ID : MRU_ 433791 | Date : Dec, 2025 | Pages : 242 | Region : Global | Publisher : MRU

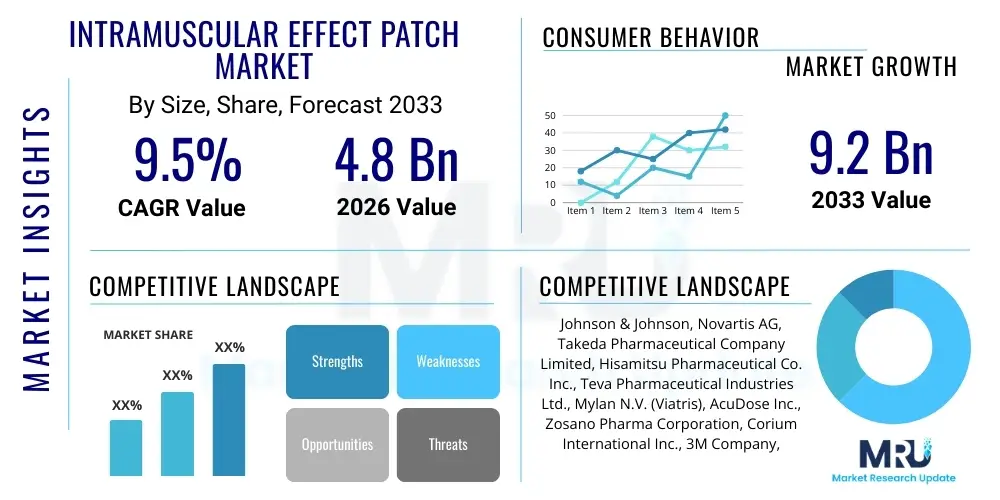

The Intramuscular Effect Patch Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 9.5% between 2026 and 2033. The market is estimated at USD 4.8 Billion in 2026 and is projected to reach USD 9.2 Billion by the end of the forecast period in 2033.

The Intramuscular Effect Patch Market encompasses specialized transdermal delivery systems designed to achieve therapeutic concentrations of active pharmaceutical ingredients (APIs) in deep muscle tissue or adjacent structures, mimicking the effects traditionally achieved through intramuscular injections, but via non-invasive means. These patches often utilize advanced technologies such as iontophoresis, micro-reservoirs, or sophisticated microneedle arrays (MNAs) embedded in a matrix to penetrate the stratum corneum and deliver drugs directly to the target muscle layers, fascia, or deeper subcutaneous tissue. The primary product goal is to provide sustained, localized drug release, minimizing systemic side effects while maximizing therapeutic efficacy at the site of injury or chronic pain.

Major applications for these sophisticated patches center around acute and chronic pain management, including conditions like severe back pain, osteoarthritis, rheumatoid arthritis, and sports-related muscle injuries such as strains and sprains. They are also increasingly being explored for the localized delivery of biologics, vaccines, and high-molecular-weight compounds that traditionally require needle administration. The convenience, reduced patient discomfort, and potential for self-administration offered by these patches are significantly contributing to their rising adoption across diverse healthcare settings, particularly in ambulatory care and rehabilitation clinics.

The market is predominantly driven by global demographic shifts, specifically the aging population facing increasing prevalence of musculoskeletal disorders, coupled with a surging preference for non-invasive drug delivery methods over conventional injections. Furthermore, advances in polymer chemistry, bioadhesives, and precise drug encapsulation techniques are enabling the development of patches capable of complex, multi-day dosing regimens, solidifying the patch as a viable, patient-preferred alternative for localized and deep tissue therapy. Regulatory approval pathways, although stringent, are increasingly accommodating these innovative systems, fostering rapid commercialization.

The global Intramuscular Effect Patch Market is experiencing robust expansion, fundamentally propelled by technological convergence in materials science and biotechnology, specifically the refinement of dissolvable and biodegradable microneedle technologies that enhance efficacy and patient compliance. Key business trends indicate a strong focus on strategic alliances and mergers between specialized patch developers and major pharmaceutical companies seeking to repurpose existing injectable drugs into convenient, differentiated transdermal formats. Furthermore, the shift towards home-based care and the increasing integration of smart patch technology—incorporating sensors for monitoring adherence and physiological responses—are transforming product value propositions across the competitive landscape.

