ID : MRU_ 438020 | Date : Dec, 2025 | Pages : 246 | Region : Global | Publisher : MRU

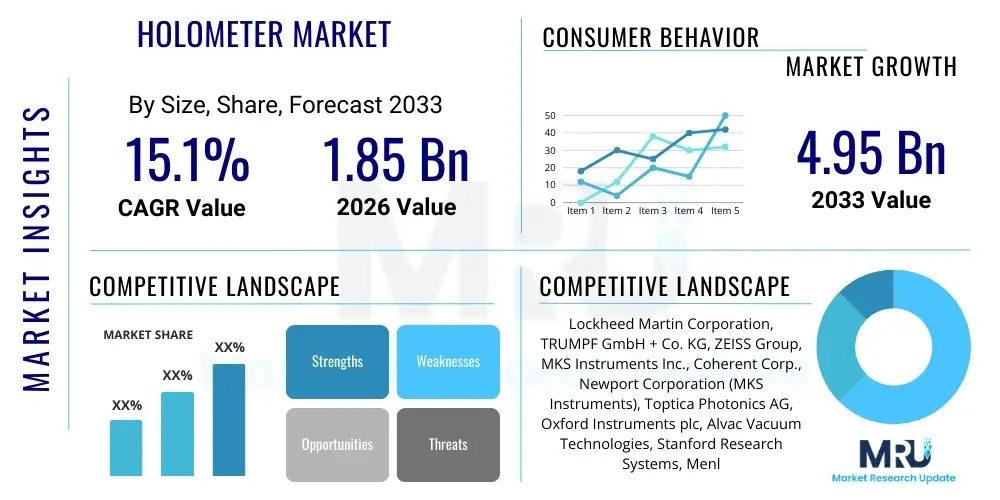

The Holometer Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 15.1% between 2026 and 2033. The market is estimated at USD 1.85 Billion in 2026 and is projected to reach USD 4.95 Billion by the end of the forecast period in 2033.

The Holometer Market encompasses highly specialized scientific instruments designed to measure minute fluctuations in spacetime, often referred to as quantum noise or holographic noise. These devices are ultra-sensitive laser interferometers constructed with unprecedented levels of precision and stability, primarily serving fundamental physics research, astrophysics, and advanced metrology. The technology's core function is to test hypotheses regarding the fundamental limits of spatial resolution imposed by quantum gravity, offering critical insights into the nature of reality at the Planck scale. Due to their complexity and niche application, the market is characterized by high entry barriers, extensive governmental funding for research, and limited adoption primarily within national laboratories and elite university research consortia.

A typical Holometer system involves kilometer-scale vacuum tubes housing highly reflective mirrors and utilizing extreme optical stability to detect movements far smaller than the diameter of a proton. Major applications revolve around experimental verification of holographic principle theories, detecting gravitational waves at high frequencies that conventional detectors might miss, and improving the precision of cosmological measurements. The sophisticated instrumentation required—including ultra-low noise detectors, active vibration isolation systems, and frequency-stabilized lasers—constitutes the primary value proposition of market participants. These systems are crucial in transitioning theoretical physics concepts into measurable empirical data, driving forward the fields of quantum mechanics and general relativity simultaneously.

Driving factors for this market include increasing global investment in fundamental scientific research infrastructure, particularly in regions like North America and the Asia Pacific, where large-scale physics projects are being initiated or upgraded. Furthermore, the continuous quest for higher measurement precision in advanced manufacturing, although a secondary application, sometimes leverages technologies derived from Holometer research, thereby expanding the potential commercial base. The inherent benefits of Holometer technology, such as the ability to probe previously inaccessible scales of physics, secure continuous, long-term government and institutional financial support, ensuring market stability and steady, albeit highly specialized, growth throughout the forecast period.

The Holometer Market is positioned for robust expansion, driven primarily by sustained governmental investment in large-scale physics experiments and the synergistic integration of advanced data processing techniques, including machine learning, to handle the vast output of high-fidelity interferometric data. Business trends indicate a strong focus on strategic collaborations between specialized optics manufacturers, quantum computing firms providing processing power, and leading research institutions to co-develop the next generation of instruments that offer increased baseline lengths and reduced instrumental noise. Key market players are consolidating their intellectual property related to ultra-high vacuum technology and vibration dampening systems, essential components for system longevity and precision.

