ID : MRU_ 438026 | Date : Dec, 2025 | Pages : 245 | Region : Global | Publisher : MRU

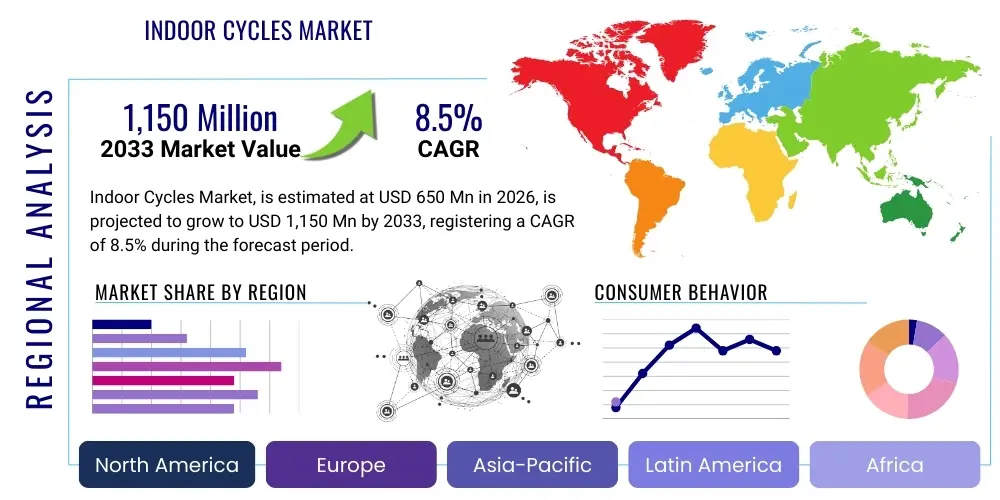

The Indoor Cycles Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 8.5% between 2026 and 2033. The market is estimated at USD 650 Million in 2026 and is projected to reach USD 1,150 Million by the end of the forecast period in 2033.

The Indoor Cycles Market encompasses the manufacturing, distribution, and sale of stationary bicycles designed specifically for indoor physical exercise. These cycles, also commonly referred to as spin bikes, stationary bikes, or exercise bikes, replicate the motions and intensity of outdoor cycling while offering a controlled environment for fitness enthusiasts, professional athletes, and individuals undergoing physical rehabilitation. The core product has evolved significantly from simple mechanical resistance mechanisms to highly sophisticated, connected fitness platforms that integrate digital displays, live class streaming, and performance tracking capabilities. This technological evolution has drastically enhanced user engagement and personalization, positioning indoor cycles as a central component of the modern home fitness ecosystem.

Major applications of indoor cycles span diverse settings, driven by the global focus on health and preventative wellness. In residential settings, particularly post-pandemic, demand surged for high-quality, compact fitness equipment that facilitates structured workouts without requiring external gym membership. Commercial applications include fitness centers, dedicated cycling studios, corporate wellness programs, and educational institutions, where high-durability, multi-user units are preferred. Furthermore, the healthcare sector utilizes recumbent and low-impact indoor cycles for cardiac rehabilitation, physical therapy, and geriatric exercise, capitalizing on their adjustability and minimal joint stress characteristics.

The market is primarily driven by increasing disposable income across developed and rapidly developing economies, coupled with a pervasive consumer preference for convenient, time-efficient exercise solutions. Technological advancements, particularly the integration of Artificial Intelligence (AI) and Machine Learning (ML) for personalized training recommendations and resistance adjustments, serve as significant accelerants. Additionally, the rising prevalence of chronic lifestyle diseases, such as obesity and cardiovascular issues, necessitates accessible and consistent cardiovascular exercise options, further solidifying the necessity and demand for reliable indoor cycling equipment.

