ID : MRU_ 432143 | Date : Dec, 2025 | Pages : 258 | Region : Global | Publisher : MRU

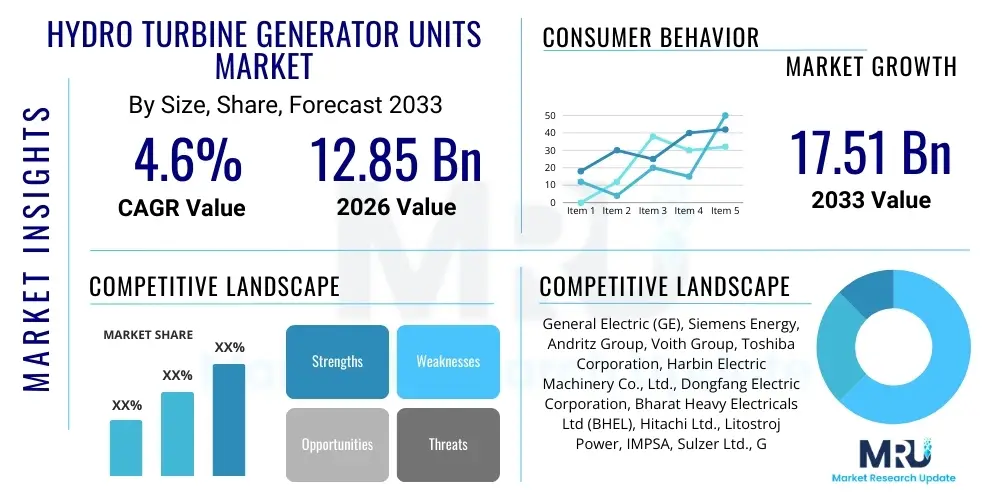

The Hydro Turbine Generator Units Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 4.6% between 2026 and 2033. The market is estimated at USD 12.85 Billion in 2026 and is projected to reach USD 17.51 Billion by the end of the forecast period in 2033.

The Hydro Turbine Generator Units Market encompasses the design, manufacturing, installation, and maintenance of specialized equipment crucial for converting the kinetic energy of flowing or falling water into electrical power. These units, which typically comprise the hydro turbine (such as Francis, Kaplan, or Pelton) mechanically coupled to an electric generator, are the foundational components of hydroelectric power plants. The market’s dynamism is directly linked to global renewable energy targets, infrastructure development in emerging economies, and the necessity for stable, dispatchable power sources to complement intermittent renewables like solar and wind. Product specifications vary significantly based on the hydraulic head and flow rate of the water source, dictating the type of turbine utilized.

Major applications for hydro turbine generator units span large-scale utility operations, pumped storage facilities vital for grid stability, and small or micro-hydro installations serving remote communities or industrial self-consumption. The enduring appeal of hydropower lies in its high efficiency, long operational lifespan, and the ability to rapidly adjust power output in response to grid demands, making it an indispensable asset in modern energy matrices. As governments worldwide commit to decarbonization, the refurbishment and modernization of existing aging hydro assets, alongside the development of new greenfield sites, continue to drive substantial market opportunities.

Key benefits derived from these units include low operating costs once installed, zero greenhouse gas emissions during operation, and the inherent stability they provide to electrical grids. Driving factors include increasing electricity demand, favorable regulatory frameworks promoting renewable energy infrastructure, technological advancements enhancing turbine efficiency (especially in areas like computational fluid dynamics for optimization), and growing concerns over energy security that prioritize domestic, reliable power sources.

The Hydro Turbine Generator Units Market demonstrates robust growth, primarily fueled by global commitments to renewable energy expansion and significant investments in modernizing aging hydroelectric infrastructure across North America and Europe. Business trends highlight a strong shift towards highly efficient Francis and Pumped Storage turbines, necessitated by the need for flexible grid operation and improved water resource management. Major market players are focusing heavily on integrating digitalization and smart grid capabilities into their offerings, emphasizing predictive maintenance, remote monitoring, and optimization software to maximize asset utilization and minimize downtime.

