ID : MRU_ 432634 | Date : Dec, 2025 | Pages : 257 | Region : Global | Publisher : MRU

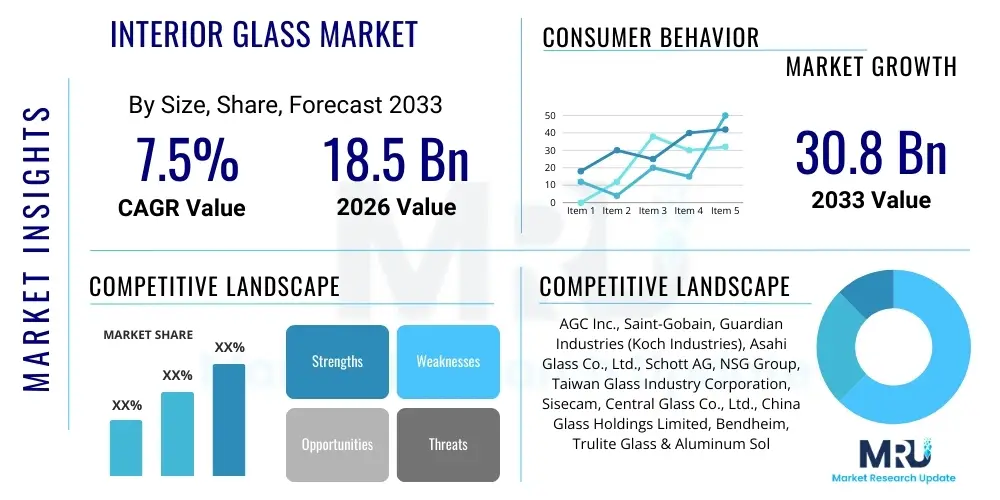

The Interior Glass Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 7.5% between 2026 and 2033. The market is estimated at USD 18.5 Billion in 2026 and is projected to reach USD 30.8 Billion by the end of the forecast period in 2033. This robust growth trajectory is primarily fueled by increasing urbanization, rising demand for aesthetic and functional partitioning solutions in commercial spaces, and the growing trend towards open-plan designs in modern residential architecture globally. Investment in smart building technologies and the adoption of high-performance glass products further contribute to this market expansion.

The Interior Glass Market encompasses the manufacture, processing, and distribution of various glass products specifically designed for indoor applications within commercial, residential, and industrial settings. These products include tempered glass, laminated glass, frosted glass, and specialized smart glass used in elements such as partitions, doors, railings, wall cladding, flooring, and decorative features. The primary function of interior glass has evolved significantly from mere transparent barriers to sophisticated design elements that enhance natural light penetration, improve spatial acoustics, and contribute to overall building energy efficiency and aesthetic appeal. The versatility and customization potential of glass—allowing for various textures, colors, and treatments—make it an indispensable material in contemporary interior design.

Major applications for interior glass span across diverse sectors. In the commercial realm, it is extensively used in corporate offices, hospitality establishments (hotels and restaurants), and healthcare facilities for creating modular meeting rooms, office partitions, shower enclosures, and highly durable surfaces. Residential applications primarily focus on enhancing luxury and openness, utilizing glass for balustrades, kitchen backsplashes, decorative wall panels, and internal doors, thereby maximizing the perception of space and light. The increasing consumer preference for sophisticated, low-maintenance, and hygienic materials is a critical driver supporting the sustained high adoption rate of interior glass products across both new construction and renovation projects.

The inherent benefits of utilizing interior glass, such as superior durability, ease of maintenance, light transmission capabilities, and aesthetic flexibility, strongly drive market growth. Furthermore, technological advancements have led to the introduction of specialized products like switchable glass (privacy glass) and anti-microbial glass, which address modern needs for privacy control and hygiene standards, particularly important in post-pandemic architectural planning. Supportive driving factors include stringent building codes mandating energy-efficient designs, increasing disposable incomes leading to higher investment in premium interior aesthetics, and the global trend toward sustainable architecture, where glass is often integral to maximizing passive solar gain and natural lighting.

