ID : MRU_ 433368 | Date : Dec, 2025 | Pages : 253 | Region : Global | Publisher : MRU

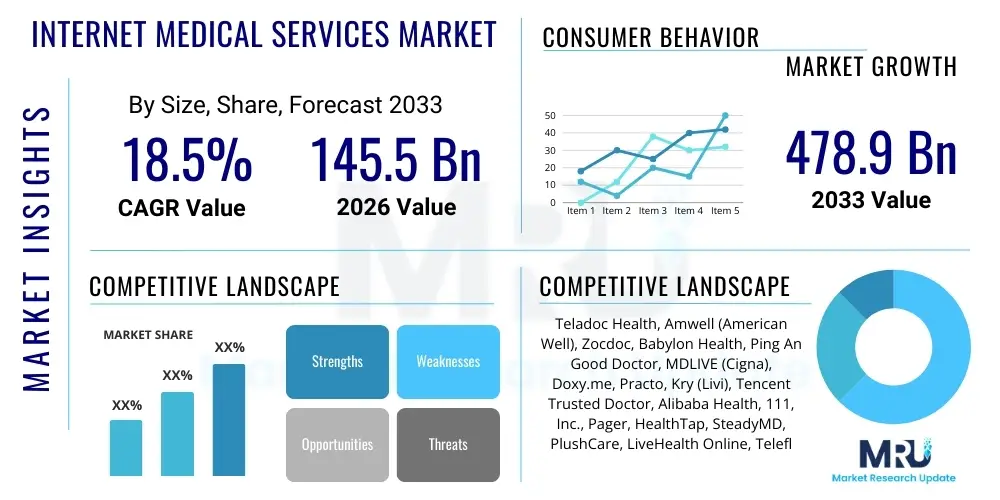

The Internet Medical Services Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 18.5% between 2026 and 2033. The market is estimated at $145.5 Billion in 2026 and is projected to reach $478.9 Billion by the end of the forecast period in 2033.

The Internet Medical Services Market encompasses a wide array of healthcare activities facilitated through digital communication platforms, offering remote access to medical expertise, data management, and preventative care. This domain includes services such as synchronous and asynchronous teleconsultation, remote patient monitoring (RPM), online prescription refills, digital health records management, and AI-powered diagnostic support tools. The core value proposition of these services lies in enhancing accessibility, reducing healthcare delivery costs, and improving patient engagement, particularly benefiting individuals in rural areas or those with mobility limitations. The integration of high-speed internet, 5G networks, and advanced wearable technology is fundamentally redefining the scope of remote care capabilities, pushing the market beyond simple video calls to comprehensive, data-driven health management systems.

Products within this sector are highly diversified, ranging from dedicated enterprise-level telehealth platforms utilized by large hospital systems to direct-to-consumer mobile applications focused on mental health or chronic disease management. Major applications span primary care consultations, specialist referrals, chronic condition management (e.g., diabetes and hypertension monitoring), radiology and pathology second opinions (teleradiology/telepathology), and post-operative follow-ups. The increasing prevalence of chronic diseases globally, coupled with aging populations, places immense pressure on traditional healthcare infrastructure, making scalable internet medical services an essential component of modern public health strategy. Furthermore, global events have accelerated regulatory acceptance and consumer adoption, solidifying these services as permanent fixtures rather than temporary supplements to conventional care.

Key benefits driving market adoption include significant cost savings for both providers and patients by minimizing facility overhead and travel time, improved efficiency through optimized scheduling and reduced wait times, and enhanced continuity of care through digitized health records and real-time data sharing. Driving factors are multifaceted, involving supportive governmental policies mandating telehealth parity, substantial venture capital investments into digital health startups, technological advancements in data security (e.g., blockchain for health data) and interoperability standards (FHIR), and growing consumer preference for convenience and personalized care delivery methods. These factors collectively create a robust ecosystem poised for sustained exponential growth.

