ID : MRU_ 432999 | Date : Dec, 2025 | Pages : 246 | Region : Global | Publisher : MRU

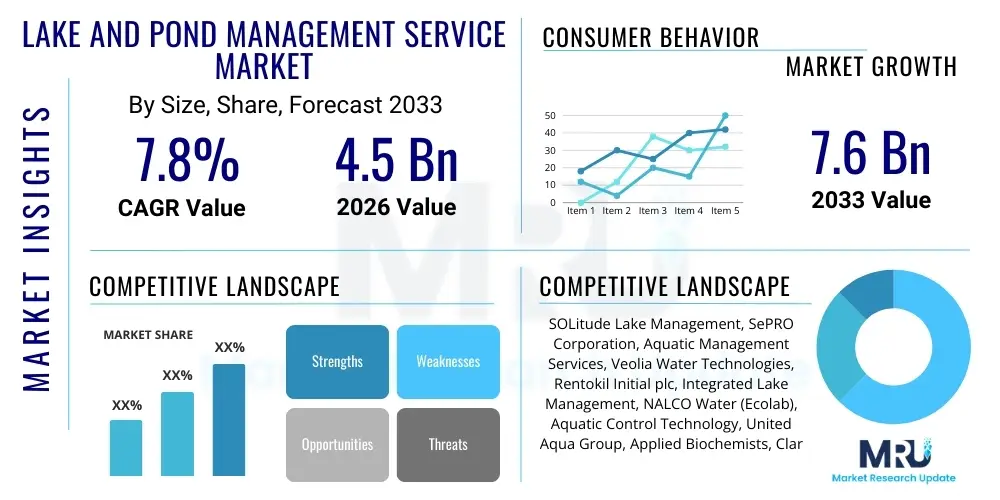

The Lake and Pond Management Service Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 7.8% between 2026 and 2033. The market is estimated at USD 4.5 Billion in 2026 and is projected to reach USD 7.6 Billion by the end of the forecast period in 2033. This robust expansion is fueled by increasing environmental regulations governing water quality, coupled with a heightened awareness among commercial, residential, and municipal stakeholders regarding the critical ecological and aesthetic value of managed aquatic resources. Furthermore, climate change impacts, such as increased frequency of harmful algal blooms (HABs), are necessitating proactive and professional intervention services.

The Lake and Pond Management Service Market encompasses a comprehensive suite of professional activities designed to maintain, restore, and enhance the ecological balance, aesthetic appeal, and functional integrity of natural and man-made aquatic ecosystems, including lakes, reservoirs, stormwater ponds, and decorative water features. These services are vital for ensuring water quality compliance, controlling invasive species, mitigating erosion, and supporting sustainable fisheries management. Service providers utilize a combination of chemical, biological, and mechanical treatments alongside advanced monitoring technologies to achieve long-term aquatic health. The scope of management ranges from routine water testing and aesthetic maintenance to complex ecosystem restoration projects required after significant environmental disturbances or regulatory non-compliance issues.

Major applications for these services span across diverse sectors, notably including golf course maintenance, where pristine water bodies are essential for play and irrigation; residential communities and Homeowners Associations (HOAs), which require consistent upkeep of amenity ponds; and municipal infrastructure, where stormwater retention ponds serve crucial roles in flood control and pollutant filtration. Key benefits derived from professional lake and pond management services include improved biodiversity, reduction in disease vectors such as mosquitoes, compliance with environmental protection agency (EPA) guidelines, preservation of property values, and enhanced recreational opportunities. The core objective is often balancing the needs of human use with the preservation of natural ecological function, ensuring the aquatic environment remains healthy and sustainable for all stakeholders.

