ID : MRU_ 433110 | Date : Dec, 2025 | Pages : 251 | Region : Global | Publisher : MRU

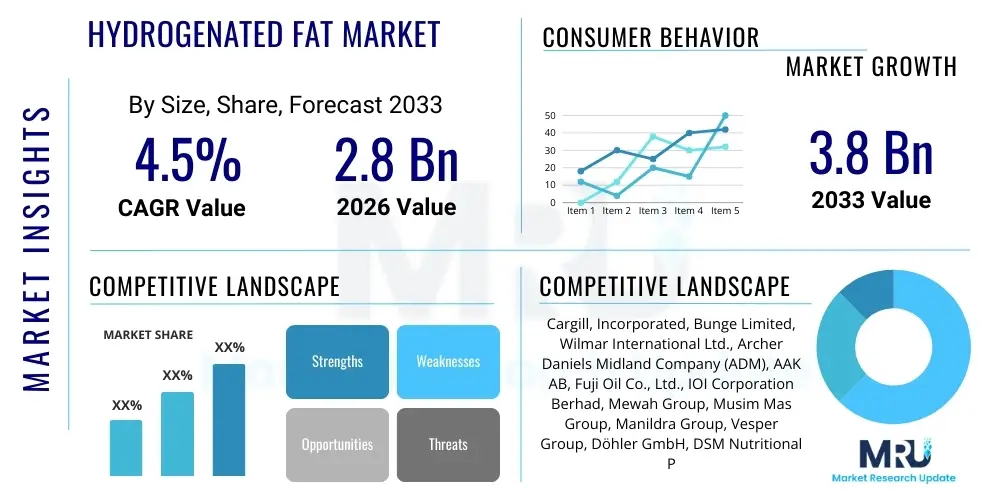

The Hydrogenated Fat Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 4.5% between 2026 and 2033. The market is estimated at USD 2.8 Billion in 2026 and is projected to reach USD 3.8 Billion by the end of the forecast period in 2033.

Hydrogenated fats, derived from vegetable or marine oils through the chemical process of hydrogenation, are crucial ingredients in the food industry, primarily valued for their enhanced oxidative stability, increased shelf life, and improved texture and mouthfeel. This process converts unsaturated fatty acids into saturated fatty acids, leading to a semi-solid or solid consistency at room temperature, which is highly desirable for baking, confectionery, and frying applications. Despite regulatory challenges aimed at limiting the consumption of Trans Fatty Acids (TFAs), the market continues to expand, driven by the demand for specific functional attributes that fully hydrogenated fats (which contain minimal TFAs) and zero-trans specialty fats provide in industrial food production, particularly in developing economies where cost efficiency and stability are paramount.

The product description encompasses various forms, including shortenings, margarines, and specific baking fats utilized across sectors such as bakery, snacks, processed foods, and dairy substitutes. Major applications involve their use as structuring agents in pastry doughs, emulsifiers in commercial baked goods, and as stable frying media. The inherent stability against rancidity allows food manufacturers to reduce waste and maintain product quality over extended periods, providing a significant benefit in supply chain management. The versatility of these fats allows for tailored formulations that meet diverse manufacturing requirements, from achieving flakey crusts to providing smooth, melt-in-the-mouth textures for chocolates and confectionery coatings.

Driving factors for the stable growth of this market include the increasing global population, urbanization, and the corresponding rise in demand for processed and convenience foods, particularly in the Asia Pacific and Latin American regions. Furthermore, technological advancements have focused on creating healthier, "zero-trans" hydrogenated products, often through combining full hydrogenation with interesterification processes, mitigating the historical health concerns associated with partially hydrogenated oils (PHOs). This innovation allows the industry to leverage the functional benefits of hydrogenation while adhering to stringent global health standards set by regulatory bodies like the FDA and WHO, thereby maintaining market relevance in essential food manufacturing segments.

The Hydrogenated Fat Market exhibits a complex dynamic characterized by stringent health regulations in developed nations and robust demand driven by convenience food expansion in emerging markets. Business trends reflect a strategic shift by key manufacturers towards advanced fat modification techniques, notably enzymatic interesterification and fractionation, to produce high-performance, trans-fat-free alternatives that mimic the functional properties of traditional hydrogenated products. This adaptation is crucial for sustaining market share, particularly as global food service chains and major packaged food companies commit to eliminating TFAs from their ingredient lists. Mergers and acquisitions focusing on specialized fat processing technologies are common, aimed at consolidating technical expertise and optimizing supply chains for palm and soybean oil derivatives, which form the primary raw material base.

