ID : MRU_ 433197 | Date : Dec, 2025 | Pages : 249 | Region : Global | Publisher : MRU

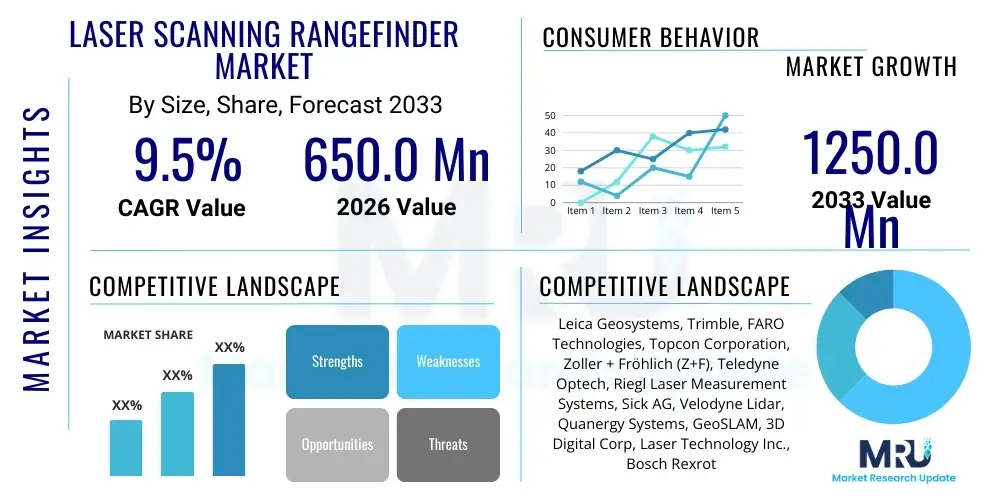

The Laser Scanning Rangefinder Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 9.5% between 2026 and 2033. The market is estimated at USD 650.0 Million in 2026 and is projected to reach USD 1250.0 Million by the end of the forecast period in 2033.

The Laser Scanning Rangefinder Market encompasses advanced optical measurement devices utilizing pulsed or continuous laser light to accurately determine distances and create high-resolution three-dimensional point clouds of objects or environments. These instruments combine the principles of ranging (distance measurement) with scanning mechanisms to capture millions of data points rapidly, essential for applications requiring precise spatial awareness and digital modeling. Key products include terrestrial laser scanners (TLS), mobile laser scanners (MLS), and airborne laser scanners (ALS), each tailored for specific operational ranges and mobility requirements.

Major applications driving the demand for laser scanning rangefinders include industrial metrology, where sub-millimeter precision is necessary for quality control and assembly verification; civil engineering and construction, used extensively for Building Information Modeling (BIM), topographical mapping, and monitoring structural deformation; and military and defense sectors, primarily for reconnaissance, target acquisition, and guided systems. Furthermore, the rise of autonomous systems and sophisticated robotics in logistics and manufacturing is accelerating the adoption of these sensors for navigation and obstacle avoidance.

The core benefits derived from utilizing laser scanning rangefinders include significantly reduced data acquisition time compared to traditional surveying methods, enhanced safety by enabling remote measurements in hazardous or inaccessible areas, and the creation of comprehensive digital twins that facilitate better decision-making, predictive maintenance, and simulation. Driving factors include the global push towards digitalization in manufacturing and infrastructure, rapid advancements in LiDAR technology leading to smaller, lighter, and more cost-effective devices, and increasing regulatory requirements for precise documentation in construction and mining industries.

The Laser Scanning Rangefinder Market is experiencing robust growth fueled by the convergence of high-precision manufacturing demands and the proliferation of 3D data capture across infrastructure development. Business trends indicate a strong move toward integrating scanner technology with other positioning systems, such as Global Navigation Satellite Systems (GNSS) and Inertial Measurement Units (IMUs), enabling seamless mobile mapping solutions. Key market players are heavily investing in software platforms capable of handling massive point cloud datasets, emphasizing features like automated feature extraction, real-time processing, and cloud-based collaboration. The competition is centered not just on hardware specifications (range, accuracy, scanning speed) but increasingly on the efficiency and usability of the accompanying data processing ecosystem, driving partnerships between hardware manufacturers and specialized software developers.

Regionally, Asia Pacific (APAC) stands out as the fastest-growing market, propelled by massive government investments in smart city projects, infrastructure development, and industrial automation, particularly in countries like China, India, and Japan. North America and Europe maintain leading positions in terms of technological adoption and market maturity, driven by stringent quality standards in aerospace, automotive, and oil and gas sectors, and the widespread adoption of BIM workflows in construction. The focus in these regions is shifting towards compact, high-speed scanners suitable for unmanned aerial vehicles (UAVs) and autonomous vehicle integration.