Driving factors stimulating market growth are multifaceted. Regulatory tightening concerning nutrient runoff and non-point source pollution compels commercial and agricultural entities to adopt preventative management strategies. The increasing incidence of extreme weather events accelerates the need for proactive erosion control and sediment removal services. Furthermore, technological advancements, particularly in remote sensing, drone-based surveying, and eco-friendly biological control methods, are making management services more efficient, targeted, and environmentally sound. This combination of strict regulatory environments, ecological challenges, and technological innovation cements the market's trajectory towards significant expansion over the forecast period, emphasizing preventative maintenance over purely reactive solutions.

The Lake and Pond Management Service Market is characterized by robust growth, driven primarily by the escalating demand for sustainable aquatic resource stewardship across North America and Europe. Business trends indicate a strong move toward consolidation, with larger national and regional players acquiring smaller, specialized firms to broaden service portfolios, especially in technologically advanced areas like drone-based mapping and predictive water quality modeling. There is a palpable shift towards subscription-based, integrated management plans that offer preventative maintenance and year-round monitoring, moving away from singular, reactive treatment applications. Furthermore, the rising awareness of the negative impacts of traditional chemical controls is fostering innovation in bio-augmentation and integrated pest management (IPM) techniques, influencing product development strategies across the industry value chain and driving higher operational costs but delivering superior long-term ecological results.

Regionally, North America maintains market dominance, propelled by extensive golf course infrastructure, mature residential development requiring HOA management, and stringent EPA water quality standards. However, the Asia Pacific (APAC) region is projected to exhibit the fastest growth rate, fueled by rapid urbanization, substantial investment in recreational tourism (eco-tourism and waterfront resorts), and government initiatives focused on restoring severely polluted urban water bodies, particularly in China and India. Europe shows stable demand, highly influenced by the European Union’s Water Framework Directive (WFD), requiring precise management practices to achieve good ecological status in freshwater bodies. These regional dynamics highlight differential service demands: high-tech compliance in the West, and large-scale remediation and aesthetic enhancement in the East.

Segment trends confirm the primacy of Algae and Aquatic Weed Control as the leading service type, given the pervasive nutrient loading issues globally. However, the Aeration Installation & Maintenance segment is experiencing significant acceleration as clients recognize the fundamental role of dissolved oxygen in preventing water quality degradation and fostering robust aquatic ecosystems. Application-wise, the Residential & Commercial sector remains the largest consumer due to high client density and aesthetic requirements, while the Municipal & Government sector is poised for substantial growth due to mandated stormwater management and public park maintenance obligations. The market is increasingly specializing services based on water body type, requiring specialized expertise for retention ponds versus deep natural lakes, thereby segmenting the consulting and diagnostic services offered by providers.

Common user questions regarding AI's impact on Lake and Pond Management Services center on four key themes: efficacy of predictive modeling for harmful algal blooms (HABs), automation of monitoring processes to reduce labor costs, the ability of AI to optimize chemical treatment dosages, and the integration of diverse data sources (satellite imagery, sensor data, historical trends) for holistic decision-making. Users seek assurance that AI can transition the industry from reactive maintenance, often involving broad-spectrum chemical application, to precise, preventative intervention. The primary concerns revolve around the initial investment cost for advanced sensor networks and AI platforms, data privacy when dealing with proprietary water resource data, and the need for a highly skilled workforce capable of interpreting and implementing AI-generated recommendations. Expectations are high for AI to deliver significant operational efficiencies, higher treatment success rates, and minimal environmental footprint.

AI is fundamentally transforming lake and pond management by enabling sophisticated predictive analytics. Machine learning algorithms analyze vast datasets, including historical weather patterns, nutrient levels, temperature fluctuations, and satellite imagery, to accurately forecast the timing and location of potential issues such as low dissolved oxygen events or the onset of problematic weed growth. This shift to predictive modeling allows service providers to deploy preventative treatments days or even weeks before a crisis develops, significantly enhancing the cost-effectiveness and success rate of management strategies. This precision minimizes the use of chemicals and targets specific, smaller areas, aligning with sustainability goals desired by both regulators and end-users.

