ID : MRU_ 432490 | Date : Dec, 2025 | Pages : 243 | Region : Global | Publisher : MRU

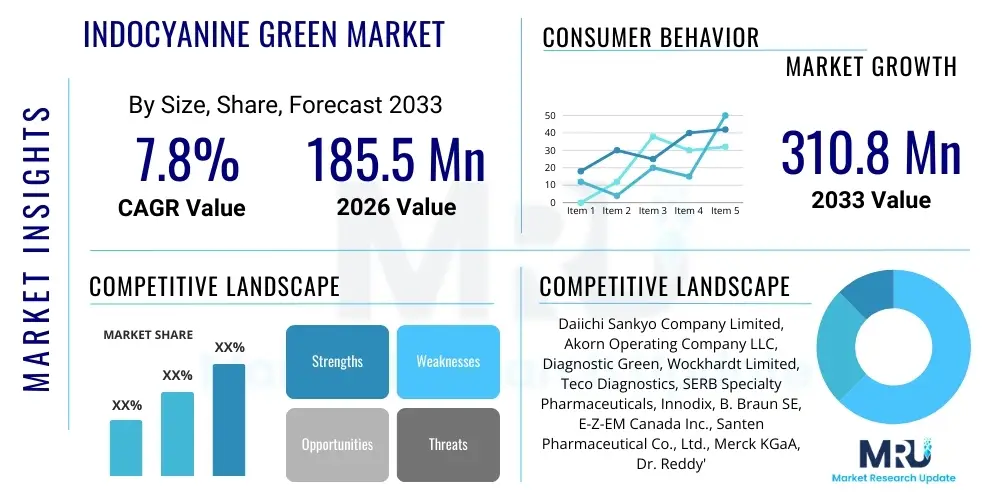

The Indocyanine Green Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 7.75% between 2026 and 2033. The market is estimated at $185.5 Million USD in 2026 and is projected to reach $310.8 Million USD by the end of the forecast period in 2033.

The Indocyanine Green (ICG) Market centers around the use of a safe, non-toxic cyanine dye widely utilized as a diagnostic aid in medical imaging, particularly in ophthalmology, cardiovascular medicine, and fluorescence-guided surgery. ICG is characterized by its absorption and emission spectra in the near-infrared (NIR) region, making it an ideal contrast agent for visualizing vascular structures, tissue perfusion, and lymphatic drainage. Its rapid uptake by the liver and biliary excretion pathway allows for effective assessment of liver function and portal circulation. The primary product is a lyophilized powder formulated for intravenous administration, offering distinct advantages over traditional contrast agents due to its minimal adverse effects and compatibility with specialized NIR imaging systems.

Major applications driving the demand for ICG include angiography in ophthalmic diseases such as age-related macular degeneration, real-time perfusion assessment during cardiac and reconstructive surgeries, and highly sensitive sentinel lymph node mapping in oncology, notably breast and thyroid cancers. Furthermore, ICG has gained significant traction in neurosurgery for aneurysm clipping and arteriovenous malformation (AVM) resection, providing crucial intraoperative visualization of blood flow dynamics. The versatility of ICG, coupled with the miniaturization and improved accessibility of specialized NIR imaging platforms, is expanding its integration across various surgical disciplines, elevating procedural accuracy and patient safety.

The core benefits of ICG usage encompass enhanced diagnostic precision, real-time visualization capabilities, and a favorable safety profile compared to alternatives. Key driving factors stimulating market growth include the rising prevalence of chronic diseases requiring advanced diagnostic imaging, the increasing adoption of minimally invasive surgical techniques (where real-time feedback is critical), and substantial technological advancements in fluorescence imaging devices. Government and private sector investments in improving surgical infrastructure, particularly in developing economies, further contribute to the market’s positive trajectory, positioning ICG as an indispensable tool in modern medical practice.

