ID : MRU_ 434251 | Date : Dec, 2025 | Pages : 255 | Region : Global | Publisher : MRU

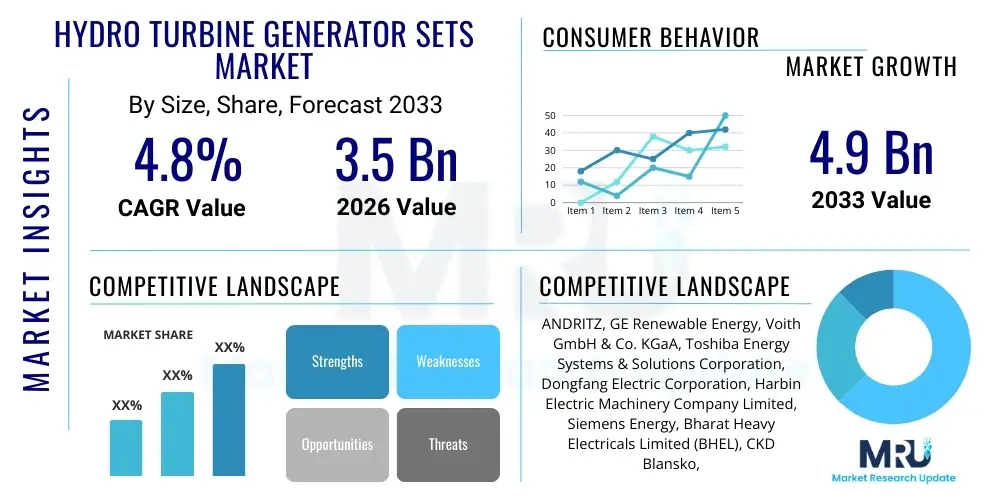

The Hydro Turbine Generator Sets Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 4.8% between 2026 and 2033. The market is estimated at USD 3.5 Billion in 2026 and is projected to reach USD 4.9 Billion by the end of the forecast period in 2033.

The Hydro Turbine Generator Sets Market encompasses the manufacturing, supply, installation, and maintenance of integrated systems crucial for converting the potential and kinetic energy of flowing water into electrical power. These sets typically include the hydraulic turbine, which extracts energy from the water flow, and the synchronous generator, which converts the mechanical rotation into electricity suitable for grid integration. The core technology relies on principles established over a century ago, but modern advancements focus heavily on efficiency, durability, and adaptability to fluctuating grid demands, especially given the rising penetration of intermittent renewable sources like solar and wind power.

Hydro turbine generator sets are indispensable components of global renewable energy infrastructure, offering reliable, dispatchable power generation and essential grid balancing services. Major applications span conventional run-of-river projects, large reservoir dams, and increasingly critical pumped storage facilities. Product variations, such as Francis, Kaplan, and Pelton turbines, are selected based on the specific hydraulic head and flow characteristics of the site, ensuring optimal performance across diverse geographical and environmental conditions. The longevity and high capacity factor of hydropower assets position these generator sets as foundational elements of sustainable energy portfolios worldwide.

Driving factors for market growth include aggressive global decarbonization targets, which necessitate increased reliance on dispatchable renewable energy storage (pumped hydro), alongside substantial investments in upgrading aging hydropower fleets in North America and Europe. Furthermore, developing economies in Asia Pacific and Latin America, rich in untapped hydro potential, continue to initiate new construction projects to meet escalating electricity demand, further solidifying the market's trajectory towards steady expansion and technological refinement, especially concerning digitalization and operational efficiency.

The Hydro Turbine Generator Sets Market demonstrates robust resilience driven primarily by the global necessity for energy security and grid stability in the transition towards renewables. Business trends emphasize strategic acquisitions and joint ventures focused on integrating digitalization capabilities, particularly leveraging IIoT sensors and advanced analytics for predictive maintenance and enhanced operational longevity. Manufacturers are shifting R&D investments towards flexible and variable speed hydro units, essential for modern pumped storage schemes that demand rapid switching between generation and pumping modes. The competitive landscape is characterized by a strong presence of established engineering conglomerates that are increasingly differentiating themselves through service contracts and long-term asset management partnerships rather than solely new equipment sales.