Furthermore, the integration of Artificial Intelligence facilitates the automation and optimization of resource allocation. AI systems can manage networks of remote sensors and automated aeration systems, adjusting parameters like oxygen flow rates or water circulation dynamically based on real-time environmental inputs, ensuring optimal ecological conditions with minimal human oversight. For chemical treatments, AI determines the lowest effective dosage required based on real-time biomass estimates derived from imagery analysis, thereby reducing chemical expenditures and environmental impact. This capability is crucial for large-scale municipal contracts and utility reservoirs where resource efficiency and minimizing treatment residues are paramount concerns for public health and environmental stewardship.

The Lake and Pond Management Service Market is shaped by a powerful interplay of forces. Strict environmental regulations, particularly concerning nutrient runoff (phosphorus and nitrogen) from agricultural and residential sources, act as the primary Driver, compelling landowners and municipalities to adopt managed solutions to avoid punitive fines. The increasing public awareness and demand for pristine, usable water resources further fuel preventative management subscriptions. Simultaneously, the inherent seasonality of aquatic issues and the dependence on favorable weather conditions pose a significant Restraint, requiring highly specialized, often costly, seasonal workforce deployment and limiting year-round revenue streams in certain climates. However, the growing technological integration—specifically remote sensing and eco-friendly biological solutions—presents a substantial Opportunity for market players to develop high-margin, scalable monitoring and treatment packages, moving the industry beyond reliance on traditional chemical application.

Impact forces within the market are predominantly driven by environmental and technological shifts. The environmental impact force centers on climate change, which increases water temperatures and nutrient stratification, leading to more frequent and intense algal blooms, thereby escalating the demand for professional intervention. Economically, the market is influenced by construction and real estate cycles; robust residential and commercial development, especially near water bodies, necessitates enhanced stormwater management and aesthetic maintenance services. Social impact forces include the rising demand from HOAs and private estates for aesthetically pleasing and safe water features, directly translating into demand for high-quality, professional maintenance contracts. These factors converge to exert a strong, positive influence on the overall market trajectory, making management services increasingly non-optional for responsible water resource custodians.

The constraints often necessitate innovative solutions. For instance, the restraint imposed by high capital costs for advanced diagnostic equipment is being mitigated by service models that bundle technology access into management contracts, making sophisticated monitoring accessible to smaller clients. The competitive landscape acts as another strong impact force; the presence of numerous specialized local and regional firms alongside large integrated environmental service corporations drives continuous innovation in cost-effective and sustainable treatment methods. Ultimately, the cumulative effect of strict environmental mandates and persistent ecological challenges, coupled with technological mitigation of service complexities, ensures the sustained expansion and formalization of the Lake and Pond Management Service sector, shifting the operational focus toward long-term ecosystem health rather than short-term problem fixing.

The Lake and Pond Management Service Market is analyzed across key dimensions including service type, application, and end-user, enabling a precise understanding of market dynamics and resource allocation. Service segmentation reveals the critical need for proactive ecological interventions, with Algae and Aquatic Weed Control dominating due to pervasive nutrient loading issues affecting nearly all freshwater systems globally. However, the fastest-growing segments relate to preventative and diagnostic services, such as water quality testing and aeration system installation, indicating a market maturation where customers are prioritizing long-term health over emergency remediation. Application analysis demonstrates that the market’s stability is derived from the consistent demands of the Residential & Commercial sectors, while future potential lies heavily in the expanding Municipal & Government utility sector, driven by increasing public infrastructure investments and compliance mandates for effective stormwater management, underscoring the shift from aesthetic maintenance to critical infrastructure service provision.

The value chain for the Lake and Pond Management Service Market begins with the upstream segment, which involves the supply of critical raw materials and technologies. This includes manufacturers of aquatic chemicals (algaecides, herbicides, biological controls), producers of aeration equipment (diffusers, fountains, solar power units), and providers of sophisticated diagnostic tools (water testing kits, remote sensors, integrated monitoring platforms). Key upstream characteristics include stringent regulatory approval for aquatic chemicals and a growing emphasis on biodegradable and environmentally safe products. Strong relationships with reliable suppliers who can offer rapid deployment of specialized equipment are crucial, particularly during peak treatment seasons when demand for specific chemicals or aeration components spikes rapidly across regional markets.

