ID : MRU_ 435434 | Date : Dec, 2025 | Pages : 242 | Region : Global | Publisher : MRU

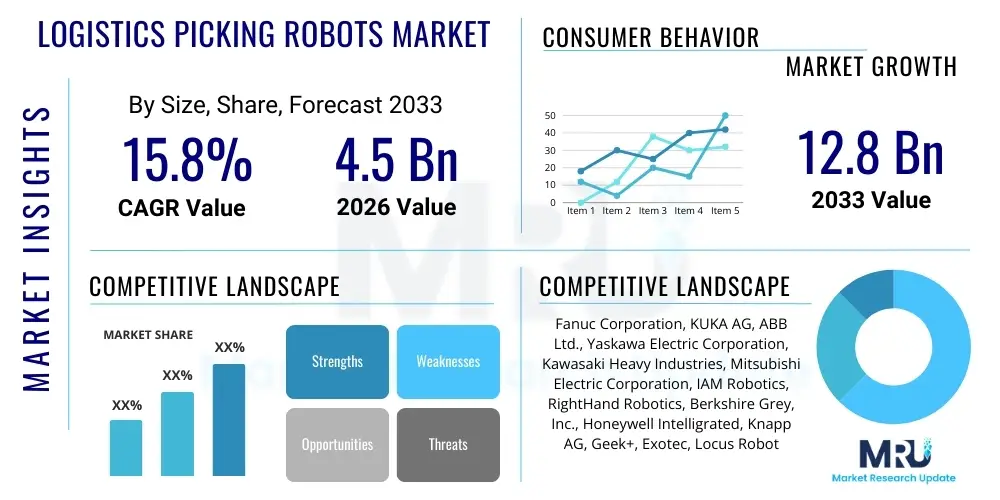

The Logistics Picking Robots Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 15.8% between 2026 and 2033. The market is estimated at USD 4.5 Billion in 2026 and is projected to reach USD 12.8 Billion by the end of the forecast period in 2033.

The Logistics Picking Robots Market encompasses specialized automated systems designed to perform item retrieval, sorting, and placement tasks within warehouses, distribution centers, and fulfillment facilities. These robotic systems utilize advanced technologies such as computer vision, machine learning, deep neural networks, and sophisticated gripping mechanisms to handle a wide variety of SKUs with high accuracy and speed. Products range from collaborative robots (cobots) working alongside humans to fully autonomous mobile robots (AMRs) integrated into large-scale automated storage and retrieval systems (AS/RS). The primary function is to optimize the 'pick' stage of the fulfillment process, which is often the most labor-intensive and error-prone activity in logistics operations. This adoption is accelerated by the need for higher throughput and reduced operating costs, driven specifically by the volatile demands of the e-commerce sector and increasing labor scarcity globally.

Major applications for logistics picking robots span e-commerce fulfillment, third-party logistics (3PL), retail distribution, and grocery supply chains. In e-commerce, these robots enable rapid handling of single-item orders and complex batch picking, essential for maintaining competitive delivery speeds. The benefits derived from deploying these solutions are multifaceted, including a significant reduction in picking errors, 24/7 operational capability, enhanced worker safety by handling strenuous tasks, and substantial improvements in overall supply chain efficiency. Furthermore, modern picking robots are increasingly modular and scalable, allowing businesses to adapt their automation levels based on seasonal demand fluctuations without massive fixed infrastructure investments.

Driving factors for this market include the relentless expansion of global e-commerce, necessitating robust automation for high-volume fulfillment, and critical shortages of manual labor in key logistical hubs worldwide. Additionally, technological advancements in robotic dexterity, sensor fusion, and sophisticated software platforms that facilitate seamless integration with existing Warehouse Management Systems (WMS) are lowering the barrier to entry for many enterprises. The ongoing pressure to reduce operational expenditure while simultaneously improving order accuracy and delivery timelines provides a strong commercial imperative for widespread adoption of logistics picking automation.

