ID : MRU_ 394876 | Date : May, 2025 | Pages : 340 | Region : Global | Publisher : MRU

The Hydrochlorofluorocarbons (HCFCs) market is poised for significant change over the forecast period (2025-2032), projected to experience a CAGR of 5%. While HCFCs were introduced as a transitional replacement for ozone-depleting chlorofluorocarbons (CFCs), their own ozone depletion potential, albeit lower than CFCs, necessitates a phased-out approach globally under the Montreal Protocol. This market analysis explores the dynamics of this complex market, considering its diminishing role due to environmental regulations and the ongoing shift towards more sustainable refrigerants and alternatives. Key growth drivers in the remaining market window include existing stock replenishment in developing nations with less developed refrigerant infrastructure and ongoing demand for HCFCs in specific niche applications where replacements havent fully penetrated the market. Technological advancements in identifying and applying alternative refrigerants have been crucial in driving the phase-out, with significant investment in research and development focused on environmentally benign refrigerants like hydrofluoroolefins (HFOs) and natural refrigerants (e.g., ammonia, CO2). The HCFCs markets role in addressing global challenges is primarily centered on its contribution to the gradual phase-out of ozone-depleting substances, thereby protecting the ozone layer and mitigating climate change. However, this role is transient, as the markets decline indicates a success story in international environmental policy and the transition to more environmentally friendly technologies. The residual market is now largely focused on managing the safe and responsible disposal of existing HCFC stocks and completing the transition to environmentally superior replacements. The transition itself presents challenges in terms of infrastructure upgrades, training and knowledge transfer to developing nations, and economic implications for industry stakeholders reliant on HCFC production and use.

The Hydrochlorofluorocarbons (HCFCs) market is poised for significant change over the forecast period (2025-2032), projected to experience a CAGR of 5%

The HCFCs market encompasses the production, distribution, and application of various HCFC compounds. Technologies associated with the market include refrigeration and air conditioning systems, foam blowing agents, and solvent applications. The key applications are diverse, ranging from refrigeration in commercial and industrial sectors to foam creation in insulation materials and various industrial processes using HCFCs as solvents or chemical intermediates. The market serves a broad range of industries, including refrigeration and air conditioning manufacturing, construction, automotive, electronics, and chemical processing. The markets significance in the broader context of global trends is inextricably linked to international efforts to protect the environment. It exemplifies a successful, albeit complex, transition towards environmentally responsible chemical products, guided by global cooperation under the Montreal Protocol. The ongoing phase-out of HCFCs illustrates the impact of international environmental regulations on market dynamics, stimulating technological innovation and requiring substantial investment in infrastructure and training to facilitate a smooth transition to safer and more sustainable alternatives. The markets shrinking size also reflects a broader global shift towards sustainable consumption and production patterns, aligning with the United Nations Sustainable Development Goals (SDGs).

The HCFCs market refers to the global commercial activity surrounding the production, distribution, and consumption of hydrochlorofluorocarbons. These are chemical compounds containing hydrogen, chlorine, fluorine, and carbon. HCFCs were developed as transitional replacements for ozone-depleting substances (ODS) like CFCs. The market components include the manufacturing of various HCFC types (such as HCFC-22, HCFC-141b, HCFC-142b, etc.), their distribution through supply chains involving wholesalers, distributors, and retailers, and their ultimate use in various applications. Key terms associated with the market include Ozone Depletion Potential (ODP), Global Warming Potential (GWP), Montreal Protocol, refrigerant, foaming agent, solvent, phase-out schedule, alternative refrigerants (HFOs, natural refrigerants), recycling, and reclamation. Understanding these terms is crucial for navigating the regulatory and technical aspects of the market. ODP and GWP are crucial metrics evaluating the environmental impact of different refrigerants, guiding the selection of safer alternatives. The Montreal Protocol serves as the international agreement driving the phase-out of HCFCs. Recycling and reclamation processes play a vital role in minimizing environmental impact and recovering valuable resources.