Regionally, the Asia Pacific (APAC) region is projected to register the highest growth rates, driven by improving healthcare infrastructure, massive patient pools suffering from chronic pain, and relatively streamlined regulatory processes for novel medical devices in countries like China and India. North America and Europe, while mature, maintain dominance in terms of market value due to high healthcare expenditure, significant penetration of advanced therapies, and robust research and development activities focused on complex drug delivery systems, particularly those targeting localized chronic inflammation and neurological disorders.

Segment trends highlight the dominance of pain management applications, specifically patches delivering NSAIDs and local anesthetics, although the segment dedicated to specialized therapeutic agents (including peptides and small biologics) is forecast to exhibit the fastest CAGR. In terms of technology, microneedle patches (MNPs) are rapidly overtaking traditional passive patches due to their superior ability to breach the skin barrier and achieve effective deep tissue concentrations. End-user demand is heavily skewed towards hospitals and specialty clinics, though the fastest growing segment is expected to be home care settings, reflecting the increasing acceptance and simplicity of self-administered therapy.

Common user questions regarding AI's influence on the Intramuscular Effect Patch Market typically revolve around how artificial intelligence can accelerate the formulation and testing phases, optimize personalized dosing based on patient biodata, and streamline the highly complex manufacturing processes associated with microneedle arrays. Users are keen to understand if AI can predict the bio-distribution profile of drug payloads delivered via transdermal routes more accurately than traditional models, thereby reducing clinical trial timelines and costs. Furthermore, there is significant interest in AI's role in monitoring real-world patch efficacy and adherence through integrated sensor data, offering dynamic feedback loops to clinicians and developers, ensuring that these non-invasive solutions are optimally utilized for chronic condition management.

AI is profoundly impacting the Intramuscular Effect Patch sector, primarily through computational drug design and material science optimization. Machine learning algorithms are being employed to predict the optimal polymeric matrices, adhesive properties, and microneedle geometries required for specific drug permeation characteristics, drastically cutting down on the trial-and-error approach traditionally used in formulation R&D. This includes simulating the interaction between the patch components and biological tissues, optimizing the needle length and shape to maximize muscular penetration while minimizing pain, leading to highly customized, high-performance patches tailored for different anatomical locations and depth requirements. Additionally, AI-powered predictive maintenance is being implemented in advanced manufacturing facilities that produce high-precision microneedle stamps, ensuring quality control and consistency across billions of micro-structures.

The integration of AI extends into the post-market phase through advanced data analytics. Smart patches embedded with micro-sensors generate vast amounts of data pertaining to application duration, skin temperature, and patient movement. AI systems analyze this complex, longitudinal patient data to refine dosing protocols, identify patient subsets most responsive to patch therapy, and predict potential side effects before they manifest. This sophisticated data processing capacity transforms the patch from a static delivery mechanism into a component of a connected digital health ecosystem, enhancing the overall standard of care for chronic pain and rehabilitation applications.

The market dynamics for the Intramuscular Effect Patch are defined by a crucial balance between strong demand-side drivers, significant regulatory and technological restraints, and emerging opportunities in personalized medicine and specialized drug delivery. The primary driving force (D) is the overwhelming global burden of chronic musculoskeletal pain and the consequential demand for effective, localized, and non-opioid pain management solutions, coupled with the rising geriatric population requiring simplified dosing methods. Conversely, stringent regulatory scrutiny imposed by agencies like the FDA and EMA regarding the precise depth of penetration and consistency of drug dose delivered via novel transdermal methods acts as a substantial restraint (R), often lengthening the time-to-market for innovative products. The most significant opportunity (O) lies in leveraging these patch platforms for the delivery of high-value biologics and macromolecules, which currently rely almost entirely on intravenous or injectable routes, opening up vast, underserved therapeutic areas.

The impact forces influencing the market are multifaceted, combining factors related to healthcare cost-effectiveness, consumer preference, and scientific advancement. Cost-benefit analysis often favors patches over repeated clinical visits for injections, serving as a powerful accelerating force. However, resistance from traditional medical practitioners habituated to conventional injectable methods, alongside challenges in scaling up the precision manufacturing of complex micro-systems (like dissolvable MNAs) without compromising sterility and consistency, exert countervailing forces. Intellectual property protection for novel patch designs, particularly concerning proprietary drug stability within the patch matrix, also dictates competitive dynamics and market entry barriers, influencing overall market fragmentation and consolidation.

