ID : MRU_ 440555 | Date : Jan, 2026 | Pages : 243 | Region : Global | Publisher : MRU

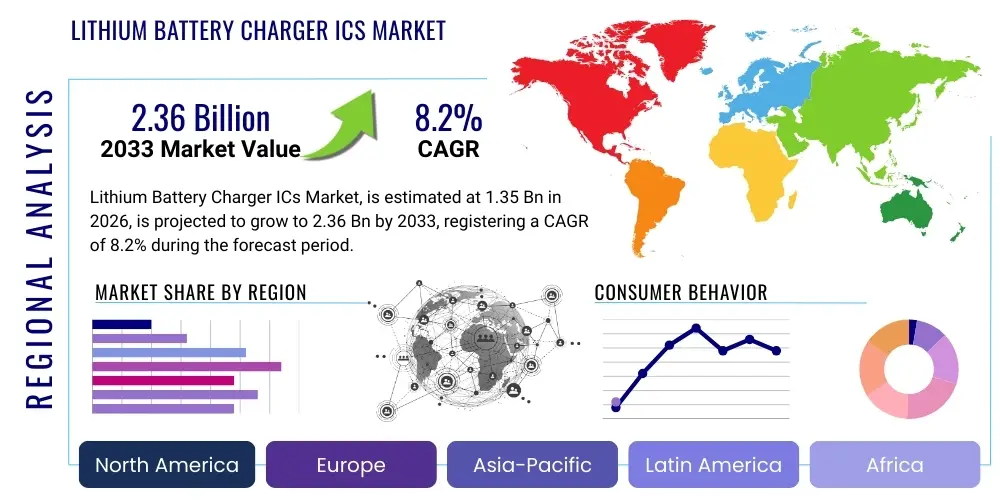

The Lithium Battery Charger ICs Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 8.2% between 2026 and 2033. The market is estimated at USD 1.35 Billion in 2026 and is projected to reach USD 2.36 Billion by the end of the forecast period in 2033.

The Lithium Battery Charger ICs market encompasses integrated circuits specifically designed to manage the charging and protection of lithium-ion and lithium-polymer batteries. These critical components are indispensable in a vast array of electronic devices, ensuring efficient power transfer, prolonged battery lifespan, and most importantly, operational safety. Charger ICs intelligently control current and voltage during the charging process, preventing overcharging, deep discharging, and overheating, which are crucial for the stability and longevity of lithium-based power sources. Their sophistication has grown significantly to meet the demands for faster charging, higher power density, and more compact designs across various applications.

The primary function of these ICs involves regulating the charge current and voltage precisely, adhering to the specific charging profile required by lithium-ion and lithium-polymer chemistries. This includes constant current (CC) and constant voltage (CV) phases, often coupled with pre-charge and termination algorithms. Beyond fundamental charging, modern Lithium Battery Charger ICs often integrate advanced features such as battery fuel gauging, temperature monitoring, cell balancing in multi-cell configurations, and various protection mechanisms including over-current, over-voltage, and short-circuit protection. These integrated functionalities enhance overall system reliability and user safety, making them integral to the design of battery-powered devices.

Major applications for Lithium Battery Charger ICs span across consumer electronics, including smartphones, tablets, laptops, wearables, and portable power banks, which demand high efficiency and compact form factors. The automotive sector, particularly in electric vehicles (EVs) and hybrid electric vehicles (HEVs), constitutes a rapidly expanding application area, requiring robust and high-power charging solutions. Industrial applications such as portable power tools, medical devices, robotics, and energy storage systems also rely heavily on these ICs for reliable power management. The benefits derived from these advanced ICs include enhanced battery safety, extended battery cycle life, faster charging times, and greater energy efficiency. Driving factors for market growth are primarily fueled by the pervasive adoption of portable electronic devices, the accelerating shift towards electric mobility, the proliferation of IoT devices, and the increasing global demand for efficient and safe energy storage solutions, all of which necessitate sophisticated battery management.

