ID : MRU_ 433230 | Date : Dec, 2025 | Pages : 245 | Region : Global | Publisher : MRU

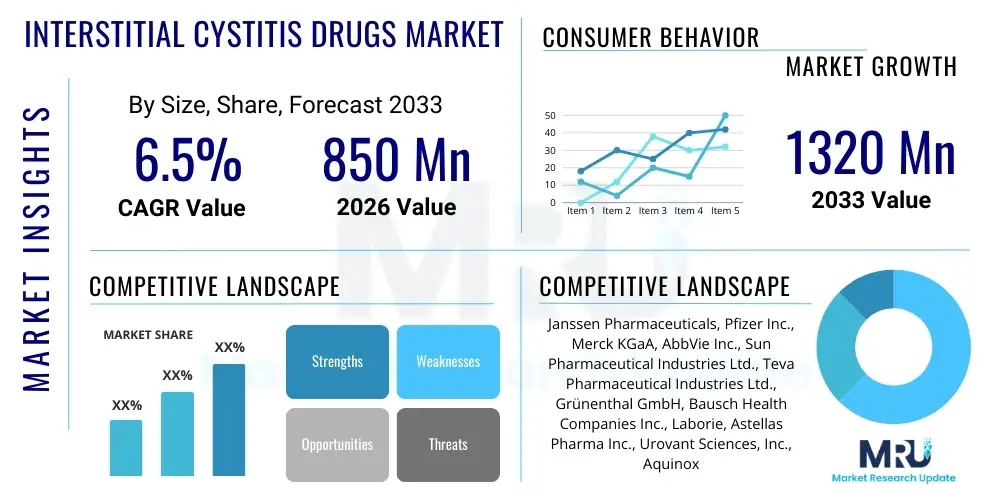

The Interstitial Cystitis Drugs Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.5% between 2026 and 2033. The market is estimated at USD 850 Million in 2026 and is projected to reach USD 1320 Million by the end of the forecast period in 2033.

The Interstitial Cystitis (IC), also known as painful bladder syndrome (PBS), drugs market encompasses pharmaceutical therapies aimed at alleviating the chronic pelvic pain, pressure, and urinary symptoms associated with this complex, non-infectious bladder condition. IC/PBS significantly diminishes the quality of life for affected patients, creating a substantial demand for effective symptomatic relief and disease modification. Current therapeutic modalities largely focus on repairing the compromised urothelial lining, modulating inflammatory pathways, and addressing central nervous system sensitization, utilizing a combination of oral medications, intravesical instillation therapies, and supportive care.

Key products dominating the market include Pentosan Polysulfate Sodium (PPS), the only FDA-approved oral drug specifically for IC, alongside off-label treatments such as tricyclic antidepressants (e.g., amitriptyline) for pain and mast cell stabilizers (e.g., hydroxyzine). The primary applications of these drugs are targeted symptom management, including reducing urgency, frequency, and pelvic pain, and improving overall bladder capacity and function. The persistent challenge of IC lies in its heterogeneous etiology and the often-limited efficacy of existing treatments, driving significant research interest toward novel, targeted therapeutics.

The market growth is primarily driven by the increasing global prevalence of IC, heightened clinical awareness leading to earlier diagnosis, and a robust pharmaceutical pipeline focusing on new mechanistic targets, such as neurogenic inflammation, specific cytokine signaling, and novel drug delivery systems like liposomal formulations. Furthermore, the rising adoption of personalized treatment algorithms based on patient phenotyping is expected to optimize therapeutic success rates, thereby fueling market expansion across major industrialized and emerging economies where healthcare infrastructure supports specialized urological care.

The Interstitial Cystitis Drugs Market is characterized by modest but stable growth, underpinned by high unmet clinical needs and the necessity for long-term symptom management in chronic sufferers. Business trends indicate a strategic pivot by pharmaceutical companies towards developing intravesical therapies that offer localized treatment with potentially fewer systemic side effects, focusing on agents like hyaluronic acid and chondroitin sulfate to repair the glycosaminoglycan (GAG) layer of the bladder. Furthermore, strategic alliances and licensing agreements focusing on Phase II and III compounds targeting specific inflammatory markers, such as P2X3 receptor antagonists, are becoming crucial for pipeline diversification and market entry for emerging biopharmaceutical entities navigating the complex regulatory landscape for chronic pain and inflammatory conditions.

