ID : MRU_ 435310 | Date : Dec, 2025 | Pages : 257 | Region : Global | Publisher : MRU

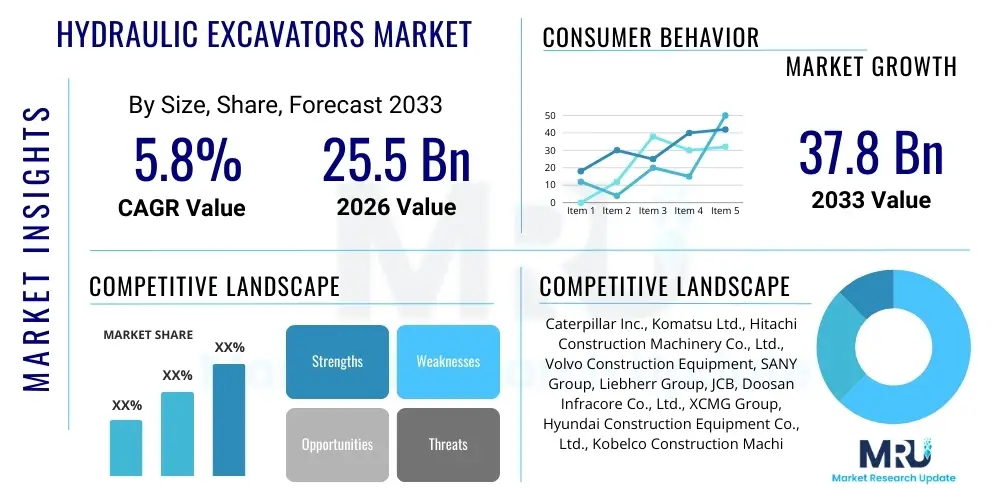

The Hydraulic Excavators Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 5.8% between 2026 and 2033. The market is estimated at $25.5 Billion in 2026 and is projected to reach $37.8 Billion by the end of the forecast period in 2033.

The Hydraulic Excavators Market encompasses the manufacturing, sales, and servicing of heavy construction equipment primarily used for digging, trenching, demolition, material handling, and grading operations. Hydraulic excavators, characterized by their boom, stick, bucket, and cab mounted on a rotating platform (house) atop an undercarriage (crawler or wheeled), utilize hydraulic fluid power to drive linear actuators and hydraulic motors. These machines are essential across core global industries, serving as the backbone for infrastructural development projects ranging from residential construction to large-scale public works, ensuring efficiency and productivity in harsh operating environments.

The product segmentation within this market is robust, spanning mini (under 6 metric tons), medium (6-30 metric tons), and large (over 30 metric tons) classes, each optimized for specific applications. Mini excavators are highly valued for urban and utility projects due to their maneuverability, while medium and large excavators dominate mining, quarrying, and extensive earthmoving operations. Key benefits driving adoption include superior power-to-weight ratio, exceptional digging force, precise control, and versatility facilitated by a wide array of attachments such as hammers, grapples, and specialized shears.

Major driving factors fueling market expansion include rapid urbanization, significant global investment in public infrastructure (roads, bridges, railways), and the increasing demand for advanced extraction techniques in the mining sector, particularly in emerging economies of the Asia Pacific region. Furthermore, technological advancements focused on fuel efficiency, operator comfort, and integration of telematics systems are bolstering replacement cycles and attracting new investments from rental fleets and construction contractors seeking optimized operational costs and enhanced safety standards.

The Hydraulic Excavators Market is experiencing robust growth, driven primarily by favorable macroeconomic conditions characterized by elevated infrastructure spending in developed and developing nations, particularly focusing on sustainable urban development and energy transition projects. Key business trends include the consolidation of manufacturing capabilities among major global original equipment manufacturers (OEMs) and a persistent focus on electrification and automation to meet stringent environmental regulations and improve on-site efficiency. The competitive landscape is intensely focused on leveraging digital solutions, such as predictive maintenance and advanced fleet management, to offer superior total cost of ownership (TCO) to end-users.

