ID : MRU_ 432935 | Date : Dec, 2025 | Pages : 257 | Region : Global | Publisher : MRU

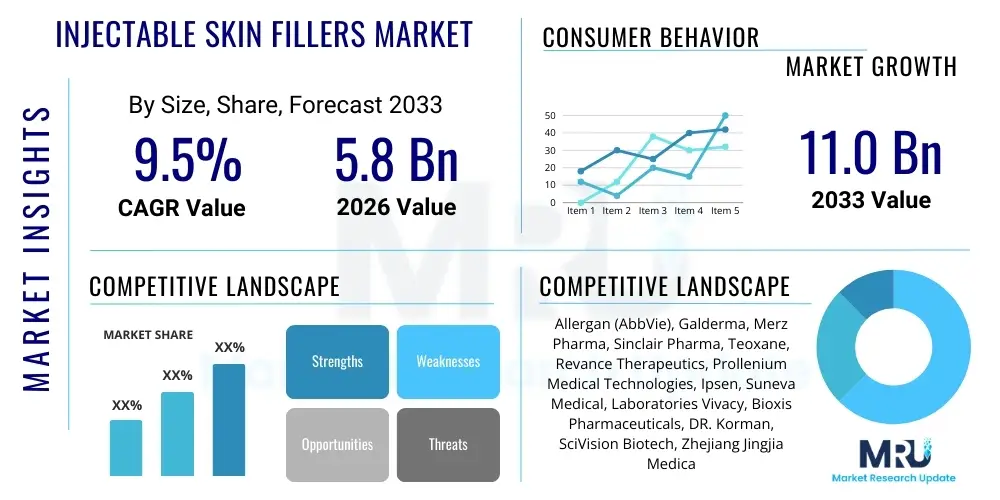

The Injectable Skin Fillers Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 9.5% between 2026 and 2033. The market is estimated at USD 5.8 Billion in 2026 and is projected to reach USD 11.0 Billion by the end of the forecast period in 2033. This substantial expansion is fundamentally driven by the escalating global demand for minimally invasive cosmetic procedures, coupled with technological advancements leading to the development of safer, longer-lasting, and more effective filler formulations. The aesthetic industry is witnessing a paradigm shift, favoring non-surgical alternatives that offer reduced downtime and immediate, visible results, thereby accelerating market adoption across mature and emerging economies.

The Injectable Skin Fillers Market encompasses a range of medical devices, primarily gels and colloidal substances, injected subdermally or intradermally to restore volume, contour facial features, smooth wrinkles, and enhance skin appearance. These products, often based on compounds such as Hyaluronic Acid (HA), Calcium Hydroxylapatite (CaHA), Poly-L-Lactic Acid (PLLA), and Polymethylmethacrylate (PMMA), serve as pivotal tools in aesthetic medicine for addressing signs of aging, lip enhancement, and scar correction. Injectable fillers offer a non-permanent or semi-permanent solution for dynamic and static wrinkles, providing significant benefits over surgical interventions, including minimal risk, swift procedure times, and immediate post-treatment results, contributing directly to their immense popularity among consumers seeking aesthetic improvements.

Major applications of these fillers span across facial aesthetics, including the correction of nasolabial folds, volume restoration in cheeks and temples, chin and jawline definition, and hand rejuvenation. The primary benefits include the provision of natural-looking results, high patient satisfaction rates, and the reversibility of certain filler types, particularly HA-based products, which offers a safety net for both practitioners and patients. Driving factors for this market include the rise in disposable incomes globally, increasing social acceptance of cosmetic procedures, heavy investment in research and development by manufacturers to improve biocompatibility and longevity, and pervasive influence of social media trends promoting aesthetic perfection and anti-aging treatments across diverse demographic groups.

The continuous innovation in filler technology, focusing on optimized rheology and enhanced cross-linking techniques, is crucial for sustained market growth. Furthermore, the expansion of qualified practitioners and the increasing number of regulated product approvals in major markets bolster consumer confidence and safety, which are essential prerequisites for driving adoption rates in this highly discretionary sector. The strategic marketing efforts by key industry players, focusing on educating consumers about the efficacy and safety profiles of different filler types, are instrumental in penetrating new patient cohorts, particularly younger demographics seeking preventative or subtle enhancement procedures, solidifying the market's trajectory towards robust expansion.

The Injectable Skin Fillers Market is characterized by vigorous growth, primarily fueled by shifting consumer preferences towards minimally invasive aesthetic solutions and rapid advancements in biomaterial science, particularly relating to specialized Hyaluronic Acid formulations. Key business trends include aggressive mergers and acquisitions among major pharmaceutical and medical aesthetics companies, focused portfolio diversification to cover temporary, semi-permanent, and permanent filler categories, and significant expansion of training programs to ensure safe and effective product utilization by certified professionals globally. Regional trends indicate North America maintaining market dominance due to high procedure volumes and established aesthetic infrastructure, while Asia Pacific exhibits the fastest growth trajectory, driven by burgeoning middle-class populations, increased awareness, and evolving beauty standards across countries like China, South Korea, and India, presenting unparalleled opportunities for market penetration and commercial scaling.