The Logistics Picking Robots Market is characterized by intense innovation centered around Artificial Intelligence (AI) and collaborative robotics. A key business trend is the transition toward Robotics-as-a-Service (RaaS) models, which significantly reduce the initial capital expenditure barrier for medium and small enterprises, accelerating market penetration. Strategic partnerships between hardware manufacturers and AI software developers are becoming crucial for delivering highly integrated, task-specific solutions capable of handling diverse and unstructured environments common in modern fulfillment centers. Furthermore, sustainability and energy efficiency are emerging focal points, with manufacturers striving to develop lighter, more power-efficient robots, aligning with corporate environmental, social, and governance (ESG) goals.

Regionally, Asia Pacific (APAC) currently dominates the market, primarily due to the vast manufacturing base, the rapid infrastructural build-out in countries like China and India to support burgeoning domestic e-commerce markets, and supportive governmental policies promoting industrial automation. North America and Europe, however, exhibit the highest adoption rates of advanced, highly autonomous picking systems, driven by high labor costs and the sophistication of existing automated logistics infrastructure. The European market, in particular, is witnessing robust growth fueled by legislative mandates concerning worker safety and the adoption of collaborative robotic solutions (cobots) that offer flexible automation within existing facility layouts.

In terms of segment trends, the hardware segment, specifically encompassing Autonomous Mobile Robots (AMRs) combined with articulated robotic arms, holds the largest market share. However, the software and services segment, including vision systems, fleet management software, and predictive maintenance services, is projected to experience the fastest growth rate. This rapid growth is attributed to the increasing complexity of robotic orchestration and the need for sophisticated AI algorithms to manage tasks like dynamic path planning, object recognition (especially for novel items), and human-robot interaction safety. The shift towards item-level picking and piece-picking capabilities, rather than case or pallet picking, defines the technical evolution within this segmented landscape.

Common user inquiries regarding AI's influence in the Logistics Picking Robots Market frequently revolve around the robot’s capability to handle novel or delicate items, the reliability of AI-driven vision systems in varied lighting conditions, the cost of integrating machine learning models, and the long-term potential for predictive maintenance and self-optimization. Users are concerned about whether AI can truly bridge the dexterity gap between human and robotic handling for highly unstructured tasks, especially in environments involving millions of unique SKUs. The core expectation is that AI will provide the necessary intelligence for robots to autonomously adapt to dynamic fulfillment environments, minimize errors, and maximize throughput, thereby ensuring a higher return on investment (ROI) compared to traditional, programmed automation. The pervasive theme is seeking solutions that move beyond simple pick-and-place routines to encompass complex decision-making processes inherent in effective warehouse operations.

The Logistics Picking Robots Market growth is primarily driven by the exponential growth of e-commerce, which necessitates highly efficient and scalable fulfillment solutions to meet increasing customer expectations for fast delivery. Another significant driver is the widespread scarcity of manual labor for warehouse operations in developed economies, making automation a necessity rather than a luxury. However, the market faces restraints, chiefly the substantial initial capital investment required for deploying sophisticated robotic systems, which can be prohibitive for smaller logistics providers. Furthermore, the complexities associated with integrating advanced robotic technologies with disparate legacy Warehouse Management Systems (WMS) and Enterprise Resource Planning (ERP) systems represent a significant technological hurdle that slows implementation timelines.

Opportunities for market expansion are abundant, particularly in the emerging field of micro-fulfillment centers (MFCs) located closer to urban consumers, requiring compact, high-speed picking solutions. The development of advanced grasping technologies capable of handling highly deformable or sensitive goods, such as fresh groceries or delicate apparel, opens entirely new market verticals. Moreover, the adoption of RaaS models presents a critical opportunity to democratize access to automation, shifting the financial risk from the end-user to the service provider and encouraging rapid scaling across 3PL operations worldwide. This flexibility in deployment is crucial for adapting to the cyclical nature of logistics demand.