The Indoor Cycles Market is characterized by vigorous innovation and intense competition, predominantly driven by the success of connected fitness models. Key business trends indicate a strategic pivot towards subscription-based services accompanying hardware sales, generating substantial recurring revenue streams for leading players. Mergers and acquisitions focused on integrating content creation studios, proprietary software development, and expanding geographical reach are prevalent. Furthermore, sustainability in manufacturing, including the use of recycled materials and energy-efficient designs, is emerging as a critical competitive differentiator, aligning with evolving consumer values regarding corporate social responsibility.

Regionally, North America and Europe remain the dominant markets, attributed to high consumer awareness, advanced fitness infrastructure, and substantial adoption of premium, high-tech cycles. However, the Asia Pacific (APAC) region is poised for the highest growth rate, fueled by expanding urbanization, increasing middle-class populations in China and India, and government initiatives promoting physical fitness. Latin America and the Middle East & Africa (MEA) represent significant untapped potential, where market penetration is currently low but is expected to accelerate due to rising health consciousness and the establishment of localized fitness chains. Companies are increasingly tailoring product offerings to meet regional power grid standards, space constraints, and cultural preferences regarding fitness content.

In terms of segmentation, the Connected/Smart segment, which integrates sophisticated sensors, personalized coaching, and competitive multiplayer features, accounts for the majority of market revenue growth. Within applications, the Home Fitness segment experienced an unprecedented boom due to shifting work and lifestyle patterns, though the Commercial Gym sector is recovering steadily, emphasizing durable, high-throughput models. The Recumbent cycle type, while slower in growth than the Spinner category, maintains a stable position, primarily serving the elderly population and rehabilitation facilities due to its superior ergonomic design and back support, addressing niche but critical market needs efficiently.

User inquiries regarding AI's influence on the Indoor Cycles Market commonly revolve around customization, safety, and engagement longevity. Users frequently ask how AI can tailor resistance automatically based on real-time biometric data (like heart rate variability or perceived exertion), ensuring optimal intensity without manual adjustments. There is also significant interest in AI-driven predictive maintenance, where sensors and algorithms forecast hardware failures before they occur, improving reliability and reducing downtime. Furthermore, consumers anticipate AI integration to solve the pervasive problem of fitness boredom, expecting algorithms to curate dynamically generated workout routes, music playlists, and coaching cues that adapt seamlessly to the user's mood, performance fluctuations, and long-term fitness goals, transforming a simple piece of equipment into a highly responsive, personalized digital coach.

The Indoor Cycles Market is significantly influenced by powerful market dynamics, where technological advancement acts as the primary accelerator, counterbalanced by cost sensitivity and supply chain volatility. The dominant Driver involves the accelerating consumer shift towards holistic wellness, coupled with the proven efficacy and convenience of connected fitness platforms offering diverse, immersive cycling experiences. However, high capital expenditure required for premium connected cycles and the ongoing cost of subscription services serve as substantial Restraints for budget-conscious consumers in emerging markets. This creates a dichotomy where high-value propositions drive growth, but accessibility remains a key bottleneck.

A major Opportunity resides in expanding the market reach through strategic partnerships with healthcare providers and insurance companies, positioning indoor cycling as a preventative medicine tool eligible for reimbursement or subsidized purchase. Further technological integration, such as advanced haptics and Virtual Reality (VR) environments, promises to elevate the immersion level, attracting a broader demographic beyond traditional cycling enthusiasts. The primary Impact Forces shaping the competitive landscape include the swift pace of digitalization in fitness, requiring manufacturers to become software and content providers, and the increasing consolidation of market share by major players capable of vertical integration across hardware, software, and content delivery.

The dynamic interplay between market drivers and constraints dictates innovation cycles. The persistent global focus on public health following the pandemic continues to fuel underlying demand, transforming indoor cycles from niche sports equipment into mainstream home appliances. Manufacturers must navigate complexities related to intellectual property surrounding digital content and personalized algorithms. Ultimately, success hinges on balancing premium product quality and sophisticated technological integration with affordable pricing structures and sustainable business models that effectively mitigate the impact of external economic volatilities.