Regionally, Asia Pacific (APAC) stands as the dominant growth engine, driven by massive dam construction projects and rural electrification initiatives in China, India, and Southeast Asian nations. North America and Europe, while slower in new construction, exhibit high market value due to extensive refurbishment and upgrade cycles, focusing on replacing or modernizing turbine runners, governors, and excitation systems to meet higher efficiency standards and extended operational lifetimes. Latin America is also emerging as a high-potential region, leveraging abundant water resources for large-scale hydro development.

Segment trends underscore the criticality of the Large Capacity segment (over 100 MW) for national grids, while the Small Hydro segment (under 10 MW) sees steady growth driven by decentralized power generation and mini-grid applications, particularly in mountainous or remote terrains. The Utility segment remains the principal consumer, although private sector involvement in Independent Power Producer (IPP) models for hydro projects is increasing, thereby influencing procurement patterns and demanding more flexible financing structures from equipment manufacturers.

User inquiries regarding the influence of Artificial Intelligence (AI) on the Hydro Turbine Generator Units Market frequently center on predictive maintenance effectiveness, real-time efficiency optimization, and the potential for autonomous operation in remote facilities. Users are particularly concerned with how AI tools can prolong asset life, reduce unexpected failures, and manage the complex variability introduced by climate change affecting water flow. A consensus theme involves the integration of AI-driven analytics with SCADA systems to move beyond simple monitoring toward prescriptive asset management, seeking tangible improvements in overall plant operational expenditure and reliability.

The key themes emerging from user expectations revolve around AI’s ability to handle vast streams of sensor data—covering vibration, temperature, pressure, and acoustic emissions—to detect nascent faults long before conventional methods. There is significant interest in using machine learning algorithms to model optimal operating points for turbines under fluctuating head and flow conditions, maximizing energy conversion efficiency dynamically. Furthermore, users anticipate that AI will facilitate better coordination between cascaded hydro plants and manage water releases more effectively for environmental compliance and water usage schedules, optimizing the complex balancing act between power generation and resource stewardship.

Overall, users expect AI to transition hydropower plant management from reactive and preventive approaches to highly predictive and prescriptive strategies. This includes using deep learning models for anomaly detection in generator stator windings or bearing wear, automating the scheduling of turbine inspections based on predicted failure probability, and optimizing bidding strategies in electricity markets by accurately forecasting available generation capacity given weather and hydrology models. This integration is viewed not just as a cost-saving measure but as an essential technological upgrade to ensure hydropower remains a competitive, reliable, and intelligent participant in the evolving smart grid ecosystem.

The Hydro Turbine Generator Units Market is significantly influenced by a confluence of accelerating drivers (D), persistent restraints (R), and substantial opportunities (O), which collectively define the Impact Forces shaping its trajectory. The primary driver is the global imperative to transition toward clean, sustainable energy sources, underpinned by favorable governmental policies, Renewable Portfolio Standards (RPS), and substantial subsidies for infrastructure development. Simultaneously, the restraints, notably the high initial capital expenditure required for large-scale projects and lengthy permitting processes often entangled with environmental impact assessments, pose considerable challenges to accelerated deployment. However, the market is poised to capitalize on opportunities presented by the burgeoning need for energy storage, particularly through Pumped Storage Hydropower (PSH), and the extensive backlog of aging hydro plants globally requiring mandatory upgrades and refurbishments to meet modern grid stability and efficiency metrics.

Key impact forces include technological advancements that continuously improve turbine design efficiency and durability, allowing plants to operate effectively across a wider range of flows and heads. Furthermore, the rising awareness and acceptance of Small and Mini Hydro projects as viable solutions for decentralized power generation in developing regions democratizes access to hydro technology, expanding the potential customer base beyond traditional large utilities. Geopolitical stability and energy independence objectives also strongly influence investment, positioning reliable hydropower as a strategic national asset, especially where indigenous fossil fuels are scarce. This strategic importance often accelerates regulatory approval for critical refurbishment projects, ensuring market continuity for maintenance and upgrade cycles.

The ongoing structural shift in the global electricity grid towards high penetration of variable renewable energy sources (solar and wind) fundamentally reinforces the value proposition of hydro turbine generator units. Hydropower, particularly PSH, acts as the natural complement, providing inertia, voltage support, and rapid response capacity essential for balancing supply and demand fluctuations. This essential grid stabilization service transcends simple electricity generation, transforming hydro assets into critical infrastructure for grid resilience, thereby guaranteeing sustained governmental and private sector investment into both new capacity and life extension programs for existing assets.

