ID : MRU_ 437192 | Date : Dec, 2025 | Pages : 243 | Region : Global | Publisher : MRU

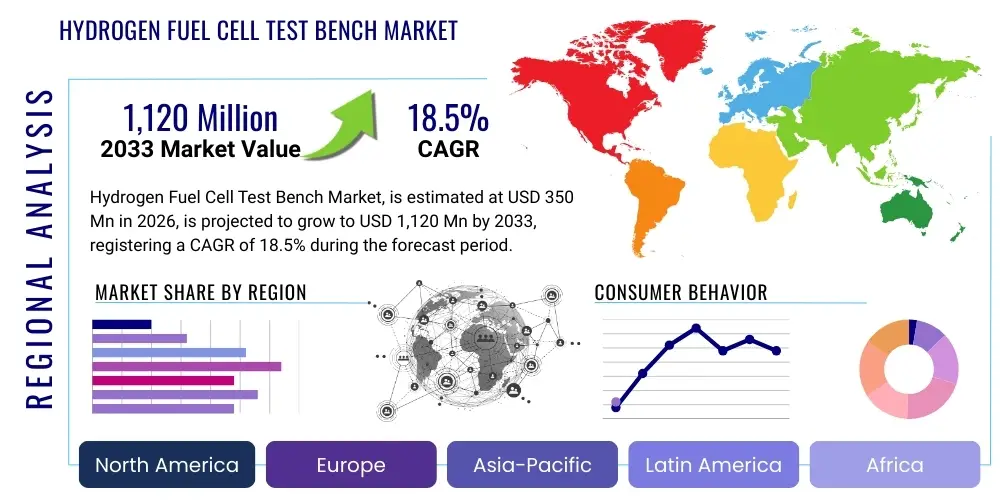

The Hydrogen Fuel Cell Test Bench Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 18.5% between 2026 and 2033. The market is estimated at USD 350 Million in 2026 and is projected to reach USD 1,120 Million by the end of the forecast period in 2033. This substantial expansion is primarily driven by the global acceleration of hydrogen infrastructure development and the increasing commercialization of fuel cell electric vehicles (FCEVs) and stationary power generation units. Regulatory mandates encouraging decarbonization across major economies necessitate rigorous quality assurance and performance validation of new fuel cell stacks, directly boosting demand for advanced, high-precision test bench systems.

The Hydrogen Fuel Cell Test Bench Market encompasses specialized equipment designed for the exhaustive performance evaluation, durability testing, and quality control of various types of hydrogen fuel cells, predominantly Proton Exchange Membrane Fuel Cells (PEMFCs) and Solid Oxide Fuel Cells (SOFCs). These sophisticated systems simulate real-world operating conditions, including variations in temperature, humidity, gas flow, and electrical load, to validate the efficiency and reliability of the cell stacks and systems before integration into final applications. Product offerings range from small-scale component test stations used in academic research to large, high-power dynamic test benches essential for automotive and maritime applications.

Major applications driving the test bench market include the automotive sector, focusing on FCEVs (passenger cars, buses, and trucks), which requires dynamic load testing and long-cycle durability assessments. Additionally, the stationary power market utilizes test benches for ensuring the stability and lifespan of combined heat and power (CHP) systems and uninterrupted power supply (UPS) units. The inherent benefits of these test benches lie in their ability to significantly reduce time-to-market, enhance product safety, and optimize operational parameters, thereby facilitating the mass production and commercial acceptance of hydrogen technologies as a viable clean energy source.

Driving factors for market growth are profoundly linked to global decarbonization efforts, massive public and private investment in the hydrogen economy, and technological advancements focusing on increasing fuel cell power density and reducing manufacturing costs. Specifically, the necessity for standardized testing procedures to meet stringent international safety and performance standards (such as IEC and ISO) acts as a persistent demand driver. Furthermore, the push towards integrating renewable energy sources often requires backup power solutions, where highly reliable stationary fuel cells, validated by precise testing equipment, play a crucial role.

