ID : MRU_ 432973 | Date : Dec, 2025 | Pages : 258 | Region : Global | Publisher : MRU

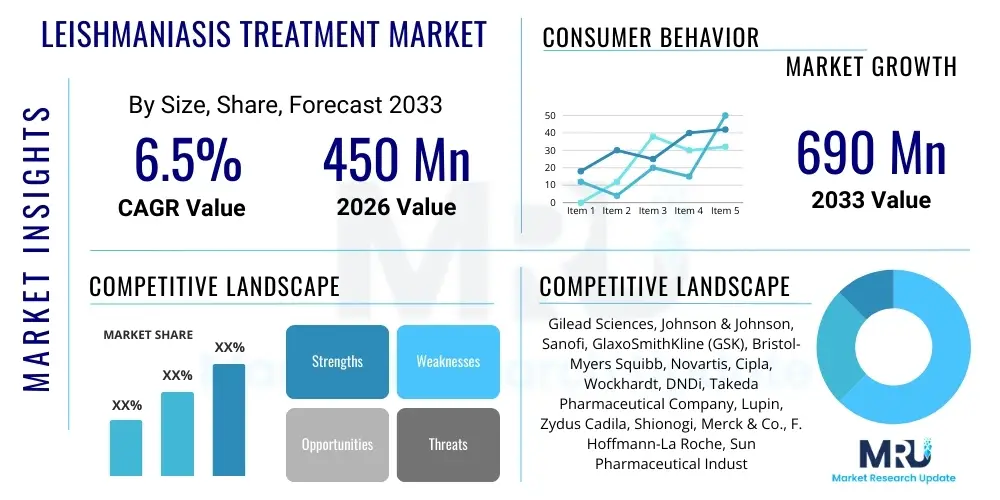

The Leishmaniasis Treatment Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.5% between 2026 and 2033. The market is estimated at USD 450 Million in 2026 and is projected to reach USD 690 Million by the end of the forecast period in 2033.

The Leishmaniasis Treatment Market encompasses the pharmaceutical and diagnostic solutions utilized to manage and eradicate leishmaniasis, a complex parasitic disease caused by protozoa of the genus Leishmania and transmitted through the bite of infected sandflies. The market includes antileishmanial drugs, such as pentavalent antimonials, amphotericin B, miltefosine, and paromomycin, as well as novel therapeutics currently in development. These treatments are essential due to the diverse clinical manifestations of the disease, ranging from cutaneous (CL), which causes skin sores, to visceral (VL) or kala-azar, which is fatal if left untreated. The growing disease burden, especially in neglected tropical disease (NTD) regions across Asia, Africa, and Latin America, mandates continuous investment in accessible and effective treatment regimens, propelling market expansion.

Major applications for leishmaniasis treatments center around three primary disease forms: visceral leishmaniasis, which requires systemic and potent drugs due to its severity; cutaneous leishmaniasis, often managed with localized or shorter-course systemic treatments; and mucocutaneous leishmaniasis, which necessitates aggressive therapy due to destructive mucosal lesions. The inherent benefits of effective treatment include significant reduction in patient morbidity and mortality, prevention of disease transmission, and substantial cost savings associated with long-term disability management. Furthermore, the development of oral treatments, such as miltefosine, has revolutionized patient compliance and decentralized care, shifting treatment paradigms away from purely injectable regimens that require intensive healthcare infrastructure.

Driving factors for this specialized market segment are multifaceted, primarily influenced by governmental and non-governmental organization (NGO) initiatives aimed at NTD elimination, improved surveillance mechanisms leading to better case reporting, and climatic changes expanding the geographical range of the sandfly vector. Increased research and development funding for neglected diseases, often channeled through public-private partnerships (PPPs), are accelerating the discovery of drugs with fewer side effects and shorter treatment durations, addressing the critical issue of drug toxicity prevalent in older therapies like pentavalent antimonials. However, market growth is often constrained by high drug costs, the emergence of drug resistance, and the overall lack of adequate healthcare infrastructure in highly endemic areas, presenting a challenging but necessary environment for therapeutic innovation.

