ID : MRU_ 435341 | Date : Dec, 2025 | Pages : 245 | Region : Global | Publisher : MRU

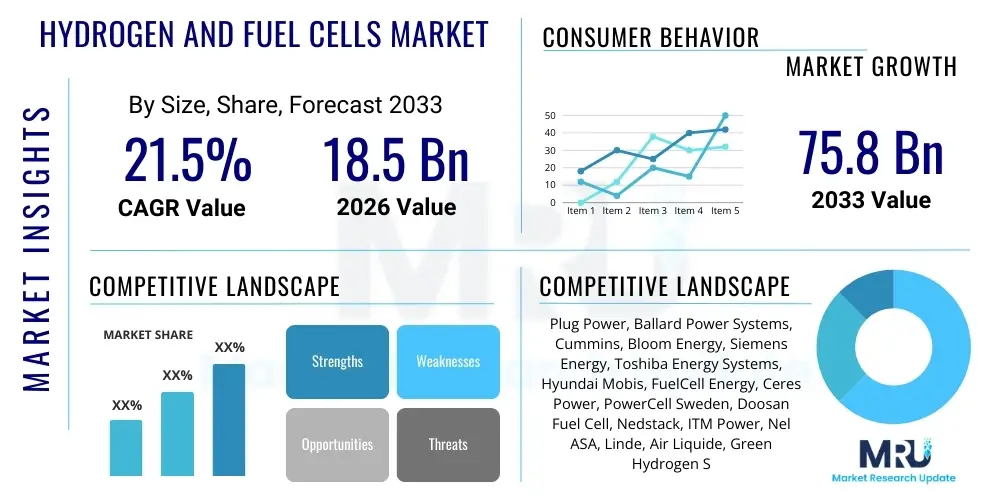

The Hydrogen and Fuel Cells Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 21.5% between 2026 and 2033. The market is estimated at $18.5 Billion in 2026 and is projected to reach $75.8 Billion by the end of the forecast period in 2033.

The global Hydrogen and Fuel Cells Market is fundamentally transforming the energy landscape, positioned as a cornerstone technology in the transition toward decarbonized global energy systems. Hydrogen, utilized as an energy carrier, offers exceptional flexibility for storage and deployment across various sectors, including heavy-duty transport, industrial processes, and grid balancing. Fuel cells, which convert the chemical energy of hydrogen directly into electricity with water as the only significant byproduct, represent a highly efficient and clean power generation technology. This convergence addresses critical climate change imperatives by providing zero-emission solutions for power generation and mobility, attracting substantial investment from both private and public sectors globally.

Major applications for hydrogen and fuel cells span transportation, where they enable long-range, zero-emission vehicles, particularly in commercial trucking, rail, and maritime sectors, and stationary power generation, providing reliable backup power, combined heat and power (CHP) systems, and utility-scale energy storage. The product descriptions include diverse fuel cell types—such as Proton Exchange Membrane Fuel Cells (PEMFCs), Solid Oxide Fuel Cells (SOFCs), and Molten Carbonate Fuel Cells (MCFCs)—each optimized for specific temperature ranges and application requirements. Benefits associated with these technologies include high energy density, reduced reliance on fossil fuels, minimal noise pollution, and enhanced energy security. The scalability of hydrogen production, especially through electrolysis powered by renewable sources (green hydrogen), further cements its role in achieving net-zero emission targets.

Key driving factors accelerating market adoption involve stringent government mandates for carbon reduction, significant technological advancements reducing the cost and improving the lifespan of fuel cell stacks, and rising corporate demand for sustainable energy solutions. Furthermore, large-scale infrastructural investments in hydrogen production facilities, pipelines, and refueling stations are crucial in building the necessary ecosystem. The market is also driven by the increasing integration of intermittent renewable energy sources, where hydrogen acts as a vital buffer, storing excess renewable electricity for later use, thereby stabilizing grid operations and promoting greater utilization of wind and solar power.

