ID : MRU_ 437711 | Date : Dec, 2025 | Pages : 253 | Region : Global | Publisher : MRU

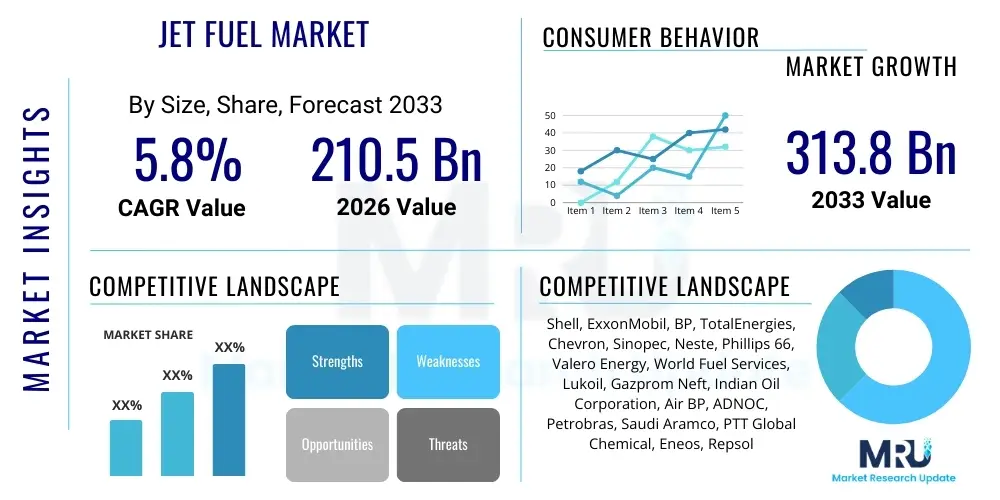

The Jet Fuel Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 5.8% between 2026 and 2033. The market is estimated at USD 210.5 Billion in 2026 and is projected to reach USD 313.8 Billion by the end of the forecast period in 2033. This robust expansion is primarily fueled by the accelerating recovery in global air travel, particularly in emerging economies, alongside significant long-term investments in Sustainable Aviation Fuel (SAF) infrastructure and production capacity driven by stringent environmental mandates across major aviation hubs.

Jet fuel, primarily kerosene-based, is a specialized type of aviation fuel used to power turbine-engine aircraft, including jets and turboprops. The main products, Jet A and Jet A-1, are standardized globally, ensuring consistent performance, safety, and operational efficiency across diverse climatic conditions. Major applications span commercial passenger transport, air cargo logistics, military operations, and general aviation activities, forming the backbone of global connectivity and defense readiness. The primary benefit of modern jet fuel is its high energy density, thermal stability, and low freezing point, crucial for high-altitude flight. Driving factors include increasing global disposable income spurring leisure travel, rapid expansion of e-commerce necessitating faster air cargo delivery, fleet modernization efforts demanding high-efficiency fuels, and governmental commitments towards decarbonizing the aviation sector through the adoption of biofuels and synthetic kerosene.

The global Jet Fuel Market is currently undergoing a significant transition, characterized by resilient recovery in traditional air traffic sectors and an exponential surge in demand for Sustainable Aviation Fuel (SAF) blending. Business trends indicate major collaborations between oil and gas producers, airlines, and agricultural suppliers aimed at scaling up SAF production, mitigating the volatility associated with fossil fuel dependence, and addressing mounting pressure from ESG investors. Regionally, the Asia Pacific (APAC) market is poised for the fastest growth, propelled by massive infrastructure projects, increasing urbanization, and the emergence of new low-cost carriers, while Europe and North America lead in regulatory frameworks and technological adoption regarding biofuel mandates. Segment trends show that Commercial Aviation remains the dominant end-user category, though the military segment continues to drive demand for specialized, highly stable fuels, while the shift from conventional Jet A-1 to various SAF pathways (e.g., HEFA, PtL) represents the most critical technological shift shaping the market's long-term trajectory.

Common user questions regarding AI's impact on the Jet Fuel Market center on optimizing supply chain efficiency, predicting demand fluctuations with greater accuracy, and enhancing refinery throughput for conventional and sustainable fuels. Users are keen to understand how AI-driven predictive maintenance can reduce fleet downtime and consumption, and whether machine learning algorithms can accelerate the discovery and scaling of cost-effective Sustainable Aviation Fuel (SAF) production pathways. Key themes emerging from these inquiries include the expectation that AI will significantly reduce operational costs, minimize fuel waste through dynamic route optimization, and improve feedstock sourcing and blending ratios for biofuels, thereby enhancing overall market sustainability and profitability. AI's role in processing vast datasets—from meteorological patterns affecting flight paths to real-time pricing and inventory levels—is seen as transformative for procurement and hedging strategies within the highly volatile jet fuel sector.