Ultimately, the market trajectory will be heavily dictated by the successful commercialization of next-generation patches that can reliably deliver large molecule drugs—a technical frontier that, if conquered, would exponentially increase the market’s scope. The convergence of wearables and therapeutic patches, enabling closed-loop drug delivery or real-time monitoring of therapeutic response, represents a major transformative force, pushing the market towards advanced digital health solutions rather than merely passive drug delivery systems. Success hinges on robust clinical evidence proving superior or equivalent efficacy to traditional intramuscular injections.

The Intramuscular Effect Patch Market is comprehensively segmented based on technology type, application area, and end-user, providing a granular view of market dynamics and identifying high-growth niches. Technological segmentation differentiates between passive diffusion patches, which rely on concentration gradients, and active transdermal systems, which utilize external energy sources such as electrical current (iontophoresis) or mechanical assistance (microneedles) to enhance penetration depth and rate. Application segmentation reveals the therapeutic areas driving demand, with pain management being the anchor, followed by niche segments like localized anti-inflammatory therapies and muscle spasm reduction. End-user categories reflect the deployment settings, ranging from high-volume clinical environments to the rapidly expanding realm of personalized home healthcare.

Microneedle patches currently hold significant promise and are expected to achieve the fastest segmental growth due to their ability to bypass the skin's barrier function reliably without causing significant trauma or pain, thus enabling the delivery of large molecules previously restricted to injections. Within applications, chronic pain management, particularly related to lumbar and cervical disorders, accounts for the largest revenue share, reflecting the high prevalence and long-term treatment requirements of these conditions. The market structure emphasizes the shift towards specialized patches designed for specific muscular groups or depth requirements, moving away from generic transdermal applications.

The value chain for the Intramuscular Effect Patch Market begins with upstream activities focused on advanced material sourcing and API synthesis, requiring specialized expertise in medical-grade polymers, hydrogels, bioadhesives, and pharmaceutical-grade active ingredients suitable for stable incorporation into a patch matrix. Key upstream components include precision polymer fabrication necessary for microneedle arrays and development of stable, potent drug formulations capable of extended release. Innovation at this stage is crucial, as the performance and safety of the final product are highly dependent on the quality and biological compatibility of the foundational materials. Strategic partnerships with specialized chemical and material science companies are essential for securing competitive advantage and maintaining supply chain resilience.

Midstream activities encompass the highly technical processes of patch manufacturing, assembly, and sterilization, where precision engineering, particularly in the creation of microneedle systems, is paramount. This stage involves sophisticated layering, drug loading, and packaging processes that must adhere to stringent GMP (Good Manufacturing Practice) standards to ensure dosage accuracy and device integrity. Following manufacturing, distribution channels are bifurcated: direct channels often involve selling high-value, prescription-only patches directly to large hospital systems or specialized clinics, whereas indirect channels utilize wholesalers, distributors, and pharmaceutical retailers to reach smaller clinics, pharmacies, and the growing segment of home care end-users. Regulatory compliance checks and quality assurance are integrated throughout the entire midstream process.

Downstream analysis focuses on market access, clinical acceptance, and patient engagement. Successful commercialization requires extensive marketing efforts targeted at pain specialists, orthopedic surgeons, and physiotherapists to drive prescription volume. Post-launch activities include continuous real-world evidence gathering and pharmacovigilance to monitor efficacy and safety, which is especially critical for novel delivery systems. The interplay between direct sales teams educating healthcare providers and indirect digital marketing efforts targeting patient self-administration strongly influences overall market penetration and revenue generation within this specialized therapeutic domain.

The primary customers for Intramuscular Effect Patches are institutions involved in high-volume patient care and individuals managing chronic conditions requiring localized, sustained therapeutic intervention. Hospitals and specialty pain clinics represent the largest institutional customer segment, purchasing patches for in-patient pain management, post-operative rehabilitation, and acute injury treatment where rapid, localized relief is necessary. These institutions prioritize products with proven clinical efficacy, ease of use for clinical staff, and cost-effectiveness compared to repeated injections or complex drug infusions. The patches serve as an ideal alternative for patients who may be needle-phobic or have conditions preventing frequent invasive procedures.

A rapidly expanding customer base includes Ambulatory Surgical Centers (ASCs) and Rehabilitation Centers. ASCs utilize these patches for managing localized pain following minor procedures, offering patients a non-systemic approach to minimize post-surgical discomfort and potentially reduce reliance on oral opioids. Rehabilitation centers focus on patients recovering from significant musculoskeletal injuries or strokes, where sustained, localized drug delivery assists physiotherapy and accelerates functional recovery. For these professional segments, reliability, dose control, and integration into existing treatment protocols are key purchasing criteria.