Regionally, the market presents a dichotomy. North America and Europe are dominated by regulations, forcing high innovation rates and a rapid transition to low-TFA hydrogenated fats, leading to slower volume growth but higher value products. Conversely, the Asia Pacific region, led by China and India, represents the highest growth trajectory, primarily due to the vast and expanding middle-class population, the burgeoning quick-service restaurant (QSR) sector, and less uniformly enforced trans-fat restrictions in certain local markets, driving high consumption of packaged snacks and baked goods requiring stable fats. Latin America also shows steady growth, leveraging local oilseed production for domestic processing, catering largely to confectionery and prepared meal industries.

Segment trends underscore the enduring dominance of the bakery and confectionery segments, which rely heavily on the structural and textural properties provided by specialized solid fats. However, there is a distinct move within the segment towards 'functional fats' derived from full hydrogenation, often labeled as fully refined, bleached, deodorized, and hardened (RB DH) oils. The raw material segment is witnessing a surge in soybean oil and palm oil usage, capitalizing on their cost-effectiveness and availability, despite sustainability concerns associated with palm oil cultivation. The fastest-growing segment is anticipated to be specialized fats designed for dairy alternatives and vegan confectionery, aligning with global dietary shifts towards plant-based consumption, where these structured fats are essential for mimicking dairy creaminess and texture.

User inquiries regarding the impact of Artificial Intelligence (AI) on the Hydrogenated Fat Market center around three core themes: optimizing raw material sourcing amidst volatile commodity prices, enhancing the efficiency and safety of the hydrogenation process itself, and accelerating the R&D cycle for trans-fat alternatives. Users are particularly concerned with how AI can predict supply chain disruptions affecting palm or soybean oil availability, optimize complex blending ratios for specialized zero-trans fats to ensure consistency across batches, and use predictive modeling to screen potential catalysts or process parameters that yield fats with desired melting profiles and textural characteristics without generating unwanted TFAs. The central expectation is that AI will primarily serve as a tool for cost reduction, quality control enhancement, and rapid innovation in regulatory compliance, allowing manufacturers to maintain high functional quality while meeting strict health standards.

The Hydrogenated Fat Market is subject to powerful and often contradictory forces that dictate its trajectory. Drivers primarily stem from the functional superiority and cost-effectiveness of these fats in industrial applications. The inherent ability of hydrogenated fats to provide structure, increase plasticity, and extend the shelf life of highly processed foods makes them indispensable for mass food producers, especially in the bakery and convenience food sectors. Furthermore, the global shift towards fully hydrogenated oils (FH Os), which are generally free of TFAs, allows the industry to continue capitalizing on the technical advantages of hydrogenation while addressing widespread public health concerns, driving innovation toward zero-trans solutions.

Restraints are overwhelmingly rooted in regulatory mandates and growing consumer health consciousness. Global and regional bans or severe restrictions on Partially Hydrogenated Oils (PHOs), led by regulatory bodies such as the U.S. FDA and the European Union, pose significant hurdles, forcing expensive and complex reformulations across the industry. Furthermore, negative perception and consumer backlash, fueled by awareness of the links between trans-fats and cardiovascular disease, pressure food manufacturers to adopt clean label strategies and replace hydrogenated fats entirely, even when the products are technically compliant (fully hydrogenated). The increasing cost of raw materials and the volatile nature of global vegetable oil markets also impose significant financial restraints on manufacturers.

Opportunities lie in the expansion of the market in emerging economies where processed food consumption is rising rapidly, and where regulatory oversight is less immediate than in mature Western markets. Moreover, the niche market for functional, non-dairy, and plant-based fats presents a substantial growth opportunity, as fully hydrogenated and interesterified fats are critical components in formulating vegan butter alternatives, cheese substitutes, and non-dairy ice creams, capitalizing on growing flexitarian and vegan dietary trends. The dominant impact force shaping the market is the regulatory pressure to achieve 'zero trans fat' status, which necessitates continuous investment in catalytic, enzymatic, and blending technologies, ultimately driving market participants towards higher value, technologically advanced fat modification processes over simple, traditional hydrogenation.

The Hydrogenated Fat Market is segmented based on product type, raw material source, application, and geography, each providing unique insights into consumption patterns and manufacturing preferences. Product segmentation differentiates between fully hydrogenated oils (FHOs) and specialty fats, which now dominate the value chain due to their compliance with global trans-fat regulations, and the rapidly diminishing volume of partially hydrogenated oils (PHOs). FHOs are essential for creating the structure needed in shortenings and solid margarines.

Raw material segmentation highlights the dependence on major global oilseed crops. Palm oil and soybean oil derivatives hold the largest market shares due to their economic advantages, widespread availability, and versatility in achieving various melting points after hydrogenation. Other raw materials like rapeseed (canola) and sunflower oil, while generally perceived as healthier, constitute smaller segments but are growing steadily in high-value, niche applications where non-GMO and specific fatty acid profiles are requested.