The Hydrogen and Fuel Cells Market is experiencing a robust expansion driven primarily by escalating global commitments to achieve net-zero carbon emissions and subsequent regulatory support mechanisms, such as feed-in tariffs and subsidies for green hydrogen projects. Business trends indicate a strong focus on industrial scaling, transitioning from pilot projects to gigafactories for electrolyzers and fuel cell manufacturing, aimed at driving down the levelized cost of hydrogen (LCOH) and ensuring supply chain stability. Strategic collaborations between energy companies, automotive original equipment manufacturers (OEMs), and infrastructure developers are becoming common, emphasizing the integrated approach required for market maturation, particularly in developing robust regional hydrogen hubs and corridors.

Regional trends highlight Asia Pacific (APAC) as a key growth engine, fueled by aggressive national strategies in countries like Japan, South Korea, and China that prioritize hydrogen for both transport and industrial decarbonization. Europe is characterized by significant governmental investment through the European Hydrogen Strategy, focusing heavily on establishing large-scale green hydrogen production capacity and connecting industrial clusters via dedicated hydrogen backbones. North America, particularly the United States, is seeing massive investment spurred by incentives within recent legislative acts, focusing on clean hydrogen production tax credits that fundamentally improve the economic viability of low-carbon hydrogen across various applications.

Segmentation trends show that the Transport segment, encompassing heavy-duty trucks, buses, and maritime vessels, remains the largest revenue contributor due to the compelling economic case for hydrogen in high-utilization, long-range applications where batteries face limitations. However, the Stationary segment is gaining momentum rapidly, driven by the demand for resilient, continuous power generation systems in critical infrastructure and data centers, often utilizing Solid Oxide Fuel Cells (SOFCs) due to their high electrical efficiency. Furthermore, the Green Hydrogen segment is projected to exhibit the fastest CAGR, supported by declining renewable energy costs and policy shifts favoring hydrogen produced via renewable energy electrolysis, moving away from conventional carbon-intensive production methods (Grey Hydrogen).

User queries regarding the intersection of Artificial Intelligence (AI) and the Hydrogen and Fuel Cells market frequently center on how AI optimizes the efficiency of production processes, manages complex grid integration, and accelerates material science innovation. Key themes include the use of machine learning for predictive maintenance of fuel cell stacks, enhancing the operational lifespan and reliability, and the application of optimization algorithms to balance hydrogen supply and demand dynamically within emerging regional hubs. Users are concerned about the complexity of managing large-scale decentralized hydrogen networks and view AI as the critical technology to ensure stability, minimize energy input costs for electrolysis, and maximize the economic return on infrastructure investments. Expectations are high that AI will be the primary tool enabling the shift from centralized, fossil-fuel-dependent grids to resilient, distributed, hydrogen-supported energy ecosystems.

AI is poised to revolutionize the entire hydrogen value chain, from production and storage to distribution and end-use. In production, AI algorithms can predict optimal renewable energy availability and consumption patterns, adjusting electrolyzer load factors in real-time to maximize efficiency and minimize input energy costs, crucial for competitive green hydrogen pricing. For fuel cell manufacturing, AI-driven quality control and design optimization, leveraging computational fluid dynamics and materials informatics, significantly shorten R&D cycles and improve stack performance metrics such as power density and durability. Furthermore, AI systems are essential for managing the dynamic injection and withdrawal of hydrogen in large-scale storage facilities, optimizing inventory based on fluctuating energy market prices and operational constraints.

The integration of hydrogen assets into existing electrical grids poses significant stability challenges, which AI is uniquely positioned to solve. AI-powered smart grid management systems analyze vast streams of data from renewable sources, electrolyzers, compressors, and fuel cell generators to forecast localized energy needs and coordinate hydrogen asset dispatch instantaneously. This predictive capability prevents bottlenecks and ensures that hydrogen facilities function effectively as flexible grid assets, providing essential ancillary services like frequency regulation. The impact extends to enhancing safety protocols, with AI monitoring sensor data within hydrogen storage and transport infrastructure to detect anomalies and predict potential failures long before human intervention would be possible, thereby mitigating risks associated with highly flammable gas handling.

