ID : MRU_ 436045 | Date : Dec, 2025 | Pages : 245 | Region : Global | Publisher : MRU

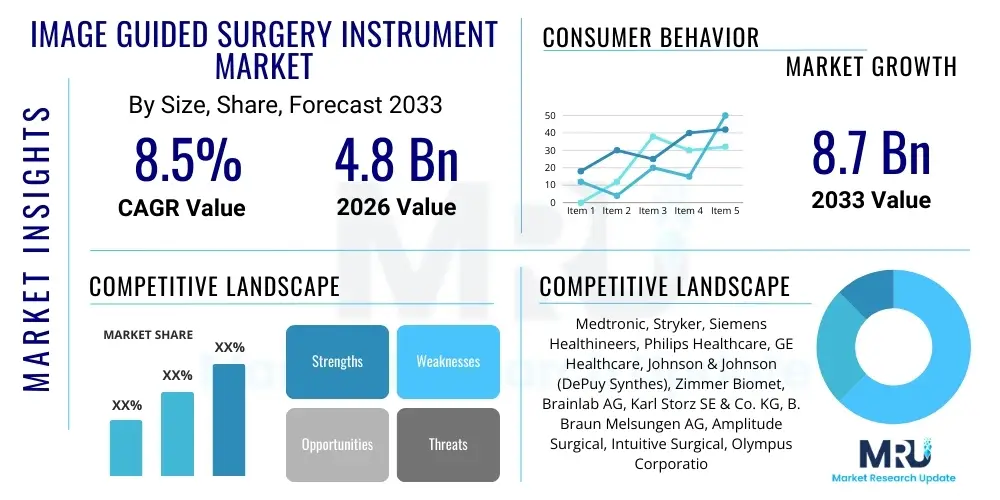

The Image Guided Surgery Instrument Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 8.5% between 2026 and 2033. The market is estimated at USD 4.8 Billion in 2026 and is projected to reach USD 8.7 Billion by the end of the forecast period in 2033.

The Image Guided Surgery (IGS) Instrument Market encompasses a range of sophisticated technologies and tools designed to enhance the precision, safety, and efficacy of surgical procedures by providing real-time visualization and navigation capabilities. These instruments leverage advanced imaging modalities, such as Computed Tomography (CT), Magnetic Resonance Imaging (MRI), Fluoroscopy, and Ultrasound, integrated with surgical planning software and tracking devices. The primary objective of IGS is to guide the surgeon accurately to the target anatomy, minimize invasiveness, and reduce collateral damage to surrounding healthy tissue. Key product categories include surgical navigation systems, surgical robots equipped with guidance features, specialized instruments like probes and trackers, and integrated software platforms used across various surgical specialties including neurosurgery, orthopedics, cardiac surgery, and oncology.

The growing adoption of minimally invasive surgery (MIS) techniques is a foundational driver for this market, as IGS instruments provide the necessary visual feedback and positional awareness often lost in small incisions. These systems significantly improve intraoperative decision-making, allowing surgeons to confirm the extent of resection or the precise placement of implants with high confidence. Furthermore, the integration of 3D modeling and augmented reality (AR) is transforming surgical planning, leading to better patient outcomes, shorter hospital stays, and quicker recovery times. The continual development of smaller, more ergonomic, and highly accurate tracking systems is expanding the utility of IGS instruments into complex procedures previously requiring extensive open surgery.

Major applications of IGS instruments span critical medical fields. In neurosurgery, IGS is indispensable for tumor resection and deep brain stimulation, offering unparalleled access to delicate structures. In orthopedics, navigation systems ensure precise alignment during joint replacement surgeries (knee, hip). The benefits derived from these technologies include reduced radiation exposure for both patient and staff (compared to conventional fluoroscopy), enhanced surgical precision leading to fewer complications, and increased procedural efficiency. Driving factors include the rising global incidence of chronic diseases requiring surgical intervention, the increasing demand for advanced healthcare infrastructure, and significant investments in research and development aimed at creating multimodal imaging integration.

The Image Guided Surgery Instrument Market is experiencing robust growth driven by the escalating demand for high-precision surgical solutions and the rapid integration of robotic assistance. Key business trends involve strategic collaborations between technology providers and major hospitals to develop comprehensive surgical suites, alongside intensive focus on cybersecurity within integrated medical networks. Regionally, North America continues to dominate due to high healthcare expenditure and early adoption of innovative technologies, while the Asia Pacific region is demonstrating the highest growth trajectory, spurred by improving healthcare access, increasing medical tourism, and government initiatives promoting advanced surgical care. The introduction of hybrid operating rooms is becoming a significant business strategy, allowing hospitals to integrate advanced imaging (CT/MRI) directly into the surgical workflow, maximizing the utility of IGS instruments.