The Internet Medical Services Market is undergoing a rapid transformative period, driven primarily by favorable shifts in regulatory frameworks, increased technological sophistication, and evolving consumer expectations regarding healthcare delivery. Current business trends indicate a strong focus on consolidation, with major telehealth platforms acquiring niche specialized service providers (e.g., mental health or RPM specialists) to offer integrated, end-to-end solutions. Furthermore, the market is witnessing the rise of hybrid care models, where physical clinics are seamlessly integrated with digital platforms, enhancing both the quality and flexibility of patient journeys. Investment is heavily concentrated on developing highly secure, user-friendly interfaces and systems capable of achieving true data interoperability across different healthcare providers and electronic health records (EHR) systems. This shift towards value-based care is propelling providers to adopt digital tools that demonstrate measurable clinical outcomes and patient satisfaction improvements, pushing away from simple fee-for-service remote appointments.

Regional trends highlight distinct growth vectors globally. North America, driven by high technology adoption rates, mature regulatory environments (especially post-pandemic policy changes regarding reimbursement), and substantial private insurance coverage, remains the dominant market shareholder. However, the Asia Pacific (APAC) region is projected to exhibit the highest Compound Annual Growth Rate (CAGR), fueled by massive populations, increasing internet penetration in developing economies, and proactive governmental initiatives in countries like China and India aimed at expanding primary care access through digital means. Europe is progressing steadily, focused heavily on cross-border data protection (GDPR compliance) and integrating digital services into nationalized healthcare systems, emphasizing remote patient monitoring for chronic disease management within publicly funded frameworks. Regulatory harmonization, particularly concerning licensing across state and national lines, remains a key regional barrier that must be addressed for sustained cross-regional service expansion.

Segmentation trends reveal Teleconsultation services maintaining the largest share, although Health Management and Remote Patient Monitoring (RPM) segments are experiencing the most accelerated growth. RPM, specifically, is benefiting from technological advancements that allow for continuous, high-fidelity monitoring of vital signs outside clinical settings, significantly reducing readmission rates and improving chronic care outcomes. In terms of platform, Mobile Applications are rapidly outpacing dedicated websites, driven by the ubiquity of smartphones and the capability of apps to seamlessly integrate with wearable devices and patient self-management tools. The End-User segment is seeing increased adoption by Large Hospital Systems and Integrated Delivery Networks (IDNs) that are implementing telehealth solutions as core components of their operational strategy, seeking efficiency gains and expanded geographical reach beyond their physical locations. This evolution underscores a strategic shift from telemedicine being an ancillary service to a foundational healthcare delivery method.

User queries regarding the intersection of Artificial Intelligence (AI) and the Internet Medical Services Market frequently revolve around three core themes: the safety and reliability of AI in diagnosis, its role in automating physician workflow, and the ethical implications concerning data privacy and algorithmic bias. Users commonly ask: "How accurate are AI diagnostic tools compared to human doctors?", "Will AI replace my primary care physician, or just assist them?", and "How is my personal health data protected when AI models analyze it?" These questions reflect a blend of excitement over efficiency gains and profound concern over clinical liability and patient-physician trust. The consensus expectation is that AI will revolutionize backend administrative tasks and initial triage/screening processes, thereby freeing up medical professionals to focus on complex decision-making and direct patient interaction, rather than outright replacement. However, widespread adoption hinges on regulatory validation of AI algorithms and demonstrable evidence of clinical efficacy that meets or exceeds human standards, requiring transparent, explainable AI models.

The strategic deployment of AI within internet medical services is rapidly moving beyond simple chatbot functions toward sophisticated machine learning models capable of processing vast amounts of patient data from disparate sources—including EHRs, real-time RPM data, and genomic information—to provide predictive analytics. AI algorithms are crucial for optimizing appointment scheduling, dynamically allocating medical resources, and identifying high-risk patients who require proactive intervention before complications arise. For virtual consultations, AI tools can transcribe physician-patient conversations in real-time, synthesize clinical notes, and instantly cross-reference symptoms against established clinical guidelines, significantly boosting efficiency and reducing administrative burden. Furthermore, AI is central to enhancing cybersecurity protocols, detecting anomalies indicative of data breaches or malicious activity, which is paramount in the highly sensitive digital health environment.