Moving through the midstream, the core value proposition lies in the service providers themselves. These companies perform diagnostic assessments, develop customized management plans, secure necessary permits, execute treatments (chemical application, mechanical harvesting, aeration system installation), and conduct post-treatment monitoring. This segment is highly dependent on specialized intellectual capital, including certified aquatic biologists and licensed applicators, ensuring compliance and maximizing treatment efficacy. Distribution channels in this market are predominantly direct, where service providers interact immediately with the end-user (HOAs, Golf Course Managers, Municipal officials). However, indirect distribution occasionally occurs through environmental consulting firms or large landscaping contractors who subcontract the specialized aquatic work to licensed management companies, especially in complex restoration projects requiring multiple specialties.

The downstream segment focuses on the client interface and long-term service maintenance. For residential and commercial clients, the service often includes recurring monitoring and preventative treatment contracts, maximizing client retention and predictable revenue streams. For municipal and large industrial clients, the focus shifts to compliance reporting and regulatory adherence, demanding meticulous documentation and data transparency from the service provider. The success downstream is measured by ecological outcomes, client satisfaction, and the longevity of the management plan. The entire chain is supported by robust research and development focused on creating non-chemical alternatives and leveraging predictive modeling technologies to ensure sustainable aquatic stewardship, thereby adding significant value across all segments from manufacturing through final service delivery.

The primary customers for Lake and Pond Management Services are diverse entities unified by the need to maintain functional, aesthetic, and compliant water features. Homeowners Associations (HOAs) and community developers represent a critical and steady customer base, driven by the need to preserve property values and ensure recreational safety within residential complexes featuring amenity ponds, decorative lakes, and retention basins. For these customers, the emphasis is heavily placed on aesthetic appearance, nuisance control (mosquitoes, foul odors), and robust contractual reliability. Similarly, operators of private estates and large land holdings require discrete, high-quality management to maintain the integrity and ecological diversity of their personal water resources, often demanding specialized services like custom fisheries management and complex shoreline stabilization projects.

The municipal and governmental sector constitutes a rapidly expanding segment of potential customers, characterized by large, long-term contracts governed by stringent procurement processes and ecological mandates. City governments, county park services, and regional water management authorities utilize these services primarily for managing essential infrastructure, such as public stormwater retention ponds, reservoirs, and public recreational lakes. Their purchasing decisions are critically influenced by regulatory compliance (e.g., meeting Total Maximum Daily Load limits for pollutants), public safety, and the ability of the provider to offer large-scale, environmentally responsible solutions like hydraulic dredging or integrated pest management across multiple sites. The complexity of these projects often mandates providers with extensive regulatory experience and substantial equipment capacity.

Further potential lies within the industrial and agricultural sectors, specifically utility companies requiring maintenance of cooling ponds and hydroelectric reservoirs, and large agricultural operations needing irrigation pond management compliant with environmental standards regarding nutrient discharge. Golf course operators remain indispensable customers, where water quality and appearance directly impact the commercial viability of the facility. These highly sophisticated customers seek comprehensive solutions that integrate irrigation system health with pond water quality, demanding services that minimize disruption to turf health while ensuring attractive, hazard-free water features. The overall trend indicates that customers are increasingly moving away from simple chemical applications toward holistic, consultative, and preventative management partnerships.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 4.5 Billion |