The Lithium Battery Charger ICs market is characterized by dynamic business trends driven by technological advancements and evolving consumer demands. Key trends include the continuous push for higher charging efficiency, enabling faster charge times while minimizing heat generation, alongside the miniaturization of IC packages to support sleeker device designs. There is a strong emphasis on integrating multiple functionalities into single chips, such as power delivery (PD) protocols, wireless charging capabilities, and advanced battery health monitoring, thereby reducing component count and simplifying system design. Furthermore, the development of charger ICs compatible with gallium nitride (GaN) and silicon carbide (SiC) power semiconductors is gaining traction, promising even greater efficiency and power density, particularly for high-power applications in automotive and industrial sectors. The market is also seeing increased adoption of programmable and intelligent charger ICs that can adapt to different battery chemistries and charging conditions, offering greater flexibility and optimized performance.

Regional trends indicate a significant dominance of the Asia Pacific (APAC) region, primarily due to its robust manufacturing ecosystem for consumer electronics and its rapidly expanding electric vehicle market, especially in countries like China, South Korea, and Japan. APAC serves as both a major production hub and a substantial consumer market for battery-powered devices. North America and Europe are pivotal regions for innovation and high-value applications, driving demand for advanced charger ICs in automotive, medical, and industrial sectors, with a strong focus on regulatory compliance and premium performance. The increasing investment in renewable energy storage solutions and smart grid infrastructure in these regions also contributes to the demand for sophisticated battery management systems incorporating these ICs. Emerging economies in Latin America, the Middle East, and Africa are showing nascent but steady growth, driven by increasing smartphone penetration and gradual adoption of electric mobility and renewable energy initiatives, presenting future growth opportunities.

In terms of segment trends, the consumer electronics segment currently holds the largest market share, propelled by the relentless demand for smartphones, laptops, tablets, and a growing ecosystem of wearables and IoT devices that rely on compact and efficient charging solutions. This segment continually pushes for faster charging, smaller footprints, and enhanced safety features. The automotive segment is projected to exhibit the highest growth rate, primarily due to the global surge in electric vehicle adoption and the accompanying need for advanced, high-power battery management systems and charging infrastructure. Industrial applications, encompassing portable power tools, medical equipment, and large-scale energy storage, represent a stable and growing segment requiring highly reliable and rugged charger ICs. The trend across all segments is towards higher integration, greater intelligence, and improved power efficiency, reflecting a broader industry move towards more sustainable and high-performance battery solutions.

Users frequently inquire about how artificial intelligence can revolutionize the performance, safety, and lifespan of lithium batteries, specifically through the lens of charger ICs. Common questions revolve around AI's ability to optimize charging cycles, predict battery degradation, and enhance overall battery management systems. There's significant interest in whether AI can lead to truly "smart" charging, adapting to real-time conditions and user behavior. Users also express concerns about the complexity and cost implications of integrating AI into these specialized ICs, as well as the data privacy aspects associated with continuous battery monitoring. The overarching theme is an expectation that AI will unlock unprecedented levels of efficiency, safety, and longevity for lithium-ion batteries, transforming how devices are powered and maintained.

Based on these inquiries, the key themes summarizing user expectations about AI's influence in the Lithium Battery Charger ICs domain include the potential for intelligent, adaptive charging algorithms that go beyond traditional CC/CV methods. Users anticipate AI-driven systems to precisely manage power delivery based on battery health, ambient temperature, and usage patterns, thereby extending battery life and mitigating degradation. There's also a strong expectation for predictive analytics, where AI can forecast potential battery failures or capacity loss, enabling proactive maintenance or replacement. Furthermore, the integration of AI is seen as a pathway to more robust safety protocols, allowing charger ICs to detect and respond to anomalous conditions more effectively than traditional hardware-based protections. However, the practical implementation challenges, including computational overhead, data requirements, and validation processes, remain key areas of user interest and concern.

Ultimately, users envision AI-powered Lithium Battery Charger ICs as central to creating truly intelligent battery ecosystems. This involves not just optimizing the charging process itself, but also contributing to a broader understanding of battery performance throughout its lifecycle. The integration of machine learning could enable charger ICs to learn from historical data, dynamically adjust parameters for optimal energy efficiency, and provide richer diagnostic information to the end-user or system. The convergence of hardware innovation in charger ICs with sophisticated AI algorithms is expected to redefine the capabilities of battery-powered devices, offering unparalleled levels of performance, reliability, and user experience, while simultaneously addressing critical safety and environmental considerations related to battery usage and disposal.