Furthermore, the end-user segment of home care settings and self-administering patients constitutes a critical growth area. These customers, often managing chronic conditions like lower back pain, knee osteoarthritis, or fibromyalgia, seek convenience, self-efficacy, and a reduction in clinical visits. The potential for the patch to deliver effective relief over multiple days, safely and discreetly at home, makes them highly attractive to patients committed to long-term pain management and active lifestyle maintenance. This segment is highly responsive to user-friendly design, clear instructions, and affordability relative to alternative therapies.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 4.8 Billion |

| Market Forecast in 2033 | USD 9.2 Billion |

| Growth Rate | 9.5% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Johnson & Johnson, Novartis AG, Takeda Pharmaceutical Company Limited, Hisamitsu Pharmaceutical Co. Inc., Teva Pharmaceutical Industries Ltd., Mylan N.V. (Viatris), AcuDose Inc., Zosano Pharma Corporation, Corium International Inc., 3M Company, Nitto Denko Corporation, Kindeva Drug Delivery, Vaxxas Pty Ltd., MicroDose Therapeutx Inc., Luye Pharma Group, Noven Pharmaceuticals Inc., Samyang Biopharmaceuticals, Nemaura Medical Inc., and DermTech Inc. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological landscape of the Intramuscular Effect Patch Market is dominated by innovations aimed at overcoming the primary biological barrier—the stratum corneum—to achieve reliable drug delivery into deep muscle tissue without systemic exposure. Microneedle Array (MNA) technology represents the forefront of this innovation. MNAs consist of micron-sized needles, often made from biocompatible polymers (like hyaluronic acid) or stainless steel, which painlessly pierce the skin's outermost layer. These MNAs can be solid, hollow, coated, or dissolving. Dissolving MNAs are particularly promising as they completely dissolve in the tissue, releasing the encapsulated drug directly into the interstitial fluid near the muscle, minimizing waste and disposal issues while ensuring precise dosing over a sustained period.

Beyond MNAs, active transdermal delivery methods such as iontophoresis and electroporation are crucial. Iontophoresis utilizes a mild electrical current to drive charged drug molecules across the skin barrier, enhancing the flux rate and allowing delivery of drugs that would otherwise struggle to penetrate. Electroporation, conversely, applies brief, high-voltage pulses to temporarily increase the permeability of the skin (creating transient aqueous pores), facilitating the transport of larger molecules. These energy-assisted approaches are complex but offer superior control over the onset and termination of drug delivery, making them suitable for potent or time-sensitive therapies requiring reliable deep tissue concentration.

Furthermore, significant research is dedicated to improving the foundational components of the patch, including advanced bioadhesives and reservoir designs. Next-generation adhesives must maintain strong adherence during vigorous activity (relevant for sports medicine applications) while remaining hypoallergenic and easy to remove. Drug encapsulation techniques, such as liposomes or polymeric nanoparticles, are integrated into the patch matrix to protect sensitive APIs, regulate their release kinetics, and ensure that the therapeutic window is maintained for the intended duration, which is essential for achieving a true intramuscular therapeutic effect over days or weeks.

The primary technical distinction is the utilization of advanced active delivery systems, such as microneedle arrays or iontophoresis, to ensure the therapeutic payload bypasses the skin barrier (stratum corneum) and reaches deep muscle tissue concentrations equivalent to or surpassing those achieved by traditional injection methods, providing localized, sustained effect.

Microneedle technology is highly significant, driving innovation and market growth by offering a minimally invasive, pain-free method to deliver large molecule drugs and achieve reliable deep tissue penetration, which is critical for treating chronic musculoskeletal and inflammatory conditions.

Chronic pain management, particularly for conditions like severe back pain, osteoarthritis, and other long-term musculoskeletal disorders, currently accounts for the largest revenue share due to the high global prevalence and the need for long-term, localized, non-opioid therapeutic solutions.

Regulatory hurdles primarily involve demonstrating reliable and consistent drug delivery depth, ensuring precise dosing accuracy throughout the entire wear period, and proving equivalence or superiority in efficacy and safety compared to established injectable drug protocols.

The Asia Pacific (APAC) region is projected to register the fastest compound annual growth rate, fueled by rapid expansion of healthcare access, increasing prevalence of chronic diseases, and growing investment in advanced medical technologies across major economies like China and India.