The Indocyanine Green (ICG) market is experiencing robust expansion driven primarily by the escalating demand for fluorescence-guided surgery (FGS) techniques across oncology and general surgery, alongside continuous application growth in ophthalmic diagnostics. Business trends indicate a strong move toward developing pre-filled syringes and highly stable formulations of ICG to improve workflow efficiency and shelf life in clinical settings. Furthermore, strategic partnerships between ICG manufacturers and imaging system developers (e.g., NIR camera manufacturers) are crucial for establishing integrated diagnostic and therapeutic platforms, ensuring optimized compatibility and expanding the clinical utility of the dye. Regulatory approvals for novel off-label uses of ICG, such as in gastrointestinal surgery for anastomotic leak detection, are also opening up new commercial pathways.

Regionally, North America maintains market dominance due to high healthcare expenditure, established adoption of advanced surgical technologies, and favorable reimbursement policies for NIR imaging procedures. However, the Asia Pacific (APAC) region is projected to exhibit the highest growth rate, fueled by improving healthcare infrastructure, a large patient population requiring complex surgeries, and increasing awareness regarding the benefits of ICG-assisted diagnostics, particularly in large economies like China and India. European countries are steadily adopting ICG, driven by standardized clinical guidelines promoting minimally invasive techniques and strong academic research validating its diverse applications in hepatic and cardiovascular assessments.

Segment trends highlight the surgical application segment, especially oncology (sentinel lymph node mapping and tumor visualization), as the primary revenue generator. The end-user segment is dominated by hospitals, owing to the concentration of complex surgical procedures and availability of necessary capital equipment (fluorescence imaging towers). There is a notable rising trend in the application of ICG in liver surgery and function testing, driven by the increasing incidence of hepatocellular carcinoma and the need for precise assessment of remnant liver capacity before major resections. Innovation in specialized formulations designed for specific anatomical targeting is also a key segmentation focus, promising higher efficacy and precision in future diagnostic procedures.

Users frequently inquire about how Artificial Intelligence (AI) can enhance the utility and precision of Indocyanine Green (ICG) imaging, specifically focusing on automated image processing, real-time clinical decision support, and standardized quantification of fluorescence data. Key concerns revolve around the reliability of AI algorithms in interpreting complex perfusion patterns during surgery and the integration challenges of AI software with proprietary NIR camera systems. Expectations center on AI’s ability to move ICG usage beyond qualitative visual assessment to quantitative, objective analysis, particularly in areas like tumor margin delineation, accurate assessment of tissue viability (perfusion status), and prediction of surgical outcomes, ultimately aiming to reduce subjectivity and increase procedural success rates in fluorescence-guided surgeries.

The integration of AI algorithms into NIR imaging systems promises to transform the ICG market by automating the complex analysis of fluorescence decay kinetics and intensity variations. AI models can be trained on vast datasets of ICG angiography videos to identify subtle deviations from normal perfusion patterns, offering surgeons real-time, objective measurements of blood flow and tissue viability that are currently left to subjective visual interpretation. This enhanced objectivity is critical in procedures such as bowel anastomosis assessment or flap reconstruction, where marginal tissue ischemia can lead to serious post-operative complications. The development of deep learning models capable of correcting for imaging artifacts and background noise further ensures data integrity, significantly boosting the clinical confidence in ICG-guided diagnoses and interventions.

Moreover, AI is anticipated to streamline the clinical workflow associated with ICG utilization. For instance, in oncology, AI-powered image segmentation can quickly highlight areas of high ICG accumulation, corresponding to tumor boundaries or metastatic lymph nodes, thereby speeding up surgical resection planning. In ophthalmology, AI can analyze ICG angiography sequences to automatically identify and measure leakage or neovascularization associated with retinal diseases, assisting diagnostic centers in high-throughput patient screening and monitoring treatment efficacy. The strategic importance of AI lies in its potential to democratize sophisticated image analysis, making ICG data more actionable and reproducible across different clinical settings, which ultimately broadens the therapeutic index of this contrast agent.