The Lithium Battery Charger ICs market is significantly shaped by a confluence of driving forces, inherent restraints, and emerging opportunities, all interacting with various impact forces that influence competitive dynamics. A primary driver is the pervasive and increasing demand for portable electronic devices, ranging from smartphones and laptops to wearables and IoT gadgets, all powered by lithium-ion batteries requiring sophisticated charging management. The rapid growth of the electric vehicle (EV) market globally also acts as a monumental driver, necessitating high-power, efficient, and safe charging solutions for propulsion batteries. Furthermore, the burgeoning renewable energy sector, with its reliance on energy storage systems (ESS), and the continuous innovation in fast charging technologies are compelling market expansion. The desire for extended battery life, enhanced safety features, and compact designs across all applications further fuels the demand for advanced charger ICs.

However, the market also faces several notable restraints. The intense price competition among IC manufacturers often leads to reduced profit margins, particularly in the high-volume consumer electronics segment. The inherent technical complexity in designing charger ICs that balance efficiency, safety, and performance across diverse battery chemistries and application requirements poses a significant challenge. Supply chain disruptions, exemplified by recent global semiconductor shortages, can severely impact production and market availability. Moreover, the lack of universal standardization for charging protocols and battery management interfaces can create fragmentation and hinder widespread adoption of certain technologies. Regulatory compliance, especially concerning safety standards and environmental directives, adds another layer of complexity and cost for manufacturers.

Despite these restraints, abundant opportunities exist for market players. The continuous innovation in materials science, particularly the development of Wide Bandgap (WBG) semiconductors like Gallium Nitride (GaN) and Silicon Carbide (SiC), offers pathways for higher efficiency and power density in charger ICs. The expansion of wireless charging technologies beyond consumer electronics into automotive and industrial applications presents a substantial growth avenue. The development of intelligent, AI-powered battery management systems (BMS) integrated with charger ICs for predictive maintenance and optimized performance also offers significant differentiation. Moreover, the increasing global focus on sustainable energy solutions, including smart grids and energy harvesting systems, creates new niches for advanced, robust, and efficient battery charging and management solutions. These opportunities encourage investment in research and development and foster strategic partnerships.

The market is also influenced by several impact forces. The bargaining power of buyers, especially large OEMs in consumer electronics and automotive sectors, is high, driving down prices and demanding specific features. Conversely, the bargaining power of suppliers, particularly for critical raw materials and advanced semiconductor fabrication services, can impact production costs and lead times. The threat of new entrants is moderate, as the market requires significant R&D investment, specialized expertise, and established supply chains, creating barriers to entry. The threat of substitutes, while present (e.g., alternative battery chemistries or power delivery methods), is currently low for core lithium-ion charging functions due to their widespread adoption and performance advantages. Finally, the intense competitive rivalry among established players, driven by innovation and product differentiation, constantly pushes technological boundaries and market efficiency.

The Lithium Battery Charger ICs market is meticulously segmented to provide a granular understanding of its diverse landscape, reflecting variations in technology, application, battery types, and charging capabilities. This segmentation is crucial for stakeholders to identify specific market niches, tailor product development, and formulate targeted marketing strategies. The primary segmentation criteria often include the type of charger IC (e.g., linear, switching, wireless), the end-use application (e.g., consumer electronics, automotive, industrial), the specific battery chemistry it supports, and the charging current or number of cells it can manage. Each segment exhibits unique growth drivers, technological requirements, and competitive dynamics, contributing to the overall market complexity and opportunity. Understanding these segments is key to navigating the evolving demands of battery-powered devices and systems.

Further analysis of these segments reveals distinct trends. For instance, in the "type" segment, switching charger ICs dominate due to their higher efficiency, making them ideal for power-sensitive applications, while wireless charging ICs are experiencing rapid growth driven by convenience and new form factors. The "application" segment highlights the ongoing dominance of consumer electronics, though the automotive sector is poised for exponential growth, demanding rugged, high-power, and safety-certified solutions. Similarly, the "battery type" segment primarily focuses on Li-Ion and Li-Polymer, with emerging demand for LiFePO4 in specific industrial and energy storage applications. The increasing sophistication in battery technology necessitates charger ICs that are adaptable, intelligent, and capable of managing various cell configurations and charging currents effectively. This detailed segmentation enables market participants to address specific pain points and capitalize on high-growth areas.

