ID : MRU_ 433999 | Date : Dec, 2025 | Pages : 253 | Region : Global | Publisher : MRU

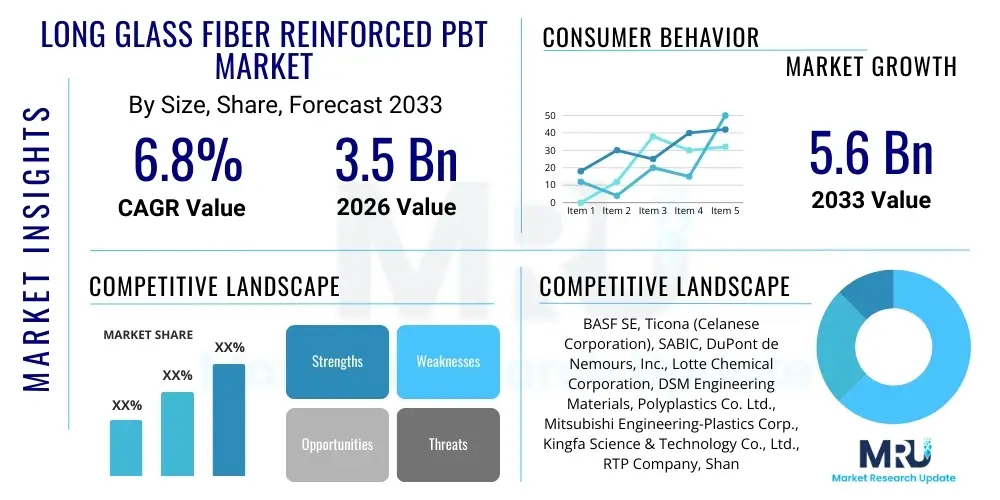

The Long Glass Fiber Reinforced PBT Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2026 and 2033. The market is estimated at USD 3.5 Billion in 2026 and is projected to reach USD 5.6 Billion by the end of the forecast period in 2033. This substantial expansion is fundamentally driven by the escalating demand for high-performance engineering plastics offering superior mechanical strength, excellent dimensional stability, and reduced weight, particularly within the automotive and electrical and electronics sectors globally. The shift towards electrification and the stringent regulatory mandates concerning vehicle lightweighting are core commercial accelerators for LGF PBT adoption, positioning it as a preferred material over traditional reinforced polymers.

Market expansion is also supported by continuous innovation in compounding technology, allowing manufacturers to produce LGF PBT grades with optimized fiber dispersion and enhanced thermal properties. These material advancements open up new application avenues in highly demanding environments, such as structural components under the hood (engine covers, intake manifolds) and critical safety parts. Furthermore, the rising awareness regarding material recycling and sustainability is indirectly supporting PBT-based compounds, provided that the supply chain can manage the complexity associated with processing long fibers while maintaining material integrity and performance standards required by tier-one suppliers and OEMs.

Geographically, the robust growth witnessed in the Asia Pacific region, led by major manufacturing hubs in China, Japan, and India, contributes significantly to the overall market valuation. The extensive manufacturing base for consumer electronics and the rapid expansion of electric vehicle (EV) production in these countries create a sustained, high-volume requirement for LGF PBT. While raw material price volatility and the complexity of the compounding process pose short-term challenges, the long-term outlook remains highly favorable, underpinned by structural market shifts toward miniaturization and advanced material specifications.

Long Glass Fiber Reinforced Polybutylene Terephthalate (LGF PBT) is a high-performance thermoplastic composite characterized by glass fibers ranging typically between 10 mm and 25 mm in length, which are fully integrated into the PBT matrix. This unique composition delivers significantly improved mechanical properties—including high strength, superior stiffness, and exceptional impact resistance—compared to short glass fiber reinforced plastics or unreinforced PBT. LGF PBT maintains the inherent advantages of PBT, such as excellent chemical resistance, high heat deflection temperature, and superb electrical insulation properties, making it an ideal substitute for metals in semi-structural and functional applications across various industries. The incorporation of long fibers ensures better stress distribution within the polymer structure, translating to greater durability and reliability for end-use components, which is critical in safety-sensitive environments.