The Hydrogen and Fuel Cells Market is characterized by powerful drivers rooted in climate policy and energy security concerns, balanced against significant restraints related primarily to cost and infrastructure maturity. Opportunities abound in niche high-value applications and technological advancements that promise to unlock mass market adoption. The central impact forces revolve around governmental commitment to decarbonization targets and sustained private investment necessary to achieve economies of scale. Successful market penetration hinges on overcoming the initial high capital expenditure required for production and distribution infrastructure, coupled with the need for standardization across global supply chains. The synergy between political will and technological innovation is the core determinant of the market trajectory over the forecast period.

Key drivers include the imperative for industrial decarbonization, particularly in hard-to-abate sectors such as steel, cement, and chemical production, where hydrogen offers one of the few viable pathways to emission reduction. Furthermore, the global push for zero-emission mobility extends beyond passenger vehicles to include heavy-duty transport, marine, and aviation, establishing a substantial long-term demand base for fuel cell systems. However, significant restraints currently temper growth, most notably the high capital cost of producing green hydrogen compared to natural gas reforming (Grey Hydrogen), although this gap is rapidly closing. The lack of a comprehensive, nationwide hydrogen pipeline infrastructure in many major economies also acts as a bottleneck, hindering cost-effective large-scale distribution from production sites to end-users.

Opportunities for market players lie in exploiting technological breakthroughs that reduce the reliance on expensive materials like platinum group metals (PGMs) in PEM fuel cells and in developing highly efficient, robust solid-oxide technologies for distributed power generation. The concept of "Power-to-X," where surplus renewable electricity is converted into hydrogen (P2H) and subsequent synthetic fuels, opens vast market potential for hydrogen as a long-duration energy storage solution and an input for sustainable aviation or maritime fuels. The primary impact forces shaping the competitive landscape are government subsidies, such as those seen in the Inflation Reduction Act (IRA) in the US and equivalent European instruments, which drastically alter project economics and accelerate private capital deployment, essentially de-risking early-stage infrastructure projects and pushing hydrogen into cost-competitiveness against traditional energy sources.

The Hydrogen and Fuel Cells market is fundamentally segmented across technology type, application area, and the method used for hydrogen production, reflecting the diverse end-use requirements and maturity levels of various solutions. Segmentation by product (fuel cell type) reveals the competitive dynamic between PEMFCs, dominant in the transport sector due to their fast start-up times and lower operating temperatures, and SOFCs, favored for stationary applications due to their high electrical efficiency and ability to utilize multiple fuels. The market structure emphasizes the shift towards modular, scalable solutions that can address needs ranging from residential backup power to multi-megawatt industrial installations. This granularity helps stakeholders target investment towards the most rapidly growing and technologically viable segments, ensuring resources are allocated efficiently to maximize market penetration and profitability in the highly competitive clean energy sector.

The Hydrogen and Fuel Cells value chain is complex and highly integrated, starting with upstream activities focused on fuel generation and purification, extending through manufacturing and integration, and culminating in downstream distribution and end-use services. Upstream activities are dominated by hydrogen production, involving either steam methane reforming (SMR) for conventional hydrogen or electrolysis powered by renewable energy for green hydrogen. Key challenges in this stage include achieving economies of scale in electrolyzer manufacturing and securing long-term, low-cost renewable energy supply. Purification and compression technologies are also crucial in the upstream stage to meet the strict quality requirements for fuel cell operation and efficient transportation.

The middle segment focuses on the manufacturing of core components, including fuel cell stacks (bipolar plates, catalysts, membranes, and electrodes) and balance-of-plant components. This segment is characterized by intense R&D aimed at developing cheaper, more durable materials, thereby driving down system costs. Downstream activities encompass the distribution channel, which is currently undergoing significant transformation. Direct distribution involves delivering packaged hydrogen units (e.g., tubes, bundles) to large industrial customers or refueling depots, whereas indirect distribution relies on developing a pervasive pipeline network and liquid hydrogen terminals, which requires massive infrastructural investment and long-term regulatory planning.