Regionally, North America maintains its dominance due to high disposable income, established reimbursement policies, and sophisticated diagnostic infrastructure leading to higher reported incidence rates and accessibility to both standard and experimental therapies. Asia Pacific is emerging as the fastest-growing region, driven by improving healthcare expenditure, increased awareness programs addressing pelvic pain disorders, and the expansion of clinical trial sites focusing on diverse patient populations. Europe demonstrates steady growth, influenced by varied national healthcare system approaches to chronic pain management and differential access to specialized urological pain clinics, necessitating localized market access strategies.

Segment trends highlight the persistent reliance on oral therapies, especially PPS, despite ongoing concerns regarding long-term side effects and efficacy variability. However, the intravesical segment is gaining significant traction, favored by urologists for localized efficacy and reduced systemic burden, particularly in patients unresponsive to oral standard-of-care. The specialized clinics segment under distribution channels is pivotal, as IC diagnosis and treatment often require multidisciplinary expertise involving urologists, pain specialists, and gynecologists, driving substantial purchasing volume through specialized institutional pharmacies linked to these centers of excellence. The development of predictive biomarkers for identifying treatment responders remains a critical, overarching trend influencing future segment trajectories.

User inquiries regarding Artificial Intelligence (AI) in the Interstitial Cystitis (IC) domain predominantly center on its capacity to accelerate the identification of novel therapeutic targets, personalize treatment protocols based on patient-specific IC phenotypes, and optimize clinical trial design to reduce costs and timelines. Users are keen to understand how AI-driven machine learning models can sift through vast clinical and genomic data to distinguish true IC subpopulations (e.g., ulcerative vs. non-ulcerative, mast cell positive vs. negative), which is essential given the high heterogeneity of the disease. Furthermore, significant concerns revolve around the integration of AI tools for predictive diagnostics—specifically, using algorithms to analyze patient symptom diaries, urine proteomics, and cystoscopy images to facilitate earlier and more accurate diagnosis, thereby improving the timing and appropriateness of drug administration and potentially repurposing existing compounds for targeted IC subgroups.

The market dynamics are shaped by a complex interplay of clinical necessity, drug efficacy limitations, and regulatory hurdles, summarized by the forces of Drivers, Restraints, and Opportunities. The primary driver stems from the debilitating nature of IC, which necessitates continuous, chronic treatment for symptom management, coupled with a growing elderly population prone to chronic bladder disorders and increased global investment in pain and inflammation research. Restraints largely involve the controversial and sometimes limited efficacy of the current first-line oral therapy (PPS), concerns over long-term adverse effects, and the lack of truly disease-modifying agents that address the root causes of the disease, leading to high treatment drop-out rates and patient dissatisfaction.

Opportunities are significant, primarily residing in the development of targeted therapies based on advanced understanding of IC pathophysiology, specifically focusing on the purinergic system (P2X3 antagonists), mast cell stabilization, and nerve growth factor (NGF) inhibition. The high impact forces include the constant regulatory pressure for demonstrating superior efficacy and safety profiles over existing standards, the influence of specialized urological societies dictating treatment guidelines, and the economic burden of chronic IC management on healthcare systems, which pushes demand towards high-value, curative or highly effective symptomatic treatments.

These forces create a dynamic environment where investment is channeled into precision medicine approaches. For instance, the high rate of clinical failure in generalized IC trials acts as a restraint, but this simultaneously drives the opportunity to develop predictive biomarkers. The overall impact force matrix suggests that while generic competition for established oral drugs limits price growth, the high commercial potential of breakthrough biological or novel intravesical delivery systems designed to overcome GAG layer deficiency presents substantial future market momentum and premium pricing opportunities, shifting the focus from broad symptomatic relief to specific mechanism-based interventions.

The Interstitial Cystitis Drugs Market segmentation provides a granular view of therapeutic approaches, drug modalities, and key distribution channels influencing market dynamics. The market is primarily segmented by Drug Class, Route of Administration, Distribution Channel, and End-User. Drug Class segmentation includes PPS, Tricyclic Antidepressants, Antihistamines, and others (e.g., neuromodulators and investigational compounds). Route of Administration delineates between Oral and Intravesical methods, reflecting the fundamental clinical dichotomy in IC management. Distribution channels are critical, distinguishing between Hospital Pharmacies, Retail Pharmacies, and Specialty Clinics/Mail Order, while End-Users include Hospitals, Clinics, and Ambulatory Surgical Centers, reflecting the varied settings where IC treatment is initiated and maintained.