The Indoor Cycles Market is systematically segmented based on product design, technological complexity, and primary end-use application, allowing for targeted product development and marketing strategies. Segmentation by type differentiates cycles based on rider position and mechanism, ranging from traditional Upright models to ergonomically focused Recumbent cycles and the performance-centric Spinner designs. Technology segmentation is critical, separating basic, resistance-controlled Traditional cycles from the rapidly expanding Connected/Smart category, which integrates digital ecosystems and interactive features. Application segmentation distinguishes between the residential Home Fitness sector and the high-utilization Commercial Gym sector, each demanding distinct levels of durability and connectivity features.

The Indoor Cycles market value chain initiates with Upstream activities encompassing the sourcing and processing of raw materials, primarily steel, specialized plastics, electronic components (microprocessors, touchscreens, sensors), and rubber for belts and pedals. Efficiency in sourcing these high-quality, durable components directly impacts the final product reliability and cost structure. Key challenges in this stage include securing stable supply lines for advanced semiconductors required for smart cycle consoles and managing the geopolitical risks associated with sourcing specialized metals and composite materials used in flywheels and frames.

Midstream activities involve sophisticated manufacturing and assembly, focusing on precision engineering, robust frame construction, and the delicate integration of electronics and software. This stage is highly proprietary, particularly regarding patented magnetic resistance systems and flywheel inertia optimization. Downstream activities cover distribution channels, which are bifurcated into Direct and Indirect sales. Direct-to-Consumer (D2C) channels, often involving online sales platforms and proprietary showrooms, are highly preferred by leading connected fitness brands as they allow for greater control over brand messaging, pricing, and the crucial customer onboarding experience, including personalized delivery and installation services.

Indirect distribution primarily involves partnerships with large retail chains (sporting goods stores, department stores), specialized fitness equipment distributors, and commercial equipment suppliers serving corporate and institutional buyers. For premium connected cycles, maintaining a high-touch, controlled delivery experience is paramount, necessitating specialized logistics partners. Effective channel management, including optimized inventory flow and post-sale support, is essential for maintaining brand reputation and ensuring sustained customer satisfaction and subscription retention, making the service element a critical component of the overall value proposition.

The Indoor Cycles Market serves a broad spectrum of end-users, fundamentally categorized into individual consumers focused on Home Fitness and institutional buyers constituting the Commercial market. For the Home Fitness segment, the primary buyer demographic includes affluent Millennials and Gen X consumers who prioritize health, convenience, and technology integration. These buyers are typically interested in immersive content, social connectivity features, and high-quality industrial design that complements modern interior aesthetics. They often exhibit a high willingness to pay for subscription services that provide personalized training content and leaderboards, driven by the desire for structured, time-efficient workouts that fit into busy professional lives.

Commercial buyers, such as owners of boutique cycling studios (e.g., SoulCycle clones), large commercial gyms (e.g., Planet Fitness, Gold’s Gym), and institutional facilities, prioritize durability, multi-user compatibility, minimal maintenance requirements, and network capabilities to manage large fleets of equipment. For these customers, factors like warranty length, rugged construction materials, and integration with existing gym management software systems are crucial purchasing criteria. The healthcare sector, including rehabilitation centers and physiotherapy clinics, represents a specialized buyer segment focusing on cycles with enhanced accessibility features, such as low step-through frames and precise, quantifiable resistance metrics suitable for therapeutic tracking.

Emerging potential customer groups include corporations investing in in-office or virtual wellness programs to combat employee burnout and enhance productivity, purchasing cycles for dedicated wellness rooms. Additionally, educational institutions, particularly university athletic departments, represent steady demand for performance-oriented indoor cycles used for professional training and conditioning. Strategic market engagement must differentiate between the needs of the content-driven individual consumer and the reliability-focused institutional purchaser, tailoring sales pitches and product features accordingly to maximize penetration across all key end-user verticals.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 650 Million |