Direct channels, typically utilized for high-purity industrial gases or localized power installations, allow manufacturers to maintain greater control over product quality and delivery timelines. Indirect channels, primarily focused on mobility and utility-scale energy, necessitate partnerships with established energy distributors and utility companies. The expansion of hydrogen hubs, connecting production sites directly to industrial consumers via short pipelines, exemplifies a hybrid distribution model aimed at minimizing transportation costs. The entire value chain relies heavily on robust safety standards and regulatory harmonization to ensure secure handling and widespread public acceptance of hydrogen technologies.

The potential customer base for the Hydrogen and Fuel Cells Market is highly diversified, ranging from large-scale energy utility operators seeking grid stability solutions to individual commercial operators adopting clean vehicle fleets. Primary end-users fall into three broad categories: Transportation, Stationary Power, and Industrial feedstock. In the Transportation sector, buyers include major Automotive OEMs and fleet operators (e.g., logistics companies, public transport agencies) investing in hydrogen fuel cell electric vehicles (FCEVs), particularly for heavy-duty applications where extended range and fast refueling times are essential differentiators compared to battery electric alternatives. Maritime and rail industries represent rapidly emerging high-value segments due to the specific power demands and operational profiles requiring hydrogen's high energy density.

In the Stationary Power segment, key buyers include operators of critical infrastructure such as hospitals, telecommunication centers, and data centers that require highly reliable, resilient backup and continuous power solutions, often favoring SOFC systems for combined heat and power (CHP). Furthermore, municipal and private utilities are major customers, leveraging fuel cells for distributed generation and using hydrogen as a mechanism for long-duration energy storage to integrate variable renewable power sources effectively into the grid. The industrial segment represents a massive potential customer base, notably steel manufacturers, fertilizer producers (ammonia), and chemical companies, who are pivoting away from carbon-intensive processes and seeking large volumes of green or blue hydrogen as a clean feedstock to meet decarbonization targets and remain compliant with increasingly strict environmental regulations imposed globally.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | $18.5 Billion |

| Market Forecast in 2033 | $75.8 Billion |

| Growth Rate | CAGR 21.5% |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Plug Power, Ballard Power Systems, Cummins, Bloom Energy, Siemens Energy, Toshiba Energy Systems, Hyundai Mobis, FuelCell Energy, Ceres Power, PowerCell Sweden, Doosan Fuel Cell, Nedstack, ITM Power, Nel ASA, Linde, Air Liquide, Green Hydrogen Systems, McPhy Energy, Mitsubishi Heavy Industries, Nikola Corporation. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological landscape of the Hydrogen and Fuel Cells Market is characterized by intense innovation across three primary domains: hydrogen production, storage/distribution, and fuel cell stack efficiency. In production, the rapid development of low-cost, highly efficient electrolyzers—specifically Polymer Electrolyte Membrane (PEM) and Alkaline Electrolyzers—is critical for scaling green hydrogen. Research is focused on increasing current density, enhancing catalyst longevity, and designing modular systems that can seamlessly integrate with intermittent renewable power sources. Furthermore, advancements in solid-oxide electrolysis cells (SOEC) are being pursued for high-temperature applications where waste heat is available, boosting overall energy conversion efficiency compared to conventional methods.

Storage and distribution technologies are equally crucial, driven by the need to handle hydrogen safely and cost-effectively at high pressures or cryogenic temperatures. Innovations include the development of advanced composite materials for high-pressure Type IV storage tanks, lightweight components vital for vehicular applications, and research into solid-state storage technologies (e.g., metal hydrides) that promise higher volumetric energy density and enhanced safety for portable and stationary uses. The construction of dedicated hydrogen pipelines, requiring specialized materials and leakage detection systems, constitutes a major infrastructure challenge currently being addressed through material science and sophisticated monitoring technologies.

Within fuel cell technology itself, the focus remains on reducing the cost and increasing the durability of the stack. For PEMFCs, this involves decreasing the loading of expensive Platinum Group Metal (PGM) catalysts or substituting them entirely with non-PGM alternatives, alongside improving membrane durability to withstand varying operating conditions. For high-temperature SOFCs, efforts are concentrated on developing cheaper, more robust interconnect materials and reducing operating temperatures to broaden the range of feasible applications. The integration of advanced power electronics and control systems is also critical for optimizing system performance, managing thermal output, and ensuring long operational lifecycles under demanding industrial and transport use cases.