Segment trends indicate that the Surgical Navigation Systems segment holds the largest market share, owing to its foundational role across multiple surgical disciplines, particularly in cranial and spinal procedures. However, the specialized Instruments and Accessories segment, which includes sterile disposable trackers, probes, and specialized software, is projected to register the fastest growth, fueled by the recurring need for consumables with every procedure and the continuous innovation in sensor technology. Furthermore, end-user trends show that hospitals, particularly large university and teaching hospitals, remain the principal consumers due to the high initial investment required for IGS systems, though specialized ambulatory surgical centers (ASCs) are increasingly adopting lower-cost or portable navigation units for routine orthopedic and ENT procedures, diversifying the customer base and focusing on outpatient efficiency.

Overall, the market is characterized by intense technological competition, with companies focusing on developing software solutions that offer greater interoperability between different imaging modalities and robotic platforms. The integration of artificial intelligence (AI) for image processing, segmentation, and predictive modeling represents a crucial future growth segment. Despite high initial capital costs acting as a restraint, the long-term cost-effectiveness resulting from fewer re-operations and improved patient outcomes reinforces the positive market outlook. Strategic positioning involves expanding geographically into emerging markets and focusing R&D efforts on miniaturization and enhanced real-time feedback mechanisms, thereby solidifying the market's strong position within the broader medical device landscape.

User inquiries regarding the impact of AI on the Image Guided Surgery Instrument Market frequently center on themes such as enhanced diagnostic accuracy, the role of machine learning in real-time intraoperative guidance, and the potential for AI to automate certain planning phases. Common concerns include data security, regulatory hurdles for AI-driven surgical devices, and the necessary training required for surgeons to effectively utilize these advanced systems. Users are keenly interested in how AI can move IGS from passive guidance to active, predictive surgical assistance, particularly in complex areas like tumor margin assessment and vascular mapping. Expectations are high regarding AI's ability to personalize surgical approaches based on vast patient data sets and improve robotic precision by compensating for minor tremor or movement.

AI's integration fundamentally elevates the capabilities of IGS instruments. Machine learning algorithms are already being deployed to rapidly analyze preoperative imaging data, enabling automated segmentation of critical structures and pathology, which drastically reduces the manual planning time required by surgeons. During the surgery itself, AI-powered image analysis can fuse multimodal data (e.g., combining MRI with intraoperative ultrasound) to provide a more comprehensive, dynamic view of the surgical field than conventional systems. This fusion capability, often augmented with predictive modeling, allows the IGS system to anticipate potential risks, such as proximity to critical nerves or blood vessels, and issue warnings or adjust robotic pathways automatically.

Looking forward, AI promises to democratize complex IGS procedures by standardizing best practices derived from large-scale surgical data. Advanced algorithms can assess the technical skills of the surgeon in real-time, providing feedback and training tools. Furthermore, AI contributes significantly to quality assurance by post-operatively analyzing procedure footage and outcome data, linking surgical steps to patient recovery. This continuous feedback loop drives iterative improvement in IGS system design and operational protocols, ultimately enhancing the overall safety and effectiveness of image-guided interventions. The emphasis is shifting from merely guiding the instrument to intelligently assisting the surgical decision-making process.

The Image Guided Surgery Instrument Market is shaped by a powerful synergy of growth enablers, significant constraints, and emerging opportunities, collectively defining the market's trajectory. Key drivers include the global shift towards minimally invasive surgery due to its associated benefits, such as reduced patient trauma and quicker recovery, which fundamentally rely on IGS technology for visualization. The increasing prevalence of age-related conditions and chronic diseases (e.g., neurological disorders, orthopedic issues, cancer) requiring complex surgical interventions further fuels demand. However, the high initial capital investment required for these advanced systems, coupled with complex maintenance protocols and the necessity for specialized training, acts as a major restraint, particularly in developing economies or smaller healthcare facilities. Furthermore, stringent regulatory approval processes for new image-guided technologies slow down product commercialization.

Opportunities for market expansion are significant, primarily driven by technological convergence and geographical penetration. The integration of advanced visualization technologies, such as augmented reality (AR) and virtual reality (VR), with conventional IGS systems opens new avenues for surgical simulation and training, as well as enhanced intraoperative spatial awareness. Moreover, the vast, untapped market potential in Asia Pacific and Latin America, where healthcare spending is rapidly increasing and infrastructure is modernizing, presents lucrative expansion opportunities for major market players. Developing lower-cost, portable, or mobile IGS solutions that cater specifically to these emerging markets is a critical strategic opportunity. The increasing trend of consolidating patient data and integrating electronic health records (EHRs) with surgical platforms also paves the way for sophisticated data-driven surgical improvements.

