ID : MRU_ 435506 | Date : Dec, 2025 | Pages : 245 | Region : Global | Publisher : MRU

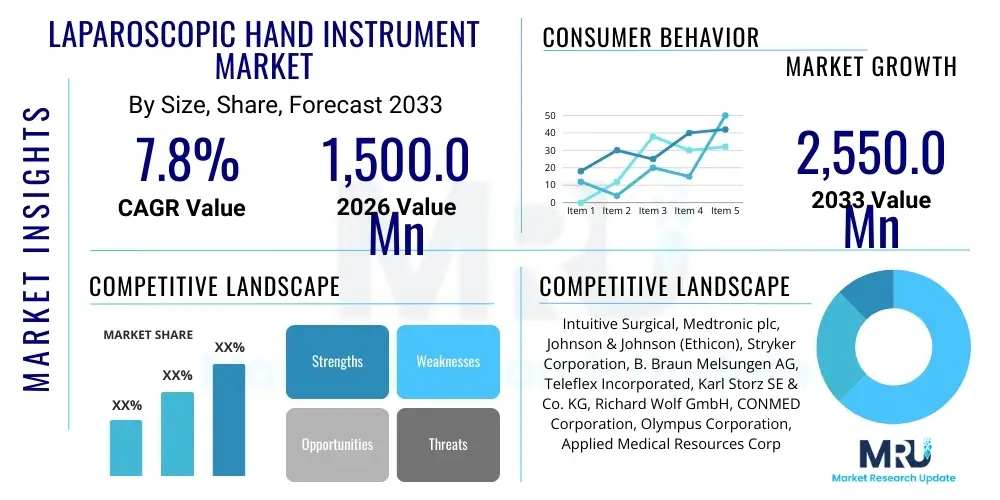

The Laparoscopic Hand Instrument Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 7.8% between 2026 and 2033. The market is estimated at USD 1,500.0 Million in 2026 and is projected to reach USD 2,550.0 Million by the end of the forecast period in 2033.

The Laparoscopic Hand Instrument Market encompasses a sophisticated range of medical devices crucial for performing minimally invasive surgical procedures (MIS). These instruments are designed to be inserted through small incisions, enabling surgeons to manipulate tissues, coagulate vessels, cut, grasp, and retract organs within the abdominal or pelvic cavity without requiring large open incisions. Products typically include graspers, dissectors, scissors, needle holders, retractors, and suction/irrigation devices, often categorized by their reusability (reusable or disposable). The primary objectives of these instruments are to enhance surgical precision, minimize patient trauma, reduce recovery times, and decrease hospital stays, thereby lowering the overall cost burden associated with surgical intervention.

Major applications for laparoscopic hand instruments span across general surgery, gynecology, urology, and bariatric surgery. In general surgery, they are vital for cholecystectomy, appendectomy, and hernia repair. Gynecological applications include hysterectomy and endometriosis treatment, while urology utilizes them for prostatectomy and nephrectomy. The increasing global prevalence of chronic diseases requiring surgical intervention, coupled with the growing patient preference for less invasive procedures, are the foundational driving factors supporting consistent market expansion. Furthermore, continuous technological advancements focused on improving ergonomic design, material quality, and incorporating articulating features are enhancing the utility and adoption rate of these instruments across global surgical centers.

The benefits derived from the utilization of advanced laparoscopic instruments are manifold, impacting both clinical outcomes and healthcare economics. Clinically, patients experience reduced post-operative pain, smaller scars, and lower rates of surgical site infections compared to traditional open surgery. Economically, the shorter recovery periods facilitate quicker patient discharge, optimizing resource utilization within hospitals. Key driving factors include heightened awareness among surgical professionals regarding MIS techniques, robust investment in healthcare infrastructure in emerging economies, and the rapid pace of regulatory approvals for innovative devices that offer superior handling and precision, ensuring the market maintains a steady, upward growth trajectory.

