ID : MRU_ 435754 | Date : Dec, 2025 | Pages : 245 | Region : Global | Publisher : MRU

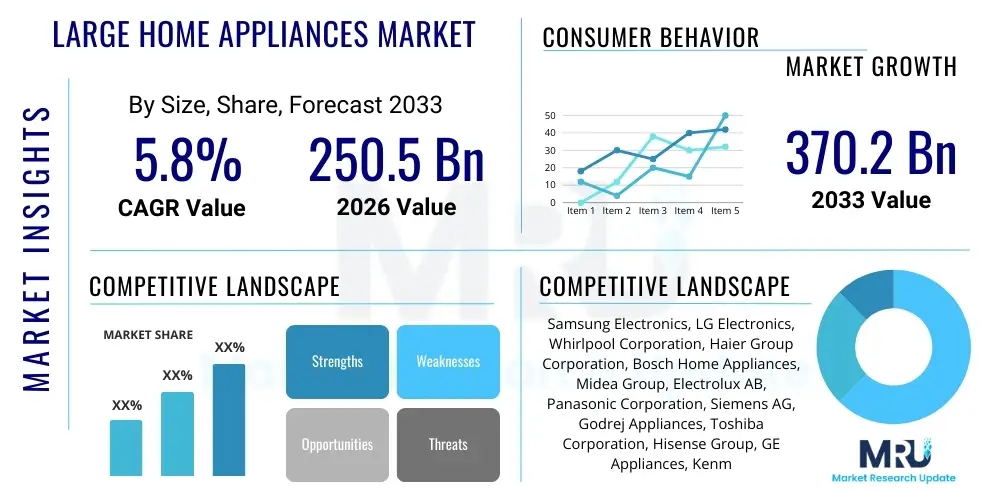

The Large Home Appliances Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 5.8% between 2026 and 2033. The market is estimated at USD 250.5 Billion in 2026 and is projected to reach USD 370.2 Billion by the end of the forecast period in 2033.

The Large Home Appliances Market, often referred to as white goods, encompasses essential residential and commercial equipment designed for major household tasks such as food preservation, laundry care, and cooking. These products include refrigerators, freezers, washing machines, dryers, dishwashers, and cooking ranges (ovens and cooktops). Characterized by high energy consumption potential and long service lifecycles, these appliances form the backbone of modern living, significantly enhancing convenience, hygiene, and overall quality of life across global demographics. The primary functionality involves reducing manual labor and optimizing resource usage (time, water, and energy) in domestic environments.

Major applications of large home appliances span residential housing units, multi-family dwellings, hotels, institutional settings, and specialized commercial kitchens. The inherent benefits include improved food safety through advanced refrigeration, enhanced sanitation via high-efficiency washing cycles, and streamlined meal preparation. The market is fundamentally driven by global housing construction rates, increasing disposable incomes in emerging economies, and the consistent demand for replacements and upgrades in developed regions, fueled by the push for energy efficiency and smart technology integration.

The transition toward smart homes and IoT connectivity is rapidly reshaping the product landscape, moving devices from mere functional tools to integrated, intelligent systems that can self-diagnose, optimize performance remotely, and interact with other household technologies. This evolution ensures that new appliance models offer not only better performance but also significant cost savings over their operational lifespan through superior energy and water conservation features, thereby attracting environmentally conscious consumers and meeting stringent regulatory mandates worldwide.

The global Large Home Appliances Market is experiencing robust growth, primarily propelled by urbanization, increasing consumer spending power in Asia Pacific, and a pervasive trend toward smart, connected kitchen and laundry solutions. Business trends indicate a strong competitive focus on product differentiation through aesthetic design, material innovation, and integration of artificial intelligence (AI) for predictive maintenance and personalized user experiences. Manufacturers are heavily investing in sustainable practices, emphasizing recycled materials and developing appliances that comply with high energy efficiency standards (like Energy Star ratings), which is becoming a crucial purchasing criterion for the modern consumer base.

Regionally, Asia Pacific maintains its dominance, driven by massive population density, rapid housing development, and the expansion of the middle class in countries such as China and India, leading to high initial purchases and rapid market penetration. North America and Europe, while being mature markets, exhibit stable demand focused on premium, integrated, and highly energy-efficient models. Segment trends clearly show that the refrigeration category holds the largest revenue share due to its essential nature, while the laundry care segment (especially dryers) is anticipated to record the highest growth rate, driven by technological advancements like heat pump drying technology and increased convenience adoption.

The industry faces constraints related to supply chain volatility, fluctuating raw material costs (especially steel and plastics), and the complexity of managing e-waste associated with the disposal of old units. However, opportunities abound in developing modular appliances, expanding direct-to-consumer (D2C) sales channels, and leveraging data analytics derived from smart appliances to enhance after-sales services and product development lifecycles. The overarching theme is the convergence of sustainability, connectivity, and premiumization across all product lines, defining the trajectory of market expansion through 2033.

