ID : MRU_ 433499 | Date : Dec, 2025 | Pages : 246 | Region : Global | Publisher : MRU

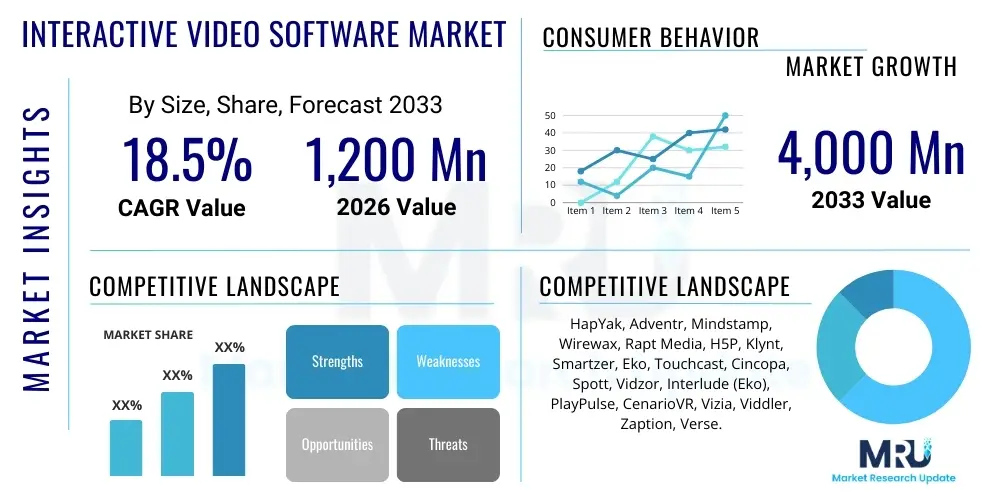

The Interactive Video Software Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 18.5% between 2026 and 2033. The market is estimated at USD 1,200 Million in 2026 and is projected to reach USD 4,000 Million by the end of the forecast period in 2033.

The Interactive Video Software Market encompasses platforms and tools designed to transform passive video content into engaging, actionable, and personalized experiences. This software enables the integration of clickable elements, branching narratives, quizzes, data input fields, and personalized pathways directly within the video stream, moving beyond linear consumption models. The core product revolves around sophisticated authoring tools, analytics dashboards, and robust integration capabilities with Customer Relationship Management (CRM) and Learning Management Systems (LMS). Interactive video is rapidly becoming a cornerstone technology for digital marketing, corporate training, e-commerce, and educational technology, driven by the need for higher viewer retention and measurable conversion rates, fundamentally changing how enterprises communicate complex information.

Major applications for interactive video span across several verticals, prominently including shoppable video for retail and e-commerce, personalized onboarding and training modules in corporate environments, and dynamic educational content that adapts based on learner input and performance. The software facilitates two-way communication, allowing viewers to dictate the direction of the content, which dramatically increases engagement metrics compared to traditional video formats. Furthermore, these platforms offer comprehensive analytics regarding viewer behavior, including click-through rates, decision points, and completion rates, providing marketers and educators with deep insights into content effectiveness and audience preferences.

The primary benefits driving market adoption include enhanced user engagement, improved data capture, superior personalization capabilities, and quantifiable return on investment (ROI) derived from higher conversion rates. Key driving factors involve the exponential growth of digital content consumption, the increasing demand for personalized marketing experiences (especially among Millennial and Gen Z consumers), and the technological advancements in streaming infrastructure that support seamless integration of interactive overlays and low-latency branching features. The shift towards remote work and digital-first education further accelerates the need for highly engaging and effective digital training and communication tools that interactive video software inherently provides.

The Interactive Video Software Market is characterized by rapid technological innovation, marked by a critical shift towards cloud-native platforms capable of handling massive viewer data and real-time decisioning. Current business trends indicate a strong move toward platform consolidation, where specialized interactive tools are being acquired or integrated into larger marketing technology (MarTech) and learning technology (LearnTech) stacks, aiming to offer seamless end-to-end content creation and distribution workflows. Furthermore, the embedding of Artificial Intelligence (AI) for automated personalization, dynamic content adjustment based on viewer profiles, and sophisticated behavioral analytics is establishing new competitive barriers. Companies are prioritizing solutions that offer robust API capabilities for integration with existing enterprise ecosystems, recognizing that stand-alone interactive video creation is insufficient without connectivity to data platforms.