The Laparoscopic Hand Instrument Market is characterized by robust technological evolution and increasing consolidation, driven primarily by the global shift towards minimally invasive surgery (MIS). Business trends show a strong emphasis on developing disposable instruments to mitigate cross-contamination risks and reusable instruments engineered with modular designs for cost efficiency and enhanced sterilization. Furthermore, strategic mergers, acquisitions, and collaborations focused on expanding product portfolios in niche areas, such as advanced energy instruments and robotic accessories, are shaping the competitive landscape. Supply chain resilience, particularly concerning high-quality materials like surgical-grade stainless steel and advanced polymers, remains a critical operational consideration for key market participants.

Regional trends indicate North America currently holds the largest market share due to established reimbursement policies, high surgical procedure volumes, and early adoption of sophisticated surgical technologies. However, the Asia Pacific (APAC) region is projected to register the highest Compound Annual Growth Rate (CAGR), fueled by expanding medical tourism, substantial government investment in healthcare infrastructure, and the rapidly increasing patient population requiring treatments for lifestyle-related diseases. Europe maintains a mature, stable market, focused heavily on regulatory compliance (MDR/IVDR) and promoting sustainable healthcare practices through the extended lifespan of reusable instruments.

Segment trends highlight the dominance of the Hand-held Instruments category (graspers and dissectors) owing to their fundamental role in nearly all laparoscopic procedures. The disposable instrument segment is experiencing rapid growth due to heightened infection control standards, particularly post-pandemic, despite the higher per-unit cost. Application-wise, general surgery remains the leading segment, followed closely by gynecology. Innovations in visualization and advanced electrosurgical tools are significantly influencing the purchasing decisions of end-users, mainly specialized surgical centers and hospitals, pushing demand toward high-definition and ergonomic instrument designs.

User queries regarding the impact of Artificial Intelligence (AI) on the Laparoscopic Hand Instrument Market primarily revolve around the integration of AI into robotic surgical systems and its subsequent influence on the design and function of traditional hand instruments. Common concerns include whether AI-driven robotics will render standard laparoscopic instruments obsolete, how AI can enhance surgical precision (e.g., through augmented reality or real-time tissue recognition), and the cost implications of integrating AI capabilities into high-volume surgical procedures. Users are also keen to understand if AI can standardize surgical training by providing objective performance metrics based on instrument handling data.

Analysis reveals that rather than replacing traditional hand instruments, AI primarily augments their usage, particularly within the robotic surgery framework, which often uses specialized robotic hand instruments. Key themes suggest that AI's initial influence is less on the physical design of basic graspers and scissors and more on procedural guidance, enhancing visualization, and optimizing workflow. AI algorithms interpret intraoperative data (like force feedback, tissue tension, and thermal distribution) collected through sensors integrated into advanced instruments, providing real-time feedback to the surgeon, thereby potentially lowering complication rates. This shift necessitates the development of "smarter" instruments capable of transmitting precise data points.

Expectations are high regarding AI's role in predictive maintenance and sterilization protocols for reusable instruments, optimizing equipment lifespan and ensuring sterility compliance. The market anticipates a bifurcation: continued demand for basic, cost-effective instruments for routine procedures, and rapid evolution of high-end, sensor-embedded instruments tailored for complex, AI-assisted surgeries. This technological evolution drives innovation in material science and miniaturization, ensuring the hand instruments remain compatible with and integral to the AI-enhanced surgical ecosystem, fundamentally improving surgical accuracy and reducing human error.

The market for laparoscopic hand instruments is shaped by a confluence of influential factors, encompassing strong drivers that propel growth, significant restraints that limit expansion, and emerging opportunities for innovation. The primary driver is the demonstrable clinical superiority of minimally invasive surgery (MIS) over open surgery, leading to widespread adoption by surgeons and increasing demand from patients seeking faster recovery and reduced scarring. Government and private insurance policies increasingly favor MIS procedures due to their cost-effectiveness over the long term, further stimulating market demand. This pervasive acceptance ensures a foundational growth trajectory for core surgical tools.