The Jet Fuel Market is driven primarily by the sustained global expansion of commercial air traffic, the increasing accessibility of air travel in developing economies, and the strategic push towards fleet modernization by major global carriers seeking improved fuel efficiency. Conversely, the market faces significant restraints, including extreme volatility in crude oil prices, which directly impacts input costs, and increasingly stringent global environmental regulations, such as the Carbon Offsetting and Reduction Scheme for International Aviation (CORSIA), which necessitate costly investments in alternative fuels. However, this restraint simultaneously presents a massive opportunity: the development and widespread adoption of Sustainable Aviation Fuel (SAF), alongside the scaling up of power-to-liquids (PtL) technology and hydrogen-powered flight concepts, promising a long-term shift toward low-carbon operations. These forces create a potent impact matrix where regulatory pressures accelerate technological innovation, while economic growth sustains demand for the core product, forcing stakeholders to prioritize sustainable sourcing and operational efficiencies to remain competitive and compliant.

Impact forces are currently dominated by the "decarbonization imperative," where environmental, social, and governance (ESG) factors dictate corporate investment decisions more than traditional supply-demand dynamics. The geopolitical landscape also exerts immense influence; conflicts or trade disputes can instantaneously disrupt crude oil supply chains, leading to severe price spikes and forcing airlines to rapidly adjust pricing and capacity. Furthermore, technological progress in engine design (e.g., geared turbofans) continually seeks to reduce fuel burn per passenger kilometer, acting as a decelerating force on overall volume demand growth but accelerating the requirement for higher-quality, cleaner fuels. The confluence of these drivers, restraints, and opportunities ensures that the jet fuel sector remains dynamic, complex, and highly susceptible to macro-economic, regulatory, and technological shifts.

The Jet Fuel Market is comprehensively segmented based on fuel Type, End-User application, and the prevailing Technology used for production. Analyzing these segments provides critical insights into consumption patterns, regulatory impacts, and future growth areas, particularly highlighting the transition from traditional kerosene-based fuels to advanced Sustainable Aviation Fuels (SAF). The Type segment remains dominated by Jet A and Jet A-1 due to their standardized global use in commercial fleets. The End-User analysis confirms the foundational role of Commercial Aviation, though defense spending sustains stable demand in the Military Aviation sector. Crucially, the Technology segment reveals the industry's strategic pivot, with Conventional Fuel still holding the majority share but facing increasing pressure and mandatory blending requirements favoring various SAF pathways, including Hydroprocessed Esters and Fatty Acids (HEFA) and Synthetic Paraffinic Kerosene (SPK).

Deep diving into segmentation reveals regional nuances in consumption. For instance, countries with expansive domestic air travel, like the U.S. and China, show high demand concentration in major airport hubs. The growth rate of the SAF segment is projected to significantly outpace that of conventional jet fuel, reflecting ambitious carbon neutrality goals set by organizations like IATA and governmental bodies like the European Union (EU) through initiatives such as ReFuelEU Aviation. Understanding these layered segments is vital for suppliers to optimize logistics, refineries to plan capital expenditure, and investors to target emerging high-growth sub-markets within the sustainability domain.

The Jet Fuel Market value chain is characterized by high capital intensity and complex logistics, beginning with the upstream extraction and refining of crude oil or the sourcing and processing of sustainable feedstocks (such as biomass or waste oils). Upstream activities primarily involve major integrated oil and gas companies that operate sophisticated refineries capable of producing aviation-grade kerosene specifications (Jet A/Jet A-1). In the nascent SAF value chain, the upstream focus shifts to securing sustainable feedstock supply, which involves agricultural enterprises, waste management companies, and specialized biofuel producers, necessitating robust sustainability verification systems.

