone Release Liners are concentrated in industries that utilize highly specialized adhesive systems requiring flawless protection and consistent, customized release properties. The dominant customer base includes sophisticated manufacturers in the healthcare sector, particularly those producing advanced wound dressings, transdermal patches (requiring tightly controlled release rates), and surgical drapes where biocompatibility is non-negotiable. Another crucial customer segment is the automotive and aerospace industry, specifically companies involved in composite prepreg manufacturing (carbon fiber and fiberglass), demanding liners that withstand high curing temperatures and prevent contamination while maintaining structural integrity during handling. These customers prioritize technical specifications, regulatory compliance, and supplier reliability over mere cost.

The electronics industry represents a rapidly expanding segment, with demand originating from manufacturers of flexible printed circuits, display protective films (for smartphones and monitors), and components requiring temporary masking during manufacturing or precise mounting via double-sided tapes. These applications often necessitate filmic substrates (PET) for exceptional clarity and dimensional stability. Furthermore, high-performance tape manufacturers (e.g., 3M, Tesa) are major buyers, integrating these liners into their specialty products used in construction, sealing, and industrial assembly, often demanding differential release coatings—a high release on one side and a medium release on the other—to facilitate complex layered products.

In summary, the key buyers are specialized converters and vertically integrated end-users who treat the release liner as a critical component of their final product’s performance, rather than just a packaging material. Their purchasing decisions are heavily influenced by quality certifications (ISO 9001, ISO 13485), technical consistency (Coat Weight Standard Deviation), and the supplier's capability to provide global technical support and customized chemical formulations to match proprietary adhesive systems. This reliance on precision and specialization creates a high barrier to entry for new suppliers.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | $1.85 Billion |

| Market Forecast in 2033 | $2.89 Billion |

| Growth Rate | 6.8% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Loparex, Mondi Group, Sappi, SJA, Siliconature, Saint-Gobain, Gascogne, Wausau Coated Products, 3M, Flexcon, KRK, Avery Dennison, UPM Specialty Papers, Rayven, Shurtape, Lintec, Daubert, H-H, Grafix, Fox River |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The High Quality Silicone Release Liners market is defined by technological sophistication, primarily centered on achieving ultra-precise and stable silicone coatings. The critical technological transition currently underway involves moving away from conventional thermal-cured, solvent-based systems towards highly efficient and environmentally friendly solvent-less and water-based (emulsion) systems. Solvent-less UV curing technology is gaining prominence, especially for filmic substrates (like PET and PP) where heat distortion must be minimized. These UV systems offer instantaneous curing, high line speeds, and zero VOC emissions, meeting both performance and sustainability mandates. Conversely, advanced thermal solvent-less systems are optimized for specialized paper substrates, offering high cross-linking density necessary for aggressive adhesives, ensuring minimal silicone transfer and excellent long-term stability.

Another pivotal area of technical innovation lies in differential release coatings and specialty formulations. Differential liners are designed to have distinct release properties on each side (e.g., tight release for the adhesive side and easy release for the end-user side), crucial for complex multi-layer constructions used in automotive damping materials and advanced medical tapes. Manufacturers leverage proprietary blends of silicone polymers, catalysts (e.g., platinum complexes), and functional additives to fine-tune the peel force to within very narrow tolerances. Furthermore, the development of high-performance barrier coatings, particularly for paper substrates, is vital to prevent silicone penetration and ensure dimensional stability, allowing paper to compete in segments traditionally dominated by films.

Finally, manufacturing efficiency and quality control technologies are key components of the competitive landscape. High-precision coating heads, such as gravure and five-roll systems, ensure consistent coat weight uniformity across wide webs, essential for large format industrial applications. Integration of advanced process monitoring tools, including automated non-contact thickness gauges (beta or X-ray gauges) and high-resolution automated optical inspection (AOI) systems, provides real-time data feedback. This commitment to 'Industry 4.0' principles, enhanced by AI and machine learning for predictive quality management, ensures that the resulting release liner meets the stringent technical specifications of high-value applications, minimizing scrap rates and maximizing operational uptime in high-speed production environments.

The global market for High Quality Silicone Release Liners exhibits distinct regional growth patterns and consumption priorities, reflecting varying levels of industrialization, regulatory environments, and dominant end-use sectors. Asia Pacific (APAC) stands out as the fastest-growing and largest consuming region, driven primarily by massive investments in electronics manufacturing, including flexible displays and printed circuit boards, and the booming electric vehicle (EV) supply chain, particularly in China, Japan, and South Korea. The region’s low-cost manufacturing base also makes it a dominant producer, although competition often focuses on price, pushing quality manufacturers to focus on specialized, high-margin niches like high-temperature resistant liners for composites. Regulatory pressures concerning environmental standards, while present, are generally less rigid than in Western markets, though this is rapidly changing, driving adoption of solvent-less technologies.

North America and Europe represent mature, high-value markets characterized by stringent regulatory oversight and a heavy emphasis on specialized applications, particularly in healthcare and aerospace. Europe, guided by REACH regulations and strong sustainability goals, shows a high penetration rate for solvent-less and UV-cured liners. Demand in both regions is stable and focused on high-specification products such as medical-grade release liners (ISO 13485 certified) and high-performance industrial tapes used in construction and automotive refinishing. The presence of major pharmaceutical and medical device corporations ensures continuous demand for custom-engineered liners with certified purity and low extractables. Pricing tends to be premium, reflecting the required compliance, traceability, and high level of technical support provided by manufacturers.

Latin America and the Middle East & Africa (MEA) currently hold smaller market shares but offer significant future growth potential. Latin America’s growth is tied to local industrial expansion and growth in packaging and labeling sectors, albeit with a focus often on more standard-quality products initially. The MEA region is developing rapidly, fueled by construction projects and investments in regional manufacturing hubs. Demand for high-quality liners here is primarily driven by international companies setting up local production for pharmaceutical and personal care products. Market penetration is slower due to fragmented distribution networks and reliance on imports, but infrastructure investments promise increased adoption of advanced materials over the forecast period, particularly in high-specification oil and gas industrial applications.

The primary drivers are the rapid expansion of high-specification end-use industries, including electric vehicle manufacturing (for battery thermal management), advanced wound care and transdermal medical devices, and the growing demand for lightweight composite materials in aerospace and automotive sectors, all requiring highly reliable release properties.

Solvent-less systems (thermal or UV cured) utilize 100% reactive silicone polymers and eliminate the need for organic solvents, drastically reducing volatile organic compound (VOC) emissions and operational energy consumption. The market is shifting due to stricter environmental regulations, lower manufacturing costs, and suitability for high-speed, temperature-sensitive filmic substrates.

Filmic substrates, particularly Polyethylene Terephthalate (PET) and specialized polyolefins, exhibit the highest growth potential. This is due to their superior dimensional stability, tear strength, transparency, and heat resistance, which are essential for precision applications in electronics, display protection, and high-temperature composite curing processes.

AI is increasingly used for real-time process control and quality assurance. AI-powered vision systems detect microscopic defects in the silicone coating layer, optimize curing parameters, and implement predictive maintenance routines, leading to reduced material waste and significantly improved product consistency and yield rates.

The main challenge is the high barrier to entry encompassing significant capital expenditure required for high-precision, wide-web coating machinery and the necessity of proprietary R&D to develop stable, customized silicone formulations. Additionally, obtaining the necessary regulatory certifications (e.g., ISO 13485 for medical applications) requires substantial time and resources.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.