Regional trends show North America maintaining market leadership due to established scientific infrastructure like Fermilab and MIT, coupled with substantial federal funding mechanisms focused on cosmology and quantum information science. However, the Asia Pacific region, particularly China and India, is rapidly gaining momentum through significant governmental mandates aimed at achieving global leadership in fundamental science, evidenced by massive investments in new research facilities capable of hosting Holometer-scale experiments. Europe remains a critical hub, leveraging pan-European collaborative frameworks (like CERN-associated research, though not directly a Holometer application, sharing infrastructure capabilities) to foster development and adoption, focusing particularly on sensor optimization and data analysis protocols.

Segment trends highlight the dominance of the Ultra-High Precision Measurement segment by Application, reflecting the core usage in confirming spacetime granularity. Technologically, the segment focused on advanced laser interferometry systems (the primary component of the Holometer) holds the largest market share, while the data acquisition and analysis software segment exhibits the fastest growth due to the exponential increase in data volume generated by operational instruments. Manufacturers are increasingly shifting focus toward modular designs that allow for easier upgrades and integration of quantum-enhanced components, such as squeezed light sources, to further suppress quantum shot noise and enhance sensitivity across all major end-user applications.

Common user questions regarding AI's impact on the Holometer Market generally center on whether AI can enhance the sensitivity of the instruments, how it manages the vast datasets generated, and if it can accelerate the interpretation of complex, noisy signals characteristic of fundamental quantum measurements. Users are specifically concerned about AI’s role in differentiating genuine spacetime fluctuations from environmental noise and instrumental drift, which are major obstacles in high-precision interferometry. Furthermore, there is interest in how machine learning algorithms could potentially optimize the operational parameters of the Holometer in real-time to maintain peak performance under varying environmental conditions. The consensus expectation is that AI will transition the Holometer from a purely passive detection tool into an active, self-optimizing research system capable of unprecedented noise suppression.

The application of sophisticated AI and Machine Learning (ML) models, particularly deep neural networks, is revolutionizing data processing within the Holometer domain. These systems are invaluable for the real-time identification and mitigation of systematic errors and non-Gaussian noise sources that frequently contaminate delicate quantum measurements. Traditional signal processing techniques often struggle with the complexity and sheer volume of data produced by modern interferometers. AI excels in pattern recognition across massive datasets, enabling researchers to filter out complex environmental factors—such as seismic activity, thermal variations, and acoustic interference—that mimic or obscure the targeted spacetime signatures, thereby dramatically improving the signal-to-noise ratio (SNR) and the overall fidelity of the experimental results.

Beyond data analysis, AI is crucial in optimizing the complex controls required for operating a Holometer. These instruments rely on maintaining precise optical alignment and environmental stability over vast distances. AI algorithms can predict and preemptively compensate for minute drifts in mirror position or laser frequency based on environmental monitoring data, ensuring continuous optimal operation. This predictive maintenance capability reduces downtime, minimizes experimental corruption due to unexpected thermal transients or mechanical settling, and maximizes the efficiency of expensive research facility usage. The integration of AI/ML is therefore moving from a post-processing tool to an integral, real-time component of the Holometer control architecture, solidifying its role as an essential driver for future sensitivity improvements.

The Holometer Market is heavily influenced by a unique set of Drivers, Restraints, and Opportunities (DRO). Primary drivers include substantial global government funding specifically allocated to fundamental physics research, astrophysics, and quantum science initiatives, alongside the intrinsic demand for experimental verification of theoretical physics models such as quantum gravity and holographic principles. Technological advancement in ultra-stable laser technology and cryogenic optics further enhances the feasibility and sensitivity of new Holometer designs. The primary restraints are the exceptionally high capital expenditure required for construction, the lengthy development cycles demanding decades of commitment, and the scarcity of specialized technical expertise required for the design, operation, and maintenance of these ultra-precise instruments. Furthermore, market growth is confined by the highly specialized, non-commercial nature of the end-user base, limiting scalability.

Opportunities in this market are tied to the potential for technological spillover into adjacent high-precision sectors, such as advanced lithography, high-fidelity defense sensing systems, and next-generation medical imaging devices that demand femtometer-level precision. The development of modular, smaller-scale interferometric prototypes, potentially suitable for educational or smaller institutional research, presents a niche expansion opportunity. Furthermore, the integration of quantum technologies, specifically squeezed light sources, promises to bypass traditional quantum noise limits, offering a significant performance enhancement opportunity that will drive replacement cycles and new investment. The impact forces are overwhelmingly dictated by governmental and institutional spending policies; changes in political priorities regarding space exploration or fundamental science funding can exert immediate and profound effects on market momentum.