Application analysis confirms the fundamental importance of these structured fats in the bakery and confectionery industries, which require plasticity and controlled crystallization for products like biscuits, cakes, laminated doughs, and chocolate coatings. The growth in the snacks and processed foods segment, particularly in ready-to-eat meals, further contributes to sustained demand, requiring stable, high-smoke-point frying oils and structure-providing fats. The diversification into functional foods and dairy substitutes represents the most dynamic segment in terms of innovation and growth potential.

The value chain for hydrogenated fats begins with the upstream activities of raw material procurement, dominated by large-scale farming and crushing of oilseeds (soybeans, palm fruit, rapeseed). This stage involves substantial commodity market volatility and sustainability scrutiny, particularly concerning deforestation related to palm oil. Major oil processors acquire crude vegetable oil, which undergoes extensive refining, bleaching, and deodorization (RBD) before the hydrogenation process itself. Efficiency at this initial stage, including logistics and hedging against price fluctuations, is crucial for determining the final cost structure of the hydrogenated product.

Midstream activities involve the specialized chemical and enzymatic processes. Crude oil is transported to dedicated fat modification facilities where hydrogenation, fractionation, and interesterification occur. These processes require advanced catalytic technology and energy management. Manufacturers differentiate themselves here by their capability to produce zero-trans, custom-specification fats tailored for specific industrial applications (e.g., highly stable deep-frying oils or low-melting point confectionery fats). Quality control and adherence to international food safety and trans-fat limitations are paramount at this production stage, often requiring expensive certification and continuous process monitoring.

The downstream segment encompasses distribution channels, marketing, and final end-user consumption. Products are distributed both directly and indirectly. Direct distribution involves sales of bulk fats (in tankers or large drums) to major industrial users like global food manufacturers (e.g., multinational bakery or snack companies). Indirect distribution utilizes specialized food ingredient distributors and traders who supply smaller bakeries, caterers, and regional food producers. The final consumers are the general public consuming the products containing these fats, though the immediate buyer is typically the food manufacturing corporation. The strong linkage between product specification and end-use functionality means that technical support and application expertise are critical components of the downstream value proposition.

Potential customers for specialized hydrogenated fats span the entire processed food industry, prioritizing entities that require structured, stable, and cost-effective fat components to achieve desirable product texture and extended shelf life. The largest consumer base resides within the commercial bakery sector, including large industrial bakeries that produce packaged breads, biscuits, cakes, and crackers. These entities rely on shortenings and margarines to provide plasticity in dough, ensure proper lamination, and control fat crystallization for optimal texture, especially in high-volume, automated production environments.

The confectionery industry represents another major end-user segment. Manufacturers of chocolate, candies, fillings, and glazes utilize hydrogenated fats as cocoa butter equivalents (CBEs) or replacers (CBRs). These fats are crucial for managing the melting curve of confectionery items, preventing fat bloom, and providing a clean, sharp melt-in-the-mouth sensation without the cost variability associated with pure cocoa butter. The shift toward specialized, low-tallow fats for achieving specific melting profiles has made this segment highly dependent on sophisticated fat modification expertise.

Beyond traditional baking and confectionery, the processed food sector, encompassing instant noodles, frozen doughs, ready-to-eat meals, and specifically, the rapidly growing non-dairy and vegan product manufacturers, are critical emerging customers. Vegan food producers require highly functional, structured vegetable fats to replicate the mouthfeel and stability traditionally provided by dairy butter or animal fats. Quick Service Restaurants (QSRs) and institutional food service providers also form a substantial customer base, consuming large volumes of high-stability, zero-trans frying oils designed to withstand repeated heating cycles without degradation or smoking, ensuring quality and maximizing oil usage efficiency.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 2.8 Billion |

| Market Forecast in 2033 | USD 3.8 Billion |

| Growth Rate | 4.5% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Cargill, Incorporated, Bunge Limited, Wilmar International Ltd., Archer Daniels Midland Company (ADM), AAK AB, Fuji Oil Co., Ltd., IOI Corporation Berhad, Mewah Group, Musim Mas Group, Manildra Group, Vesper Group, Döhler GmbH, DSM Nutritional Products, Upfield Holdings B.V., Louis Dreyfus Company B.V., Ruchi Soya Industries Limited, Premium Vegetable Oils Sdn Bhd, Goodman Fielder, Olam International, ADM Pura. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological landscape of the hydrogenated fat market is characterized by a strategic move away from traditional partial hydrogenation towards processes that achieve desired solidity and stability without generating significant levels of Trans Fatty Acids (TFAs). The cornerstone technology remains full hydrogenation, utilizing high-pressure reactors and highly efficient nickel catalysts to saturate all double bonds, resulting in highly stable fats suitable for blending. Continuous advancements focus on catalyst optimization, aiming for highly selective hydrogenation processes that improve reaction speed and reduce energy consumption while simultaneously minimizing the formation of unwanted byproducts, thereby improving the purity and consistency of the fully saturated fat base.

