ID : MRU_ 439017 | Date : Dec, 2025 | Pages : 243 | Region : Global | Publisher : MRU

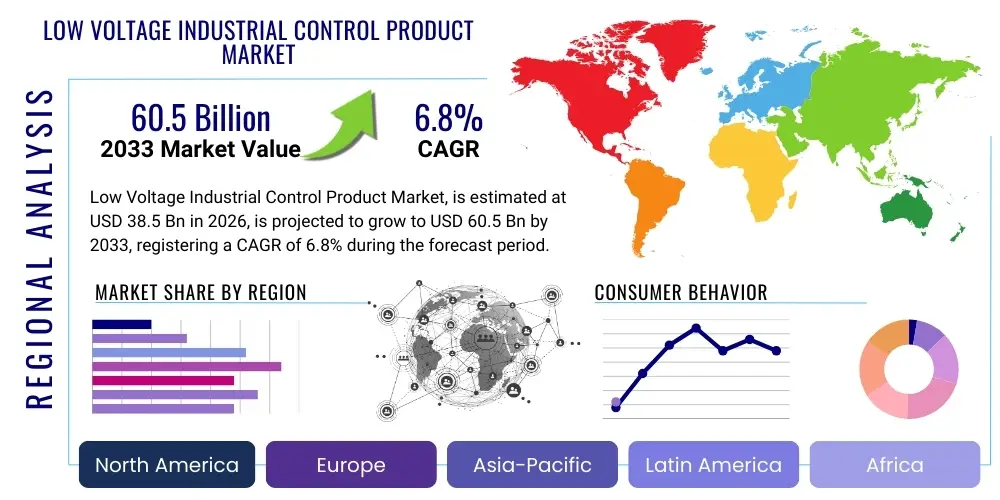

The Low Voltage Industrial Control Product Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2026 and 2033. The market is estimated at USD 38.5 Billion in 2026 and is projected to reach USD 60.5 Billion by the end of the forecast period in 2033.

The Low Voltage (LV) Industrial Control Product Market encompasses essential electrical devices designed to operate, control, and protect electrical equipment and systems typically rated below 1000V AC or 1500V DC. These products, which include motor starters, contactors, relays, circuit breakers, control switches, and pushbuttons, form the foundational layer of industrial automation and power distribution within manufacturing, utilities, and infrastructure sectors. They are vital for ensuring operational stability, protecting expensive machinery from faults like overloads and short circuits, and facilitating sequential control necessary for complex industrial processes. The pervasive integration of these components across various industries highlights their indispensable role in maintaining both efficiency and safety standards globally, driving consistent demand growth synchronized with global industrial output and modernization initiatives.

The core functionality of these LV control products revolves around switching power, providing safety interlocking mechanisms, and offering diagnostic feedback crucial for sophisticated management systems. Major applications span across discrete manufacturing (automotive, electronics), process industries (oil and gas, chemicals), and critical infrastructure (water treatment, data centers). Their inherent benefits include improved system reliability through rapid fault isolation, enhanced energy efficiency by optimizing motor operation, and compliance with stringent international safety regulations such as IEC standards. Furthermore, the modular nature of many contemporary LV devices allows for easier installation, maintenance, and scalability, providing significant operational advantages to end-users seeking flexible and reliable control architecture.

Key driving factors propelling market expansion include the global surge in industrial automation, heavily influenced by the adoption of Industry 4.0 principles, which necessitates smart, network-ready control components. Moreover, sustained investments in infrastructure development, particularly in emerging economies, alongside rigorous regulatory requirements mandating advanced electrical protection mechanisms, contribute substantially to market dynamism. The push towards sustainable manufacturing practices and the integration of renewable energy systems also fuels demand for specialized LV control solutions capable of handling diverse load profiles and complex power quality issues, positioning the market for steady, technologically driven expansion throughout the forecast period.

The Low Voltage Industrial Control Product Market is characterized by a significant shift towards digitalization and modular design, reflecting broader industrial trends focused on efficiency and connectivity. Business trends indicate a strong focus on developing integrated control platforms that combine protective, monitoring, and control functions into single, networked units, facilitating easier integration into supervisory control and data acquisition (SCADA) systems and industrial IoT (IIoT architectures. Competition remains intense, driven by major global players investing heavily in R&D to enhance product lifecycle management (PLM) capabilities and cybersecurity features of control components, addressing increasing concerns related to operational integrity and data security in interconnected factories. Furthermore, consolidation activities, including strategic acquisitions and partnerships aimed at expanding regional reach and diversifying product portfolios, are shaping the competitive landscape.

