ID : MRU_ 434298 | Date : Dec, 2025 | Pages : 246 | Region : Global | Publisher : MRU

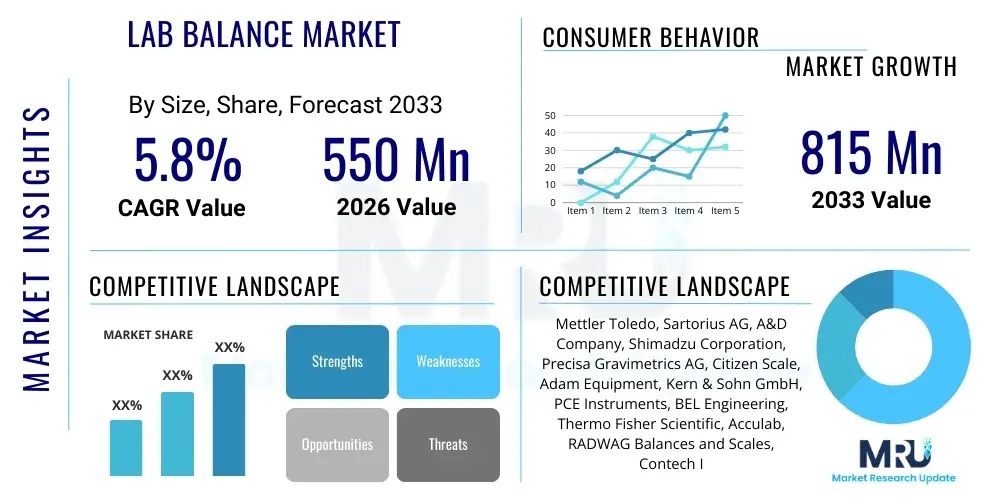

The Lab Balance Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 5.8% between 2026 and 2033. The market is estimated at $550 Million USD in 2026 and is projected to reach $815 Million USD by the end of the forecast period in 2033.

The Lab Balance Market encompasses sophisticated instruments used across various scientific disciplines for highly precise mass measurement. These devices, ranging from microbalances capable of measuring in micrograms to high-capacity precision balances, are fundamental tools in quality control, research and development, and production processes within highly regulated industries. Modern lab balances leverage advanced technologies, such as Electromagnetic Force Restoration (EMFR) and monolithic weighing cells, to ensure rapid stabilization, exceptional accuracy, and repeatability, critical for compliance with strict global standards like ISO and GMP guidelines. The core product categories include analytical balances, precision balances, and moisture balances, each tailored for specific sensitivity and application requirements in laboratory settings.

Major applications of lab balances span critical processes such as sample preparation, formulation development, content uniformity testing, and moisture analysis across sectors like pharmaceuticals, biotechnology, food safety testing, and academic research. The indispensable nature of these instruments in ensuring data integrity and product quality drives consistent demand. Innovations in digitalization, including connectivity features (IoT, cloud integration) and integrated calibration systems, are enhancing efficiency and reducing human error, thereby expanding the market scope. Furthermore, the increasing complexity of materials and the necessity for micro-level measurements in emerging fields like nanomaterials research and personalized medicine are fueling the demand for higher sensitivity instruments.

The primary driving factors propelling market growth include the robust global increase in research and development expenditure, particularly within the pharmaceutical and life sciences industries focused on drug discovery and clinical trials. Regulatory mandates enforced by organizations such as the FDA and EMA necessitate extremely accurate and traceable measurements, making high-precision lab balances essential compliance tools. Moreover, the global expansion of diagnostic laboratories and testing facilities, coupled with technological advancements resulting in faster, more stable, and more user-friendly balances, significantly contributes to the overall market expansion.