In the diagnostic and therapeutic realms, AI’s impact is transformative. Teleradiology and teledermatology benefit immensely from AI-powered image analysis, which can flag subtle abnormalities faster and with greater consistency than the human eye, accelerating the diagnostic pipeline. In mental health services delivered online, Natural Language Processing (NLP) is used to analyze patient sentiment and communication patterns, providing early warning signals for severe depression or suicidal ideation, thus enhancing the quality of remote psychological support. The major hurdle remains regulatory acceptance and establishing clear clinical pathways for AI-assisted diagnoses, ensuring accountability when errors occur. Successful integration requires robust governance frameworks that specifically address AI bias—ensuring models trained on diverse population data sets are equitable and applicable across various demographic groups accessing internet medical services globally.

The Internet Medical Services Market is propelled by powerful macro-economic and technological Drivers (D), while facing significant structural and regulatory Restraints (R), presenting substantial Opportunities (O) for innovation, all converging to form dynamic Impact Forces. The primary driver is the demonstrable cost-efficiency and convenience offered by remote care, coupled with favorable government regulations globally (especially concerning Medicare/Medicaid and private insurance reimbursement parity for telehealth). Technological acceleration, particularly the rollout of 5G networks providing ultra-low latency connections and the mass adoption of sophisticated wearable and IoT medical devices, further enables high-fidelity, real-time monitoring and consultation. The increasing global geriatric population and the corresponding rise in chronic disease burden necessitates scalable, non-facility-based care solutions, cementing internet medical services as a foundational public health tool.

However, market expansion is heavily constrained by inherent challenges, foremost among them being data privacy and security concerns, particularly compliance with stringent regulations like HIPAA in the US and GDPR in Europe. Interoperability remains a significant restraint; the lack of standardized communication protocols among disparate EHR systems, telehealth platforms, and wearable devices creates fragmented patient data silos, hindering seamless care transitions. Furthermore, digital literacy disparities, particularly among elderly populations and those in underserved communities, limit accessibility and adoption. Clinical liability and cross-state/cross-country physician licensing restrictions pose complex legal and logistical hurdles, delaying the scalability of services across geographical boundaries and increasing operational risk for providers attempting multi-regional deployment.

The market holds substantial opportunities arising from untapped specialized medical fields, such as highly personalized genomic medicine consultations delivered remotely, and the expansion into niche markets like virtual long-term care for nursing home residents. The transition towards value-based care models globally incentivizes the adoption of RPM and predictive analytics, creating strong commercial demand for integrated digital solutions that guarantee better outcomes and reduced costs. Impact forces are currently dominated by rapid regulatory acceptance, which drastically lowers the friction for market entry and service expansion. The post-pandemic sustained consumer expectation for digital convenience reinforces market penetration. Overall, while technology is ready, regulatory harmonization and robust cybersecurity infrastructure are the critical levers that will dictate the pace and extent of future growth. The market trajectory is one of inevitable high growth, contingent upon successfully navigating the complex web of privacy, licensure, and interoperability challenges.

The Internet Medical Services Market is fundamentally segmented across service type, platform technology, and end-user application, reflecting the diverse pathways through which remote care is delivered and consumed. The segmentation analysis reveals evolving market dynamics, where initial dominance by basic teleconsultation is gradually shifting toward more comprehensive, continuous care models enabled by advanced technological platforms. Understanding these segments is critical for stakeholders, as investment and innovation are increasingly targeted towards areas offering high patient engagement and measurable clinical return on investment, such as integrating AI into remote patient monitoring workflows to minimize false alarms and enhance data accuracy. This granular view allows providers to tailor service offerings to specific demographic or clinical needs, driving personalized healthcare delivery at scale.

The value chain for Internet Medical Services is characterized by a high degree of integration between technology providers and traditional healthcare entities, diverging significantly from conventional medical service delivery. The upstream segment involves critical infrastructure providers, including software developers specializing in telehealth platforms, cloud service providers (CSPs) managing data storage and processing (e.g., AWS, Azure, Google Cloud), and hardware manufacturers supplying IoT medical devices, cameras, and biometric sensors essential for remote monitoring. These entities establish the technological foundation, focusing heavily on scalability, security compliance (e.g., ISO 27001, HIPAA), and developing application programming interfaces (APIs) to ensure compatibility with existing Electronic Health Records (EHR) systems. Strategic partnerships at this stage are crucial for determining service quality and reliability, moving away from fragmented system architectures towards integrated digital ecosystems.