The primary applications driving the LGF PBT market include the automotive industry, where it is utilized for components requiring high rigidity and resistance to heat and chemicals, such as instrument panel carriers, door module carriers, front-end carriers, and various under-the-hood parts. In the electrical and electronics (E&E) sector, LGF PBT is crucial for manufacturing switchgear components, motor housings, connectors, and insulating devices, owing to its superior dielectric strength and dimensional stability under varying thermal loads. The key benefits derived from using LGF PBT components include significant weight reduction (fuel efficiency in conventional vehicles and extended range in EVs), lower processing costs compared to metal casting, and excellent Noise, Vibration, and Harshness (NVH) characteristics, enhancing overall product performance and user comfort.

The market growth is fundamentally driven by stringent global regulations aimed at curbing CO2 emissions, which mandates vehicle lightweighting and necessitates the adoption of high-strength, low-density materials like LGF PBT. Furthermore, the proliferation of complex electronic assemblies in consumer goods and industrial machinery, demanding fire-retardant and high-performance housing materials, acts as a significant market catalyst. Innovations in injection molding and extrusion technologies that minimize fiber damage during processing further enhance the commercial viability and application scope of LGF PBT, cementing its role as a key material in modern engineering and design practices across diverse industrial ecosystems.

The Long Glass Fiber Reinforced PBT market is witnessing robust growth, propelled primarily by macro-level business trends emphasizing material substitution and electrification across major manufacturing economies. The core business trend involves a persistent shift away from traditional metallic materials towards advanced composite plastics in load-bearing and semi-structural applications, notably driven by the automotive industry's focus on electric vehicle architecture. The need for materials that can withstand high operational temperatures and harsh chemical exposures while contributing to battery efficiency through reduced mass defines the current business landscape. Furthermore, heightened collaboration between resin producers, compounders, and application developers is accelerating product customization, ensuring LGF PBT meets highly specific performance requirements for complex electronic packaging and high-voltage components, thereby securing long-term market traction.

Regional trends indicate that the Asia Pacific (APAC) region currently dominates the market, attributing to its unparalleled scale in automotive and consumer electronics manufacturing, particularly in China and South Korea. This dominance is further reinforced by government initiatives promoting EV adoption and establishing large-scale battery manufacturing Gigafactories, which require specialized fire-retardant and mechanically strong polymer materials. Conversely, North America and Europe demonstrate mature market characteristics, focusing intensely on high-value, specialized applications, such media-intensive electronic components and complex automotive safety systems. In these regions, stringent environmental standards regarding volatile organic compounds (VOCs) and end-of-life recycling are pushing innovation towards bio-based or recycled content LGF PBT variants, driving premium pricing and technological differentiation within the localized supply chains.

Segment-wise, the market is broadly segmented by manufacturing process, application, and end-use. The Pultrusion process segment is expected to hold a leading share due to its efficiency in producing highly consistent, long-fiber pellets with minimal fiber degradation. In terms of end-use, the Automotive sector remains the primary revenue generator, specifically the interior, exterior, and under-the-hood applications. However, the Electrical and Electronics segment is projected to exhibit the fastest growth CAGR, fueled by the accelerating miniaturization of devices and the increased integration of smart technologies requiring superior insulating and thermal management properties. The transition to higher power requirements in E&E applications necessitates the use of robust materials like LGF PBT that can ensure device reliability and prolonged operational life.

User inquiries regarding the impact of Artificial Intelligence on the Long Glass Fiber Reinforced PBT market predominantly revolve around three key themes: how AI enhances material discovery and formulation, its role in optimizing complex compounding and molding processes, and the application of machine learning for predictive maintenance and quality control within manufacturing. Users are keen to understand if AI can accelerate the development cycle of new LGF PBT grades, especially those targeting specialized properties like ultra-high temperature resistance or improved fire safety standards for battery enclosures. Furthermore, there is significant concern regarding the complexity of fiber orientation prediction during injection molding, a critical determinant of final component performance, where traditional simulation struggles. Users anticipate that AI-driven simulation tools will enable manufacturers to achieve higher component reliability and reduce iterative design cycles, potentially lowering the overall cost of adoption.