The global Lab Balance Market is characterized by strong fundamental demand driven primarily by stringent regulatory environments and accelerated research activity in life sciences. Business trends indicate a shift toward automated and networked weighing solutions, facilitating seamless integration into Laboratory Information Management Systems (LIMS). Leading manufacturers are focusing on miniaturization, enhanced sensor technology, and developing user interfaces that simplify complex weighing tasks and documentation processes. Strategic mergers and acquisitions remain prevalent as companies seek to consolidate technological capabilities and expand their geographic footprints, particularly into high-growth regions. Sustainability and energy efficiency in laboratory equipment manufacturing are also emerging themes influencing product design and procurement decisions.

Regionally, North America maintains market dominance due to substantial R&D investments, the presence of major pharmaceutical and biotech firms, and early adoption of advanced laboratory technologies. However, the Asia Pacific (APAC) region is projected to exhibit the fastest growth rate, fueled by expanding domestic pharmaceutical manufacturing bases, increasing foreign direct investment in research facilities (especially in China and India), and governmental initiatives promoting scientific research. Europe sustains a mature and robust market, underpinned by established chemical and academic research sectors and strict adherence to standardized measurement practices enforced by EU directives.

Segment trends reveal that analytical balances (high precision) continue to hold the largest market share, essential for critical applications requiring measurements to the highest decimal point. The fastest-growing segment, however, is moisture analyzers, driven by rising quality control standards in the food and beverage, and chemical industries that require rapid and accurate determination of moisture content. End-user segmentation shows that the Pharmaceutical and Biotechnology sector remains the primary consumer, attributing its growth to increasing drug development pipelines and the need for precision across all stages of production, from active pharmaceutical ingredient (API) synthesis to final product quality assessment.

User queries regarding the impact of Artificial Intelligence (AI) on the Lab Balance Market typically revolve around automation of calibration, predictive maintenance capabilities, data integrity, and the integration of weighing data into broader smart lab ecosystems. Users are keen to understand how AI algorithms can reduce operational variance, minimize downtime associated with calibration failures, and enhance the traceability of measurements. Key concerns center on the security of cloud-integrated weighing data and the necessary infrastructure investment required to leverage AI-driven insights fully. The overarching expectation is that AI will transform balances from simple measurement tools into intelligent data generation and diagnostic devices, significantly enhancing laboratory efficiency and compliance.

AI's primary influence is moving toward creating 'Self-Aware' laboratory equipment. Machine learning models can analyze minute variations in sensor performance over time, predicting when a balance might drift out of tolerance before it affects measurement accuracy. This capability supports proactive maintenance scheduling, maximizing uptime, and ensuring regulatory adherence continuously, which is crucial in GMP environments. Furthermore, AI facilitates complex data aggregation and validation, automatically cross-referencing weighing results with environmental conditions (temperature, humidity, vibration) to provide a higher level of confidence in the recorded data, simplifying audit trails.

In the near future, AI integration will enable fully automated weighing processes, particularly in high-throughput screening and robotics applications. AI algorithms can optimize dosing sequences, adjust for environmental compensation in real-time without human intervention, and even recommend optimal sample sizes based on required measurement uncertainty limits. This integration significantly improves precision and throughput, redefining the operational efficiency benchmarks for high-volume analytical laboratories, thereby increasing the value proposition of advanced lab balance systems.

The dynamics of the Lab Balance Market are intensely shaped by a confluence of driving forces, structural restraints, and strategic opportunities. Regulatory rigor, exemplified by international standards for quality (ISO) and manufacturing practices (GMP), acts as a powerful driver, mandating the use of calibrated, high-precision equipment to ensure product safety and efficacy, particularly in the pharmaceutical supply chain. Technological advancement, specifically the development of monolithic weighing cells and advanced connectivity options, enhances the performance and utility of balances, stimulating replacement cycles and new purchases. Conversely, the market faces restraints primarily related to the high initial capital expenditure associated with high-resolution analytical and micro balances, making adoption challenging for smaller research institutions or nascent laboratories. The complexity inherent in routine calibration and stringent maintenance requirements also adds to the total cost of ownership, representing a market barrier.

