ID : MRU_ 433070 | Date : Dec, 2025 | Pages : 246 | Region : Global | Publisher : MRU

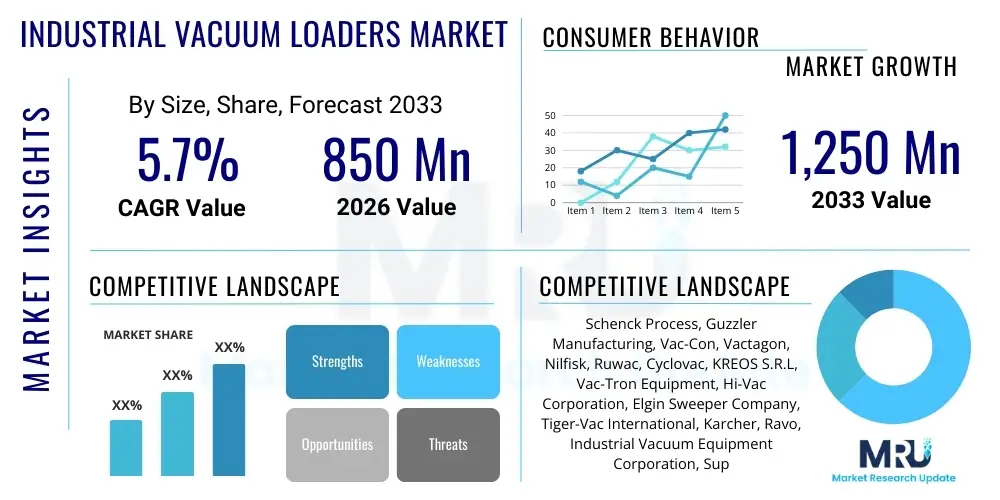

The Industrial Vacuum Loaders Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 5.7% between 2026 and 2033. The market is estimated at USD 850 Million in 2026 and is projected to reach USD 1,250 Million by the end of the forecast period in 2033. This consistent expansion is primarily fueled by stringent industrial safety regulations across developed economies and the increasing adoption of automated material handling solutions in emerging industrial hubs.

Industrial Vacuum Loaders are specialized heavy-duty equipment designed for the high-efficiency collection, conveyance, and removal of dry bulk materials, powders, slurries, and heavy debris within industrial settings. These systems utilize high-powered vacuum technology to manage large volumes of material quickly, ensuring operational cleanliness and regulatory compliance regarding dust control. They are indispensable tools in environments where spilled or waste materials must be recovered rapidly and safely, minimizing downtime and reducing manual labor risks. Their design focuses on robust construction, high suction capabilities, and versatility across various media types, ranging from fine cement dust to heavy gravel and slag.

The primary applications of Industrial Vacuum Loaders span across foundational industrial sectors, including cement manufacturing, metal processing, mining and aggregates, chemical production, and power generation facilities. In these demanding environments, the equipment is utilized for routine maintenance (cleaning silos, conveying raw materials), emergency spill recovery, and dedicated environmental remediation projects. The critical advantage offered by these loaders is their ability to handle hazardous or abrasive materials remotely, thereby significantly enhancing worker safety and environmental protection by controlling fugitive dust emissions, which is a major regulatory concern globally.

Market growth is robustly driven by several macro and micro factors. Key drivers include the escalating focus on occupational safety standards, particularly concerning silica dust and other airborne contaminants, compelling industries to upgrade to high-efficiency vacuum loading systems. Furthermore, the global surge in infrastructure development and manufacturing output necessitates faster, more reliable methods for material transfer and cleanup, making industrial vacuum loaders essential for optimizing process efficiency and throughput. The inherent benefits of reduced labor costs and minimized production interruptions further solidify their market position as critical capital equipment investments.