The dynamics of the Indocyanine Green (ICG) market are shaped by a complex interplay of clinical advancements, regulatory scrutiny, and technological innovation. The primary driver is the accelerating shift towards minimally invasive and precise surgical interventions, which rely heavily on real-time, intraoperative visualization provided by ICG fluorescence. Coupled with this is the continuous expansion of ICG’s approved and off-label applications, particularly in complex fields like robotic surgery and liver function assessment, enhancing its value proposition significantly. However, market growth is restrained by the high initial capital investment required for dedicated Near-Infrared (NIR) imaging systems and the necessity for specialized training among surgical staff to interpret fluorescence images accurately. Opportunities abound in emerging markets where surgical volumes are soaring, and through the development of highly stable, next-generation ICG formulations that address current stability and delivery challenges, positioning the market for sustained expansion.

Impact forces acting upon the market include increasing geriatric populations worldwide, which inherently raise the incidence of conditions like cardiovascular disease and cancer, thereby increasing the demand for ICG-guided interventions. The influence of regulatory bodies, particularly concerning drug stability, purity, and clinical validation for novel applications, exerts a significant force on time-to-market for new products. Moreover, competitive intensity is moderate, characterized by established pharmaceutical players and specialized dye manufacturers, focusing heavily on supply chain reliability and optimizing existing formulations. Technological advancements in competing imaging modalities (e.g., advanced ultrasound) present a modest counter-force, necessitating continuous innovation in ICG delivery and imaging systems to maintain a competitive edge. The overall impact of these forces is overwhelmingly positive, favoring market growth due to the established clinical effectiveness and safety profile of ICG as a real-time diagnostic agent.

Furthermore, the economic impact of ICG in reducing post-operative morbidity, particularly by minimizing undetected tissue ischemia during reconstruction or anastomosis, serves as a powerful market driver. By enhancing surgical decision-making in real-time, ICG procedures often lead to shorter hospital stays and fewer re-operations, resulting in substantial cost savings for healthcare systems. Restraints also include the limited shelf life of reconstituted ICG solutions, which sometimes leads to wastage, though manufacturers are actively addressing this through novel formulations. The opportunity landscape is further broadened by research into conjugating ICG with targeted therapies, exploring its use not just as an imaging agent but as part of a theranostic approach, which represents a highly lucrative long-term growth avenue for the entire market ecosystem.

The Indocyanine Green market is strategically segmented based on its diverse clinical applications, formulation types, and the end-user setting where it is primarily utilized. Segmentation is crucial for market participants to tailor their marketing and distribution strategies, identifying high-growth areas such as oncology and complex surgical procedures, which necessitate high volumes of the dye. The application segmentation, spanning ophthalmology, cardiovascular surgery, neurosurgery, and oncology, reflects the versatility of ICG, with oncology currently commanding the largest share due to widespread use in sentinel lymph node mapping and margin detection, a critical component of modern cancer care protocols. Formulation segmentation distinguishes between lyophilized powder (the traditional format) and emerging liquid or enhanced stability formulations, driven by the push for improved ease of use and reduced preparation time in operating rooms.

The dominance of the surgical segment is underpinned by the essential need for real-time visualization of perfusion and vascular structures during critical, high-stakes procedures. Cardiovascular and neurosurgical applications, while utilizing ICG in smaller volumes per case, represent high-value segments due to the complexity and cost of the procedures involved. Conversely, the diagnostic segment, particularly in liver function testing, provides a stable, recurring revenue stream due to the necessity of frequent monitoring in patients with chronic liver diseases. Analyzing these segments helps stakeholders understand shifting clinical priorities; for instance, the rapid growth in robotic surgery adoption is directly correlated with increased demand for ICG, as fluorescence imaging is often seamlessly integrated into robotic platforms, providing a tangible benefit to minimally invasive techniques.