Segment trends reveal that the terrestrial laser scanning segment dominates revenue due to its versatility and established use in surveying and metrology, while the mobile laser scanning segment is exhibiting the highest growth trajectory, benefiting from increased deployment in transportation corridor mapping and rapid city surveying. Furthermore, the pulse measurement technology segment is maintaining its prominence for long-range applications, but phase measurement technology is gaining ground in industrial settings requiring ultra-high precision and speed over shorter distances. The application segment growth is primarily led by the engineering and construction sector, which is increasingly reliant on 3D data for progress monitoring, volumetric analysis, and site planning efficiency.

User inquiries regarding AI's influence on the Laser Scanning Rangefinder Market predominantly revolve around three core themes: the automation of data processing, the real-time interpretation of complex scenes, and the enhancement of scanner performance. Users are keen to understand how AI-powered algorithms can drastically reduce the manual labor currently required for registering point clouds, filtering noise, and classifying objects (e.g., distinguishing between poles, vegetation, and ground). There is significant expectation that AI will transition 3D scanning from a data collection exercise to an instantaneous insights platform, particularly important for fast-moving applications like autonomous driving (LiDAR) and large-scale industrial inspection. Furthermore, users are questioning the potential for AI to optimize scanner hardware operation dynamically, adjusting settings like laser power and scanning density based on environmental conditions or target characteristics, thereby maximizing efficiency and data quality in the field.

The integration of artificial intelligence and machine learning (ML) is fundamentally transforming the value proposition of laser scanning rangefinders, moving them beyond mere measurement tools into intelligent sensory systems. ML algorithms are now critical components in the post-processing pipeline, enabling automated recognition of features and semantics within dense point cloud datasets. This automation accelerates the extraction of deliverables—such as generating 2D floor plans from scans, calculating volumes, or identifying defects—which previously required hours of specialized human expertise. By significantly lowering the barrier to point cloud utilization, AI integration is widening the addressable market, making sophisticated 3D data accessible to non-surveying professionals.

The impact extends directly to sensor fusion and real-time operational efficiency. Deep learning models are being utilized to enhance the filtering of atmospheric noise and motion artifacts in high-speed mobile scanning, leading to cleaner data capture. For manufacturers, AI-driven feedback loops allow for predictive maintenance and calibration adjustments. For end-users, especially in robotics and autonomous systems (where laser scanning rangefinders are often synonymous with LiDAR), AI is essential for instant decision-making, allowing vehicles or drones to navigate complex, dynamic environments safely and effectively by classifying objects and predicting movements in real time, pushing the technological boundary from passive data capture to active, cognitive sensing.

The market is predominantly driven by the accelerating demand for digital twin creation across asset lifecycle management and the critical need for high-accuracy data in industrial quality control, offset by the challenges associated with high initial capital investment and the complexity of managing large datasets. Opportunities lie in the miniaturization of sensors for integration into handheld devices and consumer electronics, alongside expansion into emerging markets such as precision agriculture and renewable energy infrastructure inspection. These forces create a dynamic environment where technological innovation in sensor hardware and processing software determines competitive success and market penetration, especially in sectors sensitive to cost versus accuracy trade-offs.

Drivers: Key drivers include the mandatory adoption of Building Information Modeling (BIM) methodologies in global construction projects, which necessitates accurate 3D spatial data capture throughout the project lifecycle. Additionally, the proliferation of autonomous vehicles, robotics, and industrial automation (Industry 4.0) relies heavily on reliable 3D vision systems provided by laser scanning rangefinders. Continuous technological advancements, such as increased scanning speed, reduced noise, and extended effective range, further enhance the utility and ROI of these systems, encouraging broader enterprise adoption.

Restraints: Significant restraints impede market growth, primarily the substantial initial cost of high-specification laser scanning equipment and the associated professional software required for data processing. Furthermore, the inherent technical challenge of accurately scanning highly reflective, transparent, or dark surfaces can limit performance in specific industrial environments. The need for highly skilled technicians to operate, calibrate, and interpret complex point cloud data also poses a persistent bottleneck, particularly in developing economies, driving up operational costs.

Opportunities: Major opportunities stem from the potential for integrating laser scanning technology into unmanned aerial vehicles (UAVs) and drones, enabling rapid and safe large-area mapping, especially in difficult terrain. The untapped potential in mass-market applications, such as security surveillance, Virtual Reality (VR), and Augmented Reality (AR) content creation, offers future diversification. Moreover, the refinement of cloud-based processing and storage solutions is making the management of large point clouds more feasible, unlocking opportunities for pay-per-use service models and wider small business adoption.

Impact Forces: The primary impact force is technological evolution, specifically the rapid reduction in the cost-per-point of LiDAR sensors driven by automotive industry investments. This downward price pressure is making high-accuracy scanning accessible to mid-tier construction and engineering firms. Secondly, the increasing regulatory requirement for infrastructure safety checks and asset verification mandates the use of reliable digital documentation, forcing compliance across critical infrastructure sectors globally. These combined forces dictate a shift toward more integrated, user-friendly, and subscription-based 3D data solutions.