| Market Forecast in 2033 | USD 1,150 Million |

| Growth Rate | 8.5% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Peloton Interactive, ICON Health & Fitness (NordicTrack), Nautilus, Life Fitness, Technogym, Precor, Schwinn, Xterra Fitness, CycleOps, Keiser, Stamina Products, Sunny Health & Fitness, Echelon Fitness, ProForm, Kettler |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technology landscape of the Indoor Cycles Market is overwhelmingly dominated by the integration of digital connectivity and immersive user experiences, moving far beyond basic mechanical functions. Central to this transformation are high-definition touchscreens and proprietary operating systems that deliver streaming fitness classes, personalized performance metrics, and gamified elements. Magnetic resistance systems, replacing older friction-based mechanisms, offer smoother, quieter, and more precise control over workout intensity, which is crucial for seamless integration with automated software-driven resistance adjustments characteristic of smart cycles. Furthermore, advanced sensor technology, including cadence sensors, power meters (measuring actual wattage output), and heart rate monitoring integration (via Bluetooth or ANT+), provides riders with crucial data points essential for structured training and physiological tracking.

The proliferation of IoT (Internet of Things) protocols enables seamless data transfer between the cycle, mobile applications, and third-party fitness platforms (like Strava or Apple Health), fostering a comprehensive digital health ecosystem. This interoperability is a growing competitive necessity, ensuring consumers can unify their disparate fitness data streams. Beyond hardware, the proprietary software stack—which includes algorithms for personalized workout generation, AI-driven coaching feedback, and robust content delivery networks (CDNs) for live streaming—represents the highest value capture area. Companies are heavily investing in protecting this digital intellectual property to maintain a competitive edge and secure recurring subscription revenues, recognizing that the content platform, not just the hardware, defines the modern product offering.

Future technology focuses heavily on augmented and virtual reality (AR/VR) integration to further enhance the immersive experience, potentially offering truly collaborative multiplayer rides or hyper-realistic simulated outdoor routes. Advancements in battery technology and self-powered systems are also being explored, particularly for commercial applications, to reduce reliance on external power sources. Critically, cybersecurity measures are increasingly important to protect user biometric and financial data transmitted through these connected devices, ensuring user trust remains intact as the ecosystem becomes more pervasive and data-rich.

Growth is primarily driven by consumer demand for convenient, personalized, and immersive home workout solutions, supported by recurring subscription revenue models offering live and on-demand fitness classes, strong community engagement features, and performance tracking capabilities. This integration of software and hardware transforms exercise into an engaging digital experience.

Magnetic resistance utilizes magnets and the flywheel to create contactless braking, resulting in quieter operation, virtually zero maintenance, and precise digital control over intensity. Friction resistance relies on physical pads pressing against the flywheel, which requires periodic replacement and is typically noisier, common in budget or older cycle models.

The Asia Pacific (APAC) region, driven by rapid urbanization, increasing middle-class disposable income, and growing health consciousness in countries like China and India, is forecasted to exhibit the highest Compound Annual Growth Rate (CAGR) in the adoption of indoor cycling equipment during the projection period.

Subscription fatigue refers to the reluctance of consumers to pay ongoing monthly fees for fitness content services associated with connected cycles. This restraint affects high-end market penetration, pushing some consumers towards mid-range or traditional cycles that offer high-quality hardware without mandatory, recurring digital content costs.

AI significantly enhances the user experience by enabling real-time personalized coaching, automatic resistance adjustments based on biometric data, and the creation of dynamically adapting workout routines. This intelligence provides an optimized, customized training session superior to static, pre-programmed workouts, maximizing efficiency and engagement.

The global Indoor Cycles Market is undergoing a rapid evolution, shifting its emphasis from pure mechanical function to integrated digital ecosystems. The convergence of high-quality hardware with proprietary, dynamic software platforms has fundamentally redefined the competitive landscape. Key industry players are aggressively investing in content creation studios, AI-driven personalization algorithms, and expanded global distribution networks to capitalize on the sustained consumer trend toward at-home wellness. Strategic focus remains on mitigating supply chain risks, reducing the friction associated with high upfront costs through innovative financing options, and developing seamless content offerings that foster high subscription retention rates—the ultimate metric of long-term success in the connected fitness domain. The market's future expansion is intrinsically linked to the continuous technological refinement of both the cycling apparatus and the interactive, digital experience it provides to a global, health-conscious consumer base.

