ID : MRU_ 432055 | Date : Dec, 2025 | Pages : 258 | Region : Global | Publisher : MRU

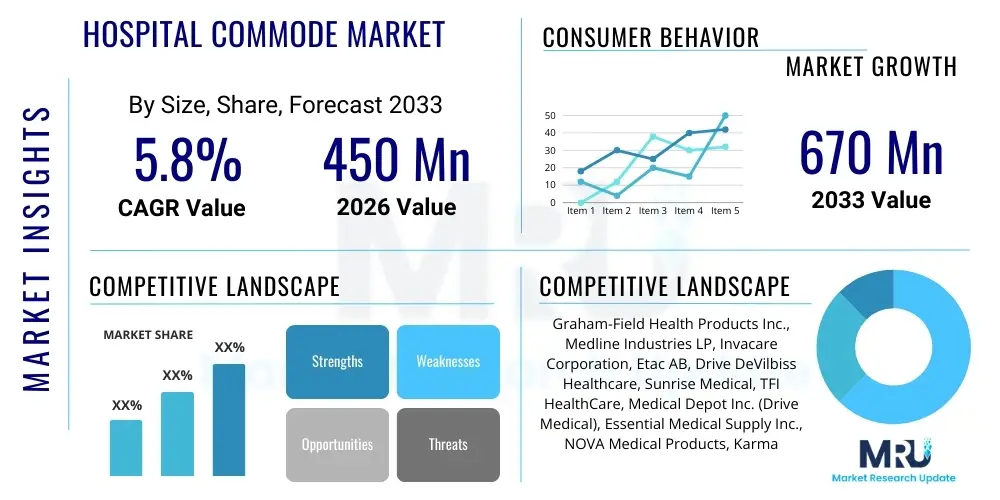

The Hospital Commode Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 5.8% between 2026 and 2033. The market is estimated at USD 450 million in 2026 and is projected to reach USD 670 million by the end of the forecast period in 2033.

The Hospital Commode Market encompasses the manufacturing, distribution, and utilization of specialized sanitary devices designed to assist patients with limited mobility in medical facilities and home care environments. These essential medical aids are critical for maintaining patient hygiene, dignity, and safety, particularly for geriatric patients, post-operative individuals, and those with physical disabilities. The primary product category includes standard bedside commodes, wheeled commode chairs (often convertible to shower chairs), and bariatric models capable of supporting higher weight capacities, all designed with a focus on ease of cleaning, durability, and robust infection control features suitable for clinical settings.

Major applications of hospital commodes span acute care hospitals, specialized rehabilitation centers, long-term care facilities, and the rapidly growing segment of home healthcare. The fundamental benefit provided by these devices is enhanced patient independence and reduced risk of fall injuries associated with transferring to distant restrooms. Furthermore, their deployment streamlines caregiving tasks, ensuring efficient and hygienic management of toileting needs. The demand for these products is intrinsically linked to global demographic trends, particularly the aging population worldwide, which requires increasing levels of mobility assistance and supportive medical equipment, thus establishing a robust foundation for market expansion.

Driving factors fueling this market growth include stringent healthcare regulations emphasizing patient safety and accessibility standards, technological advancements in material science leading to lighter yet stronger commode designs, and increased public awareness regarding the importance of assistive devices. Additionally, the shift toward home-based healthcare models, driven by cost-effectiveness and patient preference, necessitates a corresponding supply of high-quality, clinical-grade commodes for non-institutional environments, thereby broadening the market's reach and accelerating innovation in ergonomic and multi-functional designs.

The Hospital Commode Market is experiencing significant upward momentum, underpinned by favorable demographic shifts and evolving healthcare delivery models. Key business trends indicate a strong focus on product diversification, particularly the development of high-weight capacity bariatric commodes and sophisticated, electric-assisted models that cater to diverse patient needs and enhance caregiver ergonomics. Manufacturers are strategically investing in materials that offer superior microbial resistance and ease of sanitation, aligning with stringent infection control protocols globally. The competitive landscape is characterized by moderate fragmentation, with established medical device manufacturers leveraging strong distribution networks, while niche players focus on innovative, specialized solutions, particularly within the growing home care sector, driving collaborative mergers and acquisitions aimed at expanding product portfolios and regional presence.