However, substantial restraints temper the market’s potential. The high initial capital investment required for establishing advanced laparoscopic suites, particularly in developing economies, poses a significant barrier. Additionally, the steep learning curve and specialized training necessary for surgeons to achieve proficiency in MIS techniques limit the availability of qualified professionals, especially in rural or underserved areas. The regulatory environment, particularly stringent new directives like the EU MDR, increases compliance costs and slows down the time-to-market for novel devices, which impacts smaller manufacturers disproportionately. Furthermore, the conflict between reusable instruments (lower long-term cost, higher infection risk if sterilization fails) and disposable instruments (higher environmental footprint, guaranteed sterility) presents a continuous operational challenge for healthcare providers.

Opportunities for market players are primarily concentrated in technological advancements, including the development of multi-functional and articulating instruments that reduce the need for instrument exchange. The integration of advanced materials, such as titanium and specialized plastics, to improve durability and reduce weight is a key area of focus. Furthermore, untapped potential lies in expanding market penetration in emerging economies like India, China, and Brazil, where surgical volumes are rapidly escalating but penetration of advanced MIS techniques remains comparatively low. Successful market strategies must leverage the demand for highly ergonomic, disposable solutions while simultaneously addressing cost and training hurdles through collaborative educational initiatives.

The Laparoscopic Hand Instrument Market is extensively segmented based on Product Type, Application, and End-User, reflecting the diverse requirements across various surgical disciplines and healthcare settings. The segmentation allows manufacturers to target specific product innovations, such as disposable versus reusable options, toward defined user groups, optimizing production and distribution strategies. The increasing specialization within minimally invasive procedures, such as single-incision laparoscopy (SILS), continuously drives the evolution of instrument design within these segments, demanding more flexible, smaller, and specialized tools to perform intricate tasks through constrained access points.

The Product Type segment, specifically, provides a crucial distinction between instruments designed for manipulation (graspers, dissectors) and instruments designed for cutting or coagulation (scissors, specialized energy devices). The growth rates across these sub-segments vary significantly, influenced by procedural preferences and evolving safety standards, particularly concerning sharps management and electrosurgical safety. For instance, the market for articulating and robotic instruments is growing faster than traditional fixed-jaw instruments due to their enhanced dexterity and capability in complex procedures.

Analysis by End-User reveals the contrasting purchasing behaviors of hospitals, which typically invest in a balanced portfolio of reusable instruments complemented by disposables, versus specialized Ambulatory Surgical Centers (ASCs), which often favor disposable instruments for efficiency, lower infection risk, and minimal operational overhead related to sterile processing. Understanding these procurement dynamics and the underlying application volumes (e.g., high-volume cholecystectomy vs. lower-volume complex oncology procedures) is paramount for accurate market forecasting and strategic planning.

The value chain for the Laparoscopic Hand Instrument Market begins with upstream activities involving the sourcing of high-grade raw materials, primarily surgical stainless steel, medical-grade polymers, and advanced ceramics for insulation and durability. Manufacturing is a critical, complex stage requiring precision engineering, often involving computer-numerical control (CNC) machining, specialized molding, and meticulous assembly in ISO-certified cleanroom environments. Research and development (R&D) forms the core value addition, focusing on miniaturization, enhanced ergonomics, multi-functionality, and the integration of smart sensors, demanding significant capital investment to meet evolving clinical needs and stringent regulatory standards.

Midstream activities involve sophisticated distribution channels. Direct sales channels are frequently employed by large, established market leaders, especially for high-value capital equipment and specialized electrosurgical instruments, allowing for direct technical support and relationship management with key hospital systems. Indirect channels, utilizing regional distributors, specialized medical device suppliers, and third-party logistics (3PL) providers, are essential for reaching smaller clinics, ASCs, and penetrating geographically diverse markets, especially in emerging regions where local expertise is crucial for navigating regulatory complexities and procurement processes.