The Leishmaniasis Treatment Market is characterized by sluggish growth in mature pharmaceutical segments but robust expansion in novel therapeutic research driven by urgent public health needs. Current business trends heavily favor the transition toward oral, shorter-course treatments, reducing the reliance on highly toxic, long-duration intravenous or intramuscular regimens. Strategic collaborations between multinational pharmaceutical companies, academic institutions, and organizations like the WHO and DNDi (Drugs for Neglected Diseases initiative) are crucial for funding the development and ensuring the accessibility of new drugs. Key segment trends indicate a shift in market share toward liposomal amphotericin B (L-AmB) due to its higher efficacy and lower toxicity profile compared to traditional amphotericin B, particularly for visceral leishmaniasis. Furthermore, the market is seeing increased focus on combination therapies aimed at mitigating drug resistance and reducing overall treatment duration, a vital strategy in resource-limited settings.

Regional trends distinctly define the market landscape, with Asia Pacific (particularly the Indian subcontinent, which traditionally bears the largest burden of visceral leishmaniasis) serving as a critical consumption and distribution hub for first-line therapies. However, recent advances in elimination programs in countries like India, Bangladesh, and Nepal have shifted R&D attention towards regions experiencing increasing incidence, such as East Africa and parts of Latin America. The Americas, specifically Brazil and Peru, represent a significant market for cutaneous leishmaniasis treatments, fostering demand for localized treatments and topical formulations. Manufacturers are increasingly utilizing differential pricing strategies and donation programs to ensure drug availability in low- and middle-income countries (LMICs), balancing profitability concerns with global health responsibilities.

Segment trends underscore the strategic importance of diagnostics alongside therapeutics, especially the demand for rapid diagnostic tests (RDTs) for prompt case detection in field settings, which directly impacts the timely administration of treatment. The therapeutic segment is moving away from monotherapy, with combination regimens involving miltefosine and paromomycin gaining prominence in clinical guidelines. Overall, the market remains highly fragmented, heavily reliant on government procurement and NGO funding, and characterized by a high degree of regulatory intervention to ensure that life-saving treatments are both safe and affordable. The overarching trend is a concerted, global effort to transition Leishmaniasis from a debilitating neglected disease into a manageable or eliminated health concern through targeted, innovative, and accessible interventions.

User inquiries regarding the impact of Artificial Intelligence (AI) on the Leishmaniasis Treatment Market primarily revolve around how AI can accelerate drug discovery, optimize clinical trial design in endemic areas, and improve diagnostic accuracy and surveillance. Users are keen to understand if machine learning algorithms can identify new drug targets against the complex Leishmania parasite life cycle, particularly focusing on proteins involved in drug resistance or parasite metabolism. Concerns often center on data availability and quality in resource-limited settings, which are typically where leishmaniasis is most prevalent, and the ethical deployment of AI in marginalized communities. Expectations are high that AI tools could significantly reduce the time and cost associated with identifying lead compounds and predicting patient response to existing treatments, thereby addressing the persistent bottleneck in NTD R&D.

The Leishmaniasis Treatment Market is significantly influenced by a complex interplay of Drivers, Restraints, and Opportunities, collectively determining its growth trajectory and strategic landscape. A primary driver is the increasing global incidence and prevalence of the disease, exacerbated by climate change, urbanization, and displacement, which pushes endemic areas into new geographies, demanding broader therapeutic availability. Restraints largely center on the historical challenges inherent in treating NTDs, including the high toxicity and adverse side effect profiles of first-line drugs (like antimonials), the increasing incidence of drug resistance (especially to miltefosine in some regions), and the limited commercial incentive for pharmaceutical companies due to the disease predominantly affecting low-income populations. These restraints necessitate innovative public-private funding models to ensure sustained R&D efforts.

Opportunities for growth are concentrated in the development and adoption of novel, safer compounds, particularly those with oral bioavailability and short treatment courses, improving patient adherence and reducing healthcare costs. The rising acceptance and integration of highly effective but expensive therapies, such as liposomal amphotericin B (L-AmB), in national treatment guidelines, especially through differential pricing mechanisms, opens a premium segment within the essential medicines market. Furthermore, advancements in diagnostic technologies, specifically highly sensitive and specific non-invasive rapid tests, facilitate early and accurate diagnosis, significantly improving treatment outcomes and supporting mass screening programs necessary for elimination efforts, thereby driving demand for confirmed treatments.