Regionally, North America and Europe currently dominate the market due to well-established healthcare infrastructure, high healthcare spending, and proactive implementation of accessibility standards (such as ADA compliance). However, the Asia Pacific (APAC) region is projected to register the highest Compound Annual Growth Rate (CAGR), fueled by rapidly improving healthcare access, increasing government expenditure on geriatric care facilities, and the sheer scale of its aging population base, particularly in countries like China, Japan, and India. The Middle East and Africa (MEA) and Latin America are poised for growth, driven by investments in modern hospital infrastructure and rising health tourism, though market penetration remains constrained by varied regulatory frameworks and purchasing power parity across countries.

In terms of segmentation, the Fixed Commode segment holds a substantial market share due to its stability and cost-effectiveness in institutional settings, yet the Portable and Folding Commode segment is witnessing accelerated growth, largely attributed to the burgeoning demand from the home care and rehabilitation sectors requiring flexible, easily stored solutions. Furthermore, the End-User segmentation highlights Hospitals and Nursing Homes as the traditional primary revenue generators, while the Homecare Settings segment is rapidly catching up, reflecting the trend of patients preferring recovery and long-term management outside of institutional environments, thereby demanding more comfortable, aesthetically pleasing, and durable consumer-grade clinical equipment.

User inquiries frequently center on whether Artificial Intelligence (AI) can meaningfully transform such a fundamental, mechanical medical aid as a hospital commode. Key user concerns revolve around the feasibility of integrating AI for preventative care, specifically monitoring patient vital signs or detecting fall risks during transfers, and how AI-driven analytics could improve commode maintenance and sanitation scheduling in large facilities. There is high user expectation that AI could move the commode from a passive device to an active data-gathering tool, providing real-time insights into patient mobility patterns, toilet usage frequency, and even early detection of urinary tract infections (UTIs) through integrated sensor analysis of waste output, linking these data points directly to Electronic Health Records (EHRs).

While AI will not directly change the core function of the commode, its influence is profound in peripheral applications and data monetization. For instance, AI algorithms applied to sensor data (weight, movement, duration of sitting) generated by 'smart' commodes can create predictive models for patient needs, allowing nurses to proactively check on high-risk individuals before a fall occurs or a complication arises. This integration enhances patient surveillance without increasing manual labor, optimizing staff allocation in understaffed nursing homes and hospitals. The application extends beyond patient care to operational efficiency; AI can analyze usage rates across different units to optimize inventory management, ensuring the right type of commode (e.g., bariatric vs. standard) is available where needed most, minimizing wait times and improving capital expenditure management within procurement departments.

Furthermore, the data collected by AI-enabled commodes provides unparalleled feedback loops for product development. Manufacturers can use machine learning to understand common failure points, areas of discomfort reported indirectly through sensor data, or difficulties encountered during cleaning. This data-driven iterative design process ensures that future generations of hospital commodes are not just mechanically superior but are ergonomically optimized for both the patient and the caregiver, enhancing safety compliance and longevity. The synergy between robust, reliable hardware and intelligent software positioning the commode as a critical node in the broader IoT (Internet of Things) ecosystem within modern smart hospitals.

The market trajectory for hospital commodes is fundamentally shaped by a confluence of demographic, regulatory, and technological factors. The primary Driver (D) is the accelerating global aging population, leading to a massive increase in the number of individuals requiring long-term care and mobility assistance. Coupled with this is the continuous elevation of clinical safety standards and accessibility mandates globally, compelling healthcare providers to invest in high-quality, certified assistive devices. Opportunities (O) arise predominantly from the expansion of home healthcare services, which requires medical-grade yet consumer-friendly equipment, and the substantial untapped potential within emerging economies where healthcare infrastructure modernization is underway. Innovation in specialized materials, such as antimicrobial coatings and lightweight composite structures, presents a substantial technological opportunity for market incumbents to differentiate their offerings and capture premium segments.