The Hydro Turbine Generator Units Market is comprehensively segmented based on Type, Capacity, and End-User, allowing for granular analysis of demand patterns and technological preferences across different geographical and operational contexts. Segmentation by Type reflects the specific hydraulic requirements of the installation site, ranging from high-head Pelton turbines to low-head, high-flow Kaplan turbines. Capacity segmentation highlights the difference between utility-scale power generation and decentralized micro-grids. End-User analysis focuses on the primary purchasers and operators, detailing procurement trends between national utilities, independent power producers, and industrial entities.

The value chain for hydro turbine generator units is complex, starting with extensive upstream activities including raw material procurement (specialized steel, copper, composites) and highly specialized design and engineering phases. Upstream analysis involves detailed geological and hydrological studies to determine site suitability, followed by sophisticated Computational Fluid Dynamics (CFD) modeling used by manufacturers to design custom turbine runners and stators for maximum hydraulic efficiency. Key challenges in the upstream segment include volatile raw material prices and the need for precision manufacturing capabilities, often requiring massive machine tools for forging and machining large turbine components.

The midstream phase focuses on manufacturing, assembly, and rigorous testing. This is where original equipment manufacturers (OEMs) dominate, leveraging their intellectual property regarding blade profiles, sealing technologies, and generator excitation systems. Distribution channels are typically direct for large, custom-engineered projects, where the OEM handles logistics, site delivery, and installation supervision. Indirect channels, involving specialized engineering, procurement, and construction (EPC) firms, often manage smaller or standardized components, but the core turbine and generator units almost always require direct engagement between the utility/developer and the primary manufacturer.

Downstream activities center around installation, commissioning, operations, and long-term maintenance, refurbishment, and servicing. The life cycle support segment is increasingly critical, representing a stable, high-margin revenue stream for OEMs. Direct service provision ensures high quality and access to proprietary parts, extending the operational life of the assets. Furthermore, the downstream includes the integration of the hydro plant into the regional or national grid, necessitating close cooperation with grid operators and the deployment of advanced control systems (governors, exciters) capable of meeting stringent grid code requirements for frequency and voltage control.

The primary customers for hydro turbine generator units are governmental and private entities involved in large-scale electricity generation and grid management. The most significant end-users are national and regional Electric Utilities, often state-owned enterprises (SOEs) or regulated monopolies, responsible for managing vast hydroelectric portfolios that form the backbone of national power supply. These utilities drive demand for high-capacity Francis and Kaplan units for base load generation and are the primary market for large-scale refurbishment contracts, as they seek to extend the life of decades-old infrastructure.

A rapidly growing customer segment comprises Independent Power Producers (IPPs) and private infrastructure developers. These entities secure long-term Power Purchase Agreements (PPAs) and undertake financing, construction, and operation of hydro projects, ranging from large PSH facilities to medium-sized run-of-river schemes. IPPs prioritize efficiency, reliability, and lifecycle cost (LCOE), driving demand for modern, digitally enabled turbine units that promise lower operating expenditure and higher capacity factors throughout their operating life.

Secondary but important customer segments include industrial consumers, particularly those in energy-intensive sectors such as mining and pulp & paper, which often develop captive hydro power plants (especially small or mini-hydro) to ensure self-sufficiency and stabilize energy costs. Additionally, international development banks and non-governmental organizations often fund micro-hydro projects in remote or mountainous areas of developing countries, serving local communities and small industrial clusters, thereby creating demand for standardized, easily deployable small-capacity units.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 12.85 Billion |

| Market Forecast in 2033 | USD 17.51 Billion |

| Growth Rate | 4.6% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | General Electric (GE), Siemens Energy, Andritz Group, Voith Group, Toshiba Corporation, Harbin Electric Machinery Co., Ltd., Dongfang Electric Corporation, Bharat Heavy Electricals Ltd (BHEL), Hitachi Ltd., Litostroj Power, IMPSA, Sulzer Ltd., Gilkes, CWE, SNC-Lavalin, Mitsubishi Heavy Industries (MHI), WWS Wasserkraft, ATB Riva Calzoni, FLOVEL, Ganz Engineering and Energetics Machinery LLC |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technology landscape of the Hydro Turbine Generator Units Market is defined by continuous evolution aimed at boosting efficiency, enhancing operational flexibility, and extending asset lifespan, often achieved through advanced materials science and digital integration. A primary technological focus remains on hydraulic design optimization, utilizing sophisticated Computational Fluid Dynamics (CFD) modeling and 3D printing for rapid prototyping of complex runner shapes. This methodology enables manufacturers to customize turbines to specific site parameters, minimizing cavitation—a major cause of erosion and performance degradation—and maximizing the output across a fluctuating range of operating conditions. Furthermore, the development of new, corrosion-resistant and highly durable coatings and materials is vital for minimizing maintenance costs and ensuring long-term reliability in abrasive water environments.