Regionally, North America maintains market dominance due to early adoption across its robust e-commerce, media, and technology sectors, supported by significant investment in digital transformation initiatives. However, the Asia Pacific (APAC) region is projected to exhibit the highest growth rate, fueled by rapidly expanding mobile internet penetration, enormous consumer bases engaging with platforms like shoppable video, and aggressive government initiatives promoting digitalization in education and corporate training. Europe is also showing steady growth, driven by stringent data privacy regulations which necessitate localized and highly controlled interactive training and compliance content, requiring flexible software solutions.

Segment trends highlight the dominance of cloud-based deployment models, favored for their scalability, cost-effectiveness, and ease of access, particularly appealing to Small and Medium-sized Enterprises (SMEs). In terms of application, the marketing and advertising segment holds the largest share, as brands leverage interactivity to bridge the gap between awareness and conversion directly within the video asset. Conversely, the education and training segment is experiencing the fastest acceleration, driven by the realization that interactive simulations and adaptive learning pathways significantly improve knowledge retention and training effectiveness across diverse industries, from healthcare to heavy manufacturing. The rise of AR/VR integration within interactive video is also a notable trend, pushing the boundaries of immersive experiences.

User inquiries regarding the impact of Artificial Intelligence on the Interactive Video Software Market primarily revolve around themes of automation, hyper-personalization, and content scalability. Users frequently ask how AI can automate the complex branching logic required for interactive videos, reducing production time and costs. They are also highly concerned with AI’s role in real-time content modification—specifically, whether AI can dynamically insert personalized product recommendations, alter narrative paths, or adjust difficulty levels of quizzes based on viewer data ingested during playback. Key concerns center on maintaining content authenticity and creative control while maximizing AI-driven efficiency. Users expect AI to move beyond basic analytics and into prescriptive content generation and optimization, ensuring that interactive videos deliver optimal engagement and conversion rates tailored individually to millions of viewers simultaneously, thereby establishing a true one-to-one video marketing ecosystem.

The implementation of machine learning algorithms is fundamentally transforming the consumption and creation sides of interactive video. On the consumption side, AI analyzes subtle behavioral cues, such as cursor movement, hesitation points, and viewing duration of specific frames, to predict optimal moments for interaction or to suggest personalized next steps within the narrative. This predictive capability significantly enhances the relevance of the interactivity, preventing audience fatigue and maximizing click-through success. On the creation side, natural language processing (NLP) and generative AI are increasingly used to draft scripts for branching scenarios, categorize viewer responses, and even auto-generate alternative versions of video segments tailored for different demographic or geographic targets, drastically streamlining the production pipeline which traditionally required extensive manual effort for complex branching designs.

Furthermore, AI is crucial in maintaining the efficacy of interactive video across vast content libraries. AI-powered tagging and metadata generation ensure that interactive elements remain relevant even as underlying data structures evolve, improving searchability and content repurposing. The integration of AI-driven analytics allows for continuous optimization, where the system autonomously performs A/B testing on interactive placement, call-to-action designs, and narrative flow, providing concrete, data-backed recommendations to content creators. This evolution turns the interactive video platform into a dynamic optimization engine rather than just a passive delivery mechanism, signifying AI as the central force propelling the market toward truly adaptive digital communication.

The Interactive Video Software Market is propelled by powerful drivers centered on enhanced engagement metrics and quantifiable digital outcomes, while simultaneously facing resistance rooted in technical complexity and integration hurdles. The primary drivers include the universally recognized need for higher viewer retention in an attention-scarce digital environment and the critical shift in marketing strategy towards measurable, personalized experiences that directly lead to conversion (Drivers). Restraints are prominently characterized by the high initial cost of implementation and training associated with complex authoring platforms, alongside the significant challenge of integrating interactive video platforms seamlessly with diverse legacy enterprise systems (Restraints). Opportunities abound in the burgeoning demand for high-stakes interactive training simulations across regulated industries and the untapped potential of interactive content in the rapidly expanding Metaverse and spatial computing environment (Opportunities). These dynamics collectively shape the market structure and necessitate robust, user-friendly solutions that minimize the friction points associated with content creation and deployment.