Restraints (R) primarily include the high capital expenditure required for hospitals and nursing homes to continually update their equipment, especially in regions with constrained healthcare budgets, leading to prolonged replacement cycles. Furthermore, the absence of standardized procurement guidelines across various regional healthcare systems creates market inefficiencies, and the inherent reluctance of some patients to use specialized equipment due to perceived stigma or lack of comfort can occasionally limit adoption. Price sensitivity, particularly in developing markets, often favors low-cost, potentially less durable alternatives, posing a challenge to manufacturers focused on high-quality, infection-controlled products that meet stringent Western regulatory standards.

The Impact Forces determining market direction are intensely focused on regulatory compliance and the imperative for superior infection prevention. Regulatory bodies, especially in North America and Europe, impose rigorous standards for weight bearing capacity, durability, and material safety, forcing manufacturers to innovate or face market exclusion. The heightened awareness post-global pandemic regarding surface contamination and cross-infection has amplified the force driving demand for commodes designed for easy, thorough disinfection, incorporating features like seamless construction and hydrophobic surfaces. This focus on hygiene acts as a pivotal force, overriding cost considerations in many institutional procurement decisions. The sustained force of demographic pressure ensures consistent long-term demand, stabilizing the market against short-term economic fluctuations.

The Hospital Commode Market is critically segmented across several dimensions, including product type, material, end-user, and distribution channel, reflecting the varied needs within the expansive healthcare ecosystem. This granular classification allows manufacturers to tailor features and marketing strategies specifically to institutional buyers (hospitals requiring extreme durability and high capacity) versus homecare users (prioritizing compactness, portability, and ease of storage). Analyzing these segments reveals shifting consumer preferences, particularly the rise of multi-functional and bariatric models as healthcare facilities strive to accommodate a wider spectrum of patient weights and clinical requirements while maximizing utility from a single investment.

By Product Type, the market separates into fixed, folding/portable, and wheeled models. Fixed commodes, offering maximum stability, remain a cornerstone in dedicated clinical restrooms. However, the flexibility offered by folding and wheeled models, often integrated with shower functionality, is driving growth, especially in rehabilitation centers and home settings where space and versatility are premiums. Material segmentation is crucial for durability and hygiene, with stainless steel and aluminum dominating clinical-grade segments due to their longevity and ability to withstand aggressive chemical sterilization, while composite plastics are preferred in consumer-grade portable segments for their light weight and corrosion resistance.

End-User analysis confirms that institutional settings (hospitals and nursing homes) represent the largest revenue base, requiring bulk orders of robust equipment. Nevertheless, the fastest-growing segment is Homecare Settings, fueled by improved insurance coverage for assistive devices and the general societal trend toward aging-in-place. Distribution channels are diversifying rapidly; while direct sales to large hospital groups remain significant, the adoption of e-commerce platforms and specialized medical equipment retailers is broadening access for individual consumers and smaller clinics, introducing dynamic competitive pressures related to logistics and customer service efficiency.

The value chain for the Hospital Commode Market commences with the upstream analysis, involving the sourcing of primary raw materials, predominantly high-grade metals (stainless steel, aircraft-grade aluminum) and specialized plastics for seats and containers. Key suppliers in this phase are subject to commodity price volatility and strict quality control requirements regarding corrosion resistance and structural integrity. Research and Development (R&D) and design innovation form the core value-added activities in this segment, focusing on ergonomic studies, weight capacity improvements, and developing antimicrobial surface treatments to comply with clinical standards. Efficient inventory management and large-scale, automated manufacturing processes are crucial for maintaining cost competitiveness and quality consistency, especially for high-volume standard models.