However, the most critical shift is the integration of hydrogenation with complementary fat modification techniques, notably interesterification. Enzymatic interesterification (EIE) is rapidly becoming the gold standard. This technology uses lipases (enzymes) to rearrange the fatty acids within the triglyceride structure of a mixture of liquid oil and fully hydrogenated oil. This results in a structured fat with a customizable melting profile, mimicking the textural functionality of PHOs but with zero or near-zero trans fat content. EIE offers superior control over the solid fat content (SFC) curve, which is essential for specialized applications like non-tempering confectionery fats or high-performance margarines that require precise melting characteristics.

Other vital technologies include advanced fractionation, which separates fatty acids based on their melting points through controlled cooling and crystallization, and various blending methodologies. Sophisticated blending software and analytical tools, including Nuclear Magnetic Resonance (NMR) spectroscopy and Differential Scanning Calorimetry (DSC), are now essential for manufacturers to precisely control the physical properties of their fat blends. Furthermore, the adoption of continuous processing systems over traditional batch reactors is enhancing throughput, ensuring higher product uniformity, and reducing contamination risks, positioning technology and process engineering as primary competitive differentiators in a heavily regulated market environment.

The global market for hydrogenated fats displays distinct regional characteristics largely determined by regulatory environments and economic development phases. Asia Pacific (APAC) stands out as the primary growth engine, fueled by rapid urbanization, increasing consumer reliance on packaged foods, and the robust expansion of the domestic bakery and snack industries in economies like India, China, and Southeast Asia. While regulatory scrutiny regarding TFAs is increasing across APAC, compliance standards are often implemented at a slower pace compared to the West, allowing for sustained, high-volume demand for cost-effective functional fats. Manufacturers in this region are investing heavily in localized processing capabilities to serve this massive consumer base.

North America and Europe represent mature, highly regulated markets where the emphasis is overwhelmingly on technological innovation and adherence to zero-trans fat mandates. Following the FDA’s ruling to revoke the Generally Recognized as Safe (GRAS) status of PHOs in the U.S. and similar stringent European regulations, the market is completely reliant on fully hydrogenated and interesterified fat solutions. Consequently, these regions lead in value-added products, focusing on specialty and clean-label shortenings and margarines that use sophisticated oil blends derived from non-GMO sources like canola and sunflower oil, ensuring minimal TFA presence while maintaining optimal functional performance in commercial baking.

Latin America (LATAM) and the Middle East & Africa (MEA) offer moderate to high growth opportunities. LATAM benefits from large domestic oilseed production (especially soybean) in countries like Brazil and Argentina, supplying the raw materials for both domestic and international markets. The food processing sector in LATAM is expanding, driving demand for stable fats in local convenience foods. In MEA, rapid population growth and shifting dietary habits toward Western-style processed foods and confectionery are creating new consumption pockets. While the regulatory landscape is varied across MEA, the trend towards adopting international health standards is slow but perceptible, offering manufacturers a window of opportunity for market penetration with functional, stable, and cost-efficient hydrogenated fat products, especially those derived from palm oil.

Partially Hydrogenated Oils (PHOs) contain Trans Fatty Acids (TFAs) and are largely banned globally due to health risks. Fully Hydrogenated Oils (FHOs) contain minimal TFAs and are highly saturated and stable. FHOs are commonly used today, often blended with liquid oils or modified via interesterification to create zero-trans specialty fats that meet industry needs.

Regulations have severely curtailed the demand for PHOs, forcing manufacturers to invest heavily in alternative fat modification technologies like enzymatic interesterification. While volume demand for traditional PHOs has plummeted, demand for functionally equivalent, zero-trans FHOs and derived specialty fats remains robust, shifting the market toward higher-value, technology-driven products.

Palm oil and soybean oil are the primary raw materials dominating the market due to their abundant supply, relatively low cost, and versatility in achieving various solid fat content profiles necessary for industrial applications, although they face increasing scrutiny regarding sustainability and source origin.

In emerging economies, the primary drivers are the massive expansion of the bakery, confectionery, and packaged snack sectors. These industries rely on the stability and structural properties of hydrogenated fats to ensure product consistency, extended shelf life, and cost efficiency in mass production environments.

Enzymatic interesterification (EIE) is a crucial technology used to create high-performance, structured fats that are functionally similar to traditional PHOs but are trans-fat-free. EIE allows manufacturers to control the crystalline structure and melting point of fat blends, making it essential for producing modern shortenings and margarines compliant with global health standards.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.