AI’s influence is profound in material science simulation, where generative models and neural networks are used to analyze vast datasets relating polymer chemistry, fiber-matrix interaction, and final mechanical performance. This capability allows researchers to rapidly screen potential composite formulations, predicting the properties of untested LGF PBT variations with high accuracy, thus dramatically shortening the time-to-market for specialized compounds. In the manufacturing phase, AI-powered systems are deployed to monitor real-time process parameters in twin-screw extruders and injection molding machines, optimizing variables like temperature, screw speed, and residence time to ensure uniform fiber length distribution and minimal degradation. Such precision is crucial for maintaining the performance integrity of long glass fibers, which are highly susceptible to breakage during compounding, thereby improving manufacturing consistency and reducing material waste associated with off-spec production batches.

Moreover, AI is transforming quality assurance and supply chain resilience. Computer vision systems combined with machine learning algorithms are utilized for non-destructive inspection of finished LGF PBT components, accurately identifying defects such as voids, sink marks, or inconsistent fiber bundles that are often missed by conventional inspection methods. In the supply chain, predictive analytics driven by AI models help forecast demand volatility for PBT resin and glass fiber, optimizing inventory levels and mitigating risks associated with raw material procurement. This sophisticated level of operational intelligence, facilitated by AI, ultimately enhances the competitiveness of LGF PBT solutions by ensuring superior quality and a more stable, responsive supply chain capable of handling the stringent requirements of high-demand sectors like electrification and aerospace.

The Long Glass Fiber Reinforced PBT market is fundamentally shaped by a confluence of strong driving factors, critical restraints, and substantial market opportunities that collectively define the impact forces influencing its growth trajectory. The principal drivers stem from the global push for sustainability and energy efficiency, compelling industries, especially automotive OEMs, to prioritize lightweight materials to enhance fuel economy in conventional vehicles and extend the range of electric vehicles. This mandatory shift, coupled with LGF PBT's excellent performance-to-weight ratio, high rigidity, and superior impact absorption compared to traditional materials, provides a robust foundation for sustained demand growth. Additionally, the increasing complexity and heat generation in modern electronic devices necessitate materials with exceptional thermal stability and electrical insulation, characteristics that LGF PBT inherently possesses, reinforcing its adoption across the electronics supply chain.

Conversely, the market faces notable restraints, primarily centered around the volatility and fluctuation in the prices of key raw materials, namely PBT resin (derived from PTA and butanediol) and specialty glass fibers. These cost variations introduce uncertainty in manufacturing costs, potentially affecting the final pricing and profitability margins for compounders. Furthermore, the specialized nature of compounding long fibers requires complex processing machinery and highly technical expertise to prevent fiber breakage and ensure optimal fiber dispersion, posing a barrier to entry for smaller or less technologically advanced players. Competition from alternative high-performance engineering plastics, such as Long Glass Fiber reinforced Polypropylene (LGF PP) and Polyamide (LGF PA), which may offer different cost-performance trade-offs for certain applications, further restricts the market’s unchecked expansion.

Despite these challenges, significant opportunities exist for market participants. The rapid growth in the Electric Vehicle (EV) market presents a generational opportunity, as LGF PBT is highly suitable for structural battery pack components, charging infrastructure, and intricate high-voltage connection systems where fire retardancy and mechanical integrity are non-negotiable. Moreover, the exploration of bio-based PBT and the development of chemically recyclable LGF PBT compounds promise to align the market with stringent environmental, social, and governance (ESG) standards, creating premium market segments. Strategic investment in Asia Pacific manufacturing capabilities and technical partnerships focusing on developing ultra-low warp, high-flow LGF PBT grades for thin-wall applications will be instrumental in capturing long-term market share and mitigating raw material supply risks.

The Long Glass Fiber Reinforced PBT market is comprehensively segmented across several axes to accurately reflect the diverse application landscape and technological requirements of end-user industries. The segmentation is critical for compounders and material suppliers to tailor their product offerings to specific performance envelopes, such as high-temperature resistance required for under-the-hood applications or specialized dielectric properties for complex electronic housings. Key segmentation criteria include the method used for fiber introduction, the specific end-use application area, and the target industry vertical, offering a granular view of market dynamics and pockets of high growth potential. Analyzing these segments helps in strategic decision-making regarding product portfolio expansion and geographic market penetration, ensuring resources are allocated efficiently to capitalize on emerging trends like EV component manufacturing.