The midstream phase focuses on assembly, quality assurance, and certification. Manufacturers must navigate complex regulatory landscapes, obtaining necessary clearances (e.g., FDA, CE Marking) which significantly add value and act as barriers to entry. Logistics and warehousing play a critical role, particularly given the bulky nature of assembled commodes, necessitating specialized storage and transportation solutions. Downstream activities involve market penetration and product distribution. Distribution channels are bifurcated into direct and indirect routes. Direct distribution targets large institutional buyers (major hospital networks) through dedicated sales teams, offering bundled procurement and maintenance contracts, thereby securing high-volume, stable revenue streams.

Indirect distribution relies heavily on medical equipment wholesalers, retail pharmacies, and, increasingly, dedicated e-commerce platforms which serve the fragmented homecare market. E-commerce platforms excel at reaching individual consumers who prioritize privacy and rapid delivery. The value captured in this downstream phase is determined by the efficiency of the channel and the level of post-sale support provided, including warranty services and parts replacement. Successful market players strategically manage these channels to ensure broad access, leveraging direct channels for stability and indirect channels for market expansion and rapid volume increase in consumer segments.

Potential customers for the Hospital Commode Market are broadly categorized into institutional purchasers and direct consumers, each possessing distinct purchasing drivers and product requirements. The largest segment of end-users consists of hospitals (both public and private acute care facilities) and comprehensive medical centers, which purchase large quantities of durable, often stainless steel, wheeled commodes that must adhere to stringent sanitation and bariatric capacity standards. Their procurement decisions are heavily influenced by regulatory compliance, institutional budget cycles, and the clinical need to minimize patient transfer risks, prioritizing products with excellent safety track records and low maintenance profiles.

The second major institutional customer segment includes nursing homes, assisted living facilities, and long-term care centers. These buyers require commodes that offer a balance between durability and comfort, focusing on features that aid patient independence and reduce caregiver strain, such as adjustable height mechanisms and ease of maneuvering in tight spaces. Rehabilitation centers also form a key customer group, specifically seeking versatile 3-in-1 commode chairs that aid in physical therapy and regaining mobility. These institutional buyers value reliable supplier relationships, ensuring consistent access to spare parts and timely product replacement.

The rapidly expanding segment of potential customers comprises individual patients and their families managing care in Homecare Settings. These end-users typically purchase smaller, foldable, or fixed plastic composite commodes through retail or e-commerce channels. Their decision-making criteria prioritize ease of assembly, discreet aesthetics, portability for travel, and affordability, often relying on recommendations from home health aides or occupational therapists. Government entities and insurance providers indirectly influence this segment through reimbursement policies and mandates regarding durable medical equipment (DME), making them crucial stakeholders in driving consumer purchasing power.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 450 Million |

| Market Forecast in 2033 | USD 670 Million |

| Growth Rate | 5.8% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Graham-Field Health Products Inc., Medline Industries LP, Invacare Corporation, Etac AB, Drive DeVilbiss Healthcare, Sunrise Medical, TFI HealthCare, Medical Depot Inc. (Drive Medical), Essential Medical Supply Inc., NOVA Medical Products, Karman Healthcare, MHI Group, McKesson Corporation, Apex Medical Corp., GF Health Products, Cardinal Health, Prism Medical, Veleco Inc. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological landscape of the Hospital Commode Market, while traditionally reliant on simple mechanical engineering, is undergoing modernization driven primarily by advancements in material science and increasing integration of digital monitoring capabilities. Key technology focuses include the adoption of high-strength, lightweight aluminum alloys and specialized polymer composites that enhance the weight capacity of commodes while simultaneously reducing the overall weight, making them easier for caregivers to maneuver and transport. A crucial development is the pervasive application of antimicrobial coatings, often silver-ion or copper-based treatments, applied to high-touch surfaces. This technology significantly contributes to infection control by inhibiting bacterial growth, aligning commode design with rigorous hospital hygiene standards and providing a substantial advantage over legacy steel designs in sterile environments.

