ID : MRU_ 437083 | Date : Dec, 2025 | Pages : 251 | Region : Global | Publisher : MRU

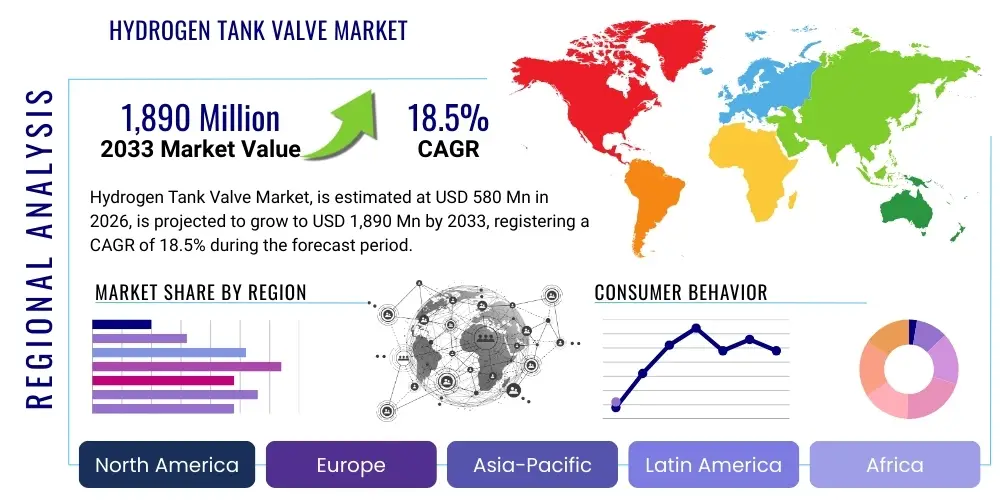

The Hydrogen Tank Valve Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 18.5% between 2026 and 2033. The market is estimated at USD 580 Million in 2026 and is projected to reach USD 1,890 Million by the end of the forecast period in 2033. This robust expansion is primarily driven by global decarbonization efforts, increasing investment in hydrogen infrastructure, and the mass adoption of Fuel Cell Electric Vehicles (FCEVs) and hydrogen-powered commercial transport, which require highly reliable and specialized valve systems capable of handling extreme pressures and cryogenic temperatures associated with hydrogen storage.

The Hydrogen Tank Valve Market encompasses specialized mechanical components essential for controlling the flow, pressure, and safety of highly compressed or liquefied hydrogen stored in high-pressure vessels, predominantly within mobility and industrial applications. These valves are critical safety elements, designed to withstand extreme operating conditions, including pressures up to 70 MPa (700 bar) and temperatures ranging from cryogenic levels for liquid hydrogen to ambient levels for compressed gas storage. The integrity and reliability of these valves, often manufactured from specialized stainless steels and robust sealing materials, are paramount for preventing leakage and ensuring safe operation in mission-critical environments like automotive fuel systems and large-scale refueling stations.

Major applications driving market demand include the rapidly expanding sector of Fuel Cell Electric Vehicles (FCEVs), particularly heavy-duty trucks, buses, and passenger cars, where Type IV carbon fiber reinforced tanks require sophisticated fill and shut-off valves. Furthermore, the burgeoning global hydrogen ecosystem includes extensive requirements for storage valves in stationary power generation, industrial blending processes, and large-scale hydrogen distribution networks. Key benefits provided by high-quality hydrogen tank valves include enhanced safety through rapid shut-off mechanisms, precise pressure regulation, and long operational lifetimes compliant with stringent international standards such as EC 79/2009 and ISO 19881. The driving factors fueling this market are predominantly supportive government policies, increasing private sector investments in green hydrogen production, and technological advancements focusing on reducing the size, weight, and cost of high-pressure components while maintaining zero-leak tolerance.