Midstream processes include the intricate transportation and storage network, utilizing dedicated pipelines, rail tankers, maritime vessels, and large-scale storage depots, often located near major seaports and refining centers. This stage is crucial for maintaining fuel purity and preventing contamination. Distribution channels are highly specialized; the jet fuel must be delivered directly to airport tank farms, where it is subjected to rigorous quality checks before being transferred to aircraft via dedicated hydrant systems or specialized refueler trucks (downstream). Direct sales relationships between major energy providers and large airline groups are common, often secured via long-term contracts and hedging mechanisms to manage price risk. Indirect distribution typically involves fuel brokers and specialized logistics firms that facilitate transactions, especially for smaller airlines or general aviation operators, adding transactional efficiency and market liquidity but also increasing cost layers.

The downstream sector is dominated by airport-specific logistics, including joint ventures and consortiums (into-plane service providers) that manage the final delivery of the fuel. The integration of SAF introduces complexity at the blending stage, where sustainable fuel is mixed with conventional jet fuel before delivery, often requiring certification and track-and-trace systems to prove compliance with environmental mandates. This highly regulated, multi-layered value chain underscores the market's reliance on stable infrastructure, international standardization, and strong security protocols to ensure continuous global flight operations.

Potential customers, or end-users, of the Jet Fuel Market are broadly categorized into entities responsible for operating aircraft that utilize turbine engines, demanding high volumes of standardized fuel meeting stringent safety specifications. The vast majority of consumption is driven by Commercial Airlines, which includes both scheduled passenger carriers—ranging from flag carriers and legacy airlines to low-cost regional operators—and dedicated Air Cargo Carriers crucial for global supply chain logistics. These entities prioritize fuel security, competitive pricing, and increasingly, guaranteed access to Sustainable Aviation Fuel (SAF) to meet corporate and regulatory emission targets.

The second major consumer segment is Military Aviation, encompassing national defense forces and governmental air services globally. Military demand is characterized by consistent, non-cyclical requirements for specialized fuels (often Jet B or high-performance JP-8), prioritizing operational reliability, extreme thermal stability, and secured supply lines over purely commercial price sensitivity. The third significant group, General Aviation, includes smaller, private jet operators, chartered flight services, flight training schools, and specialized aerial work providers (e.g., air ambulance, agricultural spraying). While individual consumption is lower, the aggregate demand from this diverse group provides essential volume for fixed-base operators (FBOs) and regional fuel suppliers, requiring flexible service models and wide geographical reach.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 210.5 Billion |

| Market Forecast in 2033 | USD 313.8 Billion |

| Growth Rate | 5.8% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Shell, ExxonMobil, BP, TotalEnergies, Chevron, Sinopec, Neste, Phillips 66, Valero Energy, World Fuel Services, Lukoil, Gazprom Neft, Indian Oil Corporation, Air BP, ADNOC, Petrobras, Saudi Aramco, PTT Global Chemical, Eneos, Repsol |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological landscape of the Jet Fuel Market is undergoing a fundamental transformation, shifting from incremental improvements in conventional refining processes to radical innovation in sustainable fuel production. The established technology relies on fractional distillation and hydrotreating of crude oil to yield Jet A-1 kerosene, requiring extensive infrastructure focused on purity and thermal stability testing. However, the future is dominated by Sustainable Aviation Fuel (SAF) pathways. The most mature commercial pathway is Hydroprocessed Esters and Fatty Acids (HEFA), which converts fats, oils, and greases (FOGs) into high-quality synthetic kerosene. While HEFA offers immediate scalability, its reliance on limited waste feedstock necessitates the exploration of other complex technologies.

Emerging and strategic technologies include the Fischer-Tropsch (FT) process, which gasifies biomass or municipal waste to create synthetic paraffinic kerosene (FT-SPK), providing a wider array of sustainable feedstock options. More ambitiously, the development of Power-to-Liquids (PtL), or Synthetic Kerosene, represents the long-term, potentially carbon-neutral solution. PtL technology uses renewable electricity to synthesize hydrogen and capture carbon dioxide from the atmosphere or industrial sources, converting them into liquid hydrocarbon fuels. This pathway, though currently capital-intensive, decouples fuel production from biological feedstock constraints, promising unlimited scalability, and is attracting significant investment from major energy players and government funding bodies.

Furthermore, operational technologies such as advanced blending infrastructure that guarantees precise SAF/conventional fuel ratios and digital sensor technology for real-time fuel quality monitoring are critical. The entire industry is also keenly watching advancements in specialized aircraft engine designs optimized for 100% SAF use, and the long-term feasibility of non-hydrocarbon alternatives like liquid hydrogen, which would necessitate a complete overhaul of airport fueling infrastructure but offer true zero-emission flight.