Impact forces currently shaping the market include significant governmental and multilateral organization commitments (e.g., WHO’s 2030 Roadmap for NTDs), which guarantee sustained procurement and fund elimination campaigns, stabilizing demand for essential treatments. The growing influence of philanthropic organizations and product development partnerships (PDPs) like DNDi ensures that the pipeline for novel therapies remains active despite commercial disincentives. The high toxicity and difficulty of administering older treatments place immense pressure on manufacturers to prioritize safer formulations, with drug resistance further forcing the adoption of combination therapies. These forces create a market where innovation is compulsory, yet profitability is highly dependent on institutional purchasing power and centralized aid efforts.

The Leishmaniasis Treatment Market is systematically segmented based on various critical parameters including drug type, disease type, distribution channel, and route of administration, providing a nuanced understanding of procurement patterns and treatment preferences across different endemic regions. The segmentation by drug type reflects the evolution of treatment protocols, moving from traditional compounds toward modern, less toxic alternatives. Disease type segmentation is crucial as visceral leishmaniasis (VL) requires highly potent systemic treatments, driving the demand for injectable products, while cutaneous leishmaniasis (CL) often allows for topical or less intensive systemic interventions. This structural dissection of the market allows stakeholders, including policymakers and pharmaceutical companies, to target their resources effectively, ensuring the right treatments reach the most affected populations based on disease manifestation and severity.

The value chain for the Leishmaniasis Treatment Market begins with upstream activities dominated by active pharmaceutical ingredient (API) manufacturing and highly specialized research and development (R&D). R&D, often conducted through Product Development Partnerships (PDPs) and academic collaborations, focuses heavily on drug repurposing and synthesizing new chemical entities specific to Leishmania strains. Key upstream challenges involve maintaining high-quality manufacturing standards for potent drugs like L-AmB and securing regulatory approval for novel compounds in multiple jurisdictions simultaneously. Due to the high-risk, low-profit nature of NTD drug development, government grants and philanthropic funding play a disproportionate role in supporting the initial stages of the value chain compared to traditional pharmaceutical markets.

The midstream segment involves formulation, clinical trials, and finished drug production, where manufacturers convert APIs into injectable, oral, or topical dosage forms. Given that many treatments are complex (e.g., liposomal formulations requiring advanced technology), manufacturing capabilities are centralized among a few specialized producers. Distribution channels are highly bifurcated: Direct distribution is prevalent for high-volume purchases made by centralized bodies such as national health ministries (for mass elimination programs) and international organizations (WHO, MSF, etc.). These direct channels ensure essential medicines reach endemic areas at negotiated, affordable prices, often bypassing typical commercial markups. Indirect distribution involves traditional routes through wholesalers and hospital pharmacies, but this route is less dominant for core antileishmanial drugs procured specifically for public health campaigns.

Downstream analysis focuses on prescription and administration. In endemic regions, treatment decisions are often made at district or primary healthcare levels, sometimes under mobile clinic settings, highlighting the necessity for treatments that are stable, easy to store, and simple to administer (i.e., oral or short-course infusions). The ultimate end-users are the patients in these often resource-poor settings. The dominance of centralized procurement means that the downstream market is price-sensitive and volume-driven, with success measured not by peak sales but by compliance with global health metrics and elimination targets. Efficient inventory management and cold chain logistics for heat-sensitive drugs like L-AmB are crucial determinants of downstream success, directly impacting treatment effectiveness and reducing waste.

The primary customers and buyers in the Leishmaniasis Treatment Market are largely institutional, reflecting the status of leishmaniasis as a public health priority disease. The largest and most influential buyers are national governments and health ministries in endemic countries (e.g., India, Brazil, Sudan, Bangladesh), which procure drugs in bulk through tenders to supply national control and elimination programs. These entities prioritize low-cost, high-volume options and increasingly demand treatments aligning with WHO guidelines, favoring combination therapies to curb resistance.