The Hydrogen Fuel Cell Test Bench Market is undergoing rapid evolution, characterized by increased integration of digitalization and sophisticated control systems to meet the demands of higher power density fuel cells. Business trends highlight a shift towards modular and customizable test solutions capable of handling diverse stack sizes and system configurations, catering to emerging sectors like heavy-duty transport and aviation. Key market players are prioritizing collaborations with major automotive original equipment manufacturers (OEMs) and national research laboratories to co-develop next-generation testing protocols, focusing heavily on non-destructive diagnostics and accelerated aging tests. The competitive landscape is marked by intense technological innovation centered on improving energy recovery capabilities during testing to enhance operational efficiency and reduce the overall cost of ownership for end-users.

Regional trends indicate that Asia Pacific (APAC), particularly China, Japan, and South Korea, maintains dominance due to robust governmental support for FCEV adoption and established manufacturing capabilities. Europe shows the fastest growth momentum, fueled by the European Green Deal and significant investments into hydrogen valleys, which require expansive R&D infrastructure, including cutting-edge test benches. North America, stimulated by policies such as the Inflation Reduction Act (IRA), is witnessing escalating demand, particularly for high-power, heavy-duty fuel cell testing necessary for long-haul trucking and industrial applications. The regional divergence in policy and application focus necessitates localized product tailoring and service specialization among test bench manufacturers.

Segment trends reveal a strong preference for high-power test benches (over 150 kW) driven by the commercialization of fuel cell applications in heavy transportation and maritime domains. The application segment sees research and development (R&D) centers remaining the primary users, although the manufacturing and production segment is forecast to show the highest CAGR as mass production ramps up. Technology-wise, dynamic load simulation capabilities are becoming standard requirements, moving beyond simple static load testing. The core strategic focus across all segments remains the accurate simulation of real-world duty cycles, combined with advanced diagnostic tools like Electrochemical Impedance Spectroscopy (EIS) to gather deeper insights into degradation mechanisms.

Common user inquiries regarding the impact of Artificial Intelligence (AI) on the Hydrogen Fuel Cell Test Bench Market frequently revolve around how AI can enhance test efficiency, accelerate the discovery of failure modes, and optimize the operational lifespan of fuel cell stacks. Users are keen to understand the application of machine learning (ML) in predicting degradation patterns based on sensor data streams, thereby moving testing methodologies from reactive validation to proactive prognostics. Major concerns include the reliability of AI algorithms in handling complex, non-linear electrochemical processes and the cybersecurity implications of integrating large-scale data platforms. Expectations center on AI significantly reducing the duration of long-term durability tests, automating complex test sequences, and improving the precision of fault isolation diagnostics, ultimately lowering R&D costs and speeding up commercialization.

AI’s influence is transforming the test bench environment by enabling predictive maintenance for the testing equipment itself and, more critically, for the fuel cell under scrutiny. Machine learning models analyze vast datasets generated during operational cycles, identifying subtle correlations between operational parameters (such as reactant flow rates, pressure differentials, and temperature) and performance degradation metrics. This allows researchers to quickly identify optimal operating windows and pinpoint critical stress factors without relying solely on traditional, time-consuming statistical analysis. Furthermore, AI-driven control systems can dynamically adjust test parameters in real time, simulating highly complex and varied duty cycles more accurately than conventional programming, thus reflecting real-world usage more faithfully.

The integration of AI also facilitates the creation of high-fidelity digital twins of fuel cell stacks. These virtual models, constantly refined by real-world testing data, allow for extensive simulation of scenarios that would be impractical or excessively expensive to run physically. This accelerates design iteration and validation. By utilizing deep learning algorithms, test bench software can automatically generate comprehensive reports, categorize failure modes (e.g., carbon corrosion, membrane drying, or catalyst poisoning), and suggest structural or material improvements, transitioning the test bench from a measurement tool to an integrated optimization platform, directly impacting the speed and success rate of new product development.