Common user questions regarding AI's impact typically revolve around practical utility, privacy concerns, and return on investment. Users frequently ask: "How will AI make my refrigerator save me money?" "Are AI-enabled washers truly better at stain removal?" and "What data is my smart oven collecting?" This analysis reveals that users prioritize tangible, measurable benefits (energy savings, enhanced performance, predictive maintenance alerts) alongside strong reassurances regarding data security and simplified interfaces. The key themes are enhanced autonomy, operational efficiency, and personalization, moving beyond basic connectivity toward genuine intelligence that anticipates user needs and optimizes resource consumption without manual intervention.

The market dynamics are defined by robust drivers stemming from technological innovation and demographic shifts, balanced by significant restraints such as price sensitivity and regulatory hurdles, while ample opportunities exist in untapped emerging markets and the circular economy model. The primary driving forces include the global acceleration of new housing starts, rising demand for energy-efficient appliances mandated by stricter governmental regulations (e.g., EU Ecodesign directives), and continuous consumer desire for convenience features enabled by IoT integration. Conversely, restraints involve high initial purchase costs for premium smart appliances, making them inaccessible to lower-income segments, and complex, rapidly evolving cybersecurity threats associated with network-connected devices. The opportunity landscape is broad, focusing on modular appliance design that facilitates easier repair and upgrades, expanding market reach through localized digital sales platforms, and developing ultra-low-energy appliances utilizing advanced materials and insulation technologies.

Impact forces currently exerting the strongest influence include the rapidly escalating costs of key raw materials like steel, copper, and specialized plastics, driven by global supply chain disruptions and geopolitical instability, which directly pressures manufacturing profit margins. Furthermore, intense competition among established global players and aggressive regional manufacturers leads to pricing wars, particularly in high-volume segments like basic refrigerators and washers. The regulatory force, driven by sustainability goals, mandates constant product redesign to achieve higher efficiency ratings, requiring significant upfront R&D investment but ultimately reshaping market standards and creating entry barriers for non-compliant models.

The consumer preference for subscription-based maintenance services and integrated warranty packages is a growing force, influencing manufacturers to shift their business models toward service-centric revenue streams rather than relying solely on hardware sales. This trend is closely tied to the longevity and reparability of appliances. Another critical impact force is the volatile economic environment, where inflation and recession fears directly influence large-ticket purchases, often leading consumers to delay replacement cycles, thereby affecting volume growth in mature markets. Manufacturers must strategically balance innovation costs with consumer affordability to maintain market share.

The Large Home Appliances Market is comprehensively segmented based on product type, distribution channel, and end-use application, providing a granular view of revenue generation and growth pockets. Product type segmentation, which includes categories like refrigeration, cooking, and laundry, forms the core of market analysis, with each sub-segment exhibiting distinct technological adoption rates and demand drivers. The distribution channel breakdown differentiates between traditional brick-and-mortar retail and the rapidly expanding e-commerce sector, reflecting evolving consumer purchasing habits heavily influenced by digital accessibility and comparative shopping tools. Understanding these segments is crucial for manufacturers to tailor their marketing and supply chain strategies effectively.

Further segmentation by end-use application distinguishes between residential consumption (the largest share) and commercial usage (hotels, restaurants, laundromats), which typically demand heavy-duty, commercial-grade appliances with specialized performance metrics and durability requirements. Geographic segmentation provides critical insight into regional maturity and consumer preferences, highlighting the dominance of the Asia Pacific region in terms of volume and the focus on premiumization in North America and Europe. The granular view afforded by this comprehensive segmentation allows stakeholders to identify specific high-growth areas, such as connected laundry appliances sold through online platforms in urban residential settings.

The value chain for large home appliances begins with upstream activities focused on raw material procurement, encompassing the sourcing of metals (steel, aluminum, copper), plastics, electronic components (microprocessors, sensors), and specialized chemicals (refrigerants, insulation). Efficiency in managing these volatile input costs is paramount, often necessitating long-term contracts and hedging strategies. Midstream activities involve high-precision manufacturing, encompassing casting, molding, assembly, quality control, and rigorous testing for safety and energy compliance. Optimization of automated assembly lines and lean manufacturing techniques are key differentiators in this stage, determining final product cost and reliability.

Downstream activities are dominated by distribution and sales. The distribution channel is bifurcated into direct sales, involving company-owned showrooms and websites, and indirect sales, leveraging a vast network of third-party specialty retailers, mass merchandisers, and, increasingly, large e-commerce platforms. The shift toward digital channels necessitates robust logistics and last-mile delivery capabilities due to the size and weight of the products. Effective inventory management, strategically placed warehouses, and rapid fulfillment are critical success factors for maintaining competitive pricing and customer satisfaction in the highly competitive retail environment.