The Industrial Vacuum Loaders Market is characterized by steady technological advancements focusing on enhanced mobility, increased suction power efficiency, and integration of predictive maintenance features. Current business trends indicate a strong shift towards mobile and truck-mounted vacuum loaders, which offer superior flexibility for handling cleanup operations across large or multi-site industrial complexes. Manufacturers are increasingly emphasizing modular designs that allow for quick configuration changes based on material type and regulatory requirements, catering to the highly customized needs of end-users in sectors like oil and gas, and heavy manufacturing. Furthermore, the development of high-filtration systems, specifically HEPA compliance for toxic materials, is a key differentiator driving purchasing decisions in regulated industries.

Regionally, the market dynamics are polarized between matured regulatory landscapes and rapidly industrializing zones. North America and Europe maintain leading market shares, primarily driven by strict environmental protection agencies and well-established industrial safety protocols that necessitate continuous replacement and upgrade of vacuum equipment. However, the Asia Pacific (APAC) region is forecasted to exhibit the highest CAGR due to massive investments in infrastructure, mining, and cement industries, particularly in countries like China, India, and Southeast Asia. This growth is also supported by the gradual adoption of Western safety standards, pushing local manufacturers to improve product quality and capacity.

Segmentation trends highlight the increasing demand for high-capacity, heavy-duty loaders (above 15 cubic yards) suitable for large-scale industrial cleanup, particularly in mining and metallurgical operations. Concurrently, the power source segment shows a growing preference for electric and natural gas-powered units over traditional diesel models, driven by corporate sustainability initiatives and lower operational noise requirements in urban or semi-urban industrial zones. The rental and leasing segment is also seeing accelerated growth, particularly among smaller and medium-sized enterprises (SMEs), allowing them access to high-cost machinery without significant capital outlay, thereby democratizing access to high-efficiency cleanup technologies and supporting temporary project needs.

User inquiries regarding AI in Industrial Vacuum Loaders primarily center around enhancing operational efficiency, extending equipment lifespan, and integrating autonomous functions within confined or hazardous spaces. Common questions address how AI can analyze vibration and temperature data for predictive maintenance (minimizing unexpected breakdowns), how machine learning algorithms optimize vacuum pressures based on the type of material being loaded (maximizing efficiency), and the feasibility of implementing semi-autonomous routing and operational sequencing for truck-mounted units at large facilities. Users are intensely focused on leveraging AI to move beyond reactive maintenance models, seeking solutions that provide prescriptive diagnostics and real-time operational adjustments to reduce fuel consumption and wear on critical components like blowers and filtration systems.

The implementation of Artificial Intelligence and advanced analytics is set to fundamentally transform the industrial vacuum loaders ecosystem, shifting these robust machines into smart, connected assets. AI-driven predictive maintenance models utilize sensor data from the blower motor, hydraulic systems, and collection systems to forecast potential failures with high accuracy, enabling proactive servicing rather than costly emergency repairs. This minimizes unplanned downtime, which is critical in capital-intensive industries such as steel manufacturing and petrochemicals, ultimately lowering the Total Cost of Ownership (TCO) for the end-user and significantly boosting asset utilization rates across the fleet.

Furthermore, AI algorithms are vital for optimizing operational parameters in real-time. For instance, sophisticated suction optimization software, powered by machine learning, can automatically adjust the airflow and vacuum level based on sensor feedback detailing material density and moisture content. This ensures maximum loading speed while simultaneously preventing damage to the vacuum pump or clogging of the conveyance pipes, thereby improving overall operational throughput and energy efficiency. The long-term trajectory involves incorporating fully autonomous navigation systems for stationary units within factory settings and advanced data integration with plant-wide Enterprise Resource Planning (ERP) systems for comprehensive waste management reporting and compliance verification.

The market for Industrial Vacuum Loaders is highly influenced by a confluence of regulatory pressures, economic drivers, technological limitations, and emerging opportunities within industrial maintenance paradigms. Drivers are predominantly centered around the global push for stricter environmental compliance and enhanced occupational safety, mandating the use of contained and efficient dust removal systems, particularly for toxic or carcinogenic materials like lead dust or certain chemical residues. Restraints often revolve around the substantial capital expenditure required for purchasing high-capacity, technically advanced units, coupled with operational constraints such as the high noise levels generated by powerful vacuum pumps, leading to noise pollution concerns in certain operational areas.