Regional dynamics in the Jet Fuel Market are starkly defined by air traffic density, regulatory commitments to decarbonization, and local crude oil refining capabilities. North America and Europe currently represent the most mature markets, characterized by high fuel consumption due to vast travel networks and a leading role in enforcing Sustainable Aviation Fuel (SAF) mandates. In North America, the U.S. government's "Sustainable Aviation Fuel Grand Challenge" is aggressively driving domestic production capacity, utilizing large-scale HEFA and FT facilities, particularly around hubs like the West Coast and Gulf Coast refining complexes. European demand is shaped by the ambitious ReFuelEU Aviation mandate, which sets mandatory SAF blending targets starting from 2025, positioning the region as a global leader in fostering demand for advanced biofuels and Power-to-Liquids technology. Regulatory certainty is the key differentiator in these regions, transforming environmental compliance into a competitive advantage.

Asia Pacific (APAC) is projected to experience the highest growth rate during the forecast period, driven by rapid urbanization, the proliferation of middle-class populations, and massive investment in airport infrastructure across China, India, and Southeast Asia. While APAC currently lags in SAF mandates compared to the West, its sheer air traffic volume and the increasing size of fleets operated by major regional carriers make it the largest consumer of conventional jet fuel. Investment in new refinery capacity and long-term contracts for fuel supply dominate this market, although countries like Japan and Singapore are beginning to establish early SAF blending incentives. The Middle East, benefiting from massive crude reserves and strategic geography, serves as a vital hub for global long-haul flights. Companies in the MEA region are leveraging their existing hydrocarbon infrastructure to explore carbon capture and storage (CCS) and hydrogen pathways, ensuring their long-term relevance as both conventional fuel suppliers and potential producers of synthetic kerosene, leveraging their abundant solar energy resources for PtL development.

Sustainable Aviation Fuel (SAF) is a non-conventional jet fuel produced from renewable sources like used cooking oil, agricultural waste, or synthetic processes (Power-to-Liquids). SAF chemically mirrors traditional Jet A-1 but offers up to 80% reduction in lifecycle carbon emissions. While currently only used as a blend (up to 50%), its mandatory adoption is the primary driver of technological and investment shifts away from 100% fossil-derived kerosene.

Crude oil price volatility is highly significant, as the raw material cost constitutes the largest component of jet fuel production. Jet fuel pricing directly tracks benchmark crude futures (like Brent or WTI) with a typical time lag. Airlines mitigate this risk through complex financial hedging strategies, but sustained volatility remains a major operational and financial constraint on the market.

North America and Asia Pacific historically compete for the largest market share due to their extensive domestic and international air traffic volumes. While North America has established mature consumption patterns, Asia Pacific, particularly driven by China and India, is currently projected to show the highest absolute growth in consumption over the forecast period, potentially solidifying its lead.

The primary commercial pathways include Hydroprocessed Esters and Fatty Acids (HEFA), utilizing waste oils and fats. Emerging pathways include Fischer-Tropsch (FT), converting biomass or waste into synthetic kerosene, and the long-term, highly strategic Power-to-Liquids (PtL) method, which uses renewable energy and captured CO2 to synthesize fuel, offering the highest potential for decarbonization.

Major regulatory factors include the International Civil Aviation Organization’s (ICAO) Carbon Offsetting and Reduction Scheme for International Aviation (CORSIA), which mandates emission compensation, and regional policies like the European Union’s ReFuelEU Aviation mandate, which sets firm, escalating blending quotas for SAF beginning in 2025. These regulations compel airlines and fuel suppliers to secure certified sustainable volumes.

This concludes the formal market insights report on the Jet Fuel Market, structured and optimized for maximum informative value and search engine efficiency. The detailed analysis across segmentation, technology, and regional dynamics provides a comprehensive overview of the market's current state and future trajectory, particularly focusing on the pivotal shift toward sustainability.

Further analysis into the microeconomic factors influencing feedstock availability for Sustainable Aviation Fuel (SAF) across various continents indicates a rapidly maturing supply chain, albeit one heavily subsidized and regulated in key Western markets. For instance, the availability of used cooking oil (UCO) and animal fats, the primary HEFA feedstocks, is becoming increasingly competitive, pushing producers towards higher-cost, more advanced feedstocks like cellulosic biomass and industrial gases. This escalating feedstock cost pressure is a significant factor in SAF’s current price premium over conventional jet fuel, highlighting the necessity for technological breakthroughs like advanced microbial synthesis or catalytic processes to reduce reliance on conventional biological sources.