The collective impact forces underscore the market’s dynamism. The increasing pressure on healthcare providers to improve patient outcomes while simultaneously controlling costs favors IGS instruments, as they reduce complications and re-operation rates, thereby proving cost-effective in the long term. Technological advances exert a continuous, high impact, forcing rapid product lifecycle evolution and requiring perpetual investment in R&D to maintain competitiveness. Regulatory bodies are grappling with the integration of AI and data privacy concerns (GDPR, HIPAA), which constitute a moderate but persistent restraining force. The overall net impact is substantially positive, propelled primarily by the undeniable clinical benefits and the relentless pursuit of surgical precision globally, ensuring sustained high growth throughout the forecast period.

The Image Guided Surgery Instrument Market is highly diversified, segmented based on product type, application, and end-user, reflecting the specific needs and technological maturity across various surgical environments. Analyzing these segments provides a granular view of growth pockets and investment priorities within the market. Product type segmentation, for instance, highlights the differential growth rates between complex capital equipment (like navigation systems) and the higher-volume consumables (like specialized instruments and software). Application segmentation reveals the dominant surgical fields utilizing IGS, with neurosurgery and orthopedics traditionally leading, but with cardiovascular and ENT showing rapid adoption rates. Understanding these divisions is crucial for manufacturers to tailor their product offerings and marketing strategies to specific clinical workflows and budgeting cycles across different healthcare settings.

The dominance of certain segments is often correlated with the complexity and criticality of the procedures performed. Neurosurgery, requiring sub-millimeter precision for interventions on the brain and spine, has been the foundational application for IGS, necessitating advanced electromagnetic and optical tracking systems. Orthopedic procedures, particularly complex trauma and joint replacement, also heavily rely on IGS to ensure correct alignment and implant sizing, driving the demand for specialized instruments. Furthermore, the End-User segment provides insight into purchasing power and volume, with large hospitals procuring multi-system contracts, while smaller clinics focus on dedicated, single-application devices. This comprehensive segmentation framework assists stakeholders in identifying areas for strategic mergers, acquisitions, and targeted product launches aimed at maximizing return on investment.

The value chain for the Image Guided Surgery Instrument Market is sophisticated and highly integrated, starting from advanced component manufacturing and culminating in highly specialized hospital usage and maintenance services. The upstream segment is dominated by specialized technology providers focusing on high-precision components such as electromagnetic sensors, optical tracking cameras, advanced microprocessors, and sophisticated medical-grade displays. These component providers require deep expertise in materials science, signal processing, and medical device compliance. Integration and system assembly, which form the core manufacturing process, require rigorous quality control and sterile production environments, often concentrated among major medical device manufacturers who hold crucial intellectual property related to proprietary software algorithms and navigation platforms.

The distribution channel is predominantly indirect, utilizing a network of highly skilled distributors and sales representatives who possess clinical expertise and technical knowledge necessary to sell, install, and service complex IGS systems. Due to the high cost and complexity of the equipment, sales cycles are lengthy, involving extensive clinical validation and budgetary approval within hospital systems. Direct sales are often reserved for key accounts or large teaching hospitals where manufacturers provide full integration services and comprehensive training programs. Post-sale services, including software updates, calibration, and routine maintenance, represent a significant and recurring revenue stream, solidifying the relationship between manufacturers and end-users, and ensuring the systems remain operational and compliant with the latest regulatory standards.

Downstream analysis centers on the implementation and utilization of these instruments by hospitals and surgical centers. The relationship here is not just transactional but consultative, involving ongoing collaboration between manufacturers, surgeons, and biomedical engineering teams to optimize system performance and integrate IGS solutions seamlessly into the operating room workflow. The ultimate value delivery is measured by improved surgical outcomes, efficiency gains (reduced procedure time), and enhanced patient safety. The efficacy of the distribution channel is highly dependent on its ability to provide localized technical support and rapid response maintenance, minimizing downtime for high-value surgical systems.

Potential customers for Image Guided Surgery Instruments are primarily institutions that perform high-volume, complex, and precision-dependent surgical procedures. The largest and most influential customer segment is comprehensive hospitals and large university medical centers. These institutions possess the substantial capital budgets required for initial system acquisition, the high volume of surgical cases across various specialties (neurosurgery, orthopedics, cardiac), and the necessary infrastructure (hybrid operating rooms, specialized staff) to effectively utilize advanced IGS technology. They often act as early adopters of the newest robotic and AI-integrated navigation systems, influencing the market adoption cycle through clinical publications and training programs.