Opportunities in this sector are strongly linked to innovation in mobility and sustainability. The growing preference for electric and alternative-fuel (e.g., CNG/LNG) vacuum loaders presents a significant avenue for market expansion, appealing to companies prioritizing reduced carbon footprints and lower operating costs compared to traditional diesel-powered systems. Moreover, the expanding industrial rental market, especially in North America and Europe, is creating substantial opportunities by allowing smaller players and construction firms to deploy state-of-the-art equipment for project-based needs without committing to heavy long-term investment, thus broadening the user base significantly.

The impact forces currently shaping the market include high industrialization rates in APAC, leading to massive demand for robust debris handling, and the relentless pressure from regulatory bodies like OSHA and EPA, which dictates minimum standards for air quality and material handling across industrialized nations. Technology acts as a powerful enabling force, with IoT integration and telematics becoming standard, driving productivity improvements and maintenance efficiency, thereby justifying the initial high cost of these sophisticated loading systems. These intertwined forces ensure sustained demand, especially for highly automated and environmentally compliant equipment that guarantees operational continuity.

The Industrial Vacuum Loaders Market is comprehensively segmented based on several key operational and technical characteristics, ensuring a detailed view of market demand across various industrial applications. Primary segmentation is categorized by mobility (Mobile vs. Stationary), power source (Diesel, Electric, Alternative Fuels), capacity (low, medium, high), and final application industry (Cement, Chemical, Mining, etc.). This multifaceted segmentation allows stakeholders to accurately gauge demand pockets and tailor product development to specific end-user needs, particularly regarding regulatory requirements and material handling volumes. The increasing complexity of industrial waste necessitates specialized equipment, driving diversification across all these segments.

The mobility segment is highly dynamic, with truck-mounted (mobile) units dominating the market share due to their flexibility and ability to serve multiple locations within large industrial parks or handle emergency response scenarios rapidly. Conversely, stationary systems, often integrated directly into production lines or centralized dust collection networks, are crucial for continuous, high-volume material transfer in facilities like power plants or major chemical processing sites. The increasing demand for mobile units is driven by outsourcing industrial cleaning and maintenance tasks, requiring equipment that can efficiently traverse different operational zones.

In terms of capacity, the heavy-duty segment (exceeding 15 cubic yards) is expected to grow significantly, fueled by expansion in the mining and construction sectors where large volumes of abrasive materials must be conveyed over long distances. Meanwhile, the medium-capacity segment remains the bedrock of demand across general manufacturing and utilities. The ongoing shift toward electric and alternative-fuel power sources is not only a response to environmental concerns but also addresses internal requirements in sensitive facilities, such as food processing or pharmaceutical manufacturing, where zero emissions are often mandated to prevent product contamination.

The value chain for the Industrial Vacuum Loaders Market begins with the upstream supply of core components, including high-grade steel, complex filtration media (e.g., HEPA filters, filter bags), specialized high-power blowers (positive displacement or centrifugal), and advanced hydraulic systems. Key success factors in the upstream phase involve securing reliable, high-performance blower technology and durable wear parts, as the efficiency and longevity of the final product heavily depend on the quality and precision of these components. Manufacturers often establish long-term relationships with specialized component suppliers to ensure quality control and optimize inventory management, mitigating risks associated with supply chain disruptions, especially for specialized materials subject to market volatility.

The manufacturing stage involves the assembly, integration, and customization of these components into the final vacuum loader system, often mounted on specialized heavy-duty chassis provided by truck manufacturers for mobile units. This stage is characterized by significant capital investment in fabrication facilities, quality assurance, and specialized engineering expertise required to design robust systems capable of handling corrosive and abrasive materials under continuous heavy load. Value addition here focuses on engineering design that maximizes suction efficiency, minimizes maintenance requirements, and ensures compliance with relevant transport and industrial safety standards, offering differentiated features like automated bag shaking systems and noise suppression technologies.