Geographic segmentation reveals distinct maturity levels; North America and Europe possess high market penetration rates and focus on specialized, high-end applications, whereas APAC and Latin America are in acceleration phases, driven by basic surgical and ophthalmic applications. End-user segmentation confirms hospitals remain the core consumer due to their infrastructure capacity for major surgeries, though ambulatory surgical centers (ASCs) are rapidly emerging as a high-growth end-user segment, particularly for ophthalmic and simpler surgical procedures utilizing ICG. This detailed segmentation allows manufacturers to prioritize investment in supply chain expansion, regulatory efforts in key geographies, and research and development focusing on the most lucrative application niches.

The value chain of the Indocyanine Green (ICG) market commences with the upstream analysis involving the sourcing and synthesis of raw chemical inputs necessary for the production of the highly specialized cyanine dye. This stage is characterized by stringent quality control requirements and reliance on specialized chemical manufacturers to ensure the purity and pharmaceutical-grade quality of the final product, which is critical given its intravenous application. Key activities at this initial stage include organic chemical synthesis, purification processes, and lyophilization to produce the stable powder form, demanding compliance with Current Good Manufacturing Practices (cGMP). High purity standards are paramount, as impurities can affect the dye’s pharmacokinetic profile and safety, thus raw material procurement forms a crucial bottleneck where quality assurance significantly influences downstream success and patient outcomes.

The midstream of the value chain involves the core manufacturing, packaging, and distribution of the sterile ICG product. Manufacturing companies handle the complex process of formulation (often involving proprietary stabilizers), aseptic filling, and final packaging into vials. Distribution channels are highly controlled and typically involve specialized pharmaceutical distributors capable of handling temperature-sensitive and regulated medical products. Direct distribution models are often employed by major players for large hospital networks, ensuring closer control over inventory and rapid response to clinical demand. Indirect channels utilize third-party wholesalers and regional specialty distributors, particularly in fragmented or geographically challenging markets, requiring strict adherence to cold chain logistics to maintain product efficacy until the point of use in healthcare facilities.

Downstream analysis focuses on the end-user adoption and utilization, encompassing hospitals, surgical centers, and diagnostic clinics. This final stage is heavily influenced by equipment manufacturers who provide the necessary NIR imaging systems (cameras and scopes) compatible with ICG. Effective market penetration relies on collaborative efforts between ICG suppliers and imaging system vendors to provide bundled solutions and comprehensive clinical training. The feedback loop from end-users regarding ease of reconstitution, stability, and clinical performance drives continuous improvement in formulation and delivery mechanisms. Reimbursement policies for ICG procedures also play a decisive role in the downstream uptake, determining the economic viability of utilizing ICG in routine clinical practice.

The primary end-users and buyers of Indocyanine Green are highly specialized clinical institutions and medical professionals who require precise, real-time visualization capabilities during diagnostic procedures and surgical interventions. Hospitals, particularly those with large surgical departments covering cardiovascular, neurosurgery, and oncology specialties, represent the largest customer segment due to the frequency of complex procedures and the necessity of capital investment in supporting NIR imaging equipment. Academic medical centers and research institutions also constitute a key customer base, utilizing ICG not only for routine clinical care but also for clinical trials and exploring novel applications of fluorescence imaging in experimental surgery and pathophysiology studies.

Ambulatory Surgical Centers (ASCs) are rapidly emerging as significant customers, particularly those specializing in outpatient procedures such as ophthalmology (retinal angiography) and specific reconstructive surgeries. The efficiency and cost-effectiveness of ASCs, coupled with the rising adoption of minimally invasive techniques, make them an attractive setting for ICG utilization where quick diagnostic turnover is essential. Diagnostic clinics specializing in liver function assessment and certain cardiovascular evaluations also regularly purchase ICG, though often in smaller cumulative volumes compared to major hospitals. The need for precision and patient safety positions these institutions as ideal long-term customers focused on reliable supply and high-purity formulations.