Digitalization forms the second major pillar of the current technology landscape. This involves the widespread integration of advanced sensors and Industrial Internet of Things (IIoT) infrastructure into turbine-generator sets. These systems collect massive amounts of data in real-time concerning temperature, vibration, shaft alignment, and electrical parameters. This data feeds into sophisticated control systems, including digital governors and voltage regulators (excitation systems), which utilize AI and machine learning algorithms to perform real-time monitoring, diagnostics, and predictive maintenance. This shift toward smart hydro plants allows for remote asset management, optimization of water usage, and instantaneous response to grid frequency fluctuations, crucial for supporting high levels of variable renewable energy.

Pumped Storage Hydropower (PSH) technology represents a specific area of intense technological development, particularly the reversible pump-turbine units. Modern PSH turbines require exceptional flexibility, operating seamlessly in both pumping and generating modes, and often needing variable speed capabilities achieved through advanced power electronics (e.g., Variable Speed Drives or Frequency Converters). This technology allows the PSH plant to consume or generate power precisely when needed, significantly enhancing its value as a grid balancing asset. Beyond the main units, auxiliary systems, such as environmentally friendly sealing and lubrication systems, are also undergoing significant innovation to meet increasingly strict ecological regulations regarding water quality and aquatic life protection.

The primary factor driving market growth is the global accelerated energy transition toward renewable sources combined with the critical need for grid stability and energy storage. Hydropower units, especially Pumped Storage Hydro (PSH) turbines, are essential for balancing the intermittency introduced by high penetration of solar and wind energy, ensuring reliable power supply and frequency regulation across major grids worldwide. Additionally, extensive government commitments to decarbonization and infrastructure modernization incentivize investment in both new hydro capacity and the refurbishment of aging fleets in developed nations.

Technological innovation significantly enhances unit efficiency through advanced hydraulic design utilizing Computational Fluid Dynamics (CFD) modeling and optimized materials science. Modern turbines are custom-designed to minimize hydraulic losses and cavitation, leading to higher power output across variable flow conditions. Digitalization, including integrated sensors and AI-driven control systems, allows for real-time adjustments of turbine parameters (governors and wicket gates) to maintain peak efficiency dynamically, vastly improving the overall capacity factor and lifespan of the equipment.

The Francis turbine type historically dominates the market due to its versatility and high efficiency across medium head and flow applications, making it suitable for most large-scale installations globally. However, the Pumped Storage Hydropower (PSH) turbine segment, typically involving reversible Francis-type pump-turbines, is experiencing the fastest growth. PSH is becoming crucial because it provides the largest capacity, longest duration, and most rapid-response energy storage currently available, essential for balancing modern electricity grids overloaded with intermittent renewable generation and stabilizing frequency deviations.

The main challenges restraining large-scale market expansion include substantial initial capital investment and extremely long, often politically sensitive, project development timelines. Regulatory hurdles, complex environmental impact assessments (EIAs), and social resistance related to land inundation and ecosystem disruption associated with large dam construction often delay or halt new greenfield projects. This high risk profile and lengthy gestation period often deter private investors, making large hydro projects reliant on extensive public sector backing or multilateral development bank financing.

Segmentation by capacity dictates the manufacturing and procurement strategies significantly. The Large Hydro segment (above 100 MW) requires highly customized, project-specific engineering and direct utility engagement, focusing on high precision and long lifecycle assurance. Conversely, the Small Hydro segment (up to 10 MW) often relies on standardized, modular designs, allowing manufacturers to focus on economies of scale, simplified installation, and offering comprehensive packages suitable for smaller, often decentralized, private or municipal buyers in remote areas.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.