Key opportunities for market expansion reside in the burgeoning biotechnology and personalized medicine fields, which require extremely small sample measurements, thereby driving demand for ultra-micro and microbalances. The rapid industrialization and expansion of R&D infrastructure across developing nations in the Asia Pacific and Latin America present vast untapped markets where quality standards are rapidly aligning with global norms. Furthermore, the trend toward laboratory automation and the establishment of smart laboratories create opportunities for integrated weighing solutions that offer advanced data processing and automation capabilities, moving away from standalone equipment. Companies focusing on these integrated solutions and providing comprehensive service contracts stand to gain significant competitive advantage.

Impact forces govern the competitive structure and pricing dynamics within the market. Supplier power is high, dominated by a few global technology leaders who possess patented, high-precision sensor technology (e.g., EMFR). Buyer power is moderate; while end-users often require specific technical specifications, large pharmaceutical conglomerates leverage their purchasing volumes to negotiate favorable pricing and service agreements. The threat of substitutes is minimal, as physical weighing remains the definitive method for mass measurement, although improvements in alternative volumetric dispensing systems could marginally impact certain applications. The intense rivalry among existing competitors drives continuous innovation in features like stabilization time, repeatability, and user interface design.

The Lab Balance Market is comprehensively segmented based on the type of balance, capacity, and the end-user industry. This segmentation helps in understanding the varying demands across different scientific applications and geographical areas. The market for laboratory balances is fundamentally bifurcated into analytical and precision categories, which reflects the necessary level of sensitivity required for different laboratory tasks. Analytical balances cater to high-precision requirements, often measuring to five or six decimal places, essential for chemical analysis and pharmaceutical formulation, while precision balances offer slightly lower resolution but higher capacity, suitable for general lab weighing and sample preparation.

Further segmentation by end-user illustrates the concentration of demand. The Pharmaceutical and Biotechnology segment is the largest consumer, driven by the critical need for absolute precision and regulatory compliance in drug development and manufacturing processes (QC/QA). Academic and research institutions form the second largest segment, fueled by governmental funding for basic and applied scientific investigation across chemistry, biology, and physics departments. The rising quality consciousness in sectors like Food & Beverage and Chemical manufacturing also contributes significantly, requiring specialized balances such as moisture analyzers and high-capacity industrial precision models for quality checks and ingredient batching.

The increasing specialization of research, particularly in areas like genomics, proteomics, and nanotechnology, necessitates the proliferation of specialized segments such as microbalances and ultra-microbalances, capable of handling sub-milligram sample weights accurately. This high-end segment, though smaller in volume, represents significant value and technological innovation, often incorporating advanced features like draft shield automation and automatic internal calibration to maintain precision under stringent conditions. Market participants are increasingly tailoring their product lines to address the specific throughput and environmental constraints faced by these specialized user groups, ensuring the availability of purpose-built weighing solutions.

The value chain for the Lab Balance Market begins with complex upstream activities focused on the procurement and development of high-precision components. The most critical component is the weighing cell (often utilizing EMFR technology or monolithic technology), which requires specialized engineering and sophisticated materials science to ensure stability and accuracy. Manufacturers typically source high-grade materials such as advanced aluminum alloys or specialized ceramics for the internal structures to minimize thermal expansion and vibration interference. R&D expenditure is significant at this stage, focusing on improving resolution, stabilization speed, and reliability under varied environmental conditions. The quality and intellectual property surrounding the sensor technology dictate the balance's core performance capabilities, giving substantial leverage to component suppliers or integrated manufacturers.