The downstream segment encompasses distribution, sales, and aftermarket services. Distribution channels are typically a mix of direct sales teams catering to large industrial corporations (e.g., mining majors) and a robust network of authorized distributors and dealers specializing in industrial maintenance equipment. Aftermarket services, including spare parts supply, maintenance contracts, and technical support, represent a crucial revenue stream and a significant factor in customer retention and brand loyalty. Direct sales are prevalent for highly customized, high-value stationary installations, while the dealer network is essential for market penetration and supporting the growing rental segment by providing localized maintenance and rapid response capabilities, ensuring maximum machine uptime for end-users.

The primary customers for Industrial Vacuum Loaders are organizations operating within heavy industry and those facing substantial challenges related to bulk material spillage, regulatory compliance for dust control, and continuous process cleanup. These customers require robust, high-throughput equipment that can handle diverse materials ranging from fine powders to heavy, dense aggregates. The core market lies within the cement, aggregates, and mining sectors, where the need for rapid recovery of spilled product and maintenance cleaning in challenging environments (e.g., kilns, conveyor systems) is constant and directly impacts operational efficiency and production quotas.

Secondary, but rapidly growing, customer segments include the chemical and petrochemical industries, and power generation plants. In these sectors, the focus shifts slightly towards safety and environmental compliance; customers need loaders capable of handling hazardous, toxic, or explosive materials (such as catalyst dust or coal ash) safely, often necessitating explosion-proof (ATEX compliant) designs and sophisticated filtration systems. For these buyers, adherence to strict OSHA and EPA standards regarding air quality and confined space entry is the paramount purchasing consideration, making specialized features like inert gas purging and advanced monitoring systems critical decision points.

A third crucial segment comprises the industrial maintenance and cleaning contractors who serve the wider industrial base. These service providers often purchase truck-mounted, mobile units to offer outsourced cleanup and material recovery services across multiple client sites, representing a significant portion of the demand for flexible, high-capacity equipment. Additionally, smaller niche markets, such as food processing and pharmaceuticals, require smaller capacity, but ultra-hygienic stainless steel loaders with HEPA filtration, where the prevention of cross-contamination is a non-negotiable requirement for product safety and regulatory adherence.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 850 Million |

| Market Forecast in 2033 | USD 1,250 Million |

| Growth Rate | 5.7% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Schenck Process, Guzzler Manufacturing, Vac-Con, Vactagon, Nilfisk, Ruwac, Cyclovac, KREOS S.R.L, Vac-Tron Equipment, Hi-Vac Corporation, Elgin Sweeper Company, Tiger-Vac International, Karcher, Ravo, Industrial Vacuum Equipment Corporation, Supersucker, Diversey, Tennant Company, Macropak, OTR Dumpers |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological landscape of Industrial Vacuum Loaders is rapidly evolving, driven primarily by the demands for greater efficiency, reduced environmental impact, and enhanced operator safety. A central technological advancement is the integration of high-efficiency particulate air (HEPA) filtration and advanced cyclone separation technologies. These systems ensure that hazardous or ultra-fine dust (such as silica or asbestos) is safely contained and filtered down to sub-micron levels, meeting the increasingly rigorous air quality standards set by global regulatory bodies. Modular filter designs that allow for easy, contained, and safe replacement of filter bags or cartridges are becoming standard, minimizing worker exposure during maintenance procedures and improving operational throughput by reducing filter cleaning downtime.

Furthermore, the incorporation of Internet of Things (IoT) sensors and advanced telematics is transforming traditional vacuum loaders into connected industrial assets. These technologies allow for continuous monitoring of critical operating parameters, including vacuum pressure, engine performance, fluid levels, and filter saturation. The data gathered is then used to facilitate remote diagnostics and predictive maintenance scheduling, significantly increasing machine uptime and operational reliability. Telematics also aids in geo-fencing and tracking mobile assets, which is crucial for large construction and mining companies managing extensive fleets across multiple remote locations, thereby improving asset security and utilization reporting.