Segment trends reveal that the Hyaluronic Acid (HA) segment remains the undisputed leader, commanding the largest revenue share due to its excellent safety profile, reversibility, and versatility across various facial applications; however, segments utilizing Poly-L-Lactic Acid (PLLA) and Calcium Hydroxylapatite (CaHA) are demonstrating accelerating growth as patients and practitioners seek longer-lasting, collagen-stimulating alternatives for profound volume loss correction. The Application segment is dominated by facial anti-aging treatments and facial volume restoration, reflecting the core consumer demand for age reversal, though lip augmentation procedures are showing exceptional growth, particularly among younger patients. Distribution channel analysis confirms that Dermatology Clinics and MedSpas collectively represent the primary point of service delivery, emphasizing the critical role of specialized outpatient settings in market accessibility and service quality.

The competitive landscape is intensely focused on product differentiation through rheological properties, duration of effect, and integration capabilities within the dermal structure, alongside strict adherence to regulatory standards across different geographical jurisdictions. Companies are leveraging digital marketing and social media engagement to directly influence consumer choices, while simultaneously investing in clinical trials to validate new indications and establish superior efficacy claims against existing benchmarks. Strategic partnerships with key opinion leaders (KOLs) and high-volume practitioners are essential components of the market strategy, ensuring rapid adoption of new product releases and maintaining brand credibility within the professional aesthetic community, which collectively steers the market toward sustainable high single-digit growth rates throughout the forecast period.

Common user questions regarding AI's impact on Injectable Skin Fillers center on personalized treatment planning, potential automation of injection techniques, and enhanced patient safety through sophisticated diagnostics. Users frequently inquire if AI algorithms can predict optimal filler placement based on individual facial anatomy and aging patterns, thus moving beyond standardized protocols. Concerns also revolve around data privacy when utilizing complex facial imaging and machine learning for aesthetic assessments, and the potential displacement of human expertise in diagnosis and administration. The overarching theme is the expectation that AI will revolutionize precision and consistency in aesthetic outcomes, moving the industry toward hyper-personalized, data-driven cosmetic procedures, while simultaneously demanding assurances regarding ethical implementation and regulatory oversight of automated diagnostic systems and procedural guidance tools, ensuring they augment, rather than replace, certified medical professionals.

The Injectable Skin Fillers Market is primarily driven by the escalating demand for minimally invasive cosmetic solutions globally, attributed to consumer preference for low downtime, immediate results, and reduced procedural risks compared to traditional surgical facelifts. Key drivers include the increasing disposable income in emerging economies, the positive influence of aesthetic procedures promoted across digital platforms, and continuous technological enhancements yielding safer, longer-lasting products. However, the market faces significant restraints, notably the high cost associated with premium filler products and specialized treatments, which limits accessibility for certain socio-economic groups, alongside persistent safety concerns related to counterfeit products and procedures performed by unqualified practitioners, necessitating stringent regulatory oversight and comprehensive consumer education.

Opportunities for market growth are abundant, particularly in geographical expansion into underserved regions like Eastern Europe and parts of Asia, coupled with product diversification into specialized areas such as body contouring and niche applications like correction of acne scarring and structural deficiencies. A pivotal opportunity lies in developing bio-stimulatory fillers that offer superior, long-term collagen regeneration capabilities, addressing the root causes of aging rather than just masking symptoms. The impact forces are generally positive, characterized by high market attractiveness driven by robust demand (Pull Force) and moderate competitive intensity, balanced by significant entry barriers related to regulatory approvals (Push Force), ensuring established players maintain a strong market position, while continuous innovation acts as a sustained upward force driving adoption and expenditure per patient.

These forces collectively shape a dynamic market environment where rapid innovation is essential for competitive advantage. The ability of companies to efficiently manage product safety profiles, obtain timely regulatory clearances, and establish comprehensive post-market surveillance systems significantly influences their trajectory. Furthermore, the rising investment in professional training and certification programs addresses the restraint posed by unqualified providers, thereby enhancing patient trust and expanding the consumer base safely. The synergistic effect of consumer demand, technological superiority, and professional skill enhancement ensures the sustained positive impact of these forces, projecting a resilient growth curve for the Injectable Skin Fillers Market despite intermittent economic volatilities.