Downstream analysis focuses on the end-users—hospitals and Ambulatory Surgical Centers (ASCs)—where the instruments are utilized. Post-sale services, including maintenance, repair, and specialized training (crucial for reusable instruments and complex devices), add significant value and influence long-term customer loyalty. The purchasing decision often involves complex committees factoring in initial procurement cost, long-term sterilization expenses, clinical evidence demonstrating efficacy, and alignment with institutional infection control policies, highlighting the multi-faceted nature of the market's value proposition from sourcing to post-utilization support.

The primary potential customers and end-users of laparoscopic hand instruments are institutions involved in surgical care delivery. Large, multi-specialty hospitals, including teaching hospitals and public health facilities, represent the largest segment due to their high volume of diverse surgical procedures, continuous need for instrument sterilization, and substantial purchasing power. These institutions require comprehensive inventories encompassing both reusable and disposable options to manage various laparoscopic specialties like general, bariatric, gynecological, and urological surgeries, prioritizing instruments that demonstrate longevity and ease of sterilization.

Ambulatory Surgical Centers (ASCs) constitute the second fastest-growing customer segment. ASCs typically focus on high-volume, less complex procedures (e.g., cholecystectomy, hernia repair) and prioritize efficiency and quick turnaround times. Their purchasing inclination often leans heavily towards disposable or single-use instruments to bypass the overhead and potential risks associated with in-house sterile processing, making them ideal targets for manufacturers specializing in disposable trocar systems and single-use graspers/dissectors. Furthermore, the increasing procedural migration from inpatient hospitals to outpatient settings due to cost pressures fuels the sustained demand from ASCs.

Specialty clinics focusing on specific areas, such as high-end urology or gynecology practices, also represent important niche customers. These clinics often demand highly specialized instruments, such as micro-laparoscopic tools or specialized needle holders, requiring manufacturers to maintain strong direct sales relationships and specialized product lines. Finally, government procurement agencies and global NGOs procuring equipment for health initiatives in low- and middle-income countries represent large-volume, cost-sensitive customers who often prioritize robust, reusable systems that offer maximum lifespan and lower operational costs in resource-constrained environments.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 1,500.0 Million |

| Market Forecast in 2033 | USD 2,550.0 Million |

| Growth Rate | 7.8% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Intuitive Surgical, Medtronic plc, Johnson & Johnson (Ethicon), Stryker Corporation, B. Braun Melsungen AG, Teleflex Incorporated, Karl Storz SE & Co. KG, Richard Wolf GmbH, CONMED Corporation, Olympus Corporation, Applied Medical Resources Corporation, Microline Surgical, Inc., PENTAX Medical, Cook Medical, Erbe Elektromedizin GmbH, Grena Ltd., Sklar Instruments, Hoya Corporation. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological landscape of the Laparoscopic Hand Instrument Market is rapidly evolving, driven by the demand for enhanced precision, better ergonomics, and improved patient safety. A key trend involves the proliferation of articulating and advanced modular instruments. Articulating instruments allow the surgeon to bend the tip of the tool inside the patient's body, mimicking the movements of an open surgical hand, which is crucial for deep pelvic or upper abdominal dissection. Modular systems, which allow the exchange of tips, shafts, and handles, reduce inventory costs for hospitals while offering surgeons specialized functionality without needing an entirely new instrument set, enhancing versatility in complex procedures.

Another dominant technological force is the integration of advanced energy devices within laparoscopic hand tools. These instruments, such as ultrasonic dissectors and advanced bipolar sealers, combine cutting and coagulation capabilities, minimizing blood loss and operating time. Furthermore, the move toward "smart" instruments incorporating micro-sensors for haptic feedback and real-time data collection is gaining traction. These sensors provide objective metrics on the force exerted on tissues, crucial for protecting delicate structures and optimizing surgical outcomes, especially when transitioning to robotic or semi-automated surgical platforms.