Further analysis indicates that while the immediate post-pandemic surge in home fitness purchases is normalizing, the underlying behavioral shift towards permanent hybrid fitness models ensures robust demand, particularly for premium, feature-rich equipment. Manufacturers are concentrating efforts on product differentiation through enhanced durability for commercial applications and superior user interfaces for home use. Environmental sustainability is also becoming a non-negotiable factor; consumers and institutional buyers increasingly favor brands that demonstrate clear commitments to eco-friendly manufacturing processes and supply chain ethics. This trend necessitates innovation in materials science and energy consumption, subtly influencing design choices across all market segments and ensuring the industry remains aligned with broader environmental, social, and governance (ESG) standards.

In summary, the Indoor Cycles Market stands at the intersection of consumer technology and fitness, requiring companies to operate as sophisticated tech providers rather than just equipment manufacturers. The successful navigation of this dynamic environment hinges on vertical integration—controlling hardware quality, content production, and software delivery—while maintaining pricing strategies that appeal to both the affluent, connected consumer and the emerging, cost-sensitive markets. Future competitive advantage will likely be determined by the ability of companies to seamlessly integrate their cycling platforms into the broader digital health landscape, establishing the indoor cycle as not merely a piece of exercise equipment, but a central health data hub.

The shift towards digital integration also presents unique challenges concerning data privacy and intellectual property. As cycles collect increasingly sensitive biometric and performance data, compliance with global data protection regulations becomes paramount, especially in key markets like Europe and North America. Companies must invest heavily in secure data architectures and transparent privacy policies to maintain user trust, which is foundational to the subscription model's success. Furthermore, the intellectual property landscape is becoming fiercely contested, with numerous lawsuits surrounding patented technology for resistance mechanisms, content delivery methods, and user interface designs, highlighting the importance of robust patent portfolios for securing market position.

Commercial sector recovery is introducing a distinct set of demands. Gyms and studios are now seeking cycles that not only withstand high-volume usage but also integrate with their proprietary facility management software and class booking systems. This requires B2B offerings to feature open APIs (Application Programming Interfaces) and ruggedized components that minimize maintenance downtime. The commercial segment is also increasingly adopting hybrid models, allowing members to access digital content provided by the equipment manufacturer outside of the physical gym, blurring the lines between home and studio cycling and creating new revenue streams for facility operators through partnership agreements.

Finally, the long-term sustainability of the market depends heavily on continuous product innovation that addresses evolving consumer needs beyond basic cardio. This includes developing cycles that better mimic outdoor terrain simulation, integrating complex power training metrics, and enhancing connectivity to include collaborative virtual racing. These advanced features ensure that the indoor cycling experience remains compelling and justifies the premium pricing often attached to smart cycle ecosystems, thereby sustaining growth beyond the initial purchase enthusiasm.

Innovation in material science is also playing a significant role in market development. The use of lighter, stronger, and more corrosion-resistant alloys, along with advanced composite plastics, contributes to improved portability and durability. This is particularly important for high-end home cycles where aesthetic appeal and ease of movement within a living space are prioritized by the consumer. Furthermore, ergonomic design improvements, such as enhanced seat adjustability, specialized pedal options, and optimized Q-factors (the distance between the pedals), are crucial for catering to a broader range of body types and reducing the risk of exercise-related injuries, thereby broadening market appeal to novice users and specialized training populations alike.

The financial viability of the subscription models remains a key area of industry focus. Customer acquisition costs (CAC) for connected fitness hardware can be high, necessitating long-term retention strategies to ensure profitability. Companies are exploring diversified content offerings, including cross-training programs (yoga, strength) accessed through the cycle's screen, and personalized nutrition planning, to increase the perceived value of the subscription beyond just cycling classes. Bundling strategies that combine hardware purchase costs with extended subscription periods are increasingly common, aiming to secure revenue predictability and establish a durable customer relationship from the outset.