The Interior Glass Market is characterized by dynamic business trends, marked by significant investment in R&D focusing on functional enhancements such as electrochromic and thermochromic glass technologies. Manufacturers are increasingly prioritizing sustainability, developing low-emissivity (low-E) coatings and incorporating recycled content to appeal to eco-conscious developers and consumers. A key business trend involves strategic mergers and acquisitions among major players aiming to consolidate market share, diversify product portfolios, and expand geographical reach, particularly into rapidly urbanizing economies in the Asia Pacific. Furthermore, the adoption of digital fabrication techniques, including advanced CNC cutting and printing on glass, is enabling higher customization and shorter lead times, revolutionizing the supply chain dynamics within the industry.

Regionally, the market exhibits varied maturity levels. North America and Europe currently represent high-value markets, driven by stringent energy efficiency regulations and a high penetration rate of smart building technologies. These regions demonstrate a strong demand for high-end, specialized products like acoustic insulating glass for commercial interiors. Conversely, the Asia Pacific region is anticipated to register the highest growth rate during the forecast period, fueled by massive infrastructure development, explosive growth in commercial real estate, and government initiatives promoting smart city development in countries like China, India, and Southeast Asian nations. Latin America and the Middle East and Africa are emerging markets, displaying potential growth driven by hospitality sector expansion and increasing luxury residential construction.

Segment trends reveal that the use of tempered glass dominates the market owing to its superior safety features and broad applicability in partitions and doors. However, the laminated glass segment is poised for rapid growth due to its enhanced security and soundproofing characteristics, making it preferred for high-traffic and noise-sensitive areas. By application, the commercial segment, particularly office spaces and retail, remains the largest consumer due to continuous demands for flexible and modern interior layouts. Simultaneously, the residential segment is showing accelerated growth, driven by affluent consumers adopting specialized glass products for aesthetic upgrades and incorporating minimalist design principles, focusing heavily on glass railings and feature walls.

Common user questions regarding the impact of AI on the Interior Glass Market frequently revolve around optimizing glass production efficiency, enhancing design capabilities, and integrating AI into smart glass applications. Users are primarily concerned with how AI-driven predictive maintenance can reduce operational downtime in manufacturing facilities, how machine learning algorithms can refine the quality control process for flawless glass finishes, and whether AI can personalize interior glass solutions more effectively for architects and designers. The key themes emerging from this analysis include expectations for streamlined supply chains, hyper-customization, and the development of intelligent interior environments where glass acts as a dynamic interface. Users anticipate AI will not only improve the manufacturing floor but also revolutionize the functional performance and interactivity of installed glass products.

In manufacturing, AI and machine learning are crucial for optimizing batch production, reducing material waste by simulating cutting patterns, and predicting equipment failure before it occurs, thereby enhancing overall equipment effectiveness (OEE). This integration allows glass manufacturers to manage complex production variables, such as furnace temperatures and cooling rates, with unprecedented accuracy, leading to superior material properties and lower production costs. Furthermore, AI systems are being utilized in automated quality inspection, using computer vision to detect microscopic flaws or structural weaknesses in finished panels far more rapidly and consistently than traditional human inspection methods, ensuring stringent safety and quality standards are met for interior applications like load-bearing floors and structural partitions.

From an end-user perspective, AI facilitates the rise of smart, responsive architectural glass. For instance, integrated sensors and AI processing units can dynamically control the opacity or tint of switchable glass based on ambient light conditions, time of day, or occupancy levels, optimizing energy consumption and maximizing occupant comfort. This intelligence transforms interior glass from a static material into an active component of the building envelope. AI is also powering sophisticated design software tools, allowing architects to visualize the optical and thermal performance of various glass types in real-time, expediting the design phase and ensuring that aesthetic goals align perfectly with functional requirements like sound attenuation and natural light maximization in large commercial projects.

