ID : MRU_ 435271 | Date : Dec, 2025 | Pages : 248 | Region : Global | Publisher : MRU

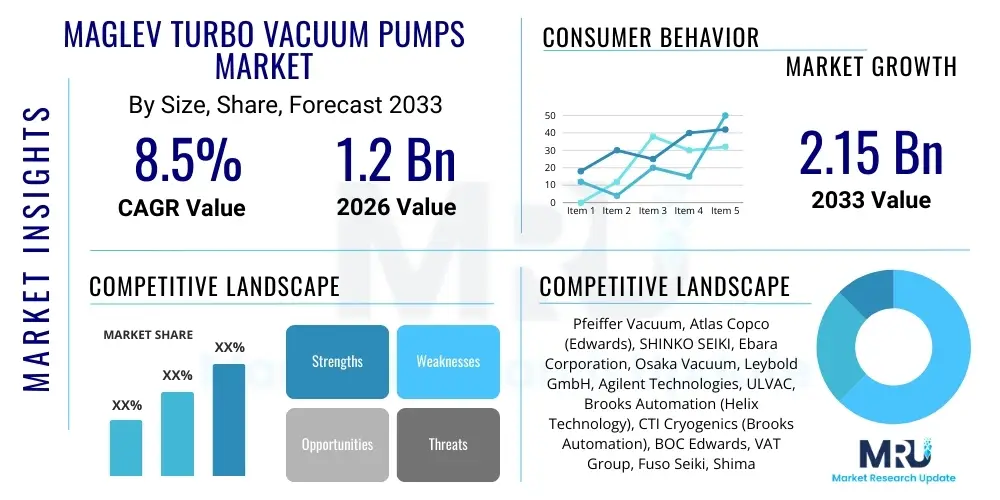

The Maglev Turbo Vacuum Pumps Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 8.5% between 2026 and 2033. The market is estimated at USD 1.2 Billion in 2026 and is projected to reach USD 2.15 Billion by the end of the forecast period in 2033.

The Maglev Turbo Vacuum Pumps Market encompasses high-technology components critical for creating and maintaining ultra-high vacuum (UHV) environments. Maglev turbo pumps distinguish themselves from traditional mechanical pumps through the utilization of magnetic bearings, eliminating mechanical contact, wear, and the need for oil lubrication. This design results in extremely low vibration, high reliability, reduced maintenance requirements, and superior contamination control, making them indispensable in sensitive industrial processes, particularly semiconductor manufacturing, solar panel production, and advanced research facilities. The core product description revolves around a sophisticated rotor suspended and spun using actively controlled magnetic fields, allowing rotational speeds reaching tens of thousands of revolutions per minute, crucial for achieving deep vacuum levels efficiently.

Major applications driving the market include the fabrication of microelectronic devices, where purity is paramount, and the development of thin-film coatings, such as those utilized in photovoltaic cells and optical instruments. Furthermore, advanced scientific domains, including high-energy physics research, mass spectrometry, and nanotechnology R&D, rely heavily on the stable, clean vacuum provided by maglev turbo pumps. The inherent cleanliness and reduced particle generation associated with magnetic levitation technology directly address the stringent quality requirements of these high-value applications, ensuring maximum yield and precision.

Key driving factors accelerating market expansion involve the relentless global investment in semiconductor fabrication plants (fabs), particularly in Asia Pacific, coupled with increasing complexity in chip architectures that demand even purer vacuum environments. The sustained focus on renewable energy technologies, specifically the scale-up of solar panel manufacturing, further fuels demand for reliable vacuum solutions. Benefits derived from adopting maglev systems—such as significantly longer lifespan, lower operational energy consumption due to reduced friction, and superior uptime—provide a compelling economic justification for their premium cost compared to conventional pump technologies.

The Maglev Turbo Vacuum Pumps Market is experiencing robust growth fueled by unprecedented capital expenditure in the semiconductor and flat panel display industries across Asia, particularly China, Taiwan, and South Korea. Business trends indicate a shift towards integrating smart monitoring and predictive maintenance capabilities within pump systems, leveraging IoT sensors and data analytics to maximize operational efficiency and preempt mechanical failure. Manufacturers are focusing on developing hybrid solutions that combine magnetic levitation with specialized materials resistant to highly corrosive gases encountered during etching and deposition processes, aiming to enhance durability and broaden application scope beyond traditional clean processes.