The central phase involves specialized manufacturing and assembly. Lab balances are high-mix, low-volume products requiring precise calibration in controlled environments. Manufacturing processes include micro-mechanics assembly, automated electronic integration, and rigorous multi-point calibration procedures. Distribution channels are highly professionalized; due to the technical nature and high value of the equipment, sales are predominantly handled through trained, authorized distributors and specialized scientific equipment dealers (indirect sales). These distributors provide localized sales support, technical training, and essential post-sale calibration and maintenance services, which are crucial for maintaining regulatory compliance and customer satisfaction. Direct sales models are often employed for large institutional purchases or high-end customized systems.

Downstream analysis focuses on installation, validation, and lifetime servicing. Unlike consumer electronics, lab balances require formal installation qualification (IQ) and operational qualification (OQ) protocols, especially in regulated pharmaceutical settings. Service contracts, including periodic calibration (often mandatory by regulation), repair, and software updates, constitute a significant and profitable segment of the downstream market. The longevity and reliability of lab balances mean that recurring revenue from calibration services often surpasses the initial sale value over the equipment's lifetime. Therefore, customer support and service network coverage are paramount competitive differentiators in the mature stages of the value chain.

The primary consumers (End-User/Buyers) of lab balances are institutions and commercial entities where mass measurement is critical for quality, safety, and scientific veracity. The Pharmaceutical and Biotechnology sectors represent the most lucrative and demanding customer base. These organizations require balances for every stage of the drug lifecycle, including R&D (compound screening, formula development), Quality Assurance (raw material testing), and manufacturing (content uniformity, dosage verification). Compliance mandates ensure continuous demand for high-end, validated equipment. The rapidly expanding field of personalized medicine further necessitates ultra-precise microbalances for analyzing scarce biological samples.

Academic and governmental research laboratories constitute a steady foundational customer segment. Universities, national research institutes, and public health labs purchase a wide range of balances for fundamental research, teaching, and compliance testing (e.g., environmental samples). Their procurement often relies on grant cycles and capital investment budgets, focusing on versatility and robustness across multiple users. Furthermore, industrial quality control laboratories across various sectors—including food processing, cosmetics, and advanced materials—rely heavily on precision balances and moisture analyzers to meet product specification requirements and maintain certification standards. For example, food manufacturers use them extensively for recipe standardization and mandatory nutritional labeling accuracy.

Emerging markets in Asia, Latin America, and the Middle East are also rapidly becoming significant potential customer hubs. As these regions strengthen their domestic manufacturing capabilities and enforce stricter regulatory standards, there is a surge in demand for modern, reliable laboratory infrastructure, often bypassing older technologies and directly adopting advanced digital weighing systems. Specialized customers, such as forensic laboratories and jewelers dealing with high-value materials, also form niche but important segments requiring verifiable accuracy and specialized measurement functions tailored to their unique regulatory environments.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | $550 Million USD |

| Market Forecast in 2033 | $815 Million USD |

| Growth Rate | 5.8% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Mettler Toledo, Sartorius AG, A&D Company, Shimadzu Corporation, Precisa Gravimetrics AG, Citizen Scale, Adam Equipment, Kern & Sohn GmbH, PCE Instruments, BEL Engineering, Thermo Fisher Scientific, Acculab, RADWAG Balances and Scales, Contech Instruments Ltd., Wipotec-OCS, Ohaus Corporation, Scientech Inc., Essae Technologics Pvt. Ltd. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological landscape of the Lab Balance Market is centered on enhancing precision, reducing measurement time, and integrating the devices within digital laboratory ecosystems. The core technology underpinning high-precision weighing is the Electromagnetic Force Restoration (EMFR) principle. EMFR utilizes an electromagnetic coil to counteract the weight of the sample, providing extremely high resolution and fast response times. Advances in materials science have led to the widespread adoption of monolithic weighing cells—a single-piece aluminum component that serves as the load cell. This design significantly minimizes the influence of temperature variations and mechanical stress, thereby enhancing long-term stability and reliability compared to multi-component traditional load cells.