The segmentation by manufacturing process, specifically distinguishing between Pultrusion and Injection Molding techniques for LGF pellet production, highlights technological differences crucial for final product quality. Pultrusion generally yields LGF pellets with superior fiber length consistency, which is preferred for high-stress structural components, whereas modified injection molding techniques might be optimized for cost efficiency in less demanding applications. Furthermore, segmenting the market based on fiber content (e.g., 20% LGF, 30% LGF, 40% LGF, and above) directly correlates with the desired mechanical properties—higher fiber content targets metal replacement applications requiring maximum stiffness and strength, while lower content may focus on improved dimensional stability in large housings. This level of detail in segmentation allows for precise mapping of customer requirements to available material solutions.

Geographically, market segmentation remains vital, as regional regulatory frameworks and industry concentrations significantly influence demand patterns. Asia Pacific dominates due to mass production capabilities, whereas North America and Europe focus on high-specification, niche markets such as medical devices and advanced industrial machinery. Understanding the interdependencies between material grade, application requirement, and regional preference is essential for developing a robust market strategy. The projected fastest-growing segment, likely within the Electrical and Electronics vertical focusing on high-voltage and thermal management components, underscores the importance of technological readiness to meet future requirements driven by 5G infrastructure expansion and consumer electronics complexity.

The value chain of the Long Glass Fiber Reinforced PBT market is complex and vertically integrated, starting with the synthesis of basic petrochemical feedstocks and culminating in the assembly of final components by Original Equipment Manufacturers (OEMs). The upstream segment is dominated by large chemical producers responsible for manufacturing the primary raw materials: Polybutylene Terephthalate (PBT) resin, high-quality sizing agents, and specialized long glass fibers (usually E-glass or R-glass). PBT production involves the polymerization of purified terephthalic acid (PTA) or dimethyl terephthalate (DMT) and 1,4-butanediol (BDO). The quality and consistency of these raw materials directly impact the final composite performance, meaning strong relationships and quality control measures between resin producers and compounders are paramount for market competitiveness.

The midstream stage involves specialized compounders and processors who undertake the critical step of reinforcing the PBT matrix with long glass fibers, typically through continuous pultrusion or direct long fiber compounding (D-LFT) methods. This stage adds the highest value, as the compounding process determines the final characteristics, such as fiber length retention, dispersion quality, and the addition of functional additives (e.g., heat stabilizers, flame retardants, UV inhibitors). Compounders often customize LGF PBT grades to meet specific OEM requirements concerning mechanical load, temperature exposure, and dimensional tolerance. These prepared LGF PBT pellets or granulated compounds are then sold to component manufacturers (molders) who utilize high-pressure injection molding techniques to create the final parts.

The downstream segment consists of Tier 1 suppliers and OEMs, primarily in the automotive and E&E sectors, which purchase the molded components for integration into their final products. Distribution channels are varied, including direct sales from compounders to large, established Tier 1 suppliers who have specialized knowledge in processing long-fiber materials, and indirect sales through specialized polymer distributors who cater to smaller molders and diverse industrial applications. The complexity of LGF PBT necessitates that the distribution channel provides substantial technical support and application expertise, ensuring correct material handling and processing parameters are maintained across the final fabrication stage to optimize component performance.

The potential customer base for Long Glass Fiber Reinforced PBT is highly concentrated within industries requiring materials that offer an optimal balance of high strength, chemical resistance, and excellent dielectric properties, often replacing die-cast metals or high-cost thermoset materials. The primary and most expansive end-user segment is the global automotive industry, which utilizes LGF PBT extensively for safety-critical and structural parts demanding superior crash resistance and weight reduction. Automotive manufacturers and their Tier 1 suppliers are continually seeking LGF PBT for front-end modules, instrument panel frames, seat structures, and complex under-the-hood components like air intake manifolds and engine covers, where exposure to high temperatures and corrosive fluids is common. The growing Electric Vehicle segment represents a specialized and high-growth customer category, demanding customized LGF PBT grades for battery module housing, charging ports, and high-voltage busbar holders due to the need for robust thermal and electrical management.