A second major customer segment includes influential international non-governmental organizations (NGOs) and humanitarian aid bodies such as Médecins Sans Frontières (MSF) and the World Health Organization (WHO), often acting as central purchasing agents for emergency relief and sustained treatment delivery in conflict zones or difficult-to-reach populations. These organizations demand robust supply chain stability and treatments suitable for field conditions. Finally, Product Development Partnerships (PDPs) like DNDi act as early-stage customers, purchasing clinical batches and working with manufacturers to scale up production for new, patented treatments before handing off to governmental or aid agencies for sustained procurement.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 450 Million |

| Market Forecast in 2033 | USD 690 Million |

| Growth Rate | 6.5% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Gilead Sciences, Johnson & Johnson, Sanofi, GlaxoSmithKline (GSK), Bristol-Myers Squibb, Novartis, Cipla, Wockhardt, DNDi, Takeda Pharmaceutical Company, Lupin, Zydus Cadila, Shionogi, Merck & Co., F. Hoffmann-La Roche, Sun Pharmaceutical Industries, Bausch Health, Hetero Drugs, Alvogen, Fresenius Kabi. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological landscape of the Leishmaniasis Treatment Market is marked by innovation primarily focused on mitigating the severe side effects and logistical challenges associated with legacy treatments. The most significant technological advance is the proliferation of liposomal drug delivery systems, exemplified by Liposomal Amphotericin B (L-AmB). This technology encapsulates the active drug within lipid vesicles, dramatically reducing systemic toxicity and allowing for higher dosages while significantly improving drug targeting to the reticuloendothelial system where the parasite resides, leading to superior efficacy in visceral leishmaniasis treatment. Manufacturers are continually working on developing thermo-stable liposomal formulations that do not require strict cold-chain management, addressing a major logistical bottleneck in tropical, remote areas.

Beyond formulation science, technological efforts are directed toward developing completely new therapeutic classes. There is substantial preclinical and early clinical research utilizing high-throughput screening (HTS) of large compound libraries to identify novel chemical scaffolds that target unique metabolic pathways in the Leishmania parasite, often with an emphasis on compounds effective against drug-resistant strains. This includes exploring synthetic small molecules and repurposed drugs originally intended for fungal infections or cancer, seeking synergistic effects in combination regimens. The use of advanced computational chemistry and genomics is accelerating the identification of promising candidates that are potent, orally active, and exhibit low mammalian toxicity, crucial factors for patient compliance and safety in a public health setting.

A parallel technological focus exists within the diagnostics segment, essential for the effective deployment of treatments. The market is increasingly adopting highly sensitive immunochromatographic tests (ICTs) for detecting Leishmania-specific antibodies, particularly the rK39 rapid diagnostic test (RDT), which is pivotal for diagnosing visceral leishmaniasis in the field due to its simplicity and speed. Future technologies are exploring molecular diagnostics, such as affordable, portable PCR systems (like loop-mediated isothermal amplification or LAMP), which offer high accuracy for species identification and confirmation of cure, helping tailor treatment protocols and monitor drug resistance, thus reinforcing the overall effectiveness of the therapeutic market.

The WHO often recommends combination therapies utilizing Liposomal Amphotericin B (L-AmB) or a combination of Miltefosine and Paromomycin. L-AmB is increasingly preferred due to its high efficacy, reduced toxicity compared to older drugs like antimonials, and the feasibility of shorter treatment regimens, particularly in elimination programs.

Drug resistance, particularly noted against pentavalent antimonials and emerging resistance to Miltefosine in parts of India and Nepal, necessitates the continuous shift towards combination therapies and the development of new, structurally unique drug classes. This drives R&D investment and influences global procurement guidelines towards safer and more efficacious alternatives.

PPPs, such as those involving DNDi and major pharmaceutical companies, are crucial as they bridge the gap created by low commercial returns associated with Neglected Tropical Diseases (NTDs). They fund preclinical research, manage clinical trials, and establish preferential pricing and distribution mechanisms to ensure that new treatments are affordable and accessible in endemic, resource-limited settings.

Key logistical challenges include maintaining the cold chain for temperature-sensitive drugs like Liposomal Amphotericin B in remote, tropical regions lacking reliable electricity. Furthermore, distribution must navigate unstable environments and reach geographically dispersed populations affected by the disease, demanding specialized, robust, and centralized procurement and supply networks.

The Liposomal Amphotericin B segment, under the Drug Type segmentation, is projected to show robust growth. This is driven by its clinical superiority, WHO endorsement, and large-scale centralized procurement for elimination programs, despite its higher initial cost compared to generic alternatives.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.