The Hydrogen Fuel Cell Test Bench Market is shaped by powerful synergistic forces: global mandates for decarbonization and sustainable energy transition (Drivers) are counterbalanced by high infrastructure capital costs and the technical complexities of hydrogen storage and handling (Restraints). However, the growing potential of hydrogen in niche, high-value sectors like maritime and aviation offers significant market Expansion Opportunities. These forces collectively dictate the investment landscape and technology adoption rates, creating a high-growth yet technologically demanding market environment where reliability and precision testing are paramount for risk mitigation and rapid commercial viability.

Drivers: The most significant driver is the increasing global commitment to hydrogen as a cornerstone of clean energy strategies, backed by substantial governmental incentives in regions like the EU, North America, and APAC. This commitment fuels massive R&D expenditures in both PEMFC and SOFC technologies, necessitating high volumes of specialized testing equipment. Secondly, the push by major automotive OEMs to transition their heavy-duty fleets to FCEVs requires dynamic and robust test benches capable of simulating extreme duty cycles with high precision and safety standards. Furthermore, the inherent need for regulatory compliance and safety certification (e.g., crash safety standards, electrical safety, operational stability) mandates the use of certified, high-quality test benches throughout the development and manufacturing lifecycle.

Restraints: A primary restraint is the substantial initial capital investment required to purchase, install, and maintain high-power fuel cell test benches, which often include sophisticated power electronics, gas handling systems, and advanced diagnostic tools. This cost barrier can limit entry for smaller research institutions or nascent manufacturing startups. Another critical challenge is the complexity associated with handling hydrogen safely, requiring specialized infrastructure and highly trained personnel, increasing operational overheads. Technical restraints include the challenge of developing test protocols that accurately reflect the severe operating conditions and rapid degradation mechanisms experienced in real-world high-power applications, leading to extended and costly testing periods.

Opportunity: Significant opportunities arise from the diversification of fuel cell applications beyond automotive into large-scale, high-power domains such as marine transport, aviation (drones and small aircraft), and large data center backup power. These sectors demand bespoke, high-voltage test solutions, opening new avenues for specialized test bench manufacturers. The global focus on standardizing testing methodologies (e.g., harmonizing durability testing cycles) also presents an opportunity for companies that can lead the development of universal, certified test platforms. Lastly, the integration of advanced technologies like AI and machine learning into diagnostic software creates opportunities for value-added services and recurring revenue streams through software licensing and maintenance contracts, transitioning the market towards smart, integrated testing solutions.

The Hydrogen Fuel Cell Test Bench Market is comprehensively segmented based on its technical specifications, application focus, and power output capabilities, reflecting the diverse requirements across the fuel cell value chain. Segmentation by component (e.g., stack test systems vs. BOP systems) helps differentiate solutions tailored for fundamental electrochemical research versus system-level integration testing. Application segmentation, spanning R&D, academia, and commercial manufacturing, captures the differing scales and precision requirements of end-users. Power output remains a critical differentiator, separating low-power academic benches from high-power (greater than 150 kW) commercial platforms necessary for heavy transport applications. This structured segmentation is vital for manufacturers to align product portfolios with specific market needs and for purchasers to select systems appropriate for their target fuel cell technology and scale of operation.

The dominance of the Proton Exchange Membrane Fuel Cell (PEMFC) segment is evident due to its suitability for transportation applications, requiring highly dynamic test benches capable of simulating transient conditions. Conversely, the rising importance of Solid Oxide Fuel Cells (SOFCs) in stationary power mandates specialized test benches capable of enduring high-temperature operation and long, static durability cycles. Geographically, segmentation highlights the concentration of demand in established FCEV markets like APAC and Europe. The evolution of the market is increasingly favoring modularity, where test benches can be easily adapted to switch between different cell chemistries or scale up power output with minimal hardware modification, reflecting a strategic response to the fluid technological landscape of hydrogen energy.

The value chain for the Hydrogen Fuel Cell Test Bench Market begins with the Upstream segment, dominated by suppliers of high-precision measurement instruments, specialized sensor technology (e.g., pressure, temperature, humidity), advanced power electronics (DC loads, power supplies, DC/DC converters), and sophisticated gas handling components (mass flow controllers, humidifiers, back pressure regulators). Quality and reliability in this initial stage are crucial as the accuracy of the final test bench is directly dependent on the calibration and performance of these core components. Key industry alliances are often formed between specialized sensor manufacturers and test bench integrators to ensure system integrity and compliance with electrochemical testing standards.