The second key customer segment includes ambulatory surgical centers (ASCs) and specialized orthopedic or spine clinics. While ASCs may lack the vast capital resources of major hospitals, they prioritize efficiency and rapid patient turnover, making mobile or more focused IGS units attractive, particularly for elective orthopedic procedures. These centers often seek systems that minimize procedure time and are easy to integrate into existing limited space. Their purchasing decisions are highly influenced by the proven cost-effectiveness and workflow optimization features of the instruments. The growing trend towards performing traditionally inpatient procedures in outpatient settings is significantly increasing the market attractiveness of ASCs as buyers.

Furthermore, government and military hospitals, along with specialized research institutes, represent significant niche markets. These entities require highly rugged, reliable systems for specific trauma or research applications. The increasing global investment in medical education and surgical training centers also positions them as potential customers, as they integrate IGS simulation and planning systems into their curricula to train the next generation of surgeons. Ultimately, the purchasing criteria across all segments revolve around clinical accuracy, system reliability, ease of integration, and the total cost of ownership (TCO) including consumables and service contracts.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 4.8 Billion |

| Market Forecast in 2033 | USD 8.7 Billion |

| Growth Rate | CAGR 8.5% |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Medtronic, Stryker, Siemens Healthineers, Philips Healthcare, GE Healthcare, Johnson & Johnson (DePuy Synthes), Zimmer Biomet, Brainlab AG, Karl Storz SE & Co. KG, B. Braun Melsungen AG, Amplitude Surgical, Intuitive Surgical, Olympus Corporation, Accuray Incorporated, navigated interventional technologies GmbH, Scopis GmbH, XION GmbH, MicroPort Scientific Corporation, Curetis N.V., Conformis Inc. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological landscape of the Image Guided Surgery Instrument Market is defined by the integration and refinement of highly sensitive tracking and visualization modalities. The foundational technologies include Optical Navigation Systems, which use high-speed infrared cameras to track passive or active markers attached to instruments and patient anatomy, offering high accuracy but requiring a clear line of sight. Contrastingly, Electromagnetic Navigation Systems use low-frequency magnetic fields to track instruments, offering flexibility by not requiring a direct line of sight, making them popular in fields like ENT and spinal surgery, though they are susceptible to interference from metal objects in the operating room. Hybrid systems, combining both optical and electromagnetic tracking, are emerging as a superior solution, leveraging the benefits of both technologies to maximize precision and versatility in complex, crowded operating environments.

Furthermore, advanced visualization is critical, moving beyond simple 2D display to immersive 3D and holographic views. Augmented Reality (AR) technology is gaining prominence, projecting critical anatomical or pre-planned surgical data directly onto the patient or into the surgeon's field of view via specialized glasses or head-mounted displays. This capability allows surgeons to overlay invisible structures, such as tumor margins or critical nerve pathways, onto the real-time surgical image, significantly improving spatial understanding and reducing cognitive load. Software innovation is equally important, particularly in image registration algorithms that accurately match preoperative imaging (CT/MRI) with the patient's actual intraoperative position, compensating for tissue shift and patient movement.

The future technology trajectory focuses heavily on seamless integration with robotic platforms and intraoperative imaging devices (like portable CT scanners and high-resolution ultrasound). Robotic-assisted IGS instruments leverage the guidance system's data to autonomously execute precise movements, enhancing dexterity beyond human capability. Moreover, sensor fusion technology, integrating force sensing, haptic feedback, and advanced machine vision, is creating safer and more intuitive surgical environments. The emphasis across all technological developments is miniaturization, wireless connectivity, and the development of intelligent, disposable instruments that offer high fidelity tracking while streamlining operating room setup and breakdown procedures.

Regional dynamics play a crucial role in shaping the Image Guided Surgery Instrument Market, reflecting variations in healthcare spending, regulatory environments, and technological adoption rates.

The primary function of IGS instruments is to provide surgeons with high-precision, real-time visualization and spatial orientation during procedures, leveraging technologies like optical and electromagnetic tracking to minimize invasiveness and enhance accuracy.

Neurosurgery and orthopedic surgery (especially joint replacement and spinal fusion) are the largest drivers, as these fields require sub-millimeter precision achievable only through advanced image guidance systems and specialized instruments.

AI is significantly impacting IGS by enabling automated preoperative image segmentation, improving intraoperative data fusion, providing real-time risk assessment, and optimizing robotic movement for enhanced surgical safety and efficiency.

Optical systems offer superior accuracy but require a clear line of sight, while electromagnetic systems function without line of sight but can be affected by metal interference, making the choice dependent on the specific surgical environment and procedure.

The Image Guided Surgery Instrument Market is projected to exhibit a Compound Annual Growth Rate (CAGR) of 8.5% between 2026 and 2033, driven by technological advancements and increasing global demand for minimally invasive procedures.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.