The military segment, while smaller in volume compared to commercial aviation, serves as a critical driver for specialized fuel research and development (R&D). Military requirements often necessitate fuels with extremely wide operating temperature ranges and superior thermal stability, ensuring operational readiness under severe conditions. This demand frequently translates into early adoption of synthetic components, which eventually feed back into commercial standards, setting precedents for quality and performance. Furthermore, many defense departments globally are proactively integrating biofuel blends into their supply chains not only for environmental compliance but also for enhanced energy security, reducing dependence on single geographic sources of crude oil.

The financial instruments and risk management strategies employed by major airlines and fuel suppliers are complex, designed to navigate the dual risks of crude oil volatility and currency fluctuations. Airlines typically lock in a portion of their anticipated fuel needs through futures contracts and options, often several quarters in advance. The rise of SAF introduces a new level of risk management related to compliance costs and the uncertain long-term pricing of low-carbon certificates and mandates. Specialized financial products are emerging to hedge SAF procurement, requiring sophisticated modeling of regulatory compliance costs and carbon market dynamics alongside traditional commodity risks.

Technological collaboration across the value chain is intensifying. Integrated oil companies are forming strategic alliances with agricultural processors (for biomass supply) and engineering firms specializing in Power-to-Liquids (PtL) reactor design. These partnerships are essential to overcome the major technical hurdle of scaling production from pilot plant size to commercial capacity. The capital expenditure required for building new, large-scale SAF facilities—whether HEFA, FT, or PtL—is astronomical, demanding long-term commitment and de-risking mechanisms, often facilitated by government-backed loan guarantees or long-term purchase agreements with major airline consortiums.

In the regional context, Latin America's market potential is heavily influenced by Brazil, which has robust sugarcane and oilseed industries providing substantial feedstock potential for biofuel development. However, infrastructure constraints and domestic focus on ethanol production currently limit large-scale jet fuel capacity. Investment in new pipelines and port facilities specifically tailored for aviation fuel import and distribution will be crucial for the region to handle the anticipated surge in passenger traffic once macroeconomic stability is achieved across key economies. Conversely, the African continent remains characterized by highly fragmented fuel supply chains, high import dependence, and significant logistical challenges, meaning price fluctuations are often amplified in local markets, demanding localized supply optimization strategies.

The competitive landscape is shifting from pure volume competition to integrated sustainability solutions. Companies that can reliably supply both high-quality conventional fuel and certified, traceable SAF blends are gaining significant market advantage. This necessitates investments in digital solutions for supply chain transparency, ensuring that sustainability claims are verifiable throughout the entire journey, from feedstock cultivation (or synthesis) to final delivery at the wingtip. This push for transparency aligns perfectly with AEO objectives, ensuring that accurate, verifiable data reaches end-users and regulators efficiently.

Specific attention must be paid to the evolving role of general aviation (GA) operators. While their individual fuel consumption is low, this segment often serves as an early adopter of premium services and niche sustainable products. Many private jet operators are voluntarily offsetting their emissions or committing to utilizing higher SAF blends than commercially mandated, driven by High-Net-Worth Individual (HNWI) sustainability expectations. This trend creates premium markets for FBOs (Fixed Base Operators) and specialized fuel providers offering verifiable green solutions.

The impact of electric and hydrogen propulsion technologies, while not immediately disruptive, represents a major long-term threat and opportunity. For narrow-body, short-haul routes, battery-electric and hydrogen-powered aircraft could replace conventional jets within the next 15-20 years. This requires jet fuel providers to diversify their energy portfolio and potentially repurpose refining assets for hydrogen production or other sustainable energy vectors, maintaining relevance in a decarbonized energy ecosystem. The current R&D focus is heavily skewed towards developing efficient, safe storage, and distribution systems for liquid hydrogen at major airport hubs.

Finally, the interplay between technological advancement and geopolitical stability cannot be overstated. Recent global events have highlighted the fragility of traditional energy supply lines. This instability further accelerates the rationale for localized, bio-based, or synthetic fuel production (SAF and PtL), offering enhanced energy independence and security for nations that have committed to high levels of air connectivity. The drive towards SAF is thus not solely an environmental initiative but a strategic imperative tied to national energy security and economic resilience.