The Hydrogen Tank Valve Market is poised for exceptional growth throughout the forecast period, underpinned by transformative business trends focusing on vertical integration and standardization of 70 MPa (700 bar) systems. Key industry players are increasingly investing in sophisticated testing facilities and adopting advanced manufacturing techniques, such as additive manufacturing, to produce valves optimized for hydrogen compatibility and durability, addressing issues like hydrogen embrittlement. The competitive landscape is characterized by strategic partnerships between valve manufacturers and hydrogen tank/system integrators to co-develop lighter, more cost-effective tank systems, responding directly to original equipment manufacturers (OEM) demands for improved vehicle range and reduced component footprints.

Regionally, Asia Pacific, particularly Japan, South Korea, and China, dominates the segment trends due to aggressive national strategies supporting FCEV deployment and establishing extensive hydrogen refueling infrastructure. Europe is exhibiting strong growth, driven by ambitious Green Deal initiatives and significant investments in long-haul hydrogen trucking and industrial decarbonization projects, creating substantial demand for stationary storage and transport valves. Segment trends reveal a strong shift toward valves optimized for Type IV composite tanks and ultra-high-pressure applications (70 MPa), driven by automotive requirements, while the increasing adoption of Liquid Hydrogen (LH2) solutions in aerospace and long-distance maritime transport is opening specialized opportunities for cryogenic valve technology development.

Users frequently inquire about how artificial intelligence (AI) can enhance the safety, reliability, and manufacturing efficiency of critical high-pressure components like hydrogen tank valves. Common concerns revolve around predictive failure analysis, optimizing complex valve designs for material stress under cyclical loading, and automating quality control during the production phase. The key themes summarized from these user expectations include leveraging AI for real-time monitoring of valve health in operational FCEVs and refueling stations, using machine learning to simulate and refine component longevity against hydrogen embrittlement, and employing generative design algorithms to optimize flow characteristics and minimize weight without compromising structural integrity. This integration of AI promises to elevate the standard of component reliability, which is crucial for public and industrial safety in the hydrogen economy.

The Hydrogen Tank Valve Market is influenced by a powerful interplay of dynamic factors: Drivers, Restraints, and Opportunities, which collectively determine its trajectory. The primary driver is the accelerating global shift towards sustainable energy solutions, supported by substantial governmental incentives and mandates promoting hydrogen as a crucial vector for decarbonizing transportation and heavy industry. Concurrently, the increasing standardization of high-pressure storage technologies, particularly 70 MPa systems for automotive applications, mandates the use of highly certified and reliable tank valves, solidifying market growth. However, this high-pressure environment also introduces significant restraints, chiefly the stringent material requirements needed to combat hydrogen embrittlement, leading to high manufacturing costs and complex certification processes which can slow market entry for new players.

Impact forces on the market are intense, driven primarily by safety regulations and technological maturity. Opportunities exist in developing cost-effective, standardized valve solutions that bridge the gap between niche aerospace applications and mass-market automotive demands. Specifically, the expansion of Liquid Hydrogen (LH2) infrastructure for long-haul shipping and aviation presents a specialized high-value opportunity for cryogenic valve technology innovation. The inherent complexity of managing hydrogen—its flammability, small molecular size, and high-pressure storage requirements—acts as a constant powerful restraint, necessitating robust and highly durable valve solutions that pass rigorous safety testing, thereby elevating the barriers to entry and reinforcing the position of established, certified market leaders. The overall impact force leans strongly towards accelerating growth, provided technological advancements continue to address cost and material compatibility restraints effectively.

The Hydrogen Tank Valve Market segmentation offers a nuanced understanding of product differentiation based on operational requirements, application demands, and pressure ratings. The market is broadly categorized by the physical type of valve (e.g., solenoid, ball, check, relief), the pressure levels they are designed to handle (35 MPa, 70 MPa, and higher), and the specific end-use application (automotive, industrial storage, refueling stations). This stratification is crucial because valves for a Fuel Cell Electric Vehicle (FCEV) require compact size, fast actuation, and extremely high pressure resistance, whereas valves for large-scale stationary storage prioritize flow capacity and long-term durability, necessitating different material and design approaches across segments. The fastest-growing segment is expected to be the 70 MPa pressure rating, driven by the immediate demand surge from the global FCEV rollout.