Regional trends reveal Asia Pacific (APAC) as the dominant and fastest-growing region, primarily driven by rapid industrialization, large-scale infrastructure projects, and the expansion of the manufacturing base, particularly in China and India. North America and Europe maintain stable growth, characterized by high adoption rates of advanced, smart control technologies focusing on predictive maintenance and energy optimization, often mandated by strict energy efficiency policies. The Middle East and Africa (MEA) and Latin America are emerging markets, showing considerable potential fueled by investments in the oil and gas sector, mining, and expansion of power distribution networks, necessitating robust and reliable LV control gear.

Segmentation trends highlight the increasing demand for electronic motor starters and intelligent relays, which offer superior control and diagnostic capabilities compared to traditional electromechanical counterparts. By component type, circuit breakers and contactors continue to command substantial market share due to their universal application in protection and switching roles. However, the fastest growth is observed in networked control components that support Fieldbus communication protocols, essential for modern decentralized automation systems. Vertically, the demand from the Discrete Manufacturing sector, especially automotive and electronics, remains robust, although the Utility and Infrastructure segment shows accelerated growth due to necessary modernization of aging electrical grids and smart city initiatives, emphasizing safety and operational transparency.

Common user questions regarding AI’s influence on the Low Voltage Industrial Control Product Market predominantly center on how artificial intelligence enhances reliability, enables predictive maintenance, and improves energy management without requiring wholesale replacement of existing infrastructure. Users frequently inquire about the integration feasibility of AI algorithms into existing LV devices, the potential for autonomous fault detection and self-healing systems, and the implications for cybersecurity inherent in smarter, connected controls. Key themes emerging from this analysis include the expectation that AI will transform LV products from passive protection devices into proactive data-generating assets, offering unprecedented insights into equipment health and operational performance. Concerns often revolve around data privacy, the required computational power at the edge, and the skills gap needed to manage these highly sophisticated control environments.

The core impact of AI integration is the transition towards condition-based monitoring, where algorithms analyze sensor data collected by smart LV products (such as smart circuit breakers or intelligent overload relays) to predict component failure well before it occurs. This predictive capability minimizes unexpected downtime, drastically reducing maintenance costs and improving overall equipment effectiveness (OEE). By embedding machine learning models into edge devices or gateways, LV controls can perform rapid, localized decision-making, optimizing processes in real-time without reliance on centralized cloud computing, thereby improving latency and resilience in critical industrial environments.

Furthermore, AI significantly enhances the energy management profile of facilities utilizing LV controls. AI-driven systems can analyze operational patterns, load profiles, and tariff structures to dynamically adjust motor speeds, optimize power factor correction, and sequence loads for peak demand reduction. This optimization leads to substantial savings and aligns perfectly with corporate sustainability goals. The influence of AI extends to product design itself, utilizing generative design and simulation to create more compact, efficient, and robust control devices that are inherently smarter and easier to integrate into complex automation networks, accelerating the pace of innovation within the LV control ecosystem.

The Low Voltage Industrial Control Product Market is strongly influenced by the intertwined dynamics of technological push and regulatory necessity. The primary driver is the accelerating pace of global industrial automation, specifically the widespread adoption of smart factory concepts under Industry 4.0, which mandates the use of highly reliable, communicative, and modular LV components. Simultaneously, the stringent focus on operational safety and energy efficiency, reinforced by updated international standards (e.g., IEC 61439, UL 508), compels industries to upgrade older, less efficient control infrastructure. These drivers create a continuous demand for advanced circuit protection and motor control solutions that offer better diagnostics and reduced total cost of ownership (TCO).

However, market growth is moderated by several significant restraints. One major challenge is the substantial initial capital expenditure required for adopting smart and integrated LV control systems, especially for Small and Medium Enterprises (SMEs) in emerging markets. Additionally, the complexity associated with integrating heterogeneous systems from different vendors, along with concerns regarding interoperability and the proprietary nature of some communication protocols, often hinders rapid deployment. A further restraint is the shortage of skilled labor capable of installing, commissioning, and maintaining these sophisticated electrical control systems, creating a bottleneck for advanced technology uptake.