Government initiatives globally promoting physical activity and fighting obesity are providing underlying support to the market. In several nations, incentives or tax deductions for fitness equipment purchases, particularly those utilized for rehabilitation or preventative health, indirectly boost demand. This governmental endorsement legitimizes the indoor cycle as a vital health tool rather than a luxury item, potentially opening avenues for broader institutional purchasing, including public schools and government wellness programs, further diversifying the customer base beyond traditional retail channels.

The competitive dynamics are highly concentrated at the top tier, dominated by companies that have successfully integrated hardware manufacturing with proprietary software and content creation. However, niche players continue to thrive by focusing on specific segments, such as highly accurate power measurement devices for serious athletes (e.g., Stages Cycling) or budget-friendly, yet reliable, traditional models (e.g., Sunny Health & Fitness). This market structure necessitates constant strategic maneuvering, requiring leading companies to continually defend their content moat while mid-tier companies seek technological partnerships to elevate their offerings and remain competitive against the high-volume, low-cost manufacturers operating primarily in APAC.

In terms of technological evolution, the development of haptic feedback systems integrated into the handlebars or pedals represents a compelling area for enhanced immersion. Haptics can simulate the vibrations and sensations associated with different road surfaces or gear shifts, providing a more realistic and engaging virtual cycling experience. Furthermore, improvements in connectivity standards, specifically the adoption of Wi-Fi 6 and future wireless protocols, are crucial for ensuring seamless, uninterrupted streaming of high-definition, live fitness classes to millions of users globally, addressing latency issues that could otherwise degrade the interactive workout experience and impact customer satisfaction and retention rates within the subscription ecosystem.

The market faces external economic pressures, particularly inflation and interest rate hikes, which impact consumer spending on discretionary high-ticket items like premium cycles. In response, financing options, including zero-interest installment plans and lease-to-own models, are becoming standard practice for mitigating sticker shock and maintaining sales volume. These financial strategies are key to making premium equipment accessible to a wider demographic, ensuring continuous market penetration even during periods of economic constraint, provided that the perceived long-term health benefits outweigh the immediate financial burden for the consumer.

Looking ahead, the successful adaptation to augmented reality (AR) applications could unlock a new wave of growth. Instead of relying solely on built-in screens, AR glasses or headsets could overlay fitness metrics, virtual coaches, and simulated terrain onto the user's actual environment, offering a unique blend of reality and digital immersion. This blending of physical and digital environments appeals to the growing segment of users seeking novel, engaging, and less isolating forms of indoor exercise, potentially rejuvenating consumer interest in the high-end market segment and driving hardware refresh cycles in the coming years.

Finally, the influence of professional sports and competitive cycling teams on product design remains significant. Innovations developed for professional training—such as highly precise power measurement, advanced biomechanical geometry, and specific saddle design—often trickle down into the high-end consumer market, positioning those models as performance tools rather than just fitness equipment. This linkage provides strong marketing narratives centered on elite performance and reliability, further justifying the premium pricing structure and appealing to the segment of highly motivated amateur athletes and serious cycling enthusiasts.

The maintenance and service aspect of the Indoor Cycles Market is evolving significantly, moving towards proactive and preventative models, largely enabled by integrated IoT sensors. Manufacturers are using remote diagnostics to monitor equipment health, often resolving minor issues via software updates before they require a technician visit. This shift from reactive repair to predictive maintenance is a crucial differentiator for commercial clients, where equipment downtime directly translates to lost revenue. For home users, streamlined remote support and robust self-help documentation contribute positively to the overall customer experience and reduce warranty claims, reinforcing the brand's commitment to reliability and service quality.