The value chain for the Hydrogen Tank Valve Market begins with the upstream sourcing of specialized materials, predominantly high-grade stainless steel (316L or specific alloys) and proprietary sealing materials suitable for hydrogen environments, requiring stringent quality control to mitigate the risk of hydrogen embrittlement. This highly specialized procurement phase dictates the eventual cost and performance of the final product. Upstream suppliers must comply with strict material certification standards required by valve manufacturers, who then engage in precision machining, sophisticated assembly processes in clean environments, and rigorous high-pressure testing protocols to ensure zero-leak tolerance and compliance with global safety standards like ISO and EC directives.

Midstream activities involve the design, prototyping, and large-scale manufacturing of the diverse valve types, including integrated valve components for specific tank systems (like Type IV assemblies). Distribution channels are critical, often categorized into direct sales and indirect channels. Direct sales are common for high-volume automotive OEMs and major industrial gas companies that require tailored solutions and integration support directly from the manufacturer or their authorized distributors. Indirect channels utilize specialized industrial fluid control suppliers and regional distributors who cater to smaller industrial end-users or maintenance, repair, and overhaul (MRO) markets. The downstream segment involves the integration of these valves into high-pressure hydrogen tanks and complete fuel system assemblies, primarily servicing FCEV manufacturers and developers of hydrogen refueling station infrastructure globally.

The primary consumers and end-users of hydrogen tank valves are highly concentrated within sectors committed to decarbonization and energy transition. The largest and fastest-growing segment of potential customers includes Original Equipment Manufacturers (OEMs) specializing in Fuel Cell Electric Vehicles (FCEVs), ranging from light-duty passenger vehicles to heavy-duty commercial transport (trucks and buses), demanding robust, compact, and highly reliable 70 MPa valve systems integrated directly into their Type IV storage assemblies. These customers require high-volume supply and consistent quality assurance to meet mass production schedules and global safety regulations.

A secondary, yet crucial, customer base is the Hydrogen Refueling Station (HRS) developers and operators. These entities require various high-flow, high-pressure valves for cascade storage systems, dispenser nozzles, and pressure regulation units used in the refueling process, necessitating industrial-grade durability and rapid cycling capability. Furthermore, major industrial gas suppliers and energy companies constructing large-scale hydrogen production and storage facilities (e.g., salt caverns or above-ground buffers) represent significant bulk buyers for larger bore, higher capacity stationary storage valves, completing the spectrum of essential buyers across the expanding hydrogen ecosystem.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 580 Million |

| Market Forecast in 2033 | USD 1,890 Million |

| Growth Rate | 18.5% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Swagelok, Parker Hannifin, Nikkiso, F.lli Cella, WEH GmbH, Rotarex, KITZ Corporation, Burkert Fluid Control Systems, Emerson Electric Co., HY-LOK Corporation, Zhejiang Huasheng Valve Co., Ltd., CIRCOR International, Flowserve Corporation, Conval, Air Products and Chemicals, Inc., Linde Engineering, GCE Group, TES Europe, Haskel International Inc., Hexagon Purus ASA. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological landscape of the Hydrogen Tank Valve Market is defined by the relentless pursuit of high-pressure capability, hydrogen compatibility, and long-term durability. A primary technological focus involves material science, specifically the development and utilization of specialized austenitic stainless steels (e.g., 316L modified, proprietary alloys) that demonstrate enhanced resistance to hydrogen embrittlement, a critical failure mechanism under cyclical high-pressure loading. Advanced sealing technologies, utilizing specialized polymer compounds like high-performance PEEK or PTFE derivatives, are continuously being engineered to ensure leak-tight performance over extended operational lifetimes, especially crucial for 70 MPa systems where the small molecular size of hydrogen poses a significant sealing challenge.