The second major group of customers comprises the Electrical and Electronics (E&E) manufacturers, spanning consumer electronics, telecommunications, and industrial power distribution. These buyers prioritize the material’s inherent fire retardancy (often meeting UL 94 V-0 standards) and excellent dimensional stability under thermal cycling. LGF PBT is the material of choice for large domestic appliance components, industrial circuit breakers, connectors, motor components, and various sensitive electronic housings where reliability and prevention of warping are critical performance metrics. Furthermore, the industrial machinery sector, including manufacturers of pumps, valves, and fluid handling equipment, are significant customers. They leverage LGF PBT's resistance to hydrolysis and wear, opting for it over conventional plastics or metals in applications exposed to harsh chemical environments, aiming for longevity and reduced maintenance cycles in heavy-duty machinery.

Emerging potential customer segments include the aerospace and defense sectors, albeit for specialized, lower-volume applications requiring lightweight structural rigidity, and the medical device industry, where specific, high-end LGF PBT grades are utilized for durable equipment housings and structural components that need to withstand repeated sterilization cycles. Across all segments, the purchasing decision for LGF PBT is rarely cost-driven alone; it is heavily influenced by total cost of ownership, part consolidation possibilities, and the material’s ability to meet rigorous technical specifications and certification standards (e.g., VDA, ASTM, or specific OEM material standards). The procurement process often involves long qualification cycles and necessitates a strong partnership with the compounder for technical support and performance validation, underscoring the B2B relationship complexity.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 3.5 Billion |

| Market Forecast in 2033 | USD 5.6 Billion |

| Growth Rate | 6.8% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | BASF SE, Ticona (Celanese Corporation), SABIC, DuPont de Nemours, Inc., Lotte Chemical Corporation, DSM Engineering Materials, Polyplastics Co. Ltd., Mitsubishi Engineering-Plastics Corp., Kingfa Science & Technology Co., Ltd., RTP Company, Shanghai PRET Composites Co., Ltd., JFE Chemical Corporation, Lanxess AG, Sumitomo Chemical Co., Ltd., Techmer PM, Sinopec, Covestro AG, Kureha Corporation, Kuraray Co., Ltd., Daicel Corporation |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological landscape of the LGF PBT market is defined by innovations aimed at optimizing fiber length retention during compounding and molding, enhancing fiber-matrix adhesion, and improving the processability of the highly viscous material. The Pultrusion compounding technology remains a cornerstone, as it is the most effective method for producing uniformly impregnated LGF pellets, ensuring that the glass fibers maintain their required length to provide maximal mechanical reinforcement in the final part. Recent advancements in pultrusion focus on developing higher throughput lines and utilizing specialized dies to achieve better fiber wet-out without compromising the molecular integrity of the PBT resin. Furthermore, advancements in Direct Long Fiber Thermoplastic (D-LFT) injection molding are gaining traction, allowing compounders to mix chopped continuous fibers directly into the melt stream at the press. While D-LFT often results in shorter fibers than pultrusion, the advantage lies in cost reduction and flexibility, making it highly competitive for certain large-volume automotive components.

Material technology advancements are equally important, particularly concerning surface treatment and sizing agents applied to the glass fibers. These chemical coatings are crucial for promoting a strong interface between the inert glass fiber and the PBT polymer matrix. Improved sizing agents are continuously being developed to withstand higher processing temperatures and chemical exposure, leading to LGF PBT composites with superior hydrolytic stability and resistance to automotive fluids. Another critical area is the development of specialized additive packages, including nucleating agents to control crystallization speed (crucial for faster molding cycles) and non-halogenated flame retardants to meet stringent fire safety standards (especially important for EV and E&E applications). The optimization of these additives allows manufacturers to tailor LGF PBT grades precisely for applications requiring fast cycle times without sacrificing dimensional precision.

The convergence of material science and digital manufacturing is also driving technological change. Advanced simulation software, incorporating rheological and structural analysis, is now standard practice to accurately predict fiber orientation and consequential anisotropic properties within the molded component. This predictive capability minimizes trial-and-error in mold design, reducing time-to-market. Furthermore, the integration of Industry 4.0 principles, including sensor technology in compounding extruders and injection molding machines, facilitates real-time monitoring and adaptive process control. This smart manufacturing approach ensures quality consistency across large batches, addressing one of the core challenges—maintaining consistent long fiber integrity—inherent to LGF composite manufacturing. This ongoing technological sophistication is key to the sustained market penetration of LGF PBT into high-specification engineering roles.

