ID : MRU_ 393785 | Date : May, 2025 | Pages : 346 | Region : Global | Publisher : MRU

The LCD Glass Substrate market is poised for significant growth from 2025 to 2032, driven by a projected Compound Annual Growth Rate (CAGR) of 5%. This robust expansion stems from several key factors. Firstly, the ever-increasing demand for high-resolution displays in various electronic devices, including televisions, laptops, and monitors, fuels the need for advanced LCD glass substrates. Technological advancements in display technology, such as the development of ultra-high-definition (UHD) and 8K displays, are pushing the boundaries of screen resolution and visual quality, consequently boosting the demand for larger and higher-quality glass substrates. Furthermore, the miniaturization of electronics and the rise of foldable and flexible displays necessitate innovative glass substrate manufacturing processes and materials, contributing to market dynamism. The LCD Glass Substrate market also plays a crucial role in addressing global challenges related to energy efficiency. Advances in LCD technology, such as improved backlighting and power management, are reducing the overall energy consumption of electronic devices, aligning with global sustainability goals. The expanding adoption of smart homes and the Internet of Things (IoT) further amplifies the markets growth trajectory, as these applications require numerous displays integrated into various devices and appliances. The trend towards larger screen sizes, particularly in televisions and monitors, significantly contributes to the increased demand for larger-sized glass substrates. Moreover, the global rise in disposable income and increased consumer spending power, particularly in developing economies, is boosting demand for premium electronics incorporating high-quality LCD displays. The continuous quest for improved visual clarity and immersive viewing experiences drives innovation within the LCD glass substrate market, thus ensuring its sustained growth.

The LCD Glass Substrate market is poised for significant growth from 2025 to 2032, driven by a projected Compound Annual Growth Rate (CAGR) of 5%

The LCD Glass Substrate market encompasses the production and supply of high-quality glass substrates used in the manufacturing of Liquid Crystal Displays (LCDs). This market incorporates various technologies involved in glass substrate manufacturing, including float glass production, precision cutting, and surface treatment processes. The applications span a wide range of industries, primarily focusing on consumer electronics, such as televisions, monitors, laptops, tablets, and smartphones. Furthermore, the market serves the commercial and industrial sectors, providing glass substrates for displays in ATMs, point-of-sale systems, and industrial control panels. The markets significance lies within the broader context of the global electronics industry. LCD technology remains a dominant force in display technology, particularly in larger screen applications, despite the emergence of OLED and other competing technologies. The continuous advancements in LCD technology, coupled with its cost-effectiveness compared to OLED, maintain its relevance and market share. The global trend towards improved display quality, driven by consumer preference for high-resolution and immersive viewing experiences, heavily influences the growth of the LCD Glass Substrate market. The market is also inextricably linked to global supply chain dynamics, with manufacturing concentrated in key regions such as Asia. Understanding the nuances of this supply chain, including raw material availability, manufacturing capacity, and geopolitical factors, is crucial in evaluating the markets future prospects. The continued innovation in LCD technology, alongside evolving consumer demands and technological advancements, makes the LCD Glass Substrate market a significant component of the larger global electronics landscape.

The LCD Glass Substrate market refers to the commercial sector involved in the manufacturing, supply, and distribution of the foundational glass sheets used in the creation of Liquid Crystal Displays (LCDs). These glass substrates are the base material onto which the liquid crystal layer, color filters, and other components are applied to form a functional LCD panel. The market encompasses various stages, from the initial raw material sourcing (primarily silica sand) to the final processing of the glass substrates to meet stringent quality and dimensional specifications. Crucial components include the glass itself, characterized by its purity, flatness, and dimensional accuracy. the various surface treatments and coatings applied to enhance optical performance and durability. and the processes involved in cutting and shaping the glass into precisely sized sheets suitable for LCD assembly. Key terms related to this market include: Generation size (Gen 8, Gen 7, etc.): This refers to the size of the glass substrate produced, impacting production efficiency and yield. Float glass process: The primary manufacturing method for producing flat glass. Surface treatment: Processes such as etching, coating, and polishing to enhance the glasss properties. Substrate quality: Factors such as surface defects, flatness, and optical clarity. Yield: The percentage of usable glass substrates produced relative to the total glass manufactured. Anisotropy: Variations in properties depending on direction. Defect density: The number of imperfections per unit area. Thickness uniformity: Consistency of thickness across the substrate. Optical transmittance: Ability of the glass to transmit light. Understanding these terms is essential for comprehending the technological intricacies and market dynamics within the LCD Glass Substrate sector.

The LCD Glass Substrate market can be segmented based on type, application, and end-user. These segments reflect the diversity of the market and the varying demands of different applications.

Gen. 8 and above: These larger substrates offer higher production efficiency and are typically used for larger displays like high-resolution televisions and large-format monitors. The increased efficiency and yields lead to lower costs per unit area, making this segment attractive despite higher initial investment. This segment benefits from economies of scale and ongoing technological refinements leading to improvements in yield and quality.

Gen. 7: This generation offers a balance between production efficiency and cost, making it suitable for a wide range of applications, including televisions, monitors, and large tablets. It serves as a crucial segment due to its versatility and relatively mature technology, ensuring reliable supply and competitive pricing.

Gen. 6, Gen. 5.5, Gen. 5, Gen. 4 and below: These smaller-sized substrates are used for smaller displays like smartphones, laptops, and smaller monitors. While the demand for smaller substrates remains, the focus is shifting towards larger sizes, thus making this segment more price-competitive.

Televisions: This segment remains a significant driver of demand, especially for larger-sized displays with high resolutions. The ongoing trend towards bigger screen sizes and improved picture quality fuels continuous growth in this application segment.