The value chain for Interstitial Cystitis drugs is characterized by high upstream R&D investment and a specialized, predominantly direct, downstream distribution system due to the chronic and often specialized nature of the treatment. Upstream analysis involves rigorous research into IC etiology, including target identification (e.g., identifying P2X3 receptors or specific mast cell profiles), active pharmaceutical ingredient (API) synthesis, and formulation development, which is particularly complex for intravesical agents requiring high stability and bioavailability within the bladder environment. Manufacturing is typically outsourced or managed internally by large pharmaceutical firms, focusing on Good Manufacturing Practice (GMP) compliance for both small molecules like PPS and complex biologics in the pipeline.

Downstream activities focus heavily on specialized clinical outreach and education. Given that IC is often misdiagnosed or under-diagnosed, pharmaceutical companies invest significantly in physician education (targeting urologists and pain specialists) and patient awareness campaigns. Distribution channels are dual: Direct sales to hospital pharmacies and specialized urology clinics are common for intravesical treatments and expensive biologics, ensuring proper handling and administration. Indirect channels involve retail and mail-order pharmacies for widely prescribed oral maintenance therapies like PPS or off-label antidepressants, providing convenience for long-term chronic management.

The distribution of IC drugs is sensitive to storage requirements and professional administration. Direct channels are preferred for drugs requiring professional monitoring (e.g., intravesical instillation kits). Furthermore, the role of payers (insurance companies and government health systems) is integrated into the downstream segment, as reimbursement policies heavily influence formulary inclusion and patient access, especially for high-cost novel therapies, completing the cycle from specialized R&D to patient access through managed care networks.

The primary end-users and buyers of Interstitial Cystitis drugs are healthcare providers and institutions specializing in urology, pain management, and pelvic floor disorders, who directly purchase the medications for administration or prescribe them to patients for retail fulfillment. Specifically, specialized Urological Centers and Hospital Systems are major customers, procuring bulk quantities of both oral and intravesical therapies for their inpatient and outpatient clinics, reflecting the high patient volume managed within these specialized environments. These institutions also serve as key decision-makers regarding formulary preference for novel intravesical solutions and high-cost biologics.

Furthermore, independent Specialty Clinics, particularly those dedicated to Chronic Pelvic Pain Management, represent a crucial customer segment. These clinics often utilize a multimodal approach, including drug therapy, physical therapy, and procedural interventions, making them consistent buyers of maintenance medications and localized pain relief drugs. Individual patients, acting through prescriptions fulfilled at Retail and Mail-Order Pharmacies, constitute the ultimate consumer base, driving demand for the long-term, accessible oral medications necessary for daily symptom control.

The procurement decisions are influenced by clinical efficacy data, ease of administration, safety profile, and, increasingly, the availability of comprehensive patient support programs offered by manufacturers. Since IC treatment is long-term, payers and managed care organizations, while not direct consumers, exert powerful buying influence through formulary inclusion and tiered co-payment structures, effectively channeling patient demand toward approved therapeutic options. Therefore, the successful marketing strategy must simultaneously target prescribing specialists, institutional purchasers, and payer organizations to ensure broad market penetration and sustained revenue generation.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 850 Million |

| Market Forecast in 2033 | USD 1320 Million |

| Growth Rate | CAGR 6.5% |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Janssen Pharmaceuticals, Pfizer Inc., Merck KGaA, AbbVie Inc., Sun Pharmaceutical Industries Ltd., Teva Pharmaceutical Industries Ltd., Grünenthal GmbH, Bausch Health Companies Inc., Laborie, Astellas Pharma Inc., Urovant Sciences, Inc., Aquinox Pharmaceuticals, Inc., Seikagaku Corporation, Sanofi S.A., Johnson & Johnson, Eli Lilly and Company, Actavis (now Teva), GlaxoSmithKline plc, Allergan (now AbbVie), Endo International plc. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological landscape in the Interstitial Cystitis (IC) drugs market is rapidly evolving, driven by the need to enhance localized drug delivery and identify patient-specific biomarkers for treatment stratification. A major technological focus is the optimization of intravesical instillation methods. This includes the development of sustained-release formulations, such as liposomes and hydrogels, designed to increase the residence time of therapeutic agents (like hyaluronic acid or heparin) within the bladder lumen. Extended contact time is crucial for repairing the damaged GAG layer and achieving prolonged symptom relief, representing a significant technical advancement over standard, rapidly diluted solutions.

Another pivotal technological area is precision medicine, utilizing advanced '-omics' technologies (genomics, proteomics, metabolomics) to identify specific molecular subtypes of IC patients. This involves developing diagnostic tools, often integrating machine learning, that can accurately classify patients based on their inflammatory profile, nerve growth factor levels, or mast cell counts. Such technological capability moves the field away from empirical treatment toward mechanism-based therapy, paving the way for targeted biologics that only benefit specific responder populations, thereby improving overall trial success rates and patient outcomes.