Impact forces dictate the competitive intensity and operational demands within the market. Supplier power is moderate, concentrated among providers offering highly proprietary AI-driven features or extensive enterprise integration ecosystems, but softened by the availability of open-source components and modular service providers. Buyer power is increasing, particularly among large enterprises and media conglomerates who demand comprehensive platform features, scalability, and favorable long-term licensing agreements, pushing prices downward for commoditized features. The threat of new entrants remains relatively high due to the modular nature of software development, where specialized startups can offer niche interactive functionalities (e.g., specific overlay types or AR integrations). However, the high barrier to entry lies in establishing robust enterprise-grade security, scalability, and cross-platform compatibility necessary for widespread adoption.

Crucially, the threat of substitutes is moderate, primarily stemming from advanced static visual aids, sophisticated data visualizations, and highly engaging immersive technologies like high-fidelity VR experiences. However, interactive video maintains a competitive edge by offering a balance between production cost, accessibility (working on standard web browsers and mobile devices), and immediate analytical feedback, which substitutes often fail to match efficiently. The overarching force is technological innovation pressure, which compels existing players to continuously upgrade their platform capabilities, integrate emerging technologies like 5G-enabled low-latency streaming, and simplify the user interface for content creators, ensuring the software remains at the forefront of digital experience design and corporate utility.

The Interactive Video Software Market is broadly segmented based on Component, Deployment Mode, End-User, and Technology utilized. This structured segmentation allows for a detailed understanding of where market value is concentrated and where high-growth opportunities lie. The Component segmentation distinguishes between the core Interactive Platform, which handles creation and hosting, and the specialized Services, such as consulting, integration, and maintenance, necessary for enterprise deployment. Deployment Mode analysis highlights the decisive shift from traditional On-Premise installations to flexible and scalable Cloud-based solutions. Furthermore, End-User categories demonstrate the widespread application of the technology, with Marketing & Advertising leading adoption, followed closely by the rapidly evolving sectors of Education & Training and Media & Entertainment. The Technology segment reflects the innovative integration of advanced viewing technologies like 360-degree video, Virtual Reality (VR), and Augmented Reality (AR) overlays within interactive streams.

The value chain for Interactive Video Software is complex, spanning content acquisition, platform development, deployment, and customer engagement. The upstream segment involves crucial activities such as raw video content creation (filming, animation) and the development of the core software engine, including proprietary algorithms for interactivity, analytics, and rendering capabilities. Key upstream players are technology developers specializing in low-latency video streaming protocols, AI/ML developers for personalization features, and professional services firms that consult on large-scale platform architecture. The quality of the core platform infrastructure, particularly its ability to integrate with diverse data sources (CDPs, CRMs) and deliver seamless cross-device compatibility, determines the ultimate utility and value of the final product.

Midstream activities focus on the delivery, distribution, and customization of the interactive experience. This includes platform providers hosting the authoring environment and managing the Content Delivery Networks (CDNs) necessary for global, high-performance streaming. Distribution channels are varied, incorporating direct sales models where software vendors license their platforms directly to enterprises, and indirect channels relying on strategic partnerships with system integrators, digital marketing agencies, and specialized reseller networks. The preference for indirect channels is growing, particularly in international markets, as agencies often embed interactive video creation and management services within broader digital transformation projects for their clients, providing turnkey solutions.

The downstream segment centers on consumption, analytics, and ongoing optimization. This involves the end-user interaction with the video and the subsequent data harvesting and reporting capabilities offered by the software. Potential customers, ranging from major retailers using shoppable video to universities utilizing adaptive learning modules, rely heavily on the analytical dashboard provided by the software to derive actionable insights, justifying the software investment. Success in the downstream is measured by user experience, conversion rates, and the platform’s ability to generate prescriptive advice for content optimization, thereby closing the feedback loop and driving continuous improvement in interactive content effectiveness.