Regionally, Asia Pacific maintains its dominance, spurred by massive infrastructure initiatives in China and India, coupled with growing residential construction activity in Southeast Asian countries. North America and Europe demonstrate mature market characteristics, where growth is primarily derived from the replacement of aging fleets with advanced, more efficient models compliant with Tier 4 Final/Stage V emission standards, and the adoption of hybrid and electric models. The Middle East and Africa present high-potential opportunities, fueled by substantial investments in oil and gas infrastructure and diversification projects aimed at building smart cities and expanding logistics networks.

Segment-wise, the medium excavator category remains the largest volume driver due to its versatility across general construction and rental applications, while the mini excavator segment exhibits the highest growth trajectory, benefiting from increased demand for compact equipment in utility and landscaping work. Technological trends favor the integration of sophisticated sensing systems and GPS guidance, transforming excavators into intelligent earthmoving machines. Furthermore, the shift towards electric and hybrid excavators, though nascent, is gaining traction, signaling a long-term transition towards sustainable construction practices across all operational sizes.

Users frequently inquire about how Artificial Intelligence (AI) and Machine Learning (ML) integration will fundamentally alter the operational dynamics, safety standards, and maintenance costs associated with hydraulic excavators. Key themes revolve around the feasibility and timeline for achieving fully autonomous excavation cycles, the reliability of AI-driven diagnostics for preventative maintenance, and the necessary skill evolution for operators and maintenance technicians in an increasingly automated environment. Concerns often include the initial capital expenditure required for AI-equipped machines and the cybersecurity risks associated with transmitting vast amounts of operational data wirelessly. Expectations are generally high regarding improved project predictability, drastic reduction in downtime, and significant enhancement in fuel and energy efficiency achieved through AI-optimized work patterns.

The immediate and measurable impact of AI is seen in the realm of predictive maintenance and operational efficiency. By processing real-time telemetry data (oil pressure, engine load, hydraulic flow rates) through complex machine learning models, AI systems can accurately predict component failure months in advance, minimizing unscheduled downtime. This capability drastically improves fleet utilization rates for large construction and mining companies. Furthermore, AI assists in optimizing duty cycles, automatically adjusting engine output and hydraulic power distribution based on soil type and digging resistance, leading to demonstrable reductions in fuel consumption per cubic meter of material moved.

In terms of advanced operational functionality, AI is critical for enabling semi-autonomous functions, such as automated trenching to specified depths and slopes, and obstacle avoidance. This not only increases precision, reducing the need for costly rework, but also significantly enhances safety on the job site by mitigating human error, especially in hazardous conditions like deep mining or demolition. The ongoing development of AI-powered vision systems further enhances situational awareness for operators and lays the groundwork for seamless integration into broader smart construction ecosystems, connecting excavation activities directly to Building Information Modeling (BIM) platforms.

The Hydraulic Excavators Market is influenced by a confluence of economic drivers, regulatory restraints, and technological opportunities, all mediated by global impact forces such as urbanization trends and commodity price volatility. Key market drivers include the accelerating demand for residential and commercial infrastructure, particularly in developing economies, coupled with increased spending on maintenance and repair of aging public works in developed regions. However, the market faces significant restraints, most notably the high initial investment cost associated with advanced machinery and the increasing scarcity and rising cost of skilled labor required to operate and maintain these complex hydraulic systems effectively. Opportunities reside primarily in the rapid commercialization of electric and hybrid models and the expansion of the equipment rental market, offering cost-effective access to modern machinery.

Impact forces significantly shape the strategic landscape. Environmental regulations, such as stringent emission standards (e.g., EU Stage V and US Tier 4 Final), compel OEMs to invest heavily in engine technology and alternative power sources, accelerating the transition away from traditional diesel engines. Furthermore, geopolitical stability and trade policies directly affect the global supply chain for critical components, influencing production costs and lead times. The cyclical nature of the construction and mining industries means that macroeconomic indicators, such as interest rates and government fiscal policies related to infrastructure spending, serve as critical external impact forces dictating short-term market demand and capital investment decisions by end-users.

Technological advancement acts as a pervasive force, offering both opportunities and competitive pressures. The integration of IoT, telematics, and AI is becoming a standard expectation, driving demand for intelligent excavators that offer lower operational expenditures (OPEX) and superior data insights. Companies that successfully leverage these technologies to deliver measurable improvements in productivity and fuel efficiency gain a significant competitive advantage. Conversely, firms lagging in digitalization face obsolescence. Therefore, the strategic balance between capitalizing on technological opportunities and mitigating the constraints imposed by high capital costs and regulatory compliance defines market performance.