The impact forces influencing the competitive landscape are highly pronounced. The threat of new entrants remains moderate but rising, primarily due to the increasing accessibility of modular components and open-source robotics software, although significant expertise is required for integration. Supplier bargaining power is moderately high, concentrated among specialized component providers, particularly those offering advanced vision sensors, custom grippers, and high-performance motors. Buyer bargaining power is also high, driven by the customizability required and the expectation of rapid ROI. The high threat of substitutes comes from alternative automation methods like fully automated AS/RS and advanced conveyor systems. However, the competitive rivalry among existing players is intense, characterized by continuous innovation in AI algorithms, payload capacity, and robotic speed, leading to aggressive pricing strategies and rapid product iteration cycles.

The Logistics Picking Robots Market is extensively segmented based on component, type, application, and end-user, reflecting the diverse operational needs across the logistics landscape. Understanding these segmentations is crucial for identifying precise market opportunities and technology adoption patterns. The component segment highlights the vital distinction between the physical hardware (robot arms, AMRs) and the crucial software (vision systems, control software, fleet management) that provides the necessary intelligence and coordination. The segmentation by type, specifically the distinction between articulated, SCARA, Cartesian, and delta robots, addresses the specific kinematic requirements for various picking tasks, from high-speed sorting to heavy-duty item handling. Overall, the software segment is emerging as the key differentiator, driving efficiency gains beyond the mechanical capabilities of the robot platform itself.

The value chain for logistics picking robots is highly complex, starting with the upstream component suppliers who provide critical technologies such as specialized industrial sensors, high-resolution 3D cameras for vision systems, precision mechanical components (motors, gears), and advanced End-of-Arm Tooling (EOAT), including proprietary grippers. Innovation at this upstream level, particularly in sensor fusion and material science for grippers, directly influences the robot's overall capability and cost structure. Major robot manufacturers then undertake the system integration, design, and assembly, often customizing the hardware platform to meet specific payload and speed requirements defined by the logistics sector.

Midstream activities involve sophisticated software development, where AI and machine learning specialists create the cognitive layer—the vision software, task planning algorithms, and fleet orchestration systems—essential for robot functionality in dynamic warehouse settings. System integrators and specialist distributors form the primary distribution channel. These entities are responsible for the complex task of integrating the robotic systems into the client's existing physical infrastructure and digital WMS/ERP platforms, often customizing the solution based on the client’s unique inventory profile (SKU variety and volume). Direct sales from Tier 1 manufacturers are common for large-scale, enterprise-level deployments, whereas indirect channels, including certified integrators and 3PL partners, serve the fragmented mid-market.

Downstream activities center around the end-users—e-commerce giants, 3PL providers, and retail chains—who utilize these robots for crucial fulfillment operations. Post-sales services, including maintenance, software updates, and predictive diagnostics provided through service agreements (often bundled in RaaS models), form a critical, high-margin component of the downstream value chain. The efficiency gains realized by the end-users through reduced labor costs, enhanced accuracy, and faster throughput ultimately validate the investment, closing the loop. The close collaboration between the integration specialists and the end-users is paramount for achieving successful long-term operational impact.

The primary potential customers for logistics picking robots are large-scale e-commerce operators and multinational third-party logistics (3PL) providers, who face overwhelming pressure to manage massive SKU catalogs and fulfill increasing volumes of individual orders with short lead times. E-commerce platforms, such as Amazon, Alibaba, and specialized online retailers, represent a critical segment due to their requirement for extremely high throughput during peak seasons and their continuous investment in scalable automation to maintain a competitive edge in delivery speeds. These customers prioritize robots capable of high-speed, accurate piece picking for unpredictable product dimensions and weights, often demanding sophisticated AI vision systems.

Another major segment comprises grocery retailers and food and beverage distributors. The demand here is driven by the rapid expansion of online grocery delivery (e-grocery), which necessitates automation capable of handling highly perishable, delicate, and temperature-sensitive items. Robots deployed in this segment must excel in dexterity, managing items like fresh produce and fragile containers without damage. Furthermore, 3PL providers are increasingly investing in modular and scalable picking robot fleets to offer flexible, advanced fulfillment services to their diverse clientele, viewing automation as a necessary competitive differentiator in winning high-value logistics contracts.