The fundamental impact forces shape the competitive landscape, creating a limited oligopoly where competition is based less on cost and more on demonstrated scientific achievement, instrument performance (sensitivity and stability), and access to highly specialized components. The bargaining power of suppliers is high due to the custom nature of ultra-stable lasers, vacuum equipment, and specialized optical components, demanding close long-term relationships with key technology providers. The high barriers to entry prevent new competitors, meaning competitive forces primarily center around incremental innovation among existing, established research teams and consortia. Overall, the market remains driven by scientific imperative rather than commercial demand, ensuring that research funding policies remain the dominant external impact factor.

The Holometer Market segmentation is defined by the instrument's intended use, its core components, and the operational scale. The primary segmentation metrics focus on Application (e.g., Fundamental Physics Research, Metrology) and Component (e.g., Interferometry Systems, Data Acquisition Hardware, Vacuum Infrastructure). Given the nature of Holometers as research instruments, the scale of the system, often categorized by baseline length (e.g., short-baseline, kilometer-scale), also forms a critical dividing factor, directly impacting sensitivity and cost. Understanding these segments is crucial for manufacturers and funding bodies to accurately allocate resources toward the most impactful technological areas and research goals, ensuring the systems meet the demanding requirements of quantum gravitational experiments.

The Component segment holds the most value, as the sophisticated laser sources, cryogenic detectors, and the ultra-stable, large-scale vacuum systems represent the highest cost and technical complexity. Within the Application segment, pure Fundamental Physics Research dominates, accounting for the vast majority of installed systems and associated infrastructure spending. However, the Metrology and Precision Engineering segment, while smaller, is growing due to the need for extreme precision standards derived from techniques pioneered in Holometer development. Regional segmentation reinforces the market's concentration in areas with major governmental or institutional scientific infrastructure investments, specifically North America, Western Europe, and increasingly, key nations in the Asia Pacific.

Future growth will be fueled by the Data Acquisition and Analysis Software segment, driven by the shift towards petabyte-scale data handling and the necessity for sophisticated AI/ML algorithms to extract meaningful signals from high-noise environments. Manufacturers should focus their R&D efforts on modularizing high-cost components and developing highly scalable, standardized data infrastructure solutions that can be adapted to various baseline lengths and environmental conditions. The segmentation analysis confirms the market's high technical specialization and low price elasticity, with performance metrics remaining the paramount consideration over cost in purchasing decisions by major end-users.

The value chain of the Holometer Market is highly specialized and linear, beginning with the upstream supply of foundational high-technology components, progressing through highly specialized system integration, and concluding with deployment in highly controlled, often government-funded, downstream research facilities. Upstream activities are dominated by specialized suppliers providing niche components such as ultra-low noise, frequency-stabilized lasers (e.g., Nd:YAG lasers), high-purity fused silica optics with specialized coatings, and proprietary ultra-high vacuum pumps and materials. The criticality of these components means that supplier bargaining power is exceptionally high, and customization is the norm rather than the exception. Manufacturers must invest heavily in quality control and long-term contracts to ensure component consistency.

Midstream involves the complex process of system design, integration, and construction. This stage requires integrating highly sensitive optical, electronic, and mechanical subsystems into a cohesive, stable instrument, often involving site preparation and the construction of kilometer-long vacuum enclosures. Direct channel distribution dominates this stage; systems are rarely sold off-the-shelf but are custom-engineered and installed directly by the system integrator or a dedicated consortium. Indirect channels, such as conventional distribution networks, are virtually non-existent due to the proprietary nature and sheer scale of the equipment. The complexity of integration demands that the primary system manufacturer maintain deep technical staff engagement throughout the installation and commissioning phases.

Downstream activities center on the operation, maintenance, and data utilization by the end-users, primarily large governmental or academic research facilities. The value capture at this stage is scientific output (publications, discoveries) rather than commercial profit. Maintenance contracts, software upgrades, and periodic component replacement (e.g., detector recalibration, laser replacement) form the secondary revenue stream for manufacturers. The entire value chain is characterized by long lead times, substantial R&D investment, and a heavy reliance on intellectual property surrounding noise suppression and interferometry techniques, making strategic partnerships across the chain essential for successful project execution and scientific viability.