Further innovation involves sophisticated ergonomic design principles, leveraging computer-aided design (CAD) and stress-testing simulations to optimize seating geometry and adjustability. The emergence of bariatric-specific technologies, including reinforced frame structures and wider, pressure-relieving seating surfaces, addresses the growing medical necessity of accommodating obese patient populations safely and comfortably. Beyond materials, the integration of 'smart' technology represents a nascent but high-potential area. This includes embedded sensors (pressure, tilt, proximity) linked to low-power wireless communication protocols (like Bluetooth Low Energy or Wi-Fi). These sensors monitor usage patterns and alert staff to instances of prolonged immobility or high-risk patient transfers, positioning the commode as a functional data-collection point within the hospital's Internet of Things (IoT) network.

Specific features driving technological adoption include advanced height adjustment mechanisms, often pneumatic or electric-powered, which facilitate seamless patient transfers and accommodate varying bed heights, significantly improving caregiver safety and reducing manual lifting injuries. Additionally, modular designs are gaining traction, allowing commodes to be quickly converted into shower chairs or toilet safety frames by swapping components, maximizing the utility of the equipment. This modular approach extends the lifespan of the device and improves cost-efficiency for healthcare facilities. The emphasis remains on developing robust, maintenance-free components that can endure intensive, frequent cleaning cycles required in high-traffic institutional settings while leveraging digital technology for enhanced patient safety oversight.

The global Hospital Commode Market exhibits significant variation in maturity, growth drivers, and regulatory compliance across different geographic regions, with established markets in North America and Europe contrasting sharply with the rapidly evolving landscapes in Asia Pacific and other developing territories. Understanding these regional dynamics is crucial for market participants seeking targeted expansion and optimal resource allocation.

North America, led by the United States and Canada, currently holds the largest share of the global hospital commode market. This dominance is attributable to several factors: a highly mature healthcare infrastructure, robust healthcare spending, high awareness and adoption of technologically advanced medical equipment, and stringent regulatory environments such as the Americans with Disabilities Act (ADA) and FDA standards, which necessitate the consistent upgrade of assistive devices. The demand here is characterized by a high preference for bariatric models and sophisticated, multi-functional commodes that integrate advanced safety features and high durability. The significant presence of large, vertically integrated hospital networks and the increasing prevalence of chronic conditions requiring long-term care further solidify this region's market leadership, with product differentiation focusing heavily on infection control certifications and ergonomic superiority. The strong reimbursement structure for Durable Medical Equipment (DME) also substantially bolsters demand in the homecare segment.

The U.S. market specifically drives innovation, especially in smart commodes featuring sensor technology for monitoring patient movement and vital signs, aligning with the broader trend toward digital healthcare integration. Hospitals prioritize stainless steel or high-grade aluminum models capable of frequent, high-temperature sterilization. Competition in this region is intense, requiring manufacturers to maintain vast distribution networks and prioritize customer service and quick parts delivery. Regulatory adherence, particularly regarding weight testing and non-toxic materials, is non-negotiable and acts as a significant entry barrier for lower-quality international competitors. The market is saturated but highly replacement-driven, requiring continuous investment in product lifecycle management and safety updates to maintain market share.

Europe represents the second-largest market, characterized by extensive, publicly funded healthcare systems and a profound focus on geriatric care due to its rapidly aging population profile, particularly in Western European nations like Germany, France, and the UK. The demand is heavily influenced by quality standards mandated by the European Medical Device Regulation (MDR), ensuring that products are highly reliable, safe, and easily traceable. European facilities show a strong preference for commodes that balance functionality with compact, aesthetic design, especially for use in long-term care facilities where patient comfort and dignity are paramount.

Scandinavia, in particular, leads in ergonomic design and sustainability, favoring materials that are both durable and environmentally responsible. The regional market growth is steady, supported by consistent government investment in accessible healthcare infrastructure and the normalization of assistive devices as essential care tools. The trend toward rehabilitation and convalescence at home significantly drives the demand for portable and folding commodes that meet high clinical specifications but are user-friendly for non-professional caregivers. Regulatory requirements often dictate standardized sizing and compatibility with other mobility aids, promoting uniformity across the continent's diverse health systems. Manufacturers must navigate different procurement policies, often involving centralized tenders for large health trusts, emphasizing price competitiveness alongside quality certifications.