The Interior Glass Market is significantly influenced by a complex interplay of Drivers, Restraints, and Opportunities (DRO), collectively forming the Impact Forces that shape its trajectory. Key drivers include the global shift towards aesthetically pleasing, light-filled architectural designs, the burgeoning demand for high-performance and safety-compliant glass (such as fire-rated and highly durable laminated glass) in public and commercial infrastructure, and the continuous growth of the global construction and renovation sectors. These drivers exert a strong, positive force, pushing innovation in glass treatments and finishes. The increasing adoption of green building standards and the desire for LEED-certified structures also act as powerful drivers, favoring glass products that enhance daylight harvesting and thermal efficiency, thus reducing overall building energy consumption and operational costs for end-users.

However, the market faces notable restraints. The high initial cost associated with specialized glass products, particularly smart glass and highly customized decorative glass, can deter price-sensitive consumers and developers in emerging markets. Furthermore, the inherent fragility and heavy weight of traditional glass necessitates careful handling and specialized logistics, contributing to higher installation costs and potential project delays. Regulatory hurdles and complex international trade policies regarding material sourcing and safety certifications also pose friction points for global market expansion. Volatility in the price of key raw materials, especially silica sand and processing chemicals, alongside energy-intensive manufacturing processes, represents a persistent economic restraint that challenges manufacturers' profit margins and pricing stability.

Opportunities within the market center around technological breakthroughs, particularly in the realm of coatings and functionality. The increasing penetration of smart glass, which offers dynamic privacy control and solar gain management, presents a substantial high-value growth avenue. Moreover, developing lightweight, highly durable alternatives, such as polymer-laminated and composite glass structures, offers solutions to mitigate transport and installation challenges. The rising trend of experiential retail and hospitality design creates continuous demand for bespoke, artistic glass installations (e.g., custom back-painted glass, etched mirrors, and sculptural glass features). Finally, expanding market penetration in emerging economies through the establishment of localized production facilities and improved distribution networks represents a primary strategic opportunity for leading global market players seeking long-term revenue growth and competitive advantage in new geographical areas.

The Interior Glass Market is comprehensively segmented based on product type, application, end-use sector, and technology. This segmentation provides a granular view of market dynamics, allowing stakeholders to identify high-growth segments and tailor their strategic investments. The product segmentation, covering basic safety glass (tempered and laminated), specialized glass (frosted, patterned, switchable), and decorative glass (colored, back-painted, mirrored), highlights the industry's shift toward functional aesthetics. The increasing complexity and performance demands placed on modern interiors have propelled the specialized and decorative segments to outpace traditional clear float glass growth rates, reflecting a consumer willingness to pay a premium for enhanced privacy, design uniqueness, and structural sound insulation properties within confined indoor spaces.

By application, the market is broadly divided into windows, partitions, doors, railings and balustrades, wall cladding, and others (including furniture components and flooring). Partitions and doors constitute the largest application area, driven by the modular design requirements of modern offices seeking flexible space management solutions. The fastest-growing application is observed in railings and balustrades, particularly in multi-story residential and commercial buildings, where glass offers unobstructed views and contemporary safety barriers. The end-use segmentation—covering commercial, residential, and industrial—shows the commercial sector maintaining market dominance due to higher consumption volumes in large-scale office, retail, and hospitality projects that frequently mandate specialized, high-specification glass for large architectural envelopes and internal division systems.

Geographical segmentation remains crucial, with high-demand regions like North America and Europe leading in adopting advanced glass technologies such as low-E coatings and acoustic laminated glass. Meanwhile, the Asia Pacific region dominates in terms of volume consumption, driven by sheer construction scale. Understanding these segments is vital for supply chain management, ensuring that manufacturing capacities are strategically aligned with regional regulatory requirements—for example, higher fire-rating specifications prevalent in certain European cities versus earthquake-resistant standards required in specific Asian locations. This detailed analytical segmentation underpins effective market entry strategies and targeted product development efforts across diverse consumer bases worldwide.