The global Hydrogen and Fuel Cells market exhibits significant regional variation in adoption rates and strategic focus, largely dictated by local energy resources, industrial structure, and government policy frameworks. Asia Pacific (APAC) leads the market in terms of deployment and investment, driven primarily by ambitious governmental hydrogen roadmaps in nations like Japan and South Korea, which view hydrogen as essential for energy independence and industrial supremacy. China’s substantial investments in fuel cell vehicle fleets and localized hydrogen production centers further solidify APAC’s dominance. The region is characterized by a strong focus on both stationary SOFC deployments and PEMFCs in captive fleets and heavy transport, aiming for swift commercialization and scale across high-density urban areas.

Europe is positioned as a powerful accelerator of green hydrogen development, backed by the European Green Deal and Hydrogen Strategy. The region is aggressively funding projects aimed at establishing a transnational hydrogen pipeline infrastructure (the European Hydrogen Backbone) connecting high-production areas (e.g., Iberia, North Sea) to industrial demand clusters (e.g., Ruhr Valley). The focus here is heavily skewed toward decarbonizing industrial feedstock use and integrating hydrogen into the energy grid as a primary storage vector, supported by robust regulatory mechanisms like carbon pricing that incentivize the switch to clean alternatives.

North America, particularly the United States, is undergoing a rapid market expansion phase, primarily fueled by supportive fiscal policies such as the Clean Hydrogen Production Tax Credit outlined in the Inflation Reduction Act. This incentivizes low-carbon hydrogen production, making it economically competitive. The US strategy emphasizes regional hydrogen hubs—clusters designed to connect production, distribution, and end-use across industrial, mobility, and power generation sectors. Canada is also active, leveraging its vast renewable resources for green hydrogen exports. Meanwhile, the Middle East and Africa (MEA) region is emerging as a critical global supplier of green and blue hydrogen, capitalizing on abundant solar resources (e.g., Saudi Arabia, UAE) and favorable geographical locations for export to Europe and Asia, positioning itself as a future hydrogen export powerhouse.

The primary factor driving green hydrogen demand is the stringent global mandate for industrial decarbonization and achieving net-zero emissions targets. Green hydrogen, produced via renewable energy electrolysis, offers a zero-carbon energy carrier necessary for reducing emissions in hard-to-abate sectors like heavy transport, chemicals, and steel manufacturing, supported by favorable government subsidies and tax incentives worldwide.

Proton Exchange Membrane Fuel Cells (PEMFCs) operate at low temperatures (below 100°C), offer fast start-up times, and are primarily used in the transport sector (FCEVs). Solid Oxide Fuel Cells (SOFCs) operate at high temperatures (600°C–1000°C), enabling higher electrical efficiency (up to 60%) and fuel flexibility (e.g., natural gas, hydrogen). SOFCs are predominantly utilized for stationary power generation and combined heat and power (CHP) systems.

The main technological challenges include the high capital cost of electrolyzers, the reliance on expensive platinum group metals (PGMs) in PEM fuel cells, and the need for standardized, cost-effective methods for hydrogen storage and large-scale distribution over long distances, such as robust pipeline infrastructure and cryogenic handling technologies.

Asia Pacific (APAC) currently holds the largest market share, driven by extensive governmental hydrogen strategies and significant investment in fuel cell vehicles (FCEVs) and stationary power applications, particularly in key economies like Japan, South Korea, and China, which have prioritized hydrogen for energy transition.

The U.S. Inflation Reduction Act (IRA) provides substantial financial incentives, most notably the Clean Hydrogen Production Tax Credit, which drastically lowers the cost of producing low-carbon hydrogen. This policy is instrumental in accelerating private investment, fostering the development of regional Hydrogen Hubs, and rapidly moving green and blue hydrogen projects toward economic viability and large-scale deployment.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.