The Midstream component consists of the core Test Bench Manufacturers and System Integrators. These entities design, assemble, and integrate the proprietary control software and hardware necessary to create a functioning test environment. Their competitive edge is derived from developing specialized software for dynamic load simulation, advanced diagnostic capabilities (like EIS), and robust safety protocols for hydrogen operation. Distribution Channels include Direct Sales models, where large OEMs purchase systems directly from manufacturers for their R&D centers, and Indirect Channels, involving specialized distributors or system integrators who provide local service, customization, and technical support, especially in geographically dispersed markets like APAC.

The Downstream phase involves the end-users: Automotive OEMs who validate their FCEV stacks, Independent Testing Laboratories offering certification services, and National Research Institutions focusing on material science and stack longevity studies. Feedback from these downstream users is critical for continuous product improvement, especially concerning the accuracy of real-world duty cycle simulation and the need for higher energy recovery efficiency within the test environment. The direct distribution channel dominates high-value, bespoke system sales, while standardized, lower-power benches often utilize indirect channels for broader market penetration and ease of localized maintenance and calibration services.

The primary consumers and End-Users of Hydrogen Fuel Cell Test Bench systems are large-scale industrial organizations heavily invested in developing, manufacturing, and commercializing hydrogen energy solutions. This group includes Global Automotive Original Equipment Manufacturers (OEMs) such as Toyota, Hyundai, and European truck manufacturers, who require comprehensive testing for their FCEV platforms, demanding high-power dynamic load systems for full system validation. These OEMs prioritize systems that offer rapid testing throughput, highly repeatable results, and advanced data analytics capabilities to expedite their vehicle development cycles and meet stringent market release deadlines.

Another significant segment comprises specialized Independent Testing Laboratories and Certification Bodies (e.g., TÜV SÜD, UL). These organizations purchase test benches to offer third-party validation, safety certification, and performance benchmarking services to fuel cell developers globally. Their requirements are centered around standardization, traceability, and the ability to test a wide variety of cell chemistries and power outputs according to international standards (ISO, IEC). The continuous evolution of regulatory frameworks drives persistent demand from this customer base, requiring frequent upgrades and calibration services to maintain accreditation status.

Furthermore, National and International Research Institutions and prominent Universities constitute a substantial customer base, focusing on fundamental material science, stack degradation mechanisms, and novel component optimization. These academic buyers generally require lower to medium power benches (typically below 50 kW) equipped with highly specialized diagnostic tools such as sophisticated gas chromatography and impedance analyzers. Government-funded energy research programs globally ensure consistent demand from this sector, prioritizing flexibility, precision, and the ability to integrate custom experimental setups for deep scientific inquiry into electrochemical processes.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 350 Million |

| Market Forecast in 2033 | USD 1,120 Million |

| Growth Rate | 18.5% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | FuelCon (HORIBA), Greenlight Innovation, AVL List GmbH, KRATOS, Power Electronics, Arcola Energy, Nuvant Systems, FCT S.R.L., M&M Control, TdV Engineering, Wuxi Lead Intelligent Equipment Co., Ltd., Shanghai Shenli High-Tech, S+P Clever Projects, DANA Incorporated (Nordresa), Technovision, Teledyne Energy Systems, Kolbenschmidt Pierburg, Wenzhou Dongbo Power Equipment, Heliocentris, Testek Inc. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological landscape of the Hydrogen Fuel Cell Test Bench Market is defined by a shift towards highly integrated, software-driven systems designed for dynamic stress testing and enhanced energy efficiency. A core advancement is the proliferation of high-speed, high-accuracy power electronics, specifically regenerative DC electronic loads. These loads are crucial as they capture the energy generated by the fuel cell during testing and feed it back into the grid, significantly reducing the operational cost and carbon footprint associated with long-duration durability testing. The ability to efficiently manage and recycle this energy is becoming a prerequisite for large-scale manufacturing test applications, moving away from resistive loads that dissipate energy as waste heat.