The Hydraulic Excavators Market is comprehensively segmented based on machine type, technology, and end-user application, allowing for a precise understanding of demand patterns across various operational environments. Segmentation by Type (Mini, Medium, Large) reflects the operational requirements regarding reach, depth, and material volume capacity, directly correlating with project scale. Segmentation by Technology, incorporating conventional, hybrid, and electric models, tracks the industry's commitment to sustainability and energy efficiency improvements. The end-user application segment, spanning Construction, Mining, Forestry, and Utility sectors, demonstrates the versatility and essential nature of these machines across the global industrial landscape.

The value chain for the Hydraulic Excavators Market begins with the upstream sourcing of raw materials, including high-grade steel alloys, sophisticated electronic components (sensors, control units), and complex hydraulic systems (pumps, valves, cylinders). This upstream segment is highly concentrated, relying on specialized global suppliers for powertrain and hydraulic components, making manufacturers sensitive to commodity price fluctuations and supply chain disruptions. The quality and reliability of these upstream inputs are paramount as they directly determine the performance and lifespan of the final equipment. Strategic partnerships with reliable component suppliers are crucial for maintaining manufacturing throughput and managing costs effectively.

The midstream stage involves the core manufacturing and assembly processes carried out by OEMs. This phase is capital-intensive, requiring advanced robotics, precision machining, and rigorous quality control. OEMs invest heavily in R&D to integrate advanced features like telematics, AI-driven controls, and efficient powertrains. Following manufacturing, the downstream segment, comprising distribution, sales, and aftermarket services, dictates market reach and customer satisfaction. The distribution channel is typically dominated by independent, authorized dealers who manage inventory, sales financing, and provide essential maintenance and parts supply. The strength and geographic coverage of this dealer network are significant competitive differentiators.

Distribution channels in the market are characterized by a mix of direct sales to major mining companies or government bodies and indirect sales through dealer networks, which handle the majority of transactions for smaller contractors and rental companies. The aftermarket segment—including spare parts, maintenance contracts, and equipment servicing—represents a high-margin, stable revenue stream critical to the total profit structure of OEMs. The shift toward digitalization is also impacting the value chain, enabling remote diagnostics and direct-to-customer parts ordering, streamlining the indirect distribution channel and enhancing customer support efficiency.

Potential customers, or end-users, of hydraulic excavators are diverse, encompassing major sectors responsible for the development and maintenance of global infrastructure and resource extraction. The largest customer base resides within the general construction industry, including large engineering procurement and construction (EPC) firms, mid-sized regional contractors, and specialized demolition and earthmoving companies who utilize excavators for foundational work, trenching for utilities, and site preparation across residential and commercial projects. These buyers prioritize reliability, financing options, and the total cost of ownership (TCO) over the operational lifespan of the machine, often demanding detailed telematics data to justify their investment.

Another major customer segment is the mining and quarrying industry, utilizing heavy-duty, large hydraulic excavators for mass excavation and loading operations in challenging environments. These customers require machines optimized for endurance, high payload capacity, and specialized attachments suitable for hard rock extraction. Governmental agencies and municipal bodies also act as significant direct purchasers for public works, road construction, and utility repair projects, where compliance with environmental standards and long-term durability are key purchasing criteria. Furthermore, the forestry sector represents a niche but important customer group, requiring specialized attachments and robust undercarriages for navigating difficult terrain.

In recent years, the equipment rental sector has emerged as a rapidly growing potential customer segment. Rental companies purchase large volumes of excavators, primarily in the mini and medium classes, to offer flexible solutions to small and medium enterprises (SMEs) that cannot afford the high upfront capital expenditure of outright ownership. These customers are driven by ease of maintenance, high residual value, and the availability of a diverse fleet. The trend towards renting rather than owning is particularly pronounced in developed markets, influencing OEMs to design machines that are durable, standardized, and easily serviceable across multiple end-user environments.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | $25.5 Billion |