| Market Forecast in 2033 | USD 7.6 Billion |

| Growth Rate | CAGR 7.8% |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | SOLitude Lake Management, SePRO Corporation, Aquatic Management Services, Veolia Water Technologies, Rentokil Initial plc, Integrated Lake Management, NALCO Water (Ecolab), Aquatic Control Technology, United Aqua Group, Applied Biochemists, Clarke Aquatic Services, Precision Lake Management, Lake Management Services LP, Total Lake Management, Foster Lake & Pond Management, Princeton Hydro, Water Resource Group, Lake Savers, Pond Champs, Airmax. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological landscape within the Lake and Pond Management Service Market is rapidly evolving, moving away from purely manual methods towards high-precision, data-driven solutions. Key technological advancements center around remote sensing and monitoring capabilities. This includes the deployment of Internet of Things (IoT) sensor networks—submersible probes that continuously monitor critical water parameters such as dissolved oxygen, pH, temperature, and nutrient concentrations—transmitting data wirelessly for real-time analysis. Furthermore, drone technology equipped with hyperspectral and multispectral cameras is becoming essential for high-resolution mapping of aquatic vegetation density, identifying invasive species spread, and conducting detailed bathymetric surveys to measure sediment accumulation, offering significant improvements in data accuracy and speed compared to traditional boat-based surveys, thereby enabling highly targeted and efficient treatment applications.

Another crucial technological area is the development and adoption of advanced sustainable treatment mechanisms. Biological augmentation, which involves introducing beneficial bacteria and specialized enzymes to enhance natural decomposition of organic muck and control nutrient cycling, is replacing broad-spectrum chemical use in many applications. Similarly, sophisticated aeration systems utilizing nanobubble technology are emerging. Nanobubble aeration significantly enhances oxygen transfer efficiency, providing a non-chemical means of improving water column health, suppressing anaerobic conditions, and preventing nutrient release from sediments. These innovations are critical for attracting environmentally conscious clients, particularly municipal and recreational entities seeking certified green solutions that comply with stringent ecological standards.

The convergence of Big Data analytics and Artificial Intelligence (AI) serves as the backbone for operational efficiency and predictive management in the modern market. AI models process the massive influx of data from sensors, drones, and historical records to create predictive maintenance schedules, optimizing resource deployment and forecasting potential ecological distress events (like HABs) before they manifest. Service providers are leveraging Geographic Information Systems (GIS) platforms to manage client sites, log treatment history, and visualize ecological data spatially. This technological sophistication necessitates a higher level of training for field technicians and drives partnerships between traditional management firms and specialized technology providers, ultimately raising the barrier to entry for new market participants but delivering superior, measurable ecological outcomes for end-users.

The market is primarily driven by increasingly stringent environmental regulations regarding nutrient runoff and water quality compliance (e.g., EPA mandates), the accelerated rate of harmful algal blooms due to climate change, and high aesthetic demands from residential communities (HOAs) and commercial entities like golf courses seeking professional upkeep of their water assets. Technological advancements in monitoring also make preventative management more accessible.

AI enhances cost-effectiveness by enabling predictive modeling of ecological issues, allowing service providers to deploy targeted, preventative treatments instead of costly, large-scale reactive applications. This precision reduces chemical usage, optimizes labor deployment through efficient scheduling, and minimizes long-term restoration costs by maintaining consistent water health using real-time data from IoT sensors.

Algae and Aquatic Weed Control services currently hold the largest market share globally. This dominance is due to the widespread environmental challenge of eutrophication—excess nutrient loading causing pervasive growth of nuisance vegetation and harmful algae across various climates and water body types, requiring continuous professional intervention.

Service providers face significant challenges related to obtaining, maintaining, and complying with diverse permitting requirements for aquatic chemical application, which vary widely by region and water body classification. Furthermore, managing the liability associated with chemical runoff and ensuring adherence to local and national water quality discharge standards necessitates complex, specialized regulatory expertise and comprehensive documentation.

The market is currently undergoing significant consolidation. While it remains fragmented at the local level with many small, independent operators, larger national and international environmental service companies are actively acquiring regional specialists to expand their geographic footprint and integrate advanced services (like aeration and diagnostics), aiming to offer holistic, unified management solutions across broader territories.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.