The value chain of the Interior Glass Market begins with upstream activities, primarily involving the extraction and processing of raw materials, such as silica sand, soda ash, and dolomite, necessary for manufacturing float glass. This phase is capital-intensive and highly dependent on global commodity prices and the energy market, as the melting process requires significant thermal input. Key upstream suppliers include mining companies and specialized chemical providers. Efficient upstream management focuses on securing consistent, high-quality material supply and implementing energy-efficient furnace operations to mitigate the substantial environmental and economic costs associated with primary glass production. Innovations at this stage often center on developing new formulations for stronger or lighter glass compositions.

Midstream activities involve the primary glass manufacturing (creating base float glass) followed by critical processing steps, including cutting, edging, tempering, laminating, insulating, and coating (such as applying low-E films or decorative finishes). This is the value-addition core of the market, where specialized equipment and intellectual property define competitive advantages. Fabricators and processors transform commodity glass into high-value interior products like safety partitions and acoustic panels. Quality control and precision engineering are paramount at this stage to meet strict architectural standards and client specifications. The midstream segment is characterized by increasing automation and the integration of digital tools to manage complex customization orders efficiently and accurately.

Downstream analysis focuses on the distribution channels and end-user installation. Products reach end-users through a combination of direct sales to large architectural firms and construction companies, and indirect sales via wholesalers, specialized glazing contractors, and retail suppliers for smaller residential projects. Direct channels offer greater control over product specifications and faster feedback loops, while indirect channels provide wider market reach and localized installation expertise. Specialized glazing contractors play a crucial role, often providing consultation, measurement, and precise installation services, which are critical given the high risk of damage during transport and fitting. Optimized distribution strategies, focusing on secure packaging and regional logistics hubs, are essential for ensuring timely and undamaged delivery of bulky and fragile interior glass systems.

Potential customers for the Interior Glass Market are highly diversified, encompassing sectors that prioritize aesthetics, functionality, safety, and energy efficiency in their built environments. The largest category of potential customers includes Commercial Real Estate Developers and Large Corporate Entities. These buyers procure substantial volumes of interior glass for new office buildings, retail complexes, mixed-use developments, and headquarters renovations, demanding high-specification products such as structural glass walls, acoustic partitions for meeting rooms, and decorative entrance systems. Their purchasing decisions are primarily driven by LEED certification goals, employee comfort, corporate branding, and the long-term maintenance costs associated with the glass solution.

Another major segment consists of the Hospitality and Healthcare sectors. Hotels, resorts, and high-end restaurants are significant consumers of decorative glass for lobbies, shower enclosures, mirrors, and custom bar tops, seeking luxury aesthetics and durability. Healthcare facilities require specialized glass, such as antimicrobial coatings and fire-rated glass for critical areas, balancing stringent hygienic standards with the need for light-filled, non-claustrophobic environments. These customers prioritize product longevity, ease of cleaning, and compliance with health and safety regulations above initial material cost, making them ideal buyers for premium, specialized glass solutions.

The Residential segment, comprising high-net-worth individuals, custom home builders, and multi-family housing developers, represents a rapidly growing customer base. Residential demand centers on luxury applications like frameless glass shower doors, custom kitchen backsplashes, interior glass stair railings, and large sliding doors that maximize natural light and create seamless transitions between indoor spaces. While budget constraints are more evident in the general residential market, the luxury residential segment frequently seeks highly customized, unique glass treatments, including digitally printed or etched glass, valuing design exclusivity and enhanced acoustic privacy provided by specialized laminated glass products.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 18.5 Billion |