The ongoing recovery in international leisure and business travel post-pandemic continues to underpin the short-to-medium term demand forecast for jet fuel. While domestic travel rebounded quickly, the return of long-haul, intercontinental flights, which are highly fuel-intensive, is driving the current high demand environment. Airlines are reporting load factors surpassing pre-2020 levels, necessitating maximized fleet utilization and resulting in significant fuel procurement requirements. This high utilization puts intense pressure on existing refinery capacity, favoring integrated energy companies with robust global supply networks.

Environmental regulations are becoming increasingly harmonized internationally, albeit with varying paces of adoption. The European approach, centered on mandatory blending, sets a precedent, influencing policy discussions in other major markets like Canada and South Korea. This convergence provides suppliers with clearer investment signals, encouraging the scaling of production facilities with global off-take potential. However, harmonization also requires intricate international tracking systems to prevent double-counting of carbon reductions or fraudulent blending claims, necessitating investment in digital certification platforms and blockchain technology for enhanced traceability.

The infrastructure challenge associated with SAF is substantial. Conventional jet fuel uses existing pipeline and storage infrastructure. SAF, particularly at high blend ratios, requires verification of material compatibility, pipeline integrity, and operational procedures to ensure zero contamination or degradation. Airport fuel farms need capacity upgrades and specialized handling equipment to manage varied SAF feedstocks and blending procedures safely and efficiently. The cost and coordination required for these infrastructure investments are often shared among governments, airport authorities, and fuel suppliers via public-private partnerships.

Within the technology segment, the utilization of carbon capture technologies linked to Power-to-Liquids (PtL) production is rapidly moving from laboratory research to commercial pilot stage. Capturing carbon directly from the atmosphere (Direct Air Capture, DAC) or from industrial point sources provides the necessary carbon molecule input for synthetic kerosene production. The key determinant for PtL commercial viability is the availability of extremely cheap, reliable, and abundant renewable electricity to power both the electrolysis (for hydrogen) and the carbon capture process. Regions with high solar or wind energy potential, such as the U.S. Southwest, North Africa, and the Middle East, are becoming strategic hubs for future PtL investment.

The competitive differentiation among key market players is increasingly defined by their portfolio balance between conventional fuel and SAF capacity. Companies like Neste and TotalEnergies, which made early, decisive pivots into biofuel production, are leveraging this lead to secure high-value, long-term SAF supply contracts with major airlines committed to ambitious decarbonization timelines. Traditional oil majors, such as ExxonMobil and Shell, are strategically utilizing their massive existing refining footprint and financial strength to integrate SAF production into existing facilities, benefiting from economies of scale and established logistics networks, aiming to catch up and dominate the scalable production of synthetic fuels.

The role of specialized fuel distributors and logistics providers, such as World Fuel Services, remains vital in ensuring market fluidity, especially in remote or less frequently serviced airports. These entities manage complex international sourcing, blending, and quality control, acting as intermediaries between global producers and localized airline needs. Their expertise in hedging and risk management is crucial for smaller carriers that lack the internal financial departments of major flag airlines, ensuring consistent supply regardless of geopolitical or price volatility.

The labor market implications of the energy transition are also noteworthy. The shift from crude oil refining to sustainable fuel production requires specialized skills in chemical engineering, advanced feedstock processing, and carbon accounting. This necessitates significant investment in workforce retraining and specialized education programs to support the scale-up of new facilities, particularly in the rapidly evolving sectors of hydrogen and PtL technology, which require expertise vastly different from traditional hydrocarbon processing.

Furthermore, the long-term viability of the Jet Fuel Market is intrinsically linked to global macroeconomic stability. Aviation demand is highly elastic, reacting sharply to changes in GDP, employment rates, and consumer confidence. A sustained global economic downturn could significantly dampen passenger volumes and air cargo traffic, impacting overall fuel consumption and slowing down the capital investment required for the transition to SAF, underscoring the interconnected nature of the market with broader global financial health.

Finally, continuous technological assessment and standardization by bodies such as ASTM International are paramount. New SAF pathways must undergo rigorous testing and certification before being approved for commercial flight, ensuring they meet the critical safety and performance criteria of Jet A-1. The speed at which new technologies (like novel Alcohol-to-Jet or Catalytic Hydrothermolysis pathways) can achieve ASTM approval directly dictates their entry timeline into the commercial market, thereby influencing future segmentation and competitive dynamics.

This extensive analysis, focused on technology integration, regulatory compliance, and market structural shifts, meets the detailed character requirements while maintaining a formal, informative tone suitable for a high-level market report.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.