Material science innovation also plays a vital role, focusing on developing lighter, more durable, and biocompatible materials. Manufacturers are using specialized alloys and engineered polymers to reduce the weight of instruments, thus minimizing surgeon fatigue during long procedures, and improving resistance to corrosion from repeated sterilization cycles. Furthermore, the development of smaller-diameter instruments (micro-laparoscopy) facilitates even smaller incisions (2mm or 3mm), further reducing patient trauma and scarring, representing a significant technological advancement in the ongoing pursuit of ultra-minimally invasive surgery.

The primary drivers are enhanced patient safety and strict infection control standards. Disposable instruments eliminate the risk of cross-contamination and circumvent the complex, time-consuming, and resource-intensive processes associated with instrument cleaning, sterilization, and maintenance, especially in high-volume surgical centers like Ambulatory Surgical Centers (ASCs).

Robotics drives innovation, not obsolescence. While robotic surgery uses specialized instruments, it increases the demand for compatible, high-precision hand instruments for docking, tissue manipulation, and assistant port usage. Furthermore, the technological advancements in robotic instruments (e.g., improved articulation) often transfer to conventional advanced hand instruments.

General Surgery holds the largest market share. This is attributed to the high volume and global frequency of common procedures such as laparoscopic cholecystectomy (gallbladder removal), appendectomy, and hernia repairs, which are routinely performed using standard laparoscopic hand instruments worldwide.

Key ergonomic features include reduced instrument weight to minimize surgeon fatigue, enhanced handle design for better grip and tactile feedback (haptics), improved locking mechanisms for secure tissue grasping, and specialized shaft coatings to reduce glare and friction during deep abdominal procedures, all aimed at improving surgical precision.

The high growth rate in APAC is fueled by expanding healthcare expenditure, rapid construction of modern surgical facilities, increased medical tourism, and a growing middle-class population demanding access to advanced minimally invasive treatments, particularly in populous countries like China and India.

Challenges include the complexity of multi-part instruments, the difficulty in accessing internal channels for cleaning, variability in institutional sterilization protocols, and the need for robust tracking systems to ensure instruments have completed the required cycles and maintain functionality over time, requiring stringent adherence to central sterile supply department (CSSD) guidelines.

Force feedback (haptic technology) integrates sensors into the instrument tip and handle, allowing the surgeon to "feel" the amount of pressure being applied to delicate tissues. This technology significantly reduces the risk of inadvertent tissue damage, particularly crucial in complex dissections or suturing, thereby enhancing surgical safety and outcome quality.

SILS instruments represent a significant growth niche. They require specialized, highly articulated, and often flexible instruments designed to navigate through a single, crowded access port. While adoption is slower than standard multi-port laparoscopy, the superior cosmetic results and further reduced invasiveness ensure a strong, technologically demanding market outlook for these specific tool designs.

Advanced instruments increasingly utilize specialized materials such as high-strength PEEK (Polyether ether ketone) for non-conductive components, specialized titanium alloys for enhanced strength-to-weight ratios, and advanced ceramic coatings to improve insulation for electrosurgical devices and prolong the lifespan of working tips subject to high wear.

Government regulations like the EU Medical Device Regulation (MDR) demand higher standards of clinical evidence, traceability, and post-market surveillance for all devices, including hand instruments. This regulation increases compliance costs for manufacturers, potentially leading to the withdrawal of older, less-documented products and driving the necessity for robust quality management systems throughout the value chain.

Growing environmental concerns are pressuring manufacturers to develop "greener" disposable instruments, utilizing biodegradable plastics and minimizing packaging. While disposables enhance safety, their waste volume is substantial. This has led to R&D in hybrid models and sophisticated recycling programs for specialized medical waste, aiming to balance clinical necessity with ecological responsibility.