The downstream segment primarily consists of service delivery channels and end-user engagement points. This includes Direct Channels, such as proprietary telehealth platforms owned and operated by large healthcare providers (e.g., Mayo Clinic, Cleveland Clinic) or specialized direct-to-consumer companies (e.g., Teladoc, Amwell) that employ or contract their own physician networks. The Indirect Channels involve distribution through third-party intermediaries, notably insurance companies (payers) who integrate telehealth services into their benefit plans, or corporate wellness programs that offer digital health solutions to employees. Retail clinics and pharmacies are increasingly becoming physical access points for digital health services, offering hybrid care models where patients can connect virtually with a specialist from a local facility. Success in the downstream market depends heavily on effective marketing, robust consumer education, and seamless patient scheduling and billing processes that minimize administrative hurdles.

The key differentiator in the value chain is the emphasis on data utilization and security protocols embedded throughout all stages. Effective aggregation and analysis of patient data—captured remotely—is central to the value proposition, enabling preventive care and population health management. Direct and indirect distribution channels are constantly optimizing their patient acquisition strategies; direct providers rely on strong brand reputation and specialized service offerings, while indirect channels leverage existing patient or member databases to rapidly scale adoption. The shift toward value-based contracts is forcing tighter vertical integration, with technology firms increasingly partnering directly with payers and large provider organizations to offer bundled solutions that manage clinical risk and improve measurable health outcomes, demonstrating the increasing convergence of technology, clinical expertise, and financial risk management.

The potential customer base for the Internet Medical Services Market is exceptionally broad, encompassing virtually all sectors involved in healthcare delivery and consumption, but is primarily focused on three key areas: large Integrated Delivery Networks (IDNs) and hospitals seeking efficiency, chronically ill individuals requiring continuous monitoring, and national governments aiming to improve public health equity. Large hospitals and IDNs are major institutional buyers, leveraging these services to manage high patient volumes, reduce overhead costs associated with unnecessary Emergency Room visits, and extend specialist reach into remote or underserved catchment areas. They purchase enterprise licenses for platform integration, focusing on scalability and compliance features to ensure the platform can handle complex workflows like credentialing, billing, and system-wide EHR integration. Their purchasing decision is heavily influenced by the platform’s demonstrated ROI in reducing readmission rates and optimizing staff utilization.

The second substantial customer segment comprises individual patients and consumers, especially those managing chronic conditions (e.g., diabetes, cardiovascular disease, mental health issues) who require frequent, convenient access to their care teams without the burden of physical travel. This group adopts direct-to-consumer services like mobile teletherapy apps, remote patient monitoring subscriptions, and digital primary care providers. This segment is highly sensitive to user experience, cost transparency (out-of-pocket expenses), and the immediate availability of appointments. Furthermore, employers and corporations are increasingly becoming indirect customers by purchasing bundled digital health services as part of their employee benefits package, aiming to reduce sick days, improve employee productivity, and lower overall long-term healthcare expenditure through preventative digital wellness programs.

Finally, governments and military health systems represent significant institutional customers, particularly in regions where geographical barriers or limited infrastructure restrict access to traditional healthcare facilities. These entities procure digital health solutions for population health management, disaster response preparedness, and ensuring medical coverage for deployed personnel or residents in remote territories. Their procurement criteria emphasize robust security, the ability to operate effectively in low-bandwidth environments, and features supporting public health campaigns (e.g., virtual disease surveillance). The underlying need across all customer groups is the fundamental requirement for flexible, accessible, secure, and high-quality medical interaction, positioning internet medical services as a critical infrastructure investment rather than a supplementary technology.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | $145.5 Billion |