Innovation is also evident in power source diversification and equipment design. There is a marked shift toward Variable Frequency Drive (VFD) technology in stationary electric units, which allows the motor speed and corresponding suction power to be precisely controlled based on material load, leading to substantial energy savings compared to fixed-speed systems. Simultaneously, for mobile units, the focus is on optimizing aerodynamic design within the material flow path and developing lightweight, high-tensile steel bodies to maximize payload capacity while maintaining regulatory compliance regarding vehicle weight restrictions. These engineering improvements aim to reduce fuel consumption and increase the overall cost-effectiveness of material recovery operations, solidifying the equipment’s value proposition in cost-sensitive industrial sectors.

The global Industrial Vacuum Loaders Market exhibits distinct growth trajectories and demand patterns across major geographical regions, influenced by localized industrial maturity, regulatory stringency, and infrastructure investment levels. North America (NA) represents a dominant market, characterized by high regulatory enforcement regarding dust control (especially silica dust) and a strong reliance on heavy-duty, truck-mounted units for environmental cleanup and emergency response. The region benefits from a mature industrial base and a high adoption rate of advanced, technologically integrated vacuum systems, driven by high labor costs that incentivize efficient automation.

Europe stands as another major market, prioritizing sustainability and efficiency. European demand is heavily influenced by strict EU directives on noise pollution (particularly for urban industrial operations) and emissions standards (Euro VI), accelerating the transition towards electric and alternative-fuel powered vacuum loaders. Germany, the UK, and France are key consumers, often opting for customized stationary units integrated into existing high-tech manufacturing and recycling processes where zero-emission operation is paramount for internal health, safety, and environmental standards.

Asia Pacific (APAC) is projected to be the fastest-growing region throughout the forecast period. This explosive growth is underpinned by rapid industrialization, extensive mining and infrastructure projects (especially in China, India, and Southeast Asia), and gradually tightening regulatory environments. While initial adoption favors cost-effective, high-capacity diesel units, there is a swift movement towards adopting advanced systems as local regulations align with international safety standards, making APAC a critical future growth engine for advanced mobile and specialized loaders.

Mobile vacuum loaders, typically truck or trailer-mounted, offer flexibility for cleanup across multiple locations or emergency spill response, dominating site-wide maintenance operations. Stationary loaders are fixed installations integrated into production lines, designed for continuous, high-volume material transfer or centralized dust extraction systems within a single facility, focusing on consistent process efficiency.

Regulations, particularly concerning silica dust (OSHA) and air quality (EPA), are driving manufacturers to integrate advanced filtration technologies like HEPA filters and self-cleaning systems. This ensures compliance by capturing sub-micron particulate matter, thereby reducing harmful emissions and minimizing worker exposure to airborne contaminants.

The Mining and Metals industry segment is the largest contributor to demand for high-capacity (over 15 cubic yards) vacuum loaders. These sectors require equipment capable of handling massive volumes of dense, abrasive materials, such as iron ore, coal, and aggregates, for large-scale recovery, transfer, and cleanup operations in demanding environments.

IoT technology enables remote monitoring and telematics, providing real-time data on engine performance, vacuum pressure, and filter status. This facilitates predictive maintenance scheduling, optimizes operational efficiency by alerting operators to potential issues before failure, and reduces overall downtime, thereby maximizing asset utilization and minimizing maintenance costs.

Yes, there is a clear market shift towards electric and alternative-fuel (CNG/LNG) powered loaders, particularly in Europe and North America. This transition is motivated by increasingly stringent noise and emission regulations, corporate sustainability mandates, and the pursuit of lower long-term operating costs associated with reduced fuel consumption and maintenance complexity.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.