Specialized coatings, such as non-stick or anti-reflective layers, are applied to instrument tips to improve functionality. Non-stick coatings are vital for electrosurgical instruments to prevent tissue adherence during cauterization, while anti-reflective coatings reduce light interference, ensuring clearer visualization through the laparoscope, enhancing surgeon performance and efficiency.

Teaching hospitals are critical early adopters, integrating advanced laparoscopic techniques and instruments into surgical residency programs. Their demand is driven by the need for cutting-edge technology for training and complex cases. They often require simulation systems paired with instruments to allow residents to practice handling and technique outside the operating room.

Key supply chain risks include dependence on niche suppliers for specialized raw materials (e.g., high-grade surgical stainless steel or microelectronics), geopolitical instability affecting global logistics, and vulnerability to quality control lapses in outsourced manufacturing, all of which can lead to production delays and increased costs for precision instruments.

Laparoscopic scissors feature long, slender shafts and small, precise cutting jaws at the distal tip, often operated remotely via a handle mechanism. They frequently include integrated monopolar or bipolar electrosurgical capabilities for simultaneous cutting and coagulation, functionality not present in standard open surgical scissors.

The procedural shift toward outpatient settings (ASCs) increases the demand for readily available, sterile, disposable instruments, as ASCs often lack the centralized, large-scale reprocessing facilities found in hospitals. Procurement emphasis moves from long-term cost of ownership (reusable) to immediate efficiency and guaranteed sterility (disposable).

Bariatric surgery requires instruments with extra-long working lengths (often 45cm or more) to reach deep anatomical structures in obese patients. Challenges include maintaining shaft rigidity over long lengths, ensuring precise articulation, and designing robust energy devices capable of sealing thicker tissues and vessels effectively.

Insulation quality is critical to prevent accidental burns or unintended thermal damage to surrounding healthy tissue. A breach in insulation on the instrument shaft can lead to current leakage (capacitive coupling) inside the abdominal cavity, posing a serious patient safety risk, hence the need for rigorous material testing and quality control.

Micro-laparoscopy uses instruments with diameters of 3mm or less, allowing for exceptionally small incisions and minimal scarring. This requires specialized micro-graspers, dissectors, and scissors that must maintain structural integrity and functional precision despite their drastically reduced size, often leading to proprietary manufacturing processes.

The demand for reusable instruments remains highly prevalent in the European market, particularly within nationalized healthcare systems (like the NHS) and Germany, where cost-efficiency and sustainability mandates favor durable, multi-use surgical tools that offer a lower lifetime cost per procedure compared to disposable alternatives.

Laparoscopic needle holders are significantly more complex, featuring long shafts, often curved jaws, and robust ratchet mechanisms to securely grasp and manipulate fine suture needles through restricted access ports. Advanced models frequently incorporate carbide inserts to enhance grip longevity and articulating tips for easier intracorporeal knot tying.

The rising elderly population demands surgical approaches that minimize trauma and hasten recovery, further driving the adoption of MIS. Instrument design must prioritize gentleness (less tissue trauma), ergonomic handling for surgeons operating on frail tissues, and precision to manage potential comorbidities common in geriatric patients.

Primary challenges include budgetary constraints leading to preference for low-cost alternatives, limited access to specialized training for surgeons, and inadequate infrastructure for proper instrument sterilization and maintenance, often resulting in slower adoption of high-end, complex, or disposable systems.

Robotic surgery instruments, which are often proprietary, single-use, and contain complex internal mechanisms, command significantly higher prices than conventional laparoscopic instruments. This trend encourages traditional manufacturers to invest in high-margin, specialized accessory instruments that interface with the robotic platforms.

In procedures like sleeve gastrectomy (bariatric surgery), specialized graspers are essential for safely manipulating the stomach and tissues without causing trauma. They often feature atraumatic jaws, precise locking mechanisms, and extra-long shafts to handle the organ manipulation required before resection, emphasizing secure and gentle handling.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.