The final stage of the value chain involves post-sale services, including installation, maintenance, warranty support, and eventual end-of-life recycling or disposal. The growing complexity of smart appliances drives demand for highly skilled technicians and sophisticated diagnostic tools. Companies that excel in providing prompt, efficient, and comprehensive after-sales support not only enhance brand loyalty but also gain invaluable data on product performance and failure modes, feeding back into the R&D process to ensure continuous product improvement and adherence to circular economy principles.

Potential customers for the Large Home Appliances Market are broadly categorized into replacement buyers and first-time buyers, primarily segmented across the residential and commercial sectors. In the residential sector, first-time buyers are typically newly formed households, young professionals moving into their first apartment, or purchasers of new construction homes, especially concentrated in rapidly urbanizing areas globally. Replacement buyers, constituting a significant volume of demand in mature markets, are generally existing homeowners seeking to upgrade old, inefficient, or non-functional units to newer models featuring enhanced connectivity, greater energy efficiency, and modern aesthetics. This segment is highly responsive to promotional offers and trade-in programs.

The commercial segment represents end-users requiring professional-grade equipment, often prioritizing durability, high capacity, and specialized functions. This includes hospitality establishments (hotels, motels, short-term rentals) needing commercial laundry equipment and robust refrigeration, healthcare facilities (hospitals, clinics) demanding high-sanitation washing and specialized storage, and the foodservice industry (restaurants, institutional kitchens) requiring high-output cooking and cooling systems. These buyers prioritize total cost of ownership (TCO) over initial price, focusing on energy consumption, maintenance downtime, and long-term service contracts. Government agencies and institutional housing projects also represent significant, large-volume potential customers focused on bulk purchases and standardization.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 250.5 Billion |

| Market Forecast in 2033 | USD 370.2 Billion |

| Growth Rate | 5.8% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Samsung Electronics, LG Electronics, Whirlpool Corporation, Haier Group Corporation, Bosch Home Appliances, Midea Group, Electrolux AB, Panasonic Corporation, Siemens AG, Godrej Appliances, Toshiba Corporation, Hisense Group, GE Appliances, Kenmore Appliances, Miele, Arçelik A.S., Daikin Industries, Fisher & Paykel Appliances, Sub-Zero Group, Viking Range LLC |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The Large Home Appliances Market is characterized by rapid technological advancement, moving beyond basic functionality toward integrated, energy-optimized, and intelligent systems. A major technological focus is the pervasive integration of the Internet of Things (IoT), enabling appliances to connect to home networks, allowing for remote monitoring, diagnostics, and control via smartphone applications. This connectivity allows for seamless interaction between different appliances, such as a smart refrigerator communicating inventory needs to a smart shopping list application, or a washing machine automatically starting a cycle based on off-peak energy pricing. This IoT integration is foundational for the smart home ecosystem, driving substantial market value.

Furthermore, significant innovation is concentrated in improving energy and water efficiency, driven by stringent global regulatory standards. Technologies such as high-efficiency inverter compressors in refrigeration minimize energy waste and noise, while heat pump technology in dryers radically reduces electricity consumption compared to traditional heating elements. Advanced sensing technologies are also vital; these sensors allow washing machines to precisely determine load size, fabric type, and required detergent amount, optimizing water usage and cycle performance. The adoption of environmentally friendly refrigerants (like R600a and R290) is also a crucial technological shift, replacing older, high Global Warming Potential (GWP) alternatives to meet global climate agreements.

Material science and manufacturing processes also contribute heavily to the technological landscape. Manufacturers are leveraging anti-microbial coatings and advanced insulation materials to enhance hygiene and performance retention over time, particularly in refrigeration units. Simultaneously, the manufacturing process is increasingly reliant on digitalization and robotics (Industry 4.0 concepts) to achieve higher precision, faster production cycles, and greater customization capacity. This investment in advanced manufacturing is essential for handling the increasing complexity of sophisticated electronic controls and integrated user interfaces that define premium modern appliances.

Market growth is primarily driven by three key factors: accelerated housing construction globally, particularly in developing economies; increasing consumer demand for energy-efficient and smart, connected appliances (IoT integration); and governmental regulations mandating higher efficiency standards and supporting infrastructure development.

The Refrigeration segment (including refrigerators and freezers) holds the largest market share globally due to its essential nature for food preservation in all climates and household types, coupled with ongoing innovation in inverter technology and smart food management features.

Smart technology, including AI integration and connectivity, generally introduces a premium price point due to the cost of sensors, microprocessors, and sophisticated software R&D. However, competitive pressure is gradually moving basic connectivity features into mid-range models, making smart functionality more accessible.

The main challenges include managing volatile global supply chains and the resultant high costs of raw materials (steel and copper), meeting increasingly strict regulatory demands for energy efficiency and e-waste management, and mitigating cybersecurity risks associated with IoT-enabled devices.

Yes, the Asia Pacific region is expected to maintain its market dominance due to its demographic advantages, rapid urbanization, rising middle-class disposable incomes, and high volume of new household formation, ensuring sustained high demand for both first-time purchases and subsequent upgrades.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.