The value chain for the Lithium Battery Charger ICs market begins with upstream activities focused on the procurement and processing of raw materials and the intricate design and manufacturing of the ICs themselves. This initial stage involves sourcing semiconductor-grade silicon wafers, various metals, and specialized chemicals essential for chip fabrication. Key players in this segment include material suppliers and highly specialized semiconductor foundries (fabs) that transform raw silicon into complex integrated circuits through processes like photolithography, etching, and deposition. Upstream analysis also covers the intellectual property and design houses that develop the core architectures, algorithms, and circuit layouts for these advanced charger ICs, often involving significant R&D investment to ensure efficiency, safety, and compliance with emerging standards. This stage is capital-intensive and requires significant technical expertise.

Following the manufacturing phase, the value chain progresses to the assembly, testing, and packaging of the charger ICs, which are then distributed to a wide array of customers. This midstream activity ensures that the manufactured dies are properly housed, protected, and verified for functionality and reliability before being integrated into larger electronic systems. The distribution channel plays a crucial role in connecting IC manufacturers with their diverse customer base. This typically involves a combination of direct sales from large semiconductor companies to major original equipment manufacturers (OEMs) for high-volume orders, and indirect channels through authorized distributors and electronic component wholesalers who serve a broader range of smaller to medium-sized enterprises and design houses. These distributors often provide technical support and supply chain logistics, making them indispensable for market penetration and customer reach. Online platforms and specialized component marketplaces are also gaining importance for smaller quantity orders and rapid prototyping.

The downstream activities involve the integration of these Lithium Battery Charger ICs into the final products that reach end-users. This includes a vast ecosystem of device manufacturers across consumer electronics (e.g., smartphone makers, laptop OEMs), automotive (e.g., EV manufacturers, automotive electronics suppliers), industrial equipment (e.g., power tool companies, medical device manufacturers), and energy storage system integrators. These customers incorporate the charger ICs into their battery management systems, power supply units, and embedded circuits to ensure the safe and efficient operation of their battery-powered products. The performance, reliability, and cost-effectiveness of the charger ICs directly impact the quality and competitiveness of these final products. The entire value chain is characterized by a high degree of specialization and collaboration, with each stage adding significant value through advanced technology, manufacturing precision, and efficient distribution networks to deliver innovative power management solutions to the global market.

The potential customers for Lithium Battery Charger ICs are incredibly diverse, encompassing nearly every sector that utilizes portable, cordless, or battery-dependent electronic devices and systems. At the forefront are manufacturers of consumer electronics, including global giants producing smartphones, tablets, laptops, and a rapidly expanding array of wearables like smartwatches and fitness trackers. This segment also extends to manufacturers of drones, virtual reality headsets, and various Internet of Things (IoT) devices such as smart home sensors and portable medical gadgets. These companies are constantly seeking smaller, more efficient, and feature-rich charger ICs to enhance user experience, enable faster charging, and maximize battery life in their increasingly compact and powerful products, making them a cornerstone customer base for the market.

Beyond consumer electronics, the automotive industry represents a rapidly growing and high-value customer segment. Electric Vehicle (EV) and Hybrid Electric Vehicle (HEV) manufacturers are major purchasers, requiring robust, high-power, and highly reliable charger ICs for their propulsion battery packs and auxiliary systems. This also includes suppliers of automotive infotainment systems, advanced driver-assistance systems (ADAS), and other in-car electronics that increasingly rely on complex battery management. The industrial sector forms another critical customer base, comprising manufacturers of portable power tools, industrial robots, medical devices (e.g., portable ventilators, diagnostic equipment), and large-scale energy storage systems (ESS) for grid applications and renewable energy integration. These customers prioritize durability, extended operational life, and strict safety compliance in their charger IC selections.