The HCFCs market is segmented by type, application, and end-user, each segment contributing differently to the overall market dynamics. These segmentations provide a granular understanding of the markets structure and help in analyzing the specific trends and drivers influencing each segments growth trajectory. The understanding of these segmentations is vital for strategic decision-making by market players and policymakers alike.

HCFC-22: Widely used as a refrigerant in air conditioning and refrigeration systems, particularly in developing countries where the transition to HFOs has been slower. Its relatively lower ODP compared to CFCs contributed to its initial adoption, but it is now facing rapid phase-out globally. This segments growth is predominantly driven by existing stock replenishment and limited replacement options in certain regions.

HCFC-141b: Primarily used as a blowing agent in the production of polyurethane foams for insulation applications. Its phase-out is influencing the shift towards environmentally friendly alternatives like HFO-blown foams and other insulation materials. Demand is expected to decline further due to stricter regulations and availability of substitutes.

HCFC-142b: This HCFC finds applications as a blowing agent and solvent. Similar to HCFC-141b, its usage is decreasing due to the availability of environmentally safer alternatives and regulatory pressures. This segment faces a declining trajectory, primarily driven by strict regulatory frameworks.

HCFC-123: Employed as a refrigerant in specific industrial applications. While its ODP is relatively low, the market for this compound is still influenced by the global phase-out schedule and adoption of sustainable alternatives.

HCFC-124: Used in niche applications, this segment exhibits a relatively small market size compared to other HCFCs. Its future depends heavily on the availability of suitable replacement chemicals and regulatory policies. This segment has limited market growth prospects.

Refrigerant: HCFCs are widely used in refrigeration and air conditioning systems. However, this application is rapidly shrinking as environmentally friendly alternatives gain market share. The remaining demand is largely driven by the need to replenish existing systems in regions with slower transitions to sustainable refrigerants.

Foaming Agent: This application involves using HCFCs in the production of polyurethane foams for insulation. The shift towards sustainable alternatives in the construction industry is driving the decline of this segment. The transition to HFOs and other eco-friendly blowing agents is rapidly accelerating, leading to significant reduction in HCFC usage in this sector.

Chemical Materials: Some HCFCs serve as chemical intermediates in the manufacturing of other chemical products. This application is also declining, as manufacturers transition to less environmentally harmful options. This segments future hinges on the adaptation of the chemical industry and the accessibility of eco-friendly alternatives.

Governments play a crucial role in setting regulations and enforcing the phase-out schedule for HCFCs. Their policies significantly influence market trends and incentivize the adoption of sustainable alternatives. They also play a critical role in funding research and development efforts focused on environmentally sound technologies.

Businesses involved in the production, distribution, and application of HCFCs are directly affected by the markets dynamics. They are adapting to the regulatory changes by transitioning their operations towards alternative refrigerants and technologies. The economic implications for these businesses vary greatly depending on their ability to adapt to the changing market landscape.

Individuals, as consumers of products utilizing HCFCs (e.g., air conditioners, refrigerators, foam insulation), are indirectly impacted by the phase-out. Consumer behavior and purchasing decisions also play a part in the markets overall transformation. Raising public awareness of the environmental implications is crucial in stimulating a faster transition to eco-friendly alternatives.

| Report Attributes | Report Details |

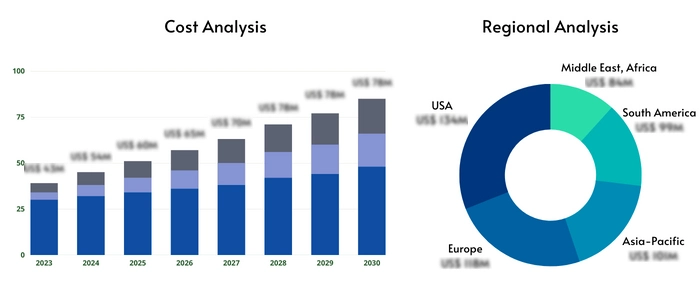

| Base year | 2024 |

| Forecast year | 2025-2032 |

| CAGR % | 5 |

| Segments Covered | Key Players, Types, Applications, End-Users, and more |

| Major Players | Gujarat Fluorochem, Navin Fluorine, Arkema, Dongyue Group, Zhejiang Juhua, Meilan Chem, Sanmei, 3F, Yingpeng Chem, Linhai Limin, Bluestar, Shandong Huaan, Zhejiang Yonghe, China Fluoro, Zhejiang Lantian |