Opportunities for expansion are abundant, particularly in the realm of edge computing and decentralized control. The development of specialized LV control products optimized for Renewable Energy Systems (Solar, Wind) and Electrical Vehicle (EV) charging infrastructure represents a lucrative avenue. Furthermore, the push for modernization of aging infrastructure in developed economies offers immense potential for retrofit projects involving smart protective relays and intelligent motor control centers (MCCs). The most impactful force is the regulatory environment, which acts as a multiplier, mandating higher performance and safety standards, thus accelerating the replacement cycle and favoring suppliers offering technologically compliant and certified solutions. Market competition intensity is also a significant force, driving down pricing pressure but simultaneously fostering innovation in feature sets and connectivity.

The Low Voltage Industrial Control Product Market is comprehensively segmented based on product type, application, component, end-user industry, and region, providing a granular view of market dynamics and opportunity landscapes. The segmentation reflects the diverse functional roles these products play across the industrial ecosystem, ranging from simple on/off switching to complex motor protection and sequence control. Analyzing these segments helps stakeholders understand where technological investment and market penetration are highest, revealing the rapid shift towards intelligent, communicative devices designed for seamless integration within IIoT environments, optimizing overall system performance and reducing maintenance complexities. The distinct requirements of each end-user industry, such as precision control in Electronics Manufacturing versus high robustness in Oil & Gas, significantly shape product design and feature prioritization within the respective segments.

The value chain for the Low Voltage Industrial Control Product Market is a complex structure starting with specialized material sourcing and culminating in integration services provided to end-users. The upstream segment is heavily dependent on the supply of high-purity raw materials, including specialized plastics, copper, silver alloys for contacts, and semiconductor components essential for smart control devices. The quality and stable supply of these materials directly impact the reliability and durability of the final products. Key upstream activities include material processing and the manufacturing of proprietary core components like arc extinguishing chambers and sophisticated electronic modules. Managing supply chain volatility and ensuring compliance with Restriction of Hazardous Substances (RoHS) regulations are crucial upstream challenges.

The midstream phase involves the core manufacturing, assembly, and testing of LV control products, dominated by major multinational OEMs. These manufacturers invest heavily in automated production lines to achieve economies of scale and maintain rigorous quality control necessary for certifications (e.g., UL, CE). Product differentiation in this stage often relies on technology integration, miniaturization, and enhancing communication capabilities (e.g., Profinet, EtherNet/IP compatibility). Downstream activities focus heavily on distribution and post-sales support. Distribution channels are typically segmented into direct sales (for large infrastructure projects or strategic accounts), and indirect channels leveraging a global network of authorized distributors, specialized electrical wholesalers, and system integrators. System integrators play a critical role, bridging the gap between component supply and complex automation requirements of the end-user.

Direct distribution often provides manufacturers with greater control over pricing and customer relationships, particularly for customized or high-value Motor Control Centers (MCCs). However, the vast majority of standard LV components are moved through indirect channels, which provide rapid local inventory access and technical support, essential for maintenance, repair, and operations (MRO) markets. The importance of specialized technical support and training at the downstream level is growing, especially as products become smarter and require sophisticated configuration and integration into IIoT platforms. This structured value chain, characterized by high barriers to entry in manufacturing but extensive reliance on efficient distribution networks, ensures robust market coverage and timely delivery to diverse industrial clients worldwide.

The potential customer base for Low Voltage Industrial Control Products is expansive and fundamentally tied to the health and expansion of the global industrial and infrastructure landscape. End-users fall broadly into categories that require reliable, safe, and efficient management of electrical power and motor assets, including large multinational corporations operating globally standardized facilities and smaller local manufacturing shops focused on regional production. These customers prioritize components that guarantee system uptime, adhere to local safety regulations, and offer data points for operational analysis. The key decision-makers often involve electrical engineers, maintenance managers, procurement specialists, and automation consultants who assess products based on mean time between failures (MTBF), ease of installation, compatibility with existing systems, and pricing structure.

The most significant buyers reside within the discrete manufacturing sector, notably the automotive and electronics industries, where high-speed production lines rely on thousands of precise switching and protection operations daily, demanding highly durable and fast-acting contactors and relays. Similarly, process industries such as Oil & Gas and Chemical Processing represent highly valuable customers, primarily driven by the need for extremely robust and explosion-proof certified components capable of operating reliably in harsh, hazardous environments. For these industries, component failure is catastrophic, making reliability and compliance the foremost purchasing criteria, often leading them to favor premium brands with established safety track records.