Market expansion in emerging economies requires localized strategic adjustments. In regions where average household space is limited, the demand for foldable, compact, and easily stored cycles is notably higher, prompting specialized product development focusing on space efficiency without compromising core functionality or digital integration. Furthermore, content must be culturally and linguistically relevant; success in APAC or LATAM depends heavily on hiring local fitness instructors and producing classes in native languages that resonate authentically with regional audiences, rather than relying solely on translated content from Western markets.

The role of data analytics has transcended basic performance tracking; companies now leverage anonymized aggregate user data to inform strategic business decisions. This includes optimizing class schedules for global audiences, identifying emerging fitness trends, and predicting which hardware features are most utilized and valued. This sophisticated use of big data allows for highly responsive content strategy and personalized marketing campaigns, creating a data-driven feedback loop that continuously improves both the hardware offering and the associated digital service platform, ensuring that product development remains highly aligned with evolving user preferences and market demands.

Furthermore, the integration with third-party digital health trackers and wearables (e.g., Apple Watch, Fitbit) is a critical feature, enhancing the seamlessness of data aggregation for the user. Modern indoor cycles must function as open platforms, easily syncing workout metrics to comprehensive health dashboards. This interoperability minimizes user effort in logging data and maximizes the perceived utility of the cycle within the broader digital wellness ecosystem, promoting brand loyalty and further establishing the cycle as an integral component of the user's long-term health monitoring strategy, distinguishing market leaders from basic hardware providers.

In conclusion, the Indoor Cycles Market is defined by a dynamic synthesis of hardware engineering, software intelligence, and proprietary content creation. The dominant growth vectors are rooted in personalization, seamless connectivity, and the transition to a service-oriented revenue model. Sustained success requires ongoing vigilance concerning technological disruption, a keen focus on localized market requirements, and rigorous attention to data security and ethical privacy practices, ensuring the market continues its trajectory of high-value innovation.

The rapid advancement in display technology, specifically the shift towards larger, higher-resolution, and more durable touchscreens, significantly enhances the immersion of the cycling experience. For connected cycles, the screen serves as the primary gateway to the fitness ecosystem, and superior visual quality is essential for delivering engaging scenic rides and detailed workout metrics. Manufacturers are increasingly adopting screens with anti-glare coatings and improved responsiveness, suitable for the high-intensity, sweaty environment typical of indoor cycling, contributing directly to the cycle's premium valuation and user satisfaction.

Regarding sustainability, the market is beginning to address the lifecycle management of electronic components and large steel frames. Initiatives include take-back programs for outdated hardware and the design of cycles with modular components that allow for easier repair and upgrades, extending the product's lifespan and reducing electronic waste. This focus on the circular economy is particularly resonant with environmentally conscious consumers in developed markets and is becoming a key factor in corporate procurement decisions for large commercial and institutional buyers, acting as a competitive lever in a highly saturated market segment.

The competitive structure is heavily influenced by intellectual property barriers, primarily surrounding proprietary resistance systems and patented subscription service mechanisms. Companies that successfully protect their core innovations—whether it is a unique magnetic braking system that offers superior realism or a novel content delivery architecture—are better positioned to maintain high margins and secure long-term market dominance. This constant legal scrutiny over IP highlights the mature and high-stakes nature of the battle for market share among the top-tier connected fitness companies, prioritizing legal strategy alongside technological development.

Moreover, the rise of the specialized boutique studio format globally continues to influence product design, requiring equipment that can handle extremely rigorous use cycles (often 10+ hours daily) while maintaining aesthetic consistency and network stability across large groups of connected machines. This high-demand commercial environment drives innovation in component ruggedization, frame geometry stability, and simplified user interfaces designed for quick transitions between riders, indirectly benefiting the high-end home user by ensuring exceptional build quality and longevity.

Finally, emerging payment technologies, such as integrated contactless payment for commercial gym usage or simplified in-app purchasing for content, are streamlining the transaction process, particularly in regions with high mobile payment adoption. Facilitating easy access to content and services reduces barriers to entry for new subscribers, supporting the overall subscription revenue stability, which remains the backbone of profitability for the leading connected cycle market participants.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.