Regionally, Asia Pacific maintains its dominance in terms of new installation capacity, propelled by massive governmental investments in large-scale projects in China, India, and Southeast Asia, aimed at expanding electrification and supporting industrial growth. Conversely, North America and Europe are key markets for modernization, refurbishment, and capacity uprating of existing facilities, addressing fleets that often exceed 50 years of operation. Latin America, particularly Brazil and countries within the Andean region, presents significant opportunity due to underdeveloped water resources and increasing energy demand, although political and regulatory stability remains a key determinant for investment pace. These regional disparities dictate varied demand profiles: high-capacity Francis turbines dominate APAC construction, while Kaplan turbines and advanced refurbishment solutions are prioritized in mature Western markets.

Segment trends highlight the critical role of the Pumped Storage Hydropower (PSH) segment, which is experiencing exponential growth forecasts globally due to its necessity in balancing intermittent solar and wind generation. Capacity-wise, the Small Hydro segment (up to 20 MW) is gaining traction, supported by simplified permitting processes and distributed generation policies, offering opportunities for specialized turbine manufacturers focusing on modular and standardized designs. Technologically, the transition to synchronous condensers and variable speed drives for large generators marks a pivotal shift, aimed at providing crucial ancillary services like voltage regulation and system inertia to increasingly volatile electrical grids.

User queries regarding the integration of Artificial Intelligence (AI) into the Hydro Turbine Generator Sets Market frequently center on how these technologies can maximize operational efficiency, extend equipment lifespan, and optimize complex water management decisions in the face of climate variability. Common themes include the efficacy of AI in predictive maintenance to reduce costly unplanned downtime, the potential for machine learning algorithms to optimize power output based on real-time grid conditions and water availability forecasts, and the development of 'digital twins' for precise simulation and testing of refurbishment strategies. Users are keenly interested in the return on investment (ROI) associated with implementing AI-driven monitoring systems and the standardization of protocols for data ingestion from geographically dispersed hydro assets. The consensus expectation is that AI will transform hydropower from a stable, but largely static, asset into a highly flexible and responsive component of the smart grid infrastructure, significantly improving overall profitability and reliability.

The Hydro Turbine Generator Sets Market dynamics are shaped by a complex interplay of global energy policy, environmental constraints, economic realities, and technological maturity. Drivers predominantly revolve around the global imperative to achieve carbon neutrality, positioning hydropower—especially pumped storage—as the backbone for reliable grid balancing against variable renewables. Significant opportunities arise from the need to modernize extensive, aging infrastructure in mature economies, alongside the burgeoning demand for standardized small hydro solutions in off-grid or distributed generation scenarios in developing nations. Conversely, the market faces headwinds from substantial capital expenditure requirements, lengthy permitting processes tied to environmental impact assessments, and increasing water scarcity risks resulting from erratic climate patterns, which impact operational capacity factors in specific regions.

The primary drivers propelling the market include government support via renewable energy mandates and feed-in tariffs, substantial public and private financing directed toward pumped storage projects globally, and the technical advantages hydropower offers in terms of long asset life and high operational efficiency compared to other generation sources. The continuous innovation in turbine design, such as runner optimization for wider operating ranges and the adoption of oil-free and environmentally friendly designs, also serves as a crucial factor attracting sustained investment. Furthermore, the necessity for robust, black start capabilities in large grids ensures continued strategic importance for hydro generators, irrespective of fluctuations in other renewable sectors.

Restraints, however, pose significant challenges. The environmental and social impact of large dam construction often leads to public opposition, complex resettlement issues, and stringent regulatory hurdles, dramatically increasing project lead times and costs. Moreover, while operational costs are low, the initial high cost of fabrication and civil works for hydro generator sets, coupled with increasing interest rates, can deter private sector investment. The impact forces compelling market transformation include rising electricity prices, which enhance the profitability of flexible hydro assets, and rapidly falling costs of complementary technologies like battery storage, which are forcing hydro operators to innovate and improve flexibility to maintain competitive edge in the ancillary services market.