Furthermore, advancements in targeted drug development are critical. The landscape features novel small molecules and biologics that specifically inhibit pathways implicated in IC pain, such as the selective P2X3 receptor antagonists. These technologies aim to selectively block afferent nerve signaling in the bladder wall without causing systemic side effects. The complexity of synthesizing and stabilizing these targeted compounds, coupled with ensuring their effective, localized concentration in the bladder, defines the cutting edge of pharmaceutical technology in this challenging therapeutic domain, emphasizing sustained bioavailability and high target specificity.

The global Interstitial Cystitis Drugs Market displays significant regional variations in terms of prevalence, treatment protocols, and market maturity, largely dictated by healthcare infrastructure and access to specialized urological care.

North America (United States and Canada): This region dominates the global market share, primarily driven by a high awareness level among both the public and medical professionals, leading to robust diagnosis rates. The U.S. market benefits from extensive research and development activities, high per capita healthcare spending, and favorable reimbursement structures for both established drugs (like PPS) and novel, high-cost investigational therapies currently in late-stage clinical trials. The presence of major pharmaceutical innovators and a well-defined regulatory pathway contributes significantly to market growth. The regional trend is characterized by the rapid adoption of specialized intravesical delivery systems and targeted pain management strategies.

Europe (Germany, UK, France, Italy, Spain): Europe represents the second-largest market, exhibiting steady growth. However, market dynamics are fragmented due to diverse national health systems and varying reimbursement policies. Germany and the UK lead in market consumption due to robust specialized clinics and clear national guidelines for IC/PBS management. The emphasis in Europe is often placed on cost-effectiveness and generic alternatives for standard oral treatments, although there is increasing adoption of advanced hyaluronic acid and chondroitin sulfate instillation treatments for GAG layer repair. Regulatory harmonization efforts, such as through the European Medicines Agency (EMA), facilitate market entry for new therapies, though local pricing negotiations remain complex.

Asia Pacific (APAC) (China, Japan, India, South Korea): APAC is projected to register the highest CAGR during the forecast period. This accelerated growth is attributed to the rapidly improving healthcare infrastructure, rising disposable incomes, and increasing urbanization leading to better access to specialist care. Japan and South Korea are key contributors, having well-established domestic pharmaceutical sectors and clear clinical pathways. China and India, despite lower per capita spending, offer immense opportunities due to their vast populations, where undiagnosed IC cases represent a major untapped market. Market players are increasingly investing in clinical trials and distribution networks in this region to capitalize on the growing patient pool and emerging private health insurance sectors.

Latin America (LATAM) and Middle East & Africa (MEA): These regions hold smaller market shares but offer potential for growth, particularly in urban centers of Brazil, Mexico, and South Africa. Growth is constrained by limited specialized infrastructure, lower awareness, and challenges in affordability and reimbursement for high-cost specialty drugs. Market activity is typically concentrated around private sector hospitals and specialized centers serving affluent populations, with increasing generic consumption driving volume growth, while innovative therapies require robust market access strategies focused on direct institutional procurement.

The primary limitations stem from the heterogeneity of IC, meaning no single drug works for all patients, and the often non-specific mechanisms of current treatments like Pentosan Polysulfate Sodium (PPS). Furthermore, difficulty in accurate patient phenotyping and ensuring sufficient drug concentration at the bladder wall are significant biological and pharmacological challenges.

Intravesical instillation is positively impacting the market by offering localized treatment, leading to higher drug concentrations directly in the bladder, which is critical for GAG layer repair, while minimizing systemic side effects associated with oral medications. This preference drives investment into advanced delivery systems, such as liposomes and sustained-release hydrogels.

Novel targets focus heavily on modulating neurogenic inflammation and chronic pain pathways. Key areas include the inhibition of Nerve Growth Factor (NGF), antagonism of P2X3 receptors (involved in afferent nerve sensitization), and the modulation of mast cell function and specific cytokine signaling associated with bladder wall damage.

Personalized medicine is crucial. Future success relies on using biomarkers and machine learning (phenotyping) to classify IC patients into distinct subgroups based on underlying pathology (e.g., specific molecular inflammation markers). This allows pharmaceutical companies to design targeted clinical trials and prescribe mechanism-specific drugs, significantly increasing treatment success rates and optimizing resource allocation.

North America's dominance is attributed to high disease awareness, a robust infrastructure for specialized urological care, high disposable income enabling access to expensive specialty drugs, and efficient regulatory pathways (FDA) that facilitate the introduction and commercialization of innovative intravesical and novel biologic therapies.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.