Another crucial technological area is digitalization and connectivity. Modern lab balances are increasingly equipped with integrated sensors and software that allow for automated internal calibration, often linked to internal temperature monitors. This self-monitoring capability ensures consistent performance without constant manual intervention. Furthermore, the incorporation of advanced communication protocols (Wi-Fi, Ethernet, USB) facilitates seamless data transfer to LIMS or cloud-based databases. Touchscreen interfaces and integrated application software guide users through complex protocols (e.g., density determination, dynamic weighing), improving user compliance and minimizing operational errors, which is a major focus in current laboratory workflows.

Future technological advancements are focused on IoT integration and sustainability. IoT integration enables remote monitoring, predictive diagnostics, and centralized asset management across entire facilities. For specialized applications, particularly moisture analysis, innovations in heating technologies, such as utilizing halogen lamps or infrared heaters, offer faster, more uniform heating, significantly reducing testing cycle times while maintaining accuracy. Efforts are also being directed towards developing balances with lower power consumption and utilizing sustainable materials, aligning with the broader industry trend towards environmentally conscious laboratory operations.

Regional dynamics heavily influence the Lab Balance Market, reflecting differences in R&D spending, regulatory maturity, and industrial growth rates. North America, encompassing the United States and Canada, stands as the leading market primarily due to the vast concentration of global pharmaceutical and biotechnology headquarters, coupled with substantial government and private sector investment in advanced scientific research. Strict FDA regulations require mandatory use of validated, high-precision weighing equipment, generating continuous demand for premium analytical balances and associated service contracts. Early adoption of automation and smart laboratory solutions further cements the region’s dominant position.

Europe represents a mature market characterized by robust academic research, strong chemical manufacturing base, and stringent pan-European quality standards enforced by bodies like the European Medicines Agency (EMA). Western European countries, notably Germany, Switzerland, and the UK, are key hubs for both manufacturing (e.g., Mettler Toledo, Sartorius) and consumption of high-end laboratory equipment. The emphasis on standardized, traceable measurement procedures across the EU sustains a stable demand, particularly for analytical and calibrated precision balances, often driving replacement sales based on regulatory cycles rather than just capacity expansion.

The Asia Pacific (APAC) region is forecasted to achieve the highest Compound Annual Growth Rate (CAGR) during the forecast period. This rapid expansion is attributed to massive investments in healthcare infrastructure, the shift of global pharmaceutical manufacturing activities (especially generics and APIs) to nations like China and India, and the overall industrial modernization across Southeast Asia. While cost sensitivity remains a factor, increasing regulatory alignment with global standards necessitates the adoption of higher quality lab balances, driving accelerated growth in both the precision and entry-level analytical segments. Latin America and the Middle East & Africa (MEA) offer potential for market penetration, driven by expanding oil and gas industries (requiring high-capacity precision weighing) and gradual improvements in local healthcare infrastructure.

The primary driver is the necessity for stringent quality control and high-precision sample preparation mandated by global regulatory bodies (e.g., FDA, EMA) within the pharmaceutical and biotechnology industries. Analytical balances are crucial for ensuring the accuracy and traceability required in drug development and testing protocols.

IoT technology allows lab balances to connect seamlessly to laboratory networks (LIMS), enabling automated data logging, centralized calibration management, remote diagnostics, and streamlined compliance documentation, significantly reducing manual effort and improving data integrity.

The Moisture Analyzer segment is anticipated to show rapid growth, driven by increasing quality control requirements in the food and beverage and chemical processing industries, where rapid and accurate moisture content determination is essential for product quality and safety.

The primary restraint is the extremely high initial capital investment required for ultra-high-resolution microbalances, coupled with the ongoing costs and complexities associated with specialized installation, stringent environmental controls, and frequent, highly sensitive calibration procedures.

North America holds the largest market share, predominantly due to its substantial, sustained investment in pharmaceutical R&D, advanced healthcare infrastructure, and the large-scale presence of global biotechnology leaders who require the most sophisticated weighing instruments.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.