Specific professional groups within these institutions are the direct decision-makers influencing procurement. These include cardiac surgeons relying on ICG for bypass graft patency checks, neurosurgeons utilizing it for vessel delineation, oncologists employing it for sentinel node mapping, and ophthalmologists depending on it for retinal angiography. Procurement decisions are typically centralized, factoring in product stability, supplier reliability, integration with existing imaging platforms, and favorable contractual agreements for consistent supply. Maintaining relationships with key opinion leaders and surgical societies is crucial for manufacturers to influence purchasing decisions and ensure widespread clinical adoption of ICG.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | $185.5 Million USD |

| Market Forecast in 2033 | $310.8 Million USD |

| Growth Rate | 7.75% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Daiichi Sankyo Company Limited, Akorn Operating Company LLC, Diagnostic Green, Wockhardt Limited, Teco Diagnostics, SERB Specialty Pharmaceuticals, Innodix, B. Braun SE, E-Z-EM Canada Inc., Santen Pharmaceutical Co., Ltd., Merck KGaA, Dr. Reddy's Laboratories Ltd., Xylum Corporation, Mylan N.V. (Viatris), Hikma Pharmaceuticals PLC |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological landscape surrounding the Indocyanine Green market is defined by continuous innovation in Near-Infrared (NIR) fluorescence imaging systems, the essential hardware required to visualize the ICG dye. These systems encompass specialized fluorescence cameras, endoscopes, laparoscopes, and robotic surgery platforms that are integrated with dedicated NIR filters and high-sensitivity detectors. The evolution of these imaging technologies focuses heavily on improving image resolution, reducing latency for real-time surgical guidance, and enhancing portability and affordability. Modern surgical visualization systems increasingly incorporate ICG capabilities as standard, offering seamless switching between white light and fluorescence modes, which significantly streamlines the operative workflow and encourages broader clinical adoption across diverse surgical specialties. The ongoing development of chip-on-the-tip technology in endoscopes is further minimizing the size and maximizing the efficiency of NIR visualization, crucial for complex minimally invasive procedures.

Beyond imaging hardware, significant technological advancements are occurring in the development of quantitative fluorescence analysis software. Traditional ICG imaging relies on subjective visual assessment of brightness, but new software platforms employ pharmacokinetic models and kinetic analysis algorithms to provide objective, measurable parameters such as tissue perfusion rates and blood flow velocities. This quantitative approach is crucial for translating ICG data into standardized clinical decision metrics, particularly vital for assessing tissue viability during anastomosis creation in gastrointestinal surgery or evaluating the functional capacity of liver segments prior to resection. These software developments often utilize advanced computational techniques, including machine learning, to normalize images and provide calibrated fluorescence intensity readings, which is a major step toward standardizing ICG usage globally.

Furthermore, the focus is shifting toward optimizing the dye itself. Research and development efforts are dedicated to creating novel ICG formulations, addressing current limitations such as solution instability, aggregation risks at high concentrations, and potential photobleaching. Next-generation formulations include liposomal ICG or nanoparticle-encapsulated ICG, which aim to improve target-specific delivery, enhance stability in solution, and prolong the circulation half-life, making the agent suitable for novel diagnostic applications requiring extended observation times. The integration of advanced microfluidics technology in preparation kits is also being explored to ensure sterile, precise, and rapid reconstitution of the powder form at the point of care, mitigating preparation errors and reducing overall wastage, thereby improving the economic efficiency of ICG utilization in high-volume surgical theaters.

North America, encompassing the United States and Canada, currently holds the largest share of the Indocyanine Green market, primarily driven by exceptionally high healthcare spending, rapid technological adoption, and the widespread use of sophisticated surgical robots and NIR imaging systems. The region benefits from established clinical guidelines that recognize ICG as the standard of care in areas like sentinel lymph node mapping for melanoma and breast cancer, and retinal angiography. Furthermore, favorable reimbursement frameworks for ICG-guided procedures incentivize hospitals and surgical centers to invest in the necessary supporting technology. The US market, in particular, is a global epicenter for innovation, characterized by active research into AI-enhanced image analysis and the introduction of next-generation formulations designed for improved stability and specific tissue targeting. The high volume of complex surgical procedures performed annually ensures consistent and robust demand for high-purity ICG formulations, solidifying the region's lead throughout the forecast period.