The Laser Scanning Rangefinder Market is segmented based on critical technical characteristics including measurement method, deployment platform, range capability, and end-use application. Analyzing these segments provides a nuanced understanding of market dynamics, revealing which technologies are gaining traction and which sectors are driving the highest volume and value. The segmentation highlights the market’s technological diversity, ranging from highly specialized, long-range pulsed systems utilized in aerial surveying to compact, high-frequency phase measurement systems essential for short-range industrial automation and metrology. The performance requirements dictated by specific application environments—such as marine environments versus indoor factory floors—shape the dominance of respective segments, influencing manufacturer R&D focus.

The segmentation by Type, specifically distinguishing between Pulse-based and Phase-based technologies, remains crucial as it directly relates to the balance between range (Pulse) and precision/speed (Phase). The deployment platform segment (Terrestrial, Mobile, Airborne) reflects the operational requirements of end-users; the shift towards Mobile and Airborne systems signifies the market demand for speed and wide-area coverage, moving away from static, ground-based measurements. Furthermore, the segmentation by Application underscores the market’s reliance on capital expenditure sectors, with Engineering & Construction and Industrial Metrology consistently representing the largest consumers of high-fidelity 3D data capture technology globally.

Geographic segmentation is vital, identifying regional demand patterns where mature markets (North America, Europe) focus on advanced integration and automation using these scanners, while emerging markets (APAC, MEA) emphasize rapid infrastructure build-out and large-scale resource mapping projects. Understanding this multilayered structure allows stakeholders to align their product offerings, sales channels, and pricing strategies effectively to address the distinct needs and growth drivers present within each segment and sub-segment, ensuring maximized market penetration and resource allocation.

The value chain for the Laser Scanning Rangefinder Market is characterized by a high degree of technological specialization across all phases, starting from upstream component manufacturing through to downstream service provision. Upstream activities involve the highly specialized production of core components, including high-power semiconductor lasers (often fiber or diode lasers), precision optical mirrors and scanning mechanisms (e.g., MEMS mirrors or rotational prisms), and high-speed detection systems (e.g., avalanche photodiodes or SPAD arrays). Suppliers in this tier focus heavily on miniaturization, power efficiency, and increasing the pulse repetition rate, as these parameters directly influence the performance and size of the final rangefinder unit. The reliance on advanced optics and sophisticated electronics means the upstream segment is concentrated among a few global specialized suppliers, creating critical dependency.

The midstream phase, dominated by the original equipment manufacturers (OEMs), involves the integration of these sophisticated components, system calibration, and packaging. This stage also includes the crucial development of proprietary firmware and control software that dictates the scanner's operational efficiency, data quality, and ease of use. OEMs invest significantly in intellectual property related to noise reduction algorithms and data synchronization technologies (e.g., coordinating laser pulses with GNSS/IMU data for mobile systems). Differentiation at this stage is achieved through superior system reliability, certified accuracy standards, and the robustness of the accompanying software suite.

Downstream activities center on distribution channels and end-user services. Direct distribution is common for high-value contracts with large industrial and defense clients, ensuring specialized consultation and integration support. Indirect distribution utilizes regional distributors, value-added resellers (VARs), and system integrators who customize the hardware/software package for niche applications like archaeology or specialized manufacturing inspection. Crucially, the downstream segment includes professional services—3D scanning service providers who offer data capture and processing on a project basis, democratizing access to the technology for organizations unwilling or unable to make the large initial capital investment. The profitability in the downstream is increasingly shifting from hardware sales to recurring software licenses and professional service contracts.

Potential customers for Laser Scanning Rangefinders span diverse high-capital and high-precision industries that require accurate dimensional data capture and spatial awareness. The primary end-users are professional surveyors and civil engineering firms who utilize the technology for topographical surveys, as-built documentation, and infrastructure planning, increasingly mandated by governmental digitization efforts. Another critical customer segment is the industrial metrology sector, encompassing aerospace, automotive, and heavy machinery manufacturers, who employ these rangefinders for quality control, deviation analysis, reverse engineering, and automated production line monitoring, ensuring adherence to strict dimensional tolerances.

Government and public sector entities constitute a substantial customer base, including military and defense organizations for reconnaissance and target acquisition systems, public works departments for infrastructure asset management (roads, bridges, utilities), and governmental mapping agencies for large-scale geospatial data acquisition (e.g., national elevation models). The energy and utilities sector, including oil and gas facilities and nuclear power plants, uses rangefinders for remote inspection and maintenance planning in hazardous environments, reducing safety risks and downtime. Furthermore, academic research institutions, particularly in geological sciences, archaeology, and remote sensing, purchase these systems for advanced scientific data collection.