Electrochemical Impedance Spectroscopy (EIS) integration represents another pivotal technology. EIS involves applying a small AC signal across the cell to analyze the resulting impedance, providing non-destructive, real-time diagnostic information about the cell’s internal state, including membrane degradation, catalyst activity, and mass transport limitations. Modern test benches integrate EIS measurement capabilities seamlessly into their control software, allowing researchers to correlate degradation patterns directly with specific operating conditions simulated during dynamic cycling. This level of granular diagnostic insight is essential for optimizing fuel cell material composition and operational strategies, accelerating the identification of failure modes far faster than traditional current-voltage curve analysis alone.

Furthermore, advancements in humidification and thermal management systems within the test benches are critical, particularly for PEMFC testing. High-precision humidifiers and temperature control units are necessary to replicate the exact moisture and thermal gradients encountered in real-world environments, which profoundly impact fuel cell performance and longevity. The utilization of sophisticated, integrated safety systems—including hydrogen leak detection, inert gas purging mechanisms, and emergency shutdown protocols managed by redundant PLCs—is standard practice. This comprehensive approach to safety is mandated by the inherent volatility of hydrogen and ensures secure testing environments for high-pressure and high-power experimental setups, supporting regulatory compliance globally.

Regional dynamics play a crucial role in shaping the Hydrogen Fuel Cell Test Bench Market, driven primarily by localized energy policies, industrial concentration, and governmental funding priorities. Asia Pacific (APAC) stands as the largest market, largely due to extensive governmental support in nations like China, South Korea, and Japan, which have set aggressive targets for hydrogen adoption in mobility and stationary power. China, in particular, dominates the manufacturing volume for both fuel cell components and test bench equipment, benefiting from state subsidies and a massive domestic automotive market shifting towards FCEVs. South Korea and Japan focus on high-precision, highly specialized testing systems to maintain their technological lead in PEMFC development.

Europe is positioned as the fastest-growing region, stimulated by the European Green Deal and national hydrogen strategies (e.g., Germany, France). This region emphasizes R&D and standardization, driving demand for advanced, flexible test benches suitable for multiple fuel cell types, including high-temperature SOFCs for stationary applications and high-power PEMFCs for heavy-duty transport (trucks, trains). European growth is also characterized by a strong focus on high energy efficiency in testing, leading to a high adoption rate of regenerative electronic load technology.

North America, led by the United States, is experiencing accelerated growth following favorable policy incentives like the Inflation Reduction Act (IRA), which promotes domestic hydrogen production and fuel cell manufacturing. The primary regional focus is on high-power testing for heavy-duty commercial vehicle applications, marine vessels, and extensive R&D collaboration between universities and private sector giants. The region demands robust, scalable test solutions that can handle the high voltage and current requirements necessary for large-scale mobility solutions, often integrated with sophisticated data security protocols.

The primary function is to rigorously validate the performance, durability, and safety of hydrogen fuel cell stacks and complete systems by simulating varied operational parameters, including load cycling, temperature, humidity, and gas flow, crucial for R&D and quality control before commercial deployment.

The High Power (Above 150 kW) segment is exhibiting the fastest growth. This acceleration is driven by the commercialization of fuel cells for heavy-duty applications such as long-haul trucks, buses, trains, and maritime vessels, which require significantly higher power testing capabilities than passenger vehicles.

EIS is a non-destructive diagnostic technique integrated into advanced test benches that measures the cell's internal impedance. This provides real-time, detailed insights into critical degradation mechanisms, such as catalyst poisoning or membrane drying, helping researchers optimize material composition and operational strategies more effectively.

Key challenges include developing high-precision dynamic load simulators capable of accurately replicating extreme real-world duty cycles, ensuring the robust safety management of hydrogen gas, and improving the energy recovery efficiency of regenerative loads to reduce operational testing costs for end-users.

AI is employed to analyze complex testing data for predictive diagnostics, automate the optimization of test sequences, and create digital twin models. This integration significantly reduces the duration of durability tests and accelerates the identification of subtle failure patterns, enhancing overall R&D efficiency.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.