Potential customers for Interactive Video Software are diverse, spanning virtually every sector that relies on digital communication, training, or product demonstration. The primary end-users are large enterprises seeking sophisticated tools to enhance their digital marketing campaigns and internal knowledge dissemination strategies. Within the E-commerce and Retail sector, buyers are focused on reducing purchase friction and increasing cart size through embedded shoppable video experiences that connect product displays directly to checkout portals. These customers prioritize platform stability, speed, and seamless integration with existing inventory and payment systems.

Another major segment of buyers includes Chief Learning Officers and HR directors in regulated industries such as Healthcare, Finance, and Manufacturing. These customers purchase interactive video software specifically for high-stakes, compliant training, leveraging features like immersive 360-degree environments for safety simulations and branching narratives for ethical decision-making training. Their buying criteria emphasize robust security, audit trail capabilities, and native integration with established Learning Management Systems (LMS) to track regulatory compliance and certify employee proficiency effectively. The demand here is driven by the mandate to replace costly and inefficient in-person training with scalable, measurable digital alternatives.

Furthermore, the Media and Entertainment industry represents significant potential, with streaming services and content creators utilizing interactive video to drive subscriber engagement, offer personalized story choices, and monetize premium content through integrated micro-transactions or fan voting mechanisms. These customers prioritize features supporting complex narrative design, high-resolution streaming, and real-time audience interaction at massive scale. Overall, the market caters to any organization aiming to move from passive broadcasting to active, personalized digital conversations with their audience, irrespective of whether the goal is sales, education, or entertainment.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 1,200 Million |

| Market Forecast in 2033 | USD 4,000 Million |

| Growth Rate | 18.5% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | HapYak, Adventr, Mindstamp, Wirewax, Rapt Media, H5P, Klynt, Smartzer, Eko, Touchcast, Cincopa, Spott, Vidzor, Interlude (Eko), PlayPulse, CenarioVR, Vizia, Viddler, Zaption, Verse. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological core of the Interactive Video Software Market relies heavily on sophisticated web technologies and robust backend infrastructure optimized for real-time delivery and data processing. Crucially, platforms utilize HTML5 and JavaScript frameworks to create seamless, cross-browser compatible interactive overlays that function without interrupting the native video stream. Low-latency streaming protocols, such as WebRTC and specialized CDNs, are essential to ensure instantaneous delivery of subsequent video segments following a user's decision point, minimizing buffering delays that can break immersion. The underlying technology must also support extensive API integration to enable the fluid flow of data between the video platform and enterprise systems like Salesforce or Moodle, ensuring personalized content delivery and accurate data logging.

A significant trend in the technology landscape is the move towards immersive capabilities, requiring integration with graphics processing technologies and specialized rendering engines to handle 360-degree video and Augmented Reality (AR) overlays. For 360-degree interactive video, the software must manage spatial tracking and dynamic hotspot placement within the panoramic environment. Furthermore, the rising use of machine learning (ML) models is central for features like facial recognition (for emotion tracking in training), object recognition (for automated shoppable tagging), and predictive analytics, which optimize the interactive experience on the fly. The continuous development of codec standards (like AV1) aimed at higher compression and quality further supports the delivery of complex interactive content to mobile devices efficiently.

Platform vendors are also heavily investing in intuitive, no-code/low-code authoring tools. This shift in the technology design philosophy aims to democratize interactive video creation, moving it away from specialized programming teams and into the hands of marketing and learning professionals. This involves using drag-and-drop interfaces, pre-set templates, and visual flowcharts for mapping complex branching narratives. The focus on user experience in the authoring environment is a key technology differentiator, ensuring rapid content iteration and scalable production across large organizations without requiring significant external development resources. Security features, including DRM and enterprise-grade SSO capabilities, are also non-negotiable elements of the key technology stack for large corporate buyers.

North America currently holds the largest market share, driven by high digital content consumption rates, robust infrastructure (widespread high-speed internet), and the presence of numerous key technology providers and early-adopting enterprises, particularly in the e-commerce, media, and technology sectors. The region benefits from substantial corporate investment in sophisticated MarTech stacks and advanced corporate training initiatives. The U.S. market is a global benchmark for personalized and shoppable video content, necessitating advanced, high-scalability interactive software solutions. High purchasing power and a strong focus on data-driven marketing decisions further solidify its leading position, particularly in the B2B segment where interactive content is used for high-value sales enablement.