Regional trends highlight the dominance of the Asia Pacific (APAC) region, which serves as both the largest production hub and the primary consumption market for these pumps, driven by high-volume manufacturing activities in electronics. North America and Europe maintain significant market shares, primarily centered on R&D, specialized scientific instrumentation, and small-scale, high-precision manufacturing. Segment trends show that the Semiconductor & Electronics segment remains the largest end-user, though the market is also witnessing accelerated adoption in emerging fields like specialized pharmaceutical lyophilization and fusion energy research, necessitating pumps capable of handling extreme conditions and large gas loads without contamination.

The executive outlook suggests sustained high-value growth throughout the forecast period, contingent upon stable global macroeconomic conditions and continued government subsidization of domestic semiconductor supply chains. Strategic priorities for market players involve securing long-term supply agreements with major fab operators, investing heavily in optimizing rotor geometry for increased pumping speed and compression ratio, and focusing on localized service networks to support the complex maintenance requirements of high-end magnetic bearing systems. This confluence of technological refinement and expansive industrial application solidifies the market's trajectory toward substantial valuation growth.

Common user questions regarding the impact of Artificial Intelligence on the Maglev Turbo Vacuum Pumps Market frequently center on how AI can enhance operational uptime, predict component failure, and optimize energy usage within highly critical manufacturing environments. Users are keen to understand the shift from traditional preventative maintenance schedules to predictive models driven by machine learning algorithms that analyze continuous vibration, temperature, and current load data generated by the magnetic bearing controllers. Furthermore, inquiries often probe the potential for AI-driven process optimization within the end-user applications, such as using deep learning to correlate vacuum stability fluctuations with process yield rates in semiconductor etching, thereby demanding higher precision and real-time responsiveness from the vacuum generation systems themselves.

The integration of AI and machine learning (ML) primarily manifests through enhanced monitoring and diagnostics (M&D) capabilities embedded in the pump control units. By training ML models on historical operational data, manufacturers can identify subtle precursors to bearing drift, motor wear, or unexpected gas loads far earlier than conventional threshold-based alarms. This predictive capability significantly reduces unplanned downtime in expensive fabrication plants, where the cost of a single hour of disruption can run into millions of dollars. The adoption of AI tools ensures that maintenance activities are scheduled precisely when needed, extending the Mean Time Between Failures (MTBF) and minimizing the Total Cost of Ownership (TCO) for end-users operating large fleets of vacuum pumps.

Additionally, AI-driven energy optimization algorithms are becoming crucial, particularly in large-scale vacuum systems where energy consumption is a major operational expense. These algorithms dynamically adjust the rotor speed based on real-time chamber conditions and required throughput, ensuring the pump operates at its most efficient point rather than a fixed maximum setting. This continuous, intelligent adjustment optimizes power draw without compromising vacuum quality, appealing directly to industries facing increasing pressure to meet sustainability goals. The influence of AI elevates the Maglev Turbo Pump from a simple hardware component to an intelligent, interconnected system vital for high-throughput, high-yield manufacturing.

The market dynamics of Maglev Turbo Vacuum Pumps are governed by a complex interplay of Drivers, Restraints, and Opportunities, collectively forming the Impact Forces shaping the industry's trajectory. Key drivers center around the accelerating demand for high-performance, contamination-free vacuum environments mandated by advancing semiconductor node sizes (e.g., 5nm, 3nm) and the proliferation of 3D NAND and EUV lithography technologies, which cannot tolerate particulate generation common in lubricated pumps. Opportunities arise from expanding industrialization in emerging economies, coupled with increased R&D spending in quantum computing, advanced materials science, and clean energy, which necessitate state-of-the-art vacuum technology. However, the high initial capital investment required for maglev technology and the dependence on a few key suppliers of advanced magnetic bearing control systems act as significant restraints. These forces dictate that while the market is premium and niche, its growth rate remains strongly correlated with global high-tech capital expenditures.

The primary driver is the structural shortage and subsequent expansion of global semiconductor fabrication capacity. Governments worldwide are prioritizing domestic chip production through substantial subsidy packages (such as the US CHIPS Act and EU Chips Act), leading to the construction of numerous new fabrication plants (fabs). Each fab requires hundreds of high-quality maglev turbo pumps for crucial process steps like plasma etching, deposition, and ion implantation. This massive infrastructural investment ensures sustained, high-volume demand for reliable, ultra-clean vacuum solutions. Furthermore, the inherent longevity and reliability of maglev pumps, reducing the overall operational risk profile, make them the preferred, if not mandatory, choice for mission-critical processes despite their higher initial cost.