Finally, traditional manufacturing and automotive distribution centers also constitute significant buyers. While not typically handling e-commerce volumes, these facilities require picking robots for kitting, sequencing parts for assembly lines (JIT), and managing spare parts inventories. Their demand often leans towards heavier payload capacity, reliability in structured environments, and seamless integration with existing manufacturing execution systems (MES). The shared characteristic across all these potential customers is the need to mitigate rising labor costs and operational bottlenecks inherent in manual material handling, making the ROI justification for robotic implementation increasingly straightforward.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 4.5 Billion |

| Market Forecast in 2033 | USD 12.8 Billion |

| Growth Rate | 15.8% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Fanuc Corporation, KUKA AG, ABB Ltd., Yaskawa Electric Corporation, Kawasaki Heavy Industries, Mitsubishi Electric Corporation, IAM Robotics, RightHand Robotics, Berkshire Grey, Inc., Honeywell Intelligrated, Knapp AG, Geek+, Exotec, Locus Robotics, Seegrid Corporation, GreyOrange, Tompkins Robotics, TGW Logistics Group, Dematic (Kion Group), MHS Global. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological landscape of logistics picking robots is rapidly evolving, driven primarily by advancements in cognitive capabilities that allow robots to operate effectively in dynamic, unstructured environments. Core to this evolution is the deployment of sophisticated Machine Vision and Deep Learning (DL) algorithms. These systems utilize high-resolution 2D and 3D cameras, often combining structured light, stereo vision, or LiDAR, to accurately perceive the geometry, material, and precise location of items in a bin or on a shelf. Deep learning models, trained on vast datasets of SKUs, enable the robot to perform rapid and reliable object recognition and pose estimation, even for previously unseen items (zero-shot picking), moving the technology beyond simple, pre-programmed pick-and-place routines and significantly increasing the reliability of piece picking operations.

Another crucial technological development involves Simultaneous Localization and Mapping (SLAM) combined with advanced navigation software, particularly utilized by Autonomous Mobile Robots (AMRs). SLAM allows AMRs to build real-time maps of the warehouse while simultaneously tracking their own location within that map, enabling dynamic path planning and obstacle avoidance without the need for fixed infrastructure like wires or magnetic tape. This flexibility is fundamental in modern fulfillment centers where floor layouts and inventory placement change frequently. Furthermore, fleet management software, often leveraging cloud-based platforms and AI optimization, is essential for coordinating hundreds of robots, minimizing traffic congestion, balancing workloads, and ensuring the overall efficiency of the automated system.

Finally, the End-of-Arm Tooling (EOAT) sector, specifically grippers, is seeing massive innovation to enhance dexterity and versatility. This includes the development of multi-modal grippers that combine vacuum suction with mechanical fingers, specialized soft robotics grippers using compliant materials for handling fragile goods (like produce), and magnetic grippers for metal items. The integration of force/torque sensors within the gripper is becoming standard, providing the robot with tactile feedback—a critical requirement for delicately handling a diverse range of items and ensuring successful, non-destructive grasping. These sensor-enhanced, multi-functional grippers are key technological differentiators, allowing logistics robots to approximate the versatility of human hands.

The primary driver is the accelerating global expansion of e-commerce, which mandates higher throughput, greater picking accuracy, and faster fulfillment capabilities that manual labor cannot sustain, compounded by increasing labor shortages in key logistical markets.

RaaS significantly lowers the high initial capital investment barrier associated with acquiring robotic systems, converting large CapEx into predictable OpEx, thereby making sophisticated automation accessible to small and medium-sized logistics and retail enterprises.

Advanced AI-driven Machine Vision systems combined with Deep Learning algorithms are the most critical technologies, enabling robots to accurately recognize, locate, and determine the optimal grasping strategy for millions of diverse, complex, or previously unseen stock-keeping units (SKUs).

The main restraints include the substantial upfront cost of implementing complex automated systems and the technical difficulty and time required to achieve seamless integration between new robotic fleets and older, disparate legacy warehouse management systems (WMS).

The Grocery & Food and Beverage segment is expected to show the fastest adoption growth, driven by the explosive demand for online grocery delivery (e-grocery) and the subsequent need for specialized picking robots capable of handling perishable, fragile, and temperature-sensitive goods with high dexterity.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.