The Hydro Turbine Generator Sets Market is critically segmented based on the operational characteristics required by diverse hydrological conditions and capacity needs globally. Segmentation by Type (Francis, Kaplan, Pelton, etc.) directly reflects site-specific constraints related to water head and flow rate, dictating manufacturing complexity and resulting efficiency. The Capacity segmentation (Small, Medium, Large Hydro) mirrors global policy trends, with small hydro often supported by regulatory incentives for decentralized power, while large hydro remains the domain of national utilities requiring massive, baseload power and water management capabilities. Understanding these segments is vital for manufacturers to tailor their R&D and supply chain strategies, addressing the bespoke engineering required for large projects versus the standardization needed for high-volume small hydro components.

Further granularity is achieved through segmentation by Application, distinguishing between conventional power generation and the increasingly vital Pumped Storage Hydropower (PSH). PSH plants require specialized reversible pump-turbines and generators, which are engineered for rapid mode switching and high flexibility, differentiating this segment significantly from conventional continuous generation assets. The evolving energy mix places PSH at the forefront of growth, demanding generator sets capable of operating synchronously and asynchronously to absorb surplus solar/wind energy and release it quickly when demand peaks. This functional differentiation drives specific technological developments in generator cooling, insulation, and control systems, ensuring high fatigue resistance throughout frequent cycling operations.

Geographical segmentation also plays a major role, with APAC dominating new capacity installation, requiring the supply of brand-new, often custom-engineered large generator sets, whereas North America and Europe primarily drive demand for refurbishment, spare parts, and capacity uprating services, requiring deep expertise in retrofitting and integrating modern control systems with legacy mechanical infrastructure. These segmented demands ensure a diverse market landscape where specialization in both new builds and long-term service contracts defines competitive success, necessitating flexible production capacities and highly skilled field service teams across all major operational segments.

The value chain for the Hydro Turbine Generator Sets Market is intricate, starting from the highly specialized upstream production of raw materials and components, extending through complex manufacturing and precise field installation, and culminating in long-term operation, maintenance, and eventual decommissioning. Upstream activities involve suppliers of specialty steel alloys, high-voltage insulation materials, and advanced cooling system components, which must adhere to strict quality and durability standards mandated by the high-stress operating environment of hydro assets. The manufacturing stage is capital-intensive, requiring advanced machining centers for runner fabrication, specialized winding facilities for generators, and extensive quality control protocols, typically undertaken by a few global conglomerates with deep engineering heritage and patented design expertise.

The downstream component of the value chain focuses heavily on project execution and service provision. Distribution channels for large, bespoke generator sets are primarily direct, involving competitive tendering processes where manufacturers bid directly to national utilities, Independent Power Producers (IPPs), or large civil engineering contractors. This stage requires significant integration between mechanical, electrical, and civil works, necessitating robust project management and logistics capabilities to transport immense components to often remote dam sites. Small hydro projects, in contrast, may utilize indirect distribution through regional engineering procurement and construction (EPC) firms or specialized system integrators who aggregate components from various suppliers.

Post-installation services represent a vital, high-margin segment of the downstream value chain. Given the multi-decade lifespan of hydro assets, long-term operation and maintenance (O&M) contracts, refurbishment, and capacity uprating services are essential revenue streams. The rising adoption of smart monitoring and predictive analytics (often provided indirectly via software partnerships or integrated service platforms) is transforming the service landscape, enabling manufacturers to move from reactive repairs to proactive asset management, thereby stabilizing cash flows and enhancing customer relationships throughout the entire lifecycle of the generator set.

The primary customers and end-users of Hydro Turbine Generator Sets are organizations responsible for electricity generation, grid management, and large-scale water resource administration. The most significant buyers are national and state-owned power utilities (such as China Three Gorges Corporation, NTPC in India, or specialized governmental hydro authorities), which purchase generator sets for large, centralized hydro and pumped storage projects integral to national energy policy. These entities prioritize reliability, efficiency, extremely long operational lifespan, and the manufacturer's proven financial stability and track record in executing complex mega-projects that require customized, high-capacity equipment.

Independent Power Producers (IPPs) constitute the second major customer segment. These private sector entities invest in hydro projects, often medium-sized or small hydro installations, driven by favorable regulatory frameworks, long-term power purchase agreements (PPAs), and the desire for stable asset returns. IPPs often seek standardized, modular designs that offer quicker deployment and lower overall risk. Their procurement decisions heavily favor suppliers offering competitive financing terms, robust maintenance packages, and streamlined installation processes, often utilizing EPC contractors as intermediaries for the equipment purchase.