The Injectable Skin Fillers market segmentation provides a granular understanding of the diverse product landscape and application spectrum that defines the industry. The market is primarily segmented based on the material type used in the filler, the specific cosmetic application, and the end-user setting where the procedures are performed. This structure highlights the dominance of Hyaluronic Acid (HA) fillers due to their biocompatibility and reversible nature, which are preferred for generalized facial volumizing and line correction. The segmentation by application clearly indicates a strong focus on core aesthetic procedures such as facial anti-aging and volume restoration, reflecting the major consumer drivers in the mature markets, while the end-user segment demonstrates the critical role specialized medical facilities play in the entire service delivery ecosystem.

Analysis of the Type segment reveals a growing competitive landscape where longer-lasting bio-stimulatory fillers (PLLA and CaHA) are increasingly challenging the traditional dominance of HA, especially for treating severe volume loss and deep structural defects where collagen induction is necessary for optimal results. In the Application segment, newer indications beyond routine wrinkle filling, such as hand rejuvenation and non-surgical rhinoplasty, are emerging as high-growth areas, broadening the market's scope and attracting a wider demographic seeking specific enhancements. Understanding these segment dynamics is crucial for manufacturers to tailor their R&D investments, target specific product formulations to niche applications, and optimize distribution strategies to align with the primary care delivery channels, thus ensuring maximum market penetration and efficient resource allocation.

The value chain for the Injectable Skin Fillers Market begins with the upstream procurement and processing of raw materials, primarily high-grade pharmaceutical ingredients like hyaluronic acid precursors, calcium compounds, or synthetic polymers, alongside specialized cross-linking agents and biocompatible carriers. This stage is critical as the purity, consistency, and source of these materials directly influence the final product's efficacy, safety, and shelf life. Significant focus is placed on sourcing high-purity, fermentation-derived HA to minimize immunogenic risks. Manufacturers then engage in complex R&D and proprietary formulation processes, utilizing advanced rheological science and specialized manufacturing techniques (e.g., homogenization, sterilization, packaging in pre-filled syringes) to create market-ready, sterile products suitable for human injection, establishing strong patent protections around proprietary cross-linking technologies.

The midstream section of the value chain involves regulatory compliance and market authorization across diverse geographical regions, which is a resource-intensive and often lengthy process due to the medical device classification of fillers. Following approval, the product moves through various distribution channels, which include both direct and indirect models. Direct distribution involves sales teams engaging directly with large hospital networks and key opinion leader clinics, ensuring controlled pricing and direct communication of product usage protocols. Indirect distribution utilizes specialized medical distributors, wholesalers, and third-party logistics providers (3PLs) who possess established networks within the aesthetic and dermatological communities, facilitating broader market reach, particularly in decentralized or regulated markets.

The downstream analysis focuses heavily on the end-users—Dermatology Clinics, Plastic Surgery Centers, and MedSpas—who administer the treatments. This phase is characterized by intensive professional training and continuing medical education, ensuring practitioners are proficient in injection techniques, complication management, and patient selection, which is vital for maintaining brand reputation and safety standards. The ultimate consumer (the patient) is influenced by marketing, practitioner recommendation, and clinical results. The feedback loop from the downstream patient experience back to the manufacturers informs future R&D cycles, particularly regarding durability, integration, and pain reduction, making the clinical application and post-market surveillance an integral part of sustaining product relevance and market growth.

The primary potential customers and end-users of injectable skin fillers are individuals seeking aesthetic enhancement, anti-aging solutions, or restorative treatments for facial structural deficiencies. The demographic profile is broad, historically dominated by women aged 35 to 65 seeking wrinkle correction and volume restoration; however, there is a significant and rapidly growing segment comprising younger adults (25-35) utilizing fillers for preventative aging measures, lip augmentation, and facial contouring (e.g., jawline definition), often influenced by digital media trends. Furthermore, the male aesthetic market is expanding, with men increasingly seeking subtle enhancements, jawline sculpting, and treatment for deep facial folds to maintain a competitive and youthful professional appearance, thus diversifying the core consumer base.

Institutional customers include a variety of specialized healthcare settings that procure and administer these products. Dermatology Clinics represent the largest buyer segment, due to their specialized focus on skin health and aesthetic procedures. Plastic Surgery Centers utilize fillers both independently and adjunctively with surgical procedures, providing comprehensive facial rejuvenation plans. MedSpas and licensed aesthetic centers are also major consumers, capitalizing on the increasing accessibility and convenience demanded by the mass market. These professional entities prioritize products based on safety profile, longevity of results, ease of use, and comprehensive professional support and training provided by the manufacturer.