| Market Forecast in 2033 | $37.8 Billion |

| Growth Rate | 5.8% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Caterpillar Inc., Komatsu Ltd., Hitachi Construction Machinery Co., Ltd., Volvo Construction Equipment, SANY Group, Liebherr Group, JCB, Doosan Infracore Co., Ltd., XCMG Group, Hyundai Construction Equipment Co., Ltd., Kobelco Construction Machinery Co., Ltd., Sumitomo Construction Machinery Co., Ltd., John Deere, Terex Corporation, LiuGong Machinery Co., Ltd., Zoomlion Heavy Industry Science and Technology Co., Ltd., Wacker Neuson SE, Case Construction Equipment, Shantui Construction Machinery Co., Ltd., Takeuchi Mfg. Co., Ltd. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technology landscape within the Hydraulic Excavators Market is undergoing a rapid evolution, moving away from purely mechanical systems toward sophisticated digital and sustainable power solutions. A primary focus is on advanced engine technologies designed to meet increasingly stringent global emission standards, requiring the integration of complex after-treatment systems like Diesel Particulate Filters (DPF) and Selective Catalytic Reduction (SCR). This necessitates deeper electronic control units (ECUs) and high-precision injection systems. Concurrently, hydraulic system innovation is centered on improved efficiency, employing load-sensing hydraulics and electronically controlled proportional valves to minimize energy losses and optimize the utilization of engine power for attachment operation.

Telematics and the Internet of Things (IoT) constitute the dominant digital technology trend. Modern excavators are equipped with extensive sensor arrays that continuously monitor hundreds of operational parameters, transmitting this data via cellular networks to cloud-based fleet management platforms. This technology enables features such as real-time tracking, fuel consumption monitoring, remote fault diagnostics, and automated reporting. These data insights are invaluable for construction managers seeking to optimize fleet deployment, enforce operator efficiency, and schedule preventative maintenance precisely, shifting the industry standard from reactive repair to proactive asset management.

The rise of electrification is the most disruptive technological shift. Hybrid excavators utilize energy regeneration systems, storing energy generated during boom-down or swing braking in capacitors or batteries, which is then reused to assist the engine during high-load operations, significantly reducing fuel use. Fully electric and battery-powered excavators, although currently limited primarily to the mini and medium classes, are gaining traction, especially in urban or indoor construction sites where zero emissions and low noise levels are mandatory. Continued advancements in battery energy density and charging infrastructure are critical determinants of the pace of adoption for these zero-emission alternatives, representing the future direction of heavy machinery design.

The global Hydraulic Excavators Market exhibits distinct regional dynamics driven by varying levels of infrastructural investment, regulatory environments, and adoption rates of new technology.

The primary drivers include escalating global investment in infrastructure renewal and expansion, particularly in emerging economies of the Asia Pacific, coupled with rapid urbanization that necessitates continuous development of residential and commercial properties. Additionally, technological advancements related to fuel efficiency, automation, and telematics systems are stimulating replacement demand in mature markets.

Stringent environmental regulations, such as EU Stage V and US Tier 4 Final emission standards, are fundamentally reshaping the market. These rules necessitate advanced engine after-treatment systems and, more significantly, accelerate the industry's shift towards developing and commercializing hybrid and fully electric hydraulic excavators that offer reduced noise pollution and zero operational emissions, especially crucial for urban construction sites.

The Mini Excavator segment (under 6 metric tons) is projected to exhibit the fastest growth rate. This accelerated adoption is driven by increasing demand for compact, highly maneuverable equipment essential for smaller utility projects, landscaping, and construction in confined urban spaces where larger machines cannot operate efficiently. Their ease of transport and lower operational costs also favor rental companies.

AI plays a crucial role in enhancing productivity, safety, and efficiency. Key applications include AI-driven predictive maintenance, which reduces downtime by anticipating component failures; autonomous grade control for precision digging; and sophisticated operational optimization algorithms that dynamically adjust machine power settings to minimize fuel consumption based on real-time task requirements.

Leading OEMs focus intensely on product differentiation through technological superiority, particularly in telematics integration, automation readiness, and sustainable powertrain development (hybrid/electric). Competitive strategies also include expanding global dealer networks, offering comprehensive aftermarket service packages, and employing aggressive pricing and financing models, particularly targeting large fleet buyers and government contracts in high-growth regions like APAC.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.