The Utilities and Infrastructure segment, encompassing power generation, water treatment facilities, and rapidly expanding data centers, constitutes another crucial customer group. These buyers frequently engage in large-scale capital projects requiring bulk procurement of circuit breakers, MCCs, and switchgear for system protection and centralized control. The increasing complexity and density of data center power infrastructure, for instance, drives demand for advanced, compact LV controls offering granular monitoring capabilities. Consequently, potential customers are unified by their imperative to maximize operational efficiency and safety, making any product offering advanced diagnostic capabilities, seamless connectivity, and extended operational life highly attractive.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 38.5 Billion |

| Market Forecast in 2033 | USD 60.5 Billion |

| Growth Rate | 6.8% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | ABB Ltd., Siemens AG, Schneider Electric SE, Eaton Corporation, Rockwell Automation, Mitsubishi Electric Corporation, Danfoss A/S, Emerson Electric Co., Fuji Electric Co., Ltd., WEG S.A., Nidec Corporation, TE Connectivity Ltd., Chint Group, L&T Electrical & Automation, Toshiba Corporation, Legrand S.A., Littelfuse Inc., Phoenix Contact GmbH & Co. KG, Omron Corporation, C&S Electric Limited |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The Low Voltage Industrial Control Product Market is undergoing a fundamental technological transformation driven by the principles of connectivity and intelligence, moving beyond basic electromechanical switching toward digitally enabled control systems. A key technology advancement is the pervasive adoption of Industrial Internet of Things (IIoT) capabilities. Modern LV devices, such as smart circuit breakers and intelligent motor control relays, are now equipped with embedded sensors and communication modules supporting standard industrial protocols like EtherNet/IP, PROFINET, and Modbus TCP/IP. This connectivity allows these devices to transmit granular operational data—such as voltage levels, current harmonics, temperature, and wear indicators—directly to cloud platforms or edge computing gateways. This data serves as the foundation for sophisticated diagnostic analysis and predictive maintenance routines, fundamentally changing how assets are monitored and managed.

Another pivotal technological shift involves the integration of edge computing capabilities directly within or adjacent to the control components. Edge computing allows for data processing and complex decision-making to occur locally, minimizing latency and reducing the reliance on centralized servers or cloud infrastructure for critical, time-sensitive control operations. For example, intelligent LV motor starters can use embedded algorithms to detect specific vibration signatures indicative of impending mechanical failure and initiate protective shutdowns instantaneously, far faster than traditional centralized control systems could react. This decentralized intelligence significantly enhances the resilience, reliability, and security of automated industrial systems, particularly in remote or geographically dispersed operational environments where consistent cloud access might be compromised or unreliable.

Furthermore, the development and application of digital twin technology are revolutionizing the lifecycle management of LV control systems. A digital twin is a virtual replica of the physical control system, allowing engineers to simulate operational scenarios, test firmware updates, optimize control sequences, and predict the impact of changes before deployment on the live system. This technology, combined with advanced software for configuration and monitoring, drastically cuts down commissioning time and reduces the risk of expensive errors during modification or expansion projects. The ongoing miniaturization of components, improvements in arc-quenching technologies for higher safety ratings, and the continuous effort to achieve higher power density also remain central themes in the technological landscape, ensuring that LV controls meet the escalating demands of increasingly compact and high-performance industrial equipment.

The primary factor driving market growth is the global acceleration of industrial automation and the widespread adoption of Industry 4.0 principles, necessitating the replacement of older, non-communicative controls with modern, smart Low Voltage (LV) devices capable of network integration and data transmission for predictive maintenance and enhanced operational safety.

IIoT integration significantly enhances the functionality of LV circuit breakers by enabling real-time monitoring of operational parameters like load current and temperature. This data, analyzed via embedded sensors and communication modules, facilitates condition-based monitoring, allowing operators to proactively schedule maintenance, thus optimizing operational lifespan and ensuring superior system uptime.

The Asia Pacific (APAC) region currently holds the largest market share, predominantly driven by extensive governmental and private sector investments in infrastructure, rapid urbanization, and continuous expansion of large-scale manufacturing capacity, particularly across key economies such as China, India, and Southeast Asia.

The main restraints include the high initial capital expenditure required for sophisticated, smart LV control equipment, potential interoperability challenges when integrating components from multiple vendors, and a persistent shortage of industrial automation technicians skilled in commissioning and maintaining these advanced connected systems.

Low Voltage (LV) industrial control products are typically designed and rated for use in systems operating at voltages below 1000 Volts AC (V AC) or 1500 Volts DC (V DC). This threshold defines the operational scope for common products such as miniature circuit breakers, motor starters, and power contactors used in industrial and commercial applications.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.