| Types | HCFC-22, HCFC-141b, HCFC-142b, HCFC-123, HCFC-124 |

| Applications | Refrigerant, Foaming Agent, Chemical Materials |

| Industry Coverage | Total Revenue Forecast, Company Ranking and Market Share, Regional Competitive Landscape, Growth Factors, New Trends, Business Strategies, and more |

| Region Analysis | North America, Europe, Asia Pacific, Latin America, Middle East and Africa |

Despite the overall decline, several factors influence the remaining market for HCFCs. These include: existing stockpiles requiring replenishment, particularly in developing countries. limited availability and higher costs of alternative refrigerants in some regions. and the presence of niche applications where viable substitutes havent been fully developed or implemented.

The primary restraint is the strict regulatory framework under the Montreal Protocol, mandating a phase-out of HCFCs. This leads to reduced production and increased costs due to diminishing supply and stricter environmental compliance requirements. The higher costs of substitute refrigerants compared to HCFCs also present a barrier to faster adoption, especially in developing countries.

Opportunities exist in the development and implementation of efficient recycling and reclamation technologies for HCFCs. Further innovation in sustainable refrigerants and the development of efficient and affordable alternatives in developing countries present significant growth prospects. This could include focusing on solutions specific to local contexts, climates, and economic conditions.

The market faces significant challenges related to the complete phase-out of HCFCs and the transition to environmentally sustainable alternatives. These challenges include the need for substantial investments in infrastructure for the handling and disposal of existing HCFCs. The high initial capital costs associated with adopting new refrigerants and technologies represent a considerable barrier for many businesses and developing nations. Technological challenges also remain in developing substitutes that fully match the performance and properties of HCFCs for all applications. Furthermore, the lack of awareness and technical expertise in many regions slows down the transition to sustainable alternatives. Finally, managing the economic implications for businesses and workers involved in the HCFC industry requires careful planning and support from governments and international organizations.

Key trends include the accelerated phase-out of HCFCs globally, a growing emphasis on environmentally friendly alternatives like HFOs and natural refrigerants, increased investments in research and development for next-generation refrigerants, and growing regulations aimed at promoting energy efficiency and environmental protection.

Regional variations in HCFC consumption and the pace of transition to alternatives are significant. Developed nations in North America and Europe are further along in the phase-out process compared to developing nations in Asia Pacific, Latin America, the Middle East, and Africa. Factors influencing regional market dynamics include the level of economic development, existing infrastructure, regulatory stringency, and the availability and affordability of alternative refrigerants. The regulatory environment varies considerably across regions, and policies play a key role in determining the pace of HCFC phase-out. Developed countries generally have stricter regulations and better infrastructure to support the transition, while developing countries often face challenges related to funding, technological capacity, and infrastructure limitations. The higher cost of alternative refrigerants can be a significant barrier to adoption in developing regions, leading to slower transitions and residual demand for HCFCs. Regional differences in climate also influence the demand for refrigeration and air conditioning, thereby indirectly affecting the market.

Q: What is the projected growth rate of the HCFCs market?

A: The HCFCs market is projected to experience a 5% CAGR from 2025 to 2032, although this reflects a declining market due to phase-out efforts.

Q: What are the key trends in the HCFCs market?

A: Key trends include the global phase-out of HCFCs, the rise of HFOs and natural refrigerants, and increased regulatory oversight.

Q: What are the most popular HCFC types?

A: HCFC-22, HCFC-141b, and HCFC-142b were historically the most prevalent, but their use is declining rapidly.

Q: What are the main challenges faced by the HCFCs market?

A: The major challenges include the high costs of alternatives, infrastructure limitations in developing countries, and managing the economic impacts of the phase-out on businesses and workers.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.