A third, rapidly growing customer group involves operators of existing hydropower facilities in mature markets (like the US, Canada, and Western Europe) requiring refurbishment and modernization services. These customers, including both utilities and smaller regional power authorities, are buyers not necessarily of new greenfield generator sets, but of sophisticated components, capacity uprating packages, and advanced control systems designed to extend the life and improve the performance of assets often built between the 1950s and 1980s. Their purchasing criteria center on compatibility, minimizing outage time, and maximizing the return on investment through incremental efficiency gains enabled by modern technologies.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 3.5 Billion |

| Market Forecast in 2033 | USD 4.9 Billion |

| Growth Rate | 4.8% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | ANDRITZ, GE Renewable Energy, Voith GmbH & Co. KGaA, Toshiba Energy Systems & Solutions Corporation, Dongfang Electric Corporation, Harbin Electric Machinery Company Limited, Siemens Energy, Bharat Heavy Electricals Limited (BHEL), CKD Blansko, Litostroj Power, Gilkes, Canyon Hydro, Flovel, Power Machines, Hitachi, Ltd., Mavel, Zwickau, WWS Wasserkraft GmbH, IMPSA. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological landscape of the Hydro Turbine Generator Sets Market is undergoing a significant evolution, moving beyond purely mechanical improvements to integrate advanced digital and material sciences. A critical focus area is the development of Variable Speed Pumped Storage (VSPS) technology, which utilizes power electronics and frequency converters to allow the pump-turbine unit to operate efficiently across a wide range of speeds. This flexibility is essential for modern grid management, enabling faster and more precise adjustment of power consumption or generation, thereby optimizing ancillary service revenue and increasing the overall stability of grids incorporating high percentages of non-synchronous renewables.

Digitalization, often encapsulated under the Industrial Internet of Things (IIoT) and advanced sensor deployment, is transforming asset management. Modern generator sets are equipped with arrays of sophisticated sensors that monitor parameters like vibration, bearing temperature, shaft alignment, partial discharge within windings, and hydraulic pressure in real-time. This continuous data stream feeds into cloud-based platforms utilizing AI and machine learning algorithms to enable predictive maintenance strategies. This technological shift allows operators to anticipate potential failures months in advance, scheduling maintenance precisely when needed, dramatically reducing the frequency of costly forced outages and maximizing the unit’s availability and lifespan.

Furthermore, innovations in material science are enhancing efficiency and durability. Advanced stainless steel alloys with improved resistance to cavitation and erosion are being used for turbine runners, particularly in high-head Francis and Pelton applications, minimizing wear and tear in abrasive water conditions. Environmentally friendly technologies are also mandated, leading to the increased adoption of water-lubricated or air-pressurized bearing systems (eliminating oil contamination risks) and the design of fish-friendly Kaplan turbines, addressing ecological concerns and streamlining the often-contentious permitting process for new hydro development, thus influencing market viability and technological adoption rates.

The primary driver is the accelerating global need for dispatchable, large-scale energy storage, specifically pumped storage hydropower (PSH), which complements intermittent solar and wind generation by providing essential grid stability and ancillary services necessary for the transition to a high-renewable energy mix.

Turbine type is determined by the site’s hydraulic conditions—specifically head and flow. Francis turbines are suited for medium head/flow, Kaplan for low head/high flow, and Pelton for high head/low flow. The generator must be matched to the turbine’s speed and torque characteristics to ensure optimal efficiency and power conversion under those specific operating parameters.

Digitalization integrates Industrial IoT (IIoT) sensors and AI for predictive maintenance. This technology allows operators to continuously monitor key mechanical and electrical parameters (like vibration and temperature), enabling the early detection of faults and optimizing maintenance scheduling to minimize unplanned downtime and maximize asset longevity and availability.

The Asia Pacific (APAC) region currently leads the market in terms of new installation capacity, primarily driven by large-scale infrastructure and pumped storage projects initiated by governments in China, India, and Southeast Asian countries to meet rapidly increasing industrial and residential electricity demand.

Key restraints include the extremely high upfront capital expenditure required for civil works and equipment, lengthy and complex regulatory and permitting processes associated with environmental impact assessments, and the vulnerability of hydro capacity to unpredictable water availability due to global climate change and prolonged drought periods.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.