Furthermore, other significant end-users and buyers include telecommunications equipment manufacturers for base stations and network infrastructure backup power, aerospace and defense contractors for specialized portable military equipment and avionics, and even emerging markets like e-bike and e-scooter manufacturers. Companies developing backup power supplies, uninterruptible power supplies (UPS), and professional camera equipment also constitute vital customer segments. Essentially, any entity involved in the design, manufacturing, or integration of battery-powered solutions across a broad spectrum of industries, where efficient, safe, and reliable lithium battery charging is paramount, represents a potential customer for Lithium Battery Charger ICs. Their needs vary significantly, driving demand for a wide range of IC specifications, from low-power single-cell solutions to high-voltage, multi-cell configurations.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 1.35 Billion |

| Market Forecast in 2033 | USD 2.36 Billion |

| Growth Rate | 8.2% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces | >|

| Segments Covered | >|

| Key Companies Covered | Texas Instruments, Analog Devices, NXP Semiconductors, STMicroelectronics, Renesas Electronics, Infineon Technologies, ON Semiconductor, Qualcomm, Microchip Technology, Diodes Incorporated, Richtek Technology, Rohm Semiconductor, Semtech, Toshiba, Monolithic Power Systems (MPS), MaxLinear, Dialog Semiconductor (now Renesas Electronics), Alpha and Omega Semiconductor, Vishay Intertechnology, Maxim Integrated (now Analog Devices) |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The Lithium Battery Charger ICs market is at the forefront of power management innovation, driven by several key technological advancements aimed at improving efficiency, safety, and functionality. One of the most significant trends is the adoption of fast charging protocols, such as USB Power Delivery (USB-PD) and Qualcomm Quick Charge (QC), which require sophisticated charger ICs capable of dynamically negotiating voltage and current levels with the connected device. These protocols demand highly efficient switching topologies, advanced control algorithms, and robust protection features to manage higher power levels without compromising battery health or safety. The integration of USB-PD controllers directly into charger ICs is becoming increasingly common, simplifying system design and reducing component count for manufacturers of consumer electronics and other portable devices.

Another pivotal technological shift involves the increasing deployment of Wide Bandgap (WBG) semiconductors, particularly Gallium Nitride (GaN) and Silicon Carbide (SiC), in power management solutions. While primarily used in external power adapters and converters, their influence is extending to integrated charger ICs, especially for high-power applications in the automotive and industrial sectors. GaN and SiC devices offer superior switching speeds, lower conduction losses, and higher temperature operation compared to traditional silicon-based components, enabling significantly higher power density and efficiency in charger designs. This allows for smaller, lighter, and more efficient charging solutions, which are critical for electric vehicles and compact industrial equipment. The miniaturization trend is further supported by advanced packaging technologies like wafer-level chip-scale packages (WLCSP) and fine-pitch QFNs, enabling high integration in minimal footprints.

Furthermore, the evolution towards intelligent and integrated Battery Management Systems (BMS) is profoundly impacting charger IC design. Modern charger ICs are increasingly incorporating sophisticated features such as accurate battery fuel gauging, advanced cell balancing capabilities for multi-cell packs, and comprehensive diagnostics for monitoring battery health and predicting degradation. Wireless charging technologies, like those based on the Qi standard, also represent a significant segment of the market's technological landscape, with specialized receiver ICs capable of efficiently converting received electromagnetic energy into charging current. The convergence of these technologies, alongside innovations in digital control, communication interfaces (e.g., I2C, SPI), and fault detection mechanisms, is driving the development of highly integrated, adaptive, and secure Lithium Battery Charger ICs that are essential for the next generation of battery-powered devices and energy systems.

The global Lithium Battery Charger ICs market exhibits distinct regional dynamics, influenced by manufacturing capabilities, technological adoption rates, and economic development. Asia Pacific (APAC) stands as the undisputed leader in this market, driven by its expansive consumer electronics manufacturing base, particularly in countries like China, South Korea, Taiwan, and Japan. This region accounts for the majority of global production and consumption of smartphones, laptops, and wearables, which are major demand drivers for charger ICs. Furthermore, the rapid growth of the electric vehicle (EV) market in China and other Asian economies significantly boosts the demand for high-power, multi-cell charger ICs. Government initiatives supporting local semiconductor industries and renewable energy projects further solidify APAC's dominant position, making it a critical hub for both innovation and volume manufacturing in the market.