Geographically, potential customers are concentrated in regions with high disposable incomes and strong cultural acceptance of cosmetic enhancement, particularly North America and Western Europe, although Asia Pacific, especially markets like China and South Korea, is rapidly closing the gap due to rising economic prosperity and the influence of K-Beauty standards globally. Manufacturers target these various customer groups—from the young, contour-seeking individual to the mature patient desiring volume restoration—through tailored product lines (different G’ prime, particle size, and viscoelasticity) designed for specific anatomical areas and aging concerns, ensuring the market addresses the highly individualized needs of its vast and evolving consumer base effectively.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 5.8 Billion |

| Market Forecast in 2033 | USD 11.0 Billion |

| Growth Rate | CAGR 9.5% |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Allergan (AbbVie), Galderma, Merz Pharma, Sinclair Pharma, Teoxane, Revance Therapeutics, Prollenium Medical Technologies, Ipsen, Suneva Medical, Laboratories Vivacy, Bioxis Pharmaceuticals, DR. Korman, SciVision Biotech, Zhejiang Jingjia Medical Technology, Huons Global, LG Chem, Bloomage Biotechnology, Cynosure (Hologic), Lumenis, Candela Medical |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological landscape of the Injectable Skin Fillers market is highly sophisticated, driven by continuous innovation aimed at optimizing filler rheology, enhancing integration into native tissue, and extending the duration of aesthetic correction. A core technology involves advanced cross-linking techniques, such as patented Vycross (Allergan) or OBT (Optimal Balance Technology by Galderma), used primarily for Hyaluronic Acid (HA) fillers. These technologies chemically bond HA molecules in specific ways to manipulate particle size, gel viscosity (G’ prime), and cohesivity. Higher cohesivity and specific cross-linking patterns allow the filler to resist degradation, provide greater lift capacity, and integrate more seamlessly into dynamic facial areas, leading to more natural-looking results and a longer residence time within the tissue. This refinement in structural engineering is crucial for differentiating premium products in a competitive environment.

Beyond HA optimization, significant technological effort is directed towards bio-stimulation and regenerative aesthetics. Fillers based on materials like Poly-L-Lactic Acid (PLLA) and Calcium Hydroxylapatite (CaHA) leverage proprietary micro-sphere and suspension technologies that initiate a controlled foreign body response, stimulating the body's natural production of collagen (neocollagenesis) over several months. Recent advancements in this area focus on reducing nodule formation risk through improved particle uniformity and suspension stability. Furthermore, delivery technology is evolving rapidly, with high-precision, low-volume syringes, specialized cannulas (blunt-tipped needles) designed to minimize vascular trauma and bruising, and integrated pressure sensors becoming standard tools, enhancing both safety and practitioner control during the injection process.

The integration of digital technology, including 3D volumetric imaging and AI-powered facial analysis, is also fundamentally reshaping the technology landscape by providing pre-procedural planning and outcome simulation. Manufacturers are increasingly incorporating proprietary local anesthetics, such as lidocaine, directly into their formulations to enhance patient comfort without compromising the stability or efficacy of the filler material. Future technology is expected to focus on fully biodegradable, customizable, smart fillers that can release growth factors or active pharmacological agents, thereby combining volume replacement with therapeutic benefits for enhanced tissue health and regeneration, marking a transition toward next-generation aesthetic biotechnology products.

The primary driver is the accelerating consumer shift towards minimally invasive cosmetic procedures, offering immediate results, minimal downtime, and lower risks compared to traditional plastic surgery. Continuous innovation in Hyaluronic Acid formulations, leading to safer and more durable products, further supports this market expansion, particularly driven by increased global aesthetic awareness and rising disposable incomes in emerging markets.

Hyaluronic Acid (HA) fillers hold the largest market share. This dominance stems from HA's exceptional biocompatibility, natural integration into the skin tissue, versatility for treating various facial areas (lips, cheeks, folds), and crucially, its reversibility with hyaluronidase, which provides an essential safety net for both practitioners and patients, making it the preferred initial choice for aesthetic corrections globally.

AI technology is expected to enhance precision and safety through advanced applications like 3D facial mapping and predictive analytics. AI algorithms can analyze individual facial anatomy and aging patterns to guide precise treatment planning, optimize injection placement, and potentially integrate with robotic systems to standardize micro-injection techniques, significantly improving consistency and personalized aesthetic outcomes.

The Asia Pacific (APAC) region presents the most significant growth opportunities, driven by economic prosperity, rapid urbanization, and a growing consumer demand for aesthetic enhancement, especially in countries like China and South Korea. Manufacturers are actively targeting this region through partnerships and localized product offerings to capitalize on the vast, untapped consumer base and favorable demographic shifts towards aesthetic treatments.

Key market restraints include the relatively high cost of premium filler treatments, which can limit accessibility for mass consumers, and ongoing concerns regarding safety risks associated with procedures performed by unqualified practitioners. Additionally, the proliferation of counterfeit or sub-standard products in some regions poses a significant challenge, necessitating stringent regulatory enforcement and increased consumer education on product authenticity and provider certification.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.