The potential customers for Holometer technology are overwhelmingly concentrated within the public sector and elite non-profit research domains due to the high cost, technical complexity, and non-commercial application profile of the instrument. The primary end-users are national laboratories responsible for advancing fundamental scientific knowledge, such as the U.S. Department of Energy (DOE) research facilities, the National Aeronautics and Space Administration (NASA) for space-based derived technologies, and equivalent national scientific research councils across Europe and Asia. These organizations utilize Holometers to conduct groundbreaking experiments that probe the limits of physical laws, requiring instruments that prioritize ultimate precision over cost efficiency or mass production.

Academic institutions with substantial endowments or access to large government grants, particularly those specializing in astrophysics, particle physics, and quantum optics, represent the second tier of potential customers. Universities such as MIT, Caltech, and institutions associated with major global collaborative physics projects (e.g., LIGO consortia members, though the Holometer is distinct, it shares the customer base focus) procure or co-develop Holometer systems. These academic buyers are driven by the need to conduct proprietary research, train future generations of scientists, and maintain institutional prestige in highly competitive scientific fields. Their purchasing decisions are heavily influenced by scientific advisory boards and peer-reviewed proposals justifying the immense investment.

A smaller, emerging customer segment includes highly specialized high-precision metrology groups within advanced defense sectors or national standards bodies. While they may not require full Holometer functionality for studying spacetime, they are interested in licensing or adopting highly refined subsystems, such as the vibration isolation platforms or the ultra-stable laser systems, for applications requiring nanometer or picometer-scale measurement accuracy in environments like semiconductor manufacturing or aerospace engineering. However, the core market remains centered on fundamental research, where the Holometer acts as a dedicated tool for experimental cosmology and quantum gravity studies.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 1.85 Billion |

| Market Forecast in 2033 | USD 4.95 Billion |

| Growth Rate | 15.1% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Lockheed Martin Corporation, TRUMPF GmbH + Co. KG, ZEISS Group, MKS Instruments Inc., Coherent Corp., Newport Corporation (MKS Instruments), Toptica Photonics AG, Oxford Instruments plc, Alvac Vacuum Technologies, Stanford Research Systems, Menlo Systems GmbH, Thorlabs Inc., Teledyne Technologies Incorporated, Hamamatsu Photonics K.K., Lumentum Holdings Inc., II-VI Incorporated (now Coherent), Advantest Corporation, Ametek Inc., FLIR Systems (Teledyne Technologies). |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological landscape of the Holometer Market is defined by the convergence of advanced laser physics, ultra-high vacuum engineering, and precision seismic isolation systems. Central to every Holometer is the laser interferometer, which requires highly frequency-stabilized, high-power continuous-wave lasers, often operating in the infrared spectrum (like 1064 nm Nd:YAG), coupled with intricate optical resonance cavities (Fabry-Perot cavities) to enhance the light path length and maximize sensitivity to spacetime distortions. Achieving this requisite stability involves utilizing sophisticated electro-optic feedback loops and external pre-stabilization cavities to suppress frequency noise to levels approaching the fundamental quantum limit, thereby ensuring that the instrument is sensitive enough to detect fluctuations hypothesized to be near the Planck length scale.

A second critical technology involves the implementation of extreme environmental control, particularly seismic and acoustic noise suppression. Holometers employ multi-stage active and passive seismic isolation platforms, often incorporating complex pendulum suspension systems and internal cryocooling to mitigate thermal noise. Furthermore, the operational environment must be maintained under ultra-high vacuum (UHV) conditions, typically pressures below $10^{-9}$ torr, across vast kilometer-long arms to prevent air density fluctuations from introducing optical path length noise, which would completely obscure the subtle quantum signals being sought. Innovation in vacuum sealing and low-outgassing materials remains a constant driver for performance improvement within this segment.

Looking forward, the integration of quantum noise suppression techniques is shaping the cutting edge of Holometer technology. The primary method involves the injection of "squeezed light" into the interferometer's dark port. Squeezed light is a quantum-engineered state of light that manipulates the Heisenberg uncertainty principle to reduce the quantum shot noise in one observable (e.g., amplitude) at the expense of increasing the noise in its conjugate variable (e.g., phase). By carefully aligning the noise reduction axis, researchers can achieve sensitivities beyond the standard quantum limit (SQL), representing a major technological leap that drives R&D investment and defines the competitive advantage among leading research instrument manufacturers and consortia seeking to push the boundaries of achievable precision.