Restraints largely stem from the technological complexity and the requirement for highly specialized servicing and maintenance personnel. Magnetic bearing control systems are highly sensitive, and any minor fluctuation requires specialized diagnostics and expensive proprietary parts, often creating vendor lock-in. Moreover, while operational costs are lower over the lifespan, the upfront investment hurdle remains substantial, particularly for smaller R&D labs or manufacturers with constrained capital budgets. Despite these restraints, the overwhelming technical advantages—superior pumping speed for light gases, lack of hydrocarbon contamination, and exceptionally low vibration—ensure that in critical high-technology applications, the performance benefits consistently outweigh the economic drawbacks, positioning the market for continued expansion where precision is paramount.

The Maglev Turbo Vacuum Pumps Market is primarily segmented based on Pumping Speed, Application, and End-User Industry. Segmentation by pumping speed, ranging from low (under 1,000 L/s) to high (above 5,000 L/s), dictates the appropriate use case, with high-speed pumps being essential for large-volume industrial chambers like those used in large-scale sputtering for display manufacturing. Application segmentation focuses on specific vacuum process types such as etching, deposition (CVD/PVD), and specialized analytics. The meticulous categorization allows manufacturers to tailor features, materials, and digital integration capabilities to specific industrial requirements, ensuring optimal performance for highly specialized processes.

The End-User Industry segmentation is crucial for understanding market dynamics, with Semiconductor & Electronics consistently dominating due to the stringent vacuum requirements of modern microchip fabrication. Other critical segments include Scientific Instruments (Mass Spectrometry, Electron Microscopy), Research & Development (Fusion Energy, Particle Accelerators), and Industrial Coatings (Thin Films, Optical Coatings). These diverse end-users each have unique operational constraints regarding gas type, corrosion resistance, and vibration tolerance, driving differentiation in product design across the competitive landscape. Understanding the nuanced needs within these segments is key for strategic market entry and product development.

The Value Chain for the Maglev Turbo Vacuum Pumps Market is characterized by high technical barriers to entry and intense integration between key stages, reflecting the product's complexity. Upstream activities involve the procurement of highly specialized materials, including high-strength, lightweight alloys for rotor construction, and sophisticated magnetic materials for bearings. Crucially, it involves the specialized manufacturing of high-precision electronic control units (ECUs) and sensors, which are the proprietary intellectual property defining the pump's performance. The manufacturing stage is concentrated among a few global experts who manage complex assembly processes requiring cleanroom environments and stringent quality control protocols to ensure zero contamination and perfect rotor balance.

The downstream analysis focuses heavily on system integration and support. Maglev turbo pumps are rarely sold in isolation; they are typically integrated into complex vacuum systems alongside fore-vacuum pumps, vacuum gauges, and sophisticated piping. Therefore, key downstream players include specialized system integrators (especially those serving semiconductor fabs) and equipment manufacturers who incorporate these pumps into larger tools (e.g., sputtering systems, lithography machines). The distribution channel is predominantly direct or through highly specialized distributors who possess the technical expertise required for installation, commissioning, and localized after-sales service. Direct sales dominate transactions involving major multinational semiconductor companies due to the necessity of detailed technical consultations and customized support agreements.

Direct channels facilitate deep collaborative relationships between manufacturers and large end-users, ensuring that pump specifications are precisely matched to application requirements, especially regarding corrosive gas handling and throughput demands. Indirect channels, often utilizing technical representatives or specialized regional distributors, are more common for smaller R&D clients or in geographically dispersed emerging markets. Critical to maintaining value post-sale is the robust service network, including regional repair centers capable of high-precision dynamic balancing and control system recalibration, differentiating premium vendors based on their global service footprint and technical responsiveness.

The primary customers for Maglev Turbo Vacuum Pumps are large corporations and government-funded research institutions that operate highly sensitive and capital-intensive manufacturing or scientific processes requiring extreme vacuum purity and stability. The most significant customer segment is semiconductor device manufacturers (IDMs and Foundries) engaged in the fabrication of integrated circuits, memory chips, and microelectromechanical systems (MEMS). These buyers demand pumps with zero vibration and absolute freedom from hydrocarbon contamination, making maglev technology the only viable choice for many critical steps in wafer processing.