Emerging customers include companies specializing in autonomous navigation and robotics, where laser scanning (LiDAR) is a core sensor technology for simultaneous localization and mapping (SLAM), essential for self-driving cars, delivery robots, and industrial AGVs. Architectural design firms and cultural heritage preservationists also rely on these scanners to accurately digitize historic structures for restoration or virtual display. The common need across all these customer segments is the requirement for rapid, non-contact measurement that provides verifiable, highly detailed 3D documentation, facilitating operational efficiency and risk mitigation in complex projects.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 650.0 Million |

| Market Forecast in 2033 | USD 1250.0 Million |

| Growth Rate | 9.5% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Leica Geosystems, Trimble, FARO Technologies, Topcon Corporation, Zoller + Fröhlich (Z+F), Teledyne Optech, Riegl Laser Measurement Systems, Sick AG, Velodyne Lidar, Quanergy Systems, GeoSLAM, 3D Digital Corp, Laser Technology Inc., Bosch Rexroth, Jenoptik, Hilti Corporation, Hemisphere GNSS, YellowScan, Phoenix Lidar Systems, Cepton Technologies. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological landscape of the Laser Scanning Rangefinder Market is characterized by intense innovation focused on increasing resolution, speed, and accuracy while simultaneously reducing size and power consumption. The fundamental technology relies on Light Detection and Ranging (LiDAR), implemented primarily through Time-of-Flight (ToF) for long-range performance or Phase-Shift methods for high-accuracy, short-range industrial applications. Recent advancements include the shift towards solid-state LiDAR, eliminating moving parts (like rotating mirrors), which drastically improves durability, reduces manufacturing costs, and enables integration into smaller form factors, essential for automotive and consumer electronics applications. Furthermore, Frequency Modulated Continuous Wave (FMCW) technology is gaining prominence as it offers superior immunity to ambient light interference and provides both distance and velocity information for every measured point, a crucial advantage in dynamic environments.

Data handling and processing represent another core technological frontier. The raw output of modern scanners is extremely large point clouds (often billions of points), requiring sophisticated software solutions for efficient consumption. Key developments include enhanced simultaneous localization and mapping (SLAM) algorithms, particularly crucial for mobile and handheld scanners, allowing accurate positioning and mapping without reliance on external GNSS signals in indoor or GPS-denied environments. Cloud-based computing platforms are becoming standard, enabling remote processing, storage, and collaborative access to large datasets, significantly reducing the hardware requirements and computational burden on field teams and individual users.

The integration of multisensory data is paramount. High-end laser scanning rangefinders are increasingly packaged with high-resolution digital cameras and thermal sensors to colorize the point cloud, adding visual context and improving object recognition through AI. Furthermore, inertial measurement units (IMUs) are mandatory components in mobile and airborne systems, ensuring precise orientation and trajectory tracking, which is essential for accurate geospatial referencing of the collected data points. The future technology direction involves increasing spectral sensitivity (multi-spectral LiDAR) to capture material properties and better differentiate objects, moving the technology closer to truly cognitive sensing platforms.

ToF (Pulse Measurement) rangefinders measure the time taken for a single laser pulse to return, offering superior long-range capability (hundreds of meters) crucial for aerial and external surveying. Phase-Shift (Continuous Wave) scanners measure the phase difference between the emitted and returned beam, providing ultra-high precision and speed, making them preferred for short-range industrial metrology and highly detailed indoor scanning.

LiDAR (Light Detection and Ranging) is the core technology underlying most laser scanning rangefinders. While all laser scanning rangefinders use laser light to determine distance and 3D position, the term LiDAR is often specifically used to denote the sensor systems deployed in autonomous vehicles, drones (UAVs), and mobile mapping solutions, emphasizing the collection of massive, georeferenced point clouds.

The primary driver is the demand for speed and efficiency in large-area data capture. MLS systems, mounted on vehicles or backpacks, drastically reduce the time required to survey transportation corridors, railways, and urban environments compared to traditional static terrestrial scanning, increasing productivity and lowering overall project costs, supported by sophisticated SLAM algorithms.

Building Information Modeling (BIM) mandates the creation and management of digital representations of physical and functional characteristics of places. Laser scanning rangefinders are essential tools for BIM workflows, providing accurate as-built data crucial for clash detection, progress monitoring, quality assurance, and comparison against design models, ensuring projects adhere to digital design specifications.

Yes, the high initial capital investment remains a significant restraint, particularly for small and medium-sized enterprises. However, this barrier is being mitigated by two trends: the emergence of lower-cost, solid-state LiDAR components driven by the automotive sector, and the increasing availability of affordable rental options and pay-per-use scanning service contracts, broadening market accessibility.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.