Regional dynamics within the Holometer Market are fundamentally tied to national commitments to scientific discovery and the presence of world-class scientific infrastructure. North America, specifically the United States, commands the largest share of the market. This dominance is attributed to extensive, long-term federal funding from agencies like the NSF and DOE, supporting major facilities and consortia involved in high-energy physics and cosmology. The region benefits from a dense ecosystem of specialized technology suppliers and highly skilled academic talent, ensuring continuous technological innovation and rapid adoption of new interferometry techniques. The robust presence of key defense and aerospace contractors, which often utilize Holometer-derived precision systems, further solidifies its market position, focusing heavily on technology localization and proprietary research.

Europe represents the second-largest market, characterized by strong international collaborations and pan-European funding mechanisms (e.g., through the European Research Council). Countries such as Germany, the UK, and Italy host significant scientific facilities and possess deep expertise in advanced optics and vacuum technology. European research efforts often prioritize the standardization of measurement protocols and the development of highly customized, ultra-stable optical components. While infrastructure investment is steady, the market here is characterized by a high level of inter-institutional sharing of resources, leading to optimized, albeit slower, adoption cycles compared to the more decentralized North American approach. The focus remains heavily on theoretical validation and the creation of standardized, high-quality instruments.

The Asia Pacific (APAC) region is projected to exhibit the highest growth rate during the forecast period. This acceleration is largely fueled by ambitious governmental mandates in China, Japan, and India to become global leaders in fundamental science and quantum technology. China, in particular, has demonstrated unparalleled investment in new large-scale physics research facilities, creating immense demand for high-precision scientific instruments, including Holometer technology and its derivatives. This region’s rapid expansion is driven by a strategy of leapfrogging existing technology, often integrating the latest advancements, such as AI-enhanced data processing and squeezed-light technology, from the outset. This governmental prioritization of scientific prestige makes APAC the critical growth engine for the future of the Holometer Market.

The primary function of a Holometer is to measure minute fluctuations in spacetime at the quantum level (holographic noise) to test fundamental physics theories, such as the holographic principle. Unlike standard commercial or laboratory interferometers, Holometers are purpose-built on a massive scale, utilizing ultra-high vacuum and advanced quantum noise suppression techniques, achieving sensitivities orders of magnitude higher than conventional instruments.

North America, particularly the United States, holds market leadership due to substantial, long-term governmental funding for fundamental physics research. The Asia Pacific region, led by China, is the fastest-growing market, driven by significant strategic investment in large-scale scientific infrastructure and the ambition to advance quickly in quantum technology research.

The greatest restraints are the extreme technical demands related to noise mitigation, including seismic isolation and thermal stabilization over large distances, coupled with the reliance on ultra-stable, highly customized laser and vacuum systems. The high capital expenditure and the scarcity of specialized engineering expertise also limit market expansion and accessibility.

AI is crucial for real-time noise cancellation, environmental modeling, and automated data analysis. AI algorithms filter complex environmental interference (e.g., seismic or acoustic noise) from genuine quantum signals, dramatically improving the signal-to-noise ratio and ensuring the continuous optimal operational stability of the sophisticated interferometry systems.

Future sensitivity gains will be primarily driven by the full integration of quantum technologies, specifically the injection of squeezed light sources into the interferometers. This technique helps surpass the standard quantum limit of precision (shot noise), allowing for the detection of even smaller, more subtle spacetime fluctuations required for next-generation fundamental physics experiments.

The primary customers are large governmental scientific research facilities and national laboratories (e.g., DOE, NSF-funded centers) and elite academic consortia specializing in astrophysics and quantum gravity research. Commercial adoption is minimal, limited to the procurement of derived high-precision components by specialized metrology or defense groups.

The ultra-high vacuum (UHV) infrastructure is essential because it eliminates air molecules as a source of optical path length noise, which would easily dominate and mask the subtle spacetime signals. The UHV system represents a significant portion of the construction cost and complexity, making specialized vacuum equipment suppliers critical, high-bargaining-power stakeholders in the value chain.

Since the market is almost entirely research-driven, it exhibits extremely high sensitivity to government budget cycles, especially long-term funding commitments for major scientific facilities. Periods of reduced science funding or shifts in national research priorities can immediately stall new project initiation and slow technological upgrades, as capital expenditure is highly dependent on institutional grants.

While the Holometer itself is not commercial, derivative technologies have significant commercial spillover potential. Specifically, the ultra-stable laser sources, the extreme vibration isolation platforms, and the high-precision metrology techniques developed for Holometers are highly valuable in advanced semiconductor lithography, high-end defense sensing, and calibration standards for next-generation measurement instruments.