| Market Forecast in 2033 | USD 30.8 Billion |

| Growth Rate | 7.5% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | AGC Inc., Saint-Gobain, Guardian Industries (Koch Industries), Asahi Glass Co., Ltd., Schott AG, NSG Group, Taiwan Glass Industry Corporation, Sisecam, Central Glass Co., Ltd., China Glass Holdings Limited, Bendheim, Trulite Glass & Aluminum Solutions, Oldcastle BuildingEnvelope, Vitro Architectural Glass, G&G Glass, Glazette, Glassolutions (Saint-Gobain subsidiary), Techno Glass, Fuyao Glass Industry Group Co., Ltd., Prelco Inc. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technology landscape of the Interior Glass Market is rapidly evolving, driven by the demand for enhanced safety, insulation, and interactivity. The foundational technology remains the Float Glass Process, which produces the flat, high-quality base glass used in almost all interior applications. However, significant innovations occur in post-processing. Tempering technology, which involves rapid cooling after heating, remains crucial for enhancing safety by creating glass that shatters into small, less harmful fragments. Lamination technology, utilizing interlayers like Polyvinyl Butyral (PVB) or SentryGlas Plus (SGP), is advancing to provide superior structural integrity, UV protection, and acoustic insulation, making it essential for high-rise interiors and sound-sensitive environments such as recording studios or executive offices. The refinement of these core safety technologies is continuous, focusing on increasing efficiency and reducing the thermal footprint of the manufacturing process.

A major technological frontier is the development and commercialization of Functional Coatings. Low-emissivity (Low-E) coatings, typically metal oxide layers, are applied to manage solar heat gain, which, while traditionally critical for exterior glass, is increasingly applied to interior glass partitions in thermally zoned buildings to prevent heat transfer between areas. More sophisticated functional coatings include anti-glare, anti-fingerprint, and highly resilient scratch-resistant finishes, vital for high-traffic interior surfaces like table tops and transaction counters. The precise application of these coatings, often through sputtering or pyrolysis, is a key area of competitive differentiation, allowing manufacturers to tailor glass panels for specific functional requirements such as reduced reflectivity in retail displays or enhanced durability in educational settings.

The most transformative technology influencing the market is Smart Glass, specifically electrochromic (EC) and Polymer Dispersed Liquid Crystal (PDLC) glass. EC technology allows the glass tint to be controlled electronically, optimizing light and heat transmission, while PDLC technology (Switchable Privacy Glass) instantly changes from opaque to clear, providing on-demand privacy, which is invaluable for conference rooms and healthcare examination areas. These technologies are increasingly integrated with Building Management Systems (BMS) and IoT platforms, allowing for automated responses based on environmental data and user schedules. The complexity lies in integrating the electronic components discreetly and ensuring long-term reliability and low power consumption, driving rapid innovation in thin-film deposition and miniaturized control electronics that are seamless with modern interior design aesthetics.

The most common types are tempered safety glass for structural integrity and laminated glass for enhanced sound insulation and security. Tempered glass is preferred in high-risk areas due to its safe shattering pattern, while laminated glass is chosen where superior acoustic performance and occupant safety from breakage are critical, such as executive offices or healthcare facilities.

Smart glass, including electrochromic and PDLC switchable glass, enhances functionality by providing on-demand privacy and glare control. These technologies allow users to electronically adjust the opacity or tint of interior partitions and windows, optimizing natural light, reducing energy consumption related to artificial lighting, and maximizing flexible space utilization within commercial and residential settings.

The key drivers in the Asia Pacific region are rapid urbanization, substantial investment in commercial and residential infrastructure development, and increasing disposable income leading to higher demand for aesthetically superior and modern building materials. Government initiatives focused on sustainable and smart city development also significantly accelerate the adoption of high-performance glass products.

Yes, acoustic performance is a critical factor, particularly in commercial and high-density residential buildings. Laminated glass, often with specialized acoustic interlayers, is widely adopted to mitigate noise pollution between offices, meeting rooms, or adjacent living units. Architects prioritize high Sound Transmission Class (STC) ratings to ensure occupant comfort and productivity.

Sustainability heavily influences the market through demand for glass products with low-E coatings to enhance energy efficiency, the incorporation of recycled content in manufacturing, and reduced operational waste. Manufacturers are also focusing on optimizing production processes to minimize carbon emissions and comply with green building certifications like LEED and BREEAM, promoting glass as a durable and recyclable material.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.