The Asia Pacific region is forecast to be the fastest-growing market globally, driven by massive population demographics, rapid expansion of private healthcare investment, and substantial economic growth lifting healthcare spending capabilities, particularly in China, India, and Southeast Asia. The sheer size of the geriatric population in countries like Japan and South Korea, combined with rapidly developing urban infrastructure, creates an unprecedented demand for modern hospital equipment, including commodes.

While price sensitivity remains a factor in rural and lower-tier urban markets, the introduction of international healthcare standards and the establishment of sophisticated private hospitals are boosting demand for premium, high-quality, imported or locally manufactured commodes meeting international safety benchmarks. Market opportunities are immense for companies willing to tailor designs to local requirements, such as cultural preferences for certain materials or sizes, and establish robust localized distribution chains. The primary challenge in APAC lies in navigating diverse regulatory requirements and fragmented distribution systems, but the long-term growth prospects, fueled by increasing health insurance penetration and modernization of public health systems, are overwhelmingly positive.

The Latin American market is experiencing moderate but accelerating growth, largely dependent on governmental efforts to upgrade public hospital infrastructure and address socioeconomic disparities in healthcare access. Key growth markets include Brazil, Mexico, and Argentina. The demand in this region is primarily driven by the need for cost-effective, yet reliable, commode solutions. Imported products face competitive pressure from local manufacturers offering lower-cost alternatives, though frequently at a trade-off in advanced features or material quality.

Market penetration is correlated with economic stability and investment in primary healthcare services. Institutional buyers often prioritize durability and ease of maintenance due to limited resources for equipment replacement and repair. Manufacturers entering LATAM must focus on building strong local partnerships and ensuring efficient supply chain management to counter logistical challenges and import tariffs. The burgeoning private healthcare sector, often catering to wealthier populations, presents a niche demand for high-end, technologically sophisticated commodes mirroring those used in North America.

The MEA region presents a diverse market scenario. The Gulf Cooperation Council (GCC) countries (UAE, Saudi Arabia, Qatar) drive demand for premium hospital commodes due to significant government investment in world-class medical cities and health tourism initiatives. These facilities demand the latest technology, often mirroring the specifications of European or North American equipment, with a high emphasis on advanced sterilization and luxury components, reflecting the high-end patient experience sought in these regions.

Conversely, sub-Saharan Africa represents a largely untapped market where growth is heavily reliant on international aid, philanthropic efforts, and gradual improvements in basic public health services. Demand is focused on essential, highly durable, and easily repairable commodes. Manufacturers need to consider the challenging environmental conditions, prioritizing robust materials resistant to rust and wear. The overall market growth in MEA is bifurcated, strong in high-income oil economies and foundational in developing nations, requiring distinct market entry and product strategies for maximum success.

The primary factor driving market growth is the accelerating global aging population, coupled with increasing chronic diseases and mobility impairment conditions. This demographic shift significantly boosts demand for assistive devices, particularly in long-term care and homecare settings.

Infection control is critical, driving the adoption of commodes made from non-porous materials like stainless steel and high-grade plastic composites that withstand frequent, aggressive chemical sterilization. Designs emphasize seamless construction and antimicrobial coatings to minimize pathogen retention and cross-contamination risk in clinical environments.

The Folding/Portable Commode Chairs segment is projected to show the highest growth rate, primarily driven by the expansion of the homecare market. These models offer versatility, ease of storage, and are favored by patients transitioning out of institutional care who require reliable, clinical-grade mobility assistance at home.

While not yet standard, smart commodes integrating sensors for monitoring patient movement and detecting fall risks are rapidly gaining traction, particularly in high-acuity and geriatric care units in developed markets like North America and Western Europe. This technology enhances patient safety protocols and provides valuable data for preventative care and optimizing staff response times.

The main challenges in APAC include navigating diverse and evolving regulatory frameworks, addressing significant price sensitivity in emerging sub-markets, and establishing efficient localized distribution networks to penetrate fragmented geographic areas effectively while competing against low-cost local alternatives.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.