| Market Forecast in 2033 | $478.9 Billion |

| Growth Rate | 18.5% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Teladoc Health, Amwell (American Well), Zocdoc, Babylon Health, Ping An Good Doctor, MDLIVE (Cigna), Doxy.me, Practo, Kry (Livi), Tencent Trusted Doctor, Alibaba Health, 111, Inc., Pager, HealthTap, SteadyMD, PlushCare, LiveHealth Online, Teleflex, BioTelemetry (Philips), ResMed. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The foundational technology landscape for the Internet Medical Services Market is centered on five pillars: high-speed connectivity, cloud infrastructure, AI/ML capabilities, sophisticated data security, and seamless integration tools. The evolution of 5G and fiber optics is critical, enabling the transmission of large volumes of high-definition video and real-time biometric data necessary for detailed examinations and high-fidelity remote monitoring, minimizing latency and improving the clinical efficacy of virtual visits. Cloud computing platforms provide the necessary scale and elasticity for handling fluctuating patient loads and securely storing massive datasets, adhering to strict industry standards for redundancy and availability. Furthermore, the reliance on Software-as-a-Service (SaaS) models allows providers to rapidly deploy and scale telehealth services without significant capital expenditure on physical IT infrastructure, accelerating market penetration across smaller practices and specialized clinics.

Artificial Intelligence (AI) and Machine Learning (ML) algorithms are increasingly integrated to automate non-clinical administrative tasks, enhance diagnostic support, and personalize patient outreach. This includes natural language processing (NLP) for clinical documentation generation and conversational AI for initial patient triage and scheduling. The technology landscape is heavily influenced by the need for robust cybersecurity measures, particularly end-to-end encryption, multi-factor authentication, and blockchain technologies being explored for immutable patient data management, ensuring compliance with global privacy mandates. The integrity and security of the communication channel itself, often utilizing dedicated, encrypted video conferencing solutions (e.g., Doxy.me, Zoom for Healthcare), is non-negotiable for maintaining patient trust and regulatory adherence, driving continuous investment in advanced threat detection systems.

Interoperability technology, specifically the utilization of standards like Fast Healthcare Interoperability Resources (FHIR), represents a crucial technological focus. These standards facilitate the seamless, bidirectional exchange of patient data between disparate telehealth platforms, hospital EHRs (e.g., Epic, Cerner), and third-party applications, which is essential for comprehensive longitudinal care management and reducing the risk of clinical errors due to incomplete patient history. Wearable and IoT medical devices (e.g., continuous glucose monitors, smart scales, ECG patches) are fundamental to the Remote Patient Monitoring segment, requiring platforms capable of securely ingesting, normalizing, and analyzing high-frequency data streams. The market’s future depends on establishing standardized APIs and data normalization layers that allow these varied technologies to communicate effectively, moving from siloed data collection to unified digital health ecosystems that support holistic patient care.

The primary driver is the widespread implementation of favorable governmental and regulatory policies, particularly those ensuring reimbursement parity for telehealth services. This change, accelerated globally by public health necessities, has lowered the financial barrier to entry for providers and boosted consumer trust, making remote consultation economically sustainable and clinically acceptable.

RPM contributes significantly by shifting healthcare from reactive to proactive models. By utilizing wearable IoT devices to continuously collect vital signs, RPM reduces hospital readmissions, improves chronic disease management outcomes, and lowers the long-term cost of care, making it highly valuable in value-based reimbursement frameworks.

Major security concerns revolve around protecting sensitive Patient Health Information (PHI) from breaches and ensuring regulatory compliance (e.g., HIPAA, GDPR). Providers must invest heavily in advanced encryption, secure cloud storage, and robust authentication mechanisms to mitigate risks and maintain patient confidentiality.

The Asia Pacific (APAC) region is projected to exhibit the fastest CAGR due to vast, underserved populations, rapid digital infrastructure improvements (high mobile penetration), and aggressive governmental strategies in major economies like China and India to leverage digital health for expanding basic medical access.

No, AI is not expected to replace physicians entirely but will function as a powerful assistive tool. AI primarily automates administrative tasks, enhances diagnostic accuracy in areas like teleradiology, and optimizes triage, allowing human medical professionals to focus their expertise on complex patient cases and direct care delivery.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.