Specialization is paramount. Competition is not based on mass production or low cost, but on the ability to deliver bespoke, ultra-high-performance components and system integration expertise. Key players are highly specialized manufacturers of optics, vacuum technology, and sensor systems, forming an oligopoly where technical reputation and scientific partnerships are the key competitive differentiators.

Quantum noise suppression refers to techniques used to counteract the inherent uncertainty in photon counting (shot noise), which limits the maximum achievable sensitivity. The cutting-edge method involves injecting 'squeezed light'—a quantum state of light—into the interferometer to redistribute the noise such that it is minimized along the measurable axis of interest, pushing the measurement past the standard quantum limit.

The Holometer Market is projected to grow at a robust Compound Annual Growth Rate (CAGR) of 15.1% during the forecast period of 2026 to 2033, driven by sustained global interest and investment in experimental verification of quantum gravitational theories.

While both use interferometry, traditional Gravitational Wave Detectors (like LIGO) are optimized for low-frequency astrophysical phenomena (tens to hundreds of Hz) involving massive black holes. Holometers are designed specifically to probe higher frequencies and the fundamental granular structure of spacetime (Planck scale physics), making their application scope more focused on fundamental quantum mechanics and holographic theory testing.

Kilometer-scale systems represent the dominant segment in terms of value and research impact, as the sensitivity of a Holometer scales directly with the length of its interferometer arms. These large-scale systems are necessary to achieve the extreme precision required to detect the hypothesized minute fluctuations in spacetime, defining the cutting edge of current research capability.

The major upstream components dictating cost include ultra-high-power, frequency-stabilized laser systems; proprietary, highly specialized optics and mirror coatings designed for minimal absorption; and the custom, large-scale, ultra-high vacuum infrastructure required to house the interferometer arms, all demanding exceptional manufacturing precision.

Specialized optics suppliers exert high bargaining power because the mirrors and lenses used in Holometers require coatings with extraordinary reflectivity and minimal thermal noise generation, representing highly proprietary and complex manufacturing processes that only a few global firms can reliably execute. These components are non-substitutable and crucial for system performance.

Academic institutions are essential drivers of the R&D cycle. They conceive the theoretical requirements, secure the majority of grant funding, act as the primary end-users, and often collaborate directly with manufacturers to prototype and validate new technologies, such as advanced data processing algorithms and novel noise suppression techniques.

The Holometer Market is projected to reach an estimated value of USD 4.95 Billion by the end of the forecast period in 2033, reflecting substantial anticipated growth fueled by large-scale scientific infrastructure projects globally.

This segment is exhibiting the fastest growth due to the exponential data volumes generated by high-sensitivity instruments (petabytes per experiment). The market demands increasingly sophisticated, AI-driven software to rapidly process, clean, and interpret complex signals, transitioning from hardware-centric challenges to data science complexities.

The market heavily relies on tripartite strategic collaborations involving research consortia (defining scientific needs), governmental agencies (providing funding and oversight), and specialized industrial partners (providing ultra-precision hardware, optics, and integration expertise) to manage the massive technical and financial risk associated with Holometer construction.

Operational stability is critical because the desired spacetime fluctuations are incredibly subtle and easily masked by instrumental drift, thermal transients, or mechanical noise. Achieving continuous stability over long periods (months or years) is necessary to integrate enough data to statistically confirm the presence of these quantum-level signals, validating the experiment's scientific output.

The holographic principle suggests that the physical information contained in a volume of space can be encoded on its boundary, implying a fundamental granularity to spacetime. Holometers are specifically designed to empirically test whether this granularity exists by trying to detect the spatial limits imposed by quantum information, providing experimental support for the holographic universe theory.

The exceptionally long lead times—often several years for component procurement, custom manufacturing, and site preparation—result in market dynamics that are slow to react to short-term economic changes. Purchasing decisions are based on decades-long research plans, prioritizing reliability and long-term performance guarantees over immediate cost savings.

Companies such as ZEISS Group, Coherent Corp., Lumentum Holdings Inc., and MKS Instruments (via Newport) are key players, providing the necessary high-power lasers, ultra-precise optical coatings, and vibration control platforms essential for maintaining the high standards of stability and sensitivity required by Holometer systems.

The adoption of modular design is crucial for reducing high upgrade costs and simplifying maintenance. Modular components, especially for data acquisition, laser injection, and detector systems, allow research facilities to integrate quantum-enhanced upgrades (like new squeezed light sources) without requiring a complete rebuild of the massive vacuum infrastructure, thus extending the operational life of the instrument.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.