Canada and the U.S. lead innovation in applying AI to interactive video, focusing on automation of narrative flow and real-time audience segmentation. The demand is shifting towards solutions offering seamless integration with major cloud ecosystems (AWS, Azure, Google Cloud) and established CRM platforms. Regulatory requirements in sectors like finance and healthcare necessitate tools capable of creating highly customized, compliance-focused interactive training modules that provide detailed audit trails. The competitive landscape is mature, focusing on platform differentiation through superior analytics and ease of use in the authoring environment.

Europe represents a substantial and steadily growing market. Growth is primarily fueled by stringent data privacy regulations (like GDPR), which increase the need for highly localized and compliant training and internal communication tools. Interactive video is highly valued in the corporate sector for reducing travel costs associated with international training and ensuring standardized knowledge transfer across diverse linguistic and regulatory environments. Countries such as the UK, Germany, and France are leading adoption, especially in the automotive, pharmaceutical, and financial services sectors, where simulation and compliance training are mandatory and frequent.

The European market shows a strong preference for secure, on-premise, or highly controlled private cloud deployments, reflecting the region's focus on data sovereignty. While e-commerce adoption is robust, educational and professional development applications are key drivers. Partnerships between software vendors and local system integrators are vital for successfully navigating diverse national market requirements and integrating platforms with the multitude of unique legacy IT infrastructures present across the continent. The emphasis is often placed on multi-language support and culturally sensitive interactive design.

The APAC region is projected to register the highest CAGR during the forecast period. This exponential growth is driven by massive mobile internet penetration, rapid urbanization, and a burgeoning middle class eager for digital content, particularly in emerging economies like India, China, and Southeast Asia. Interactive video is revolutionizing local e-commerce, with shoppable live streams and short-form interactive content dominating consumer platforms. The educational technology (EdTech) sector is another major accelerator, as governments and private institutions invest heavily in scalable, distance learning solutions.

Challenges in APAC include diverse connectivity quality and language fragmentation, necessitating software solutions that are highly optimized for mobile delivery and capable of handling multiple complex scripts and localized payment methods within the video experience. Japan, South Korea, and Australia lead in technological sophistication, utilizing interactive video for cutting-edge gaming and media production, while emerging markets drive volume demand for basic, high-utility interactive marketing tools. The competitive environment is characterized by intense localized competition and a strong focus on platform affordability and mobile-first design philosophy.

These regions represent significant emerging opportunities. In LATAM, growing broadband access and increasing investment in digital infrastructure, particularly in countries like Brazil and Mexico, are boosting demand for cost-effective interactive marketing and corporate communication tools. The MEA region, particularly the GCC countries, is investing heavily in futuristic smart city projects and high-end educational institutions, driving demand for premium, immersive interactive video solutions, often tied to government-led digital transformation agendas. Adoption here is often characterized by leapfrogging older technologies, resulting in immediate demand for cloud-native and AI-enabled platforms.

The Interactive Video Software Market is projected to exhibit a high growth rate, forecasted at an 18.5% Compound Annual Growth Rate (CAGR) between 2026 and 2033, driven by the increasing need for measurable engagement and personalized digital content.

Interactive video enables two-way communication by integrating clickable elements, branching narratives, and data input fields directly into the stream, allowing the viewer to actively influence the content flow, unlike passive standard linear video.

The Marketing and Advertising segment currently holds the largest market share, leveraging interactive video primarily for shoppable campaigns, lead generation, and highly engaging product demonstrations that directly lead to higher conversion rates.

AI's primary role is to enable hyper-personalization, automating complex branching logic, and utilizing predictive analytics to adjust content elements in real-time based on individual viewer behavior and historical data, thereby optimizing engagement automatically.

The Cloud-based deployment model is dominating the Interactive Video Software Market due to its superior scalability, lower infrastructure costs, ease of maintenance, and ability to handle global content distribution efficiently, making it ideal for both SMEs and large enterprises.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.