The regulatory environment, largely governed by the U.S. Food and Drug Administration (FDA), provides a rigorous but clear pathway for new product introductions and expanded applications, ensuring high standards of safety and efficacy. Key strategic activities in this region include intensive marketing efforts targeting surgical specialty societies and establishing strong partnerships between ICG manufacturers and leading surgical device companies (such as Intuitive Surgical for robotic platform integration). The presence of major pharmaceutical manufacturers and the concentration of advanced academic research institutions further contribute to the rapid uptake of new ICG applications, such as its growing role in perfusion assessment for critical care and trauma surgery. The high degree of consumer awareness regarding advanced diagnostic options also plays a role in driving patient demand for minimally invasive, image-guided procedures.

The Canadian market mirrors the US in terms of high technological standards but operates under a distinct, publicly funded healthcare system, influencing procurement strategies which often favor long-term, high-volume supply contracts. Despite differing procurement methods, the clinical drivers remain identical: the necessity for precise, real-time feedback during complex interventions. The North American market is saturated with advanced NIR imaging systems, ensuring that the infrastructure required for ICG utilization is readily available across almost all major metropolitan and regional medical centers. This technological readiness provides a critical advantage, making ICG adoption relatively seamless when compared to infrastructure-constrained regions, thereby ensuring its continuous market superiority.

Europe represents a mature and highly lucrative market for ICG, characterized by robust healthcare systems and increasing standardization of clinical practices across the European Union. Countries such as Germany, the United Kingdom, and France are leading the adoption curve, driven by established research protocols validating the use of ICG in liver surgery (ICG clearance test) and cardiovascular applications. European medical device regulations (MDR) require stringent certification, ensuring that ICG products and associated imaging equipment meet high safety and quality benchmarks. The adoption rate is steadily increasing as national guidelines increasingly recommend ICG for sentinel node biopsy in various cancers beyond breast cancer, including gynecological and prostate malignancies.

The fragmentation of healthcare systems across Europe necessitates a tailored approach to market entry and distribution. While procurement processes vary significantly, the overall trend is toward minimizing surgical invasiveness and maximizing diagnostic precision, which directly favors ICG technology. Investment in advanced medical technologies, often supported by regional public health initiatives, facilitates the purchase of necessary NIR imaging platforms. A key regional driver is the strong presence of academic institutions engaged in collaborative multinational clinical trials, which often drive the early validation and subsequent widespread adoption of new ICG applications and techniques, ensuring the market remains highly responsive to new evidence.

Eastern European nations are showing accelerated growth, albeit from a smaller base, driven by modernization efforts in healthcare infrastructure and increasing affordability of imaging technology. As these economies align their clinical standards with Western European counterparts, the demand for high-quality diagnostic agents like ICG is expected to surge. Strategic efforts in Europe focus heavily on educating surgeons on the latest techniques and demonstrating the long-term economic benefits (reduced complications, shorter hospital stays) derived from using ICG in fluorescence-guided procedures, reinforcing its vital role in optimizing surgical outcomes across the continent.

The Asia Pacific region is forecast to exhibit the fastest growth rate globally, making it the primary focus for future market expansion. This explosive growth is underpinned by massive population bases, improving economic conditions leading to increased healthcare expenditure, and substantial government investments in establishing advanced medical facilities, particularly in rapidly developing nations such as China, India, and South Korea. The rising incidence of chronic diseases, especially liver and gastric cancers prevalent in the region, significantly boosts the demand for ICG in hepatic surgery and function assessment, where its utility is highly valued.