Monitors: The demand for high-quality monitors for professional use and gaming is a crucial growth engine. The focus on higher resolution and refresh rates influences the demand for higher-quality glass substrates within this sector.

Laptops: While the growth rate might be slower compared to televisions and monitors, the consistent demand for high-resolution and portable displays ensures sustained market share for this application.

The major end-users include manufacturers of LCD panels, which then supply to Original Equipment Manufacturers (OEMs) of consumer electronics. Government and institutional procurement plays a relatively smaller role, while individuals primarily consume through the purchase of finished electronic devices.

| Report Attributes | Report Details |

| Base year | 2024 |

| Forecast year | 2025-2032 |

| CAGR % | 5 |

| Segments Covered | Key Players, Types, Applications, End-Users, and more |

| Major Players | Corning, AGC, NEG, Tunghsu Optoelectronic, AvanStrate, IRICO, CGC, LG Chem |

| Types | Gen. 8 and above, Gen. 7, Gen. 6, Gen. 5.5, Gen. 5, Gen. 4 and below |

| Applications | Televisions, Monitors, Laptops |

| Industry Coverage | Total Revenue Forecast, Company Ranking and Market Share, Regional Competitive Landscape, Growth Factors, New Trends, Business Strategies, and more |

| Region Analysis | North America, Europe, Asia Pacific, Latin America, Middle East and Africa |

Several factors drive the growth of the LCD Glass Substrate market. These include technological advancements in LCD display technologies, such as higher resolutions (UHD, 8K), improved color gamut, and higher refresh rates. the increasing demand for larger screen sizes across various electronic devices. government policies promoting the growth of domestic electronics manufacturing in several countries. the rising popularity of smart TVs and gaming monitors. and the continuous integration of displays in various appliances as a part of the Internet of Things (IoT).

Challenges include the high initial investment required for setting up advanced glass substrate manufacturing facilities. competition from other display technologies such as OLED and QLED. the impact of geopolitical factors and trade disputes on raw material supply and manufacturing operations. and fluctuations in the price of raw materials, especially silica sand.

Growth prospects lie in the development of innovative glass substrate materials with improved optical properties, higher durability, and lower manufacturing costs. the expansion into new applications such as augmented reality (AR) and virtual reality (VR) devices. the integration of advanced features such as touch-sensitive surfaces. and the focus on sustainable manufacturing practices to reduce environmental impact.

The LCD Glass Substrate market faces several challenges that could impact its growth trajectory. One major challenge is the intense competition from emerging display technologies such as OLED and MicroLED. These technologies offer superior picture quality, better contrast ratios, and thinner form factors, posing a significant threat to the continued dominance of LCD technology. The high capital expenditure required to establish and maintain advanced manufacturing facilities is another critical barrier to entry, limiting the number of players in the market and creating potential for oligopolies. Furthermore, the market is susceptible to fluctuations in raw material prices, especially silica sand, a primary component in glass manufacturing. Price volatility can significantly impact production costs and profitability. Geopolitical factors and international trade regulations can also disrupt the supply chain, potentially leading to shortages and price increases. The industry also needs to address environmental concerns associated with glass manufacturing, including energy consumption and waste management. Meeting increasingly stringent environmental regulations requires significant investments in cleaner production technologies. Finally, technological advancements are constantly driving the need for higher quality and more sophisticated glass substrates, requiring continuous R&D investments to stay competitive. Effectively navigating these challenges is crucial for continued growth and market leadership in the LCD Glass Substrate industry.

Key trends include the increasing adoption of larger generation glass substrates for improved production efficiency. the development of specialized glass substrates with enhanced optical properties for improved display performance. the growing demand for ultra-high-definition (UHD) and 8K displays. and the emergence of flexible and foldable display technologies, requiring innovative glass substrate designs and manufacturing processes.

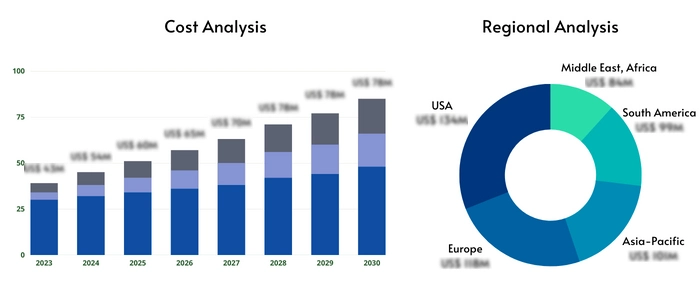

Asia, particularly China, South Korea, and Taiwan, dominates the LCD Glass Substrate market due to the concentration of major manufacturers and a robust electronics manufacturing ecosystem. North America and Europe have a smaller share but represent important markets for the consumption of LCD-based products. Latin America, the Middle East, and Africa are emerging markets with growing demand, although their share remains relatively small at present. The dynamics in each region are influenced by factors such as manufacturing capacity, government policies supporting the electronics industry, consumer purchasing power, and the availability of skilled labor. For instance, government incentives and investments in infrastructure have played a significant role in driving growth in Asia. In contrast, North America and Europe focus more on high-value-added products and advanced display technologies, while developing regions are characterized by increasing affordability and rising adoption of electronic devices.

The projected CAGR is 5%.

Key trends include the adoption of larger generation substrates, development of enhanced optical properties, demand for UHD and 8K displays, and the emergence of flexible displays.

Gen 8 and above substrates are gaining popularity due to their higher production efficiency, while Gen 7 remains a significant segment due to its versatility.

Competition from OLED and other technologies, high capital expenditures, raw material price volatility, geopolitical factors, and environmental regulations are key challenges.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.