The global market for Long Glass Fiber Reinforced PBT exhibits distinct regional variations in demand, application focus, and growth drivers. Asia Pacific (APAC) stands out as the undisputed leader, driven by the sheer volume of manufacturing activities in China, South Korea, and Japan. The region's dominance is underpinned by its massive automotive manufacturing base, which includes a rapidly expanding electric vehicle production ecosystem, coupled with its role as the global hub for consumer electronics and industrial machinery production. APAC growth is characterized by high-volume, cost-competitive production, with increasing local compounders strengthening the regional supply chain. Governments across APAC are actively promoting investments in advanced materials and clean energy technologies, further accelerating the adoption of LGF PBT for structural and thermal management components within these new industrial capacities. The scale of development ensures APAC will likely maintain the highest growth rate throughout the forecast period.

Europe represents a mature yet highly quality-driven market, focusing intensely on high-performance, specialized LGF PBT grades that meet stringent environmental regulations, particularly concerning recyclability and low VOC emissions (Volatile Organic Compounds). The European automotive sector, particularly German premium OEMs, drives demand for LGF PBT in highly engineered structural components that enable maximum vehicle lightweighting and passive safety enhancements. The region is also a key innovation hub for industrial automation and high-end electronics, demanding materials with exceptional long-term reliability and precise dimensional stability. European manufacturers often collaborate closely with specialized compounders to develop tailor-made solutions, emphasizing innovation over sheer volume, which translates to a higher average selling price for LGF PBT compounds in this geography compared to Asia.

North America maintains a robust market share, largely fueled by the strong presence of major automotive OEMs and Tier 1 suppliers in the U.S. and Canada, coupled with significant aerospace and defense component manufacturing. The current regulatory environment, especially regarding fuel economy standards (CAFE) and electrification mandates, heavily incentivizes the use of lightweight composites like LGF PBT. Furthermore, the industrial machinery and oil and gas sectors in North America utilize LGF PBT for demanding applications where chemical resistance and mechanical endurance are paramount. While growth rates might be marginally lower than APAC, the market value is consistently high due to the demanding specifications and complex engineering requirements characteristic of the defense and high-performance industrial segments, requiring localized supply chains and rapid technical service support for specialized grades.

LGF PBT offers significantly enhanced mechanical properties, including higher impact strength, superior stiffness, and creep resistance, due to the effective load transfer enabled by the long fiber architecture. This makes it ideal for structural and semi-structural applications requiring high strength-to-weight ratios, outperforming short glass fiber PBT which typically exhibits lower impact resistance.

The Automotive industry is the largest consumer. Adoption is accelerating due to global lightweighting mandates aimed at reducing carbon emissions and improving fuel economy. LGF PBT is critical for replacing metallic parts in engine compartments and internal structures, contributing to vehicle mass reduction while maintaining necessary safety and thermal stability standards, particularly for electric vehicle components like battery module frames and high-voltage connections.

The primary challenges include the high complexity of the compounding process, where maintaining long fiber integrity without breakage is crucial for performance. Additionally, the market faces instability due to volatile raw material prices (PBT resin and glass fiber), requiring effective supply chain management and forward planning to mitigate cost fluctuations and ensure consistent material availability for large-scale production runs.

Pultrusion is the preferred method because it efficiently impregnates the continuous glass fiber bundles with PBT resin while minimizing mechanical stress. This process ensures the resulting pellets have high and consistent fiber length (often exceeding 10mm), which maximizes the composite material's load-bearing capacity and stiffness in the final injection molded part, leading to superior structural performance.

The outlook is highly positive. LGF PBT is expected to see rapid growth in the E&E segment driven by the proliferation of 5G infrastructure, smart devices, and complex power distribution systems. Its properties—excellent dielectric strength, flame retardancy (UL 94), and superior dimensional stability under high heat—make it essential for reliable motor housings, switchgear, and complex, miniaturized electronic connectors.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.