Market dynamics in APAC are characterized by price sensitivity and a preference for local manufacturing partnerships, although high-quality, imported formulations are dominant in specialty procedures. Japan and South Korea are mature APAC markets, boasting high technological sophistication and early adoption of robotic surgery and associated ICG technology. Conversely, Southeast Asian countries and India represent enormous untapped potential, where expansion is contingent upon regulatory simplification, greater awareness among clinicians, and the development of cost-effective imaging solutions that are suitable for regional budgetary constraints. Educational initiatives focused on teaching fundamental ICG usage protocols are critical for widespread clinical acceptance in these developing markets.

Government focus on reducing healthcare disparities and promoting medical tourism further propels the adoption of internationally recognized standards, including ICG usage. Local manufacturers are actively seeking collaborations or licensing agreements with global ICG suppliers to secure access to high-purity raw materials and advanced formulation technology. The sheer scale of the patient population requiring diagnostic and surgical services across APAC guarantees that this region will be the core driver of volume growth for the Indocyanine Green market in the latter half of the forecast period, transitioning from basic ophthalmic use to complex surgical oncology applications.

The LAMEA region represents a diverse group of emerging markets with varying levels of infrastructure development and market maturity. Latin America, particularly Brazil and Mexico, demonstrates steady demand, driven by increased private healthcare investment and modernization of surgical centers. ICG adoption here is primarily concentrated in major urban centers and high-end specialty hospitals, focusing on ophthalmology and early surgical applications. Market penetration is often slower due to economic volatility and reliance on imported products, making stable supply chain management a critical success factor.

The Middle East, supported by high per capita healthcare spending in countries like Saudi Arabia and the UAE, is rapidly investing in world-class medical facilities and attracting international surgical expertise. This focus on premium healthcare services translates into high demand for advanced diagnostic aids, including ICG, especially in complex cardiac and oncological surgeries. The market here is less price-sensitive than in other emerging regions and highly receptive to integrated technological solutions (ICG dye paired with advanced imaging systems).

Africa, while constrained by limited healthcare access and infrastructure in many sub-Saharan countries, presents long-term potential in key economies such as South Africa. Current ICG use is highly limited and focused mainly on ophthalmic diagnostics and academic research. Future growth depends critically on improving the overall hospital infrastructure, securing international aid funding for medical equipment, and establishing reliable distribution networks for temperature-sensitive pharmaceutical products. Despite current challenges, the rising medical needs across LAMEA offer strategic entry points for ICG manufacturers prioritizing long-term market establishment and expansion.

ICG serves as a near-infrared (NIR) fluorescent contrast agent primarily used to visualize blood flow, tissue perfusion, and lymphatic structures in real-time during diagnostic angiography and fluorescence-guided surgical interventions (FGS). Its main clinical use is in ophthalmology, neurosurgery, and oncology for precise visualization.

The oncology segment, particularly sentinel lymph node mapping and tumor margin delineation during cancer surgery, currently holds the largest market share due to the widespread adoption of ICG in procedures for breast, gastric, and thyroid cancers, where precise tissue identification is critical for optimal outcomes.

The primary restraint is the necessity for high capital expenditure on specialized Near-Infrared (NIR) imaging systems (cameras, scopes) required to visualize ICG fluorescence, which can limit adoption in budget-constrained healthcare settings. Additionally, the short shelf life of reconstituted ICG solutions presents practical limitations.

AI is projected to revolutionize ICG imaging by enabling quantitative fluorescence analysis, moving beyond subjective visual assessment. AI algorithms will automate the measurement of perfusion rates, assist in real-time tumor boundary detection, and standardize image interpretation, enhancing clinical accuracy and reproducibility across institutions.

The Asia Pacific (APAC) region is expected to demonstrate the highest Compound Annual Growth Rate (CAGR) due to rapid improvements in healthcare infrastructure, substantial government investments in surgical technologies, and the rising prevalence of chronic diseases requiring advanced image-guided diagnostics and surgery.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.