In terms of component design, the industry is increasingly adopting highly integrated valve packages, such as the Tank-Mounted Valve (TMV) assembly, which combines multiple safety functions (shut-off, pressure relief, temperature monitoring, and excess flow limitation) into a single, compact unit. This integration reduces system complexity, weight, and potential leak paths, meeting the stringent space and weight constraints of FCEVs. Furthermore, there is a rising trend in incorporating smart sensing technology and telemetry capabilities directly into the valve bodies. These smart valves enable real-time monitoring of internal temperature, pressure, and operational cycles, feeding data back into vehicle management systems or refueling station diagnostics, thereby enhancing proactive maintenance and overall system safety.

The regional dynamics of the Hydrogen Tank Valve Market are highly correlated with governmental commitment to hydrogen mobility and infrastructure rollout, leading to distinct growth patterns across key geographic areas. Asia Pacific (APAC) stands as the dominant market, primarily fueled by aggressive FCEV adoption mandates in countries like South Korea, which has established substantial targets for hydrogen vehicles and refueling stations, and Japan, a pioneer in hydrogen technology. China’s extensive industrial policy also drives significant demand for industrial-scale storage valves and supporting infrastructure. This region benefits from established supply chains and governmental readiness to subsidize the early stages of hydrogen ecosystem development, requiring massive volumes of certified valves for both transport and stationary applications.

Europe represents the second-largest and fastest-growing region, stimulated by the European Green Deal and national strategies focused on green hydrogen production and utilization, particularly in heavy-duty transport and industrial clusters along key hydrogen corridors. Countries like Germany, France, and the Netherlands are investing heavily in refueling networks and developing long-haul hydrogen truck fleets, driving demand for robust 70 MPa dispensing and tank valves. North America, led by the United States, is accelerating its hydrogen economy through legislative support like the Infrastructure Investment and Jobs Act, focusing on hydrogen hubs. This is creating significant localized demand, particularly for large-scale industrial valves and valves suitable for specialized applications like railway transport and maritime bunkering, marking a shift toward diversified applications beyond traditional automotive uses.

The primary technical challenge is mitigating hydrogen embrittlement. Since hydrogen atoms can diffuse into the metal structure under high pressure (up to 70 MPa), this degrades the material's mechanical properties, necessitating the use of specialized, highly durable stainless steel alloys and proprietary surface treatments to ensure long-term safety and integrity.

The 70 MPa (700 bar) pressure rating currently dominates market demand, particularly within the Fuel Cell Electric Vehicle (FCEV) segment. This ultra-high pressure enables maximum hydrogen storage density in Type IV composite tanks, maximizing vehicle range and meeting the performance expectations of both passenger cars and commercial heavy-duty trucks.

Safety regulations heavily influence manufacturing by mandating rigorous certification processes, adherence to international standards (e.g., ISO 19881, EC 79/2009), and exhaustive testing protocols, including fire resistance and cyclical pressure testing. This regulatory environment forces manufacturers to invest significantly in quality control and advanced material research, acting as a high barrier to entry.

The Fuel Cell Electric Vehicle (FCEV) segment, specifically commercial heavy-duty trucks and buses, is projected to show the fastest growth rate in valve demand. Global mandates for zero-emission commercial fleets and the technical suitability of hydrogen for heavy-duty long-haul transport are driving massive scale-up in required tank and valve production volumes.

A Tank-Mounted Valve (TMV) is an integrated assembly that consolidates multiple safety and flow control functions—such as manual shut-off, pressure relief, solenoid activation, and excess flow limitation—into a single unit mounted directly on the hydrogen storage tank. The TMV simplifies system integration, reduces weight, and minimizes potential leak points, crucial for compact automotive applications.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.