North America and Europe represent mature markets characterized by high technological adoption, strong R&D investments, and a focus on high-value applications. North America, with its robust automotive industry and leading technology companies, drives demand for advanced charger ICs in electric vehicles, data centers, and sophisticated industrial and medical equipment. The region's emphasis on fast charging standards and cutting-edge battery management systems also fuels innovation. Europe, similarly, boasts a strong automotive sector, particularly in Germany and France, alongside significant investments in industrial automation and renewable energy storage solutions. Both regions prioritize regulatory compliance, safety standards, and high-performance, pushing for charger ICs with advanced protection features, higher efficiency, and complex power delivery capabilities. These regions are key for premium and specialized charger IC solutions.

Latin America, the Middle East, and Africa (MEA) are emerging markets that are poised for considerable growth in the Lithium Battery Charger ICs sector, albeit from a smaller base. The increasing penetration of smartphones and other portable electronic devices, coupled with growing infrastructure development and a gradual shift towards electric mobility in major urban centers, are key growth catalysts. While manufacturing capabilities are less developed compared to APAC, these regions present significant opportunities for market expansion as disposable incomes rise and access to technology improves. Investment in renewable energy projects and off-grid solutions, particularly in MEA, also creates demand for robust and efficient battery charging systems. International manufacturers and distributors are increasingly focusing on these regions to tap into new customer bases and capitalize on burgeoning economic development, making them important areas for future market growth and strategic partnerships.

A Lithium Battery Charger IC (Integrated Circuit) is a specialized electronic component designed to safely and efficiently manage the charging process of lithium-ion and lithium-polymer batteries. Its primary function is to regulate the charge current and voltage according to the battery's specific chemistry and profile, typically involving Constant Current (CC) and Constant Voltage (CV) phases. This regulation prevents overcharging, deep discharging, and overheating, which are critical for extending battery lifespan and ensuring operational safety in various electronic devices.

Lithium Battery Charger ICs are crucial because they ensure the optimal performance, longevity, and safety of the lithium-based batteries that power nearly all modern portable electronic devices, electric vehicles, and energy storage systems. Without precise charging control, lithium batteries can suffer irreversible damage, reduced capacity, or even become safety hazards (e.g., thermal runaway). These ICs also enable advanced features like fast charging, battery health monitoring, and efficient power management, which are indispensable for contemporary user expectations and device functionality across consumer, automotive, and industrial applications.

Key technological trends include the integration of fast charging protocols (e.g., USB-PD, Quick Charge) for quicker power delivery, the adoption of Wide Bandgap (WBG) semiconductors like GaN and SiC for higher efficiency and power density, and advancements in wireless charging technologies. There's also a significant trend towards higher integration of functionalities within a single IC, such as fuel gauging, cell balancing, and comprehensive protection features. Furthermore, the development of intelligent, AI-powered charging algorithms for adaptive optimization and predictive maintenance is an emerging trend shaping the market's future.

The major consumers are primarily the consumer electronics industry (smartphones, laptops, wearables, IoT devices) and the automotive industry (Electric Vehicles, Hybrid Electric Vehicles). Demand from consumer electronics is driven by the continuous need for smaller, more efficient, and faster-charging solutions for an ever-increasing array of portable devices. The automotive sector's demand is propelled by the global shift towards electric mobility, requiring robust, high-power, and highly reliable charger ICs for EV battery packs and associated systems, with safety and performance being paramount.

Challenges include intense price competition, particularly in high-volume segments, along with the technical complexity of balancing efficiency, safety, and diverse application requirements. Supply chain disruptions and the lack of universal charging standards also pose hurdles. Opportunities lie in the continuous innovation in materials (GaN/SiC), expansion of wireless charging, integration of AI for advanced battery management, and the growing demand from emerging markets and sustainable energy solutions (smart grids, energy storage systems). Developing highly integrated, intelligent, and adaptable ICs capable of meeting diverse and evolving needs is key to capitalizing on these opportunities.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.