Secondary but rapidly growing customer bases include manufacturers in the flat panel display industry (producing OLED and LCD screens), particularly those involved in thin-film deposition processes requiring large-area uniformity under vacuum. Furthermore, the global scientific community represents a crucial segment, encompassing universities, national laboratories, and large-scale research projects like particle accelerators and fusion reactors (e.g., ITER), which require pumps capable of handling large volumes and extreme operational conditions while maintaining ultra-clean environments for experimental stability.

The purchasing decisions of these end-users are driven not just by initial cost, but fundamentally by reliability, longevity (Mean Time Between Failure), and the vendor's ability to provide swift, specialized global service. Since pump failure can halt production lines valued at billions of dollars, the emphasis is heavily placed on proven track records and comprehensive service agreements rather than cost minimization. Thus, potential buyers are characterized by high purchasing power, long procurement cycles, and stringent technical validation requirements.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 1.2 Billion |

| Market Forecast in 2033 | USD 2.15 Billion |

| Growth Rate | 8.5% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Pfeiffer Vacuum, Atlas Copco (Edwards), SHINKO SEIKI, Ebara Corporation, Osaka Vacuum, Leybold GmbH, Agilent Technologies, ULVAC, Brooks Automation (Helix Technology), CTI Cryogenics (Brooks Automation), BOC Edwards, VAT Group, Fuso Seiki, Shimadzu Corporation, Varian, Kyungwon-Trade, KASHIYAMA, Gasho, EKO-VAK Ltd., Vacuum Systems & Components |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The core technological landscape of the Maglev Turbo Vacuum Pumps Market is defined by advanced magnetic bearing systems and sophisticated power electronics required for high-speed, contactless rotor suspension. Active Magnetic Bearings (AMBs) are the dominant technology, utilizing position sensors and digital signal processors (DSPs) to continuously adjust the magnetic fields, ensuring the rotor remains perfectly centered and stable, even under variable gas loads or minor seismic activity. The continuous refinement in digital control algorithms is crucial, as stability directly translates to lower vibration levels (essential for nanometer-scale precision processes) and allows for higher rotational speeds, thereby increasing pumping efficiency and compression ratios for light gases like hydrogen and helium.

A significant trend involves the development of hybrid bearing systems, which integrate a magnetic suspension for the primary operational axis with a mechanical safety bearing system designed for infrequent contact only during power failure or catastrophic system events. This hybrid approach aims to combine the cleanliness benefits of magnetic levitation with the robustness and smaller footprint often associated with traditional bearing designs, making these pumps suitable for slightly less demanding, but still high-precision, industrial environments. Furthermore, material science innovation plays a crucial role, particularly in developing corrosion-resistant rotor materials and surface treatments that can withstand the highly reactive, corrosive gas chemistries common in advanced etching processes without compromising the structural integrity or balance of the high-speed rotor.

Beyond the mechanical and electronic core, the landscape is increasingly focused on smart technology integration. Modern maglev pumps feature embedded control systems capable of real-time communication (often utilizing industrial protocols like EtherCAT or PROFINET), enabling remote diagnostics, predictive maintenance scheduling through integrated AI/ML modules, and detailed performance logging. The move towards fully digital, interconnected vacuum systems ensures seamless integration into the automated manufacturing ecosystem (Industry 4.0), allowing end-users to maximize tool utilization and minimize process variability across large fleets of production equipment. The continuous technological thrust is centered on higher reliability, reduced power consumption, and increased ability to handle complex gas mixtures.

The regional analysis of the Maglev Turbo Vacuum Pumps Market reveals significant disparities in terms of manufacturing capacity, consumption volume, and technology adoption rates, heavily influenced by global semiconductor supply chains.

Asia Pacific (APAC) Dominance: APAC remains the undisputed market leader, driven by massive investments in semiconductor fabrication plants (fabs) in countries like China, Taiwan, South Korea, and Japan. These nations are home to the world's largest memory chip producers (Samsung, SK Hynix) and foundry operators (TSMC), creating unparalleled demand for high-end vacuum components. Government initiatives and subsidies aimed at boosting domestic chip production further accelerate the installation base of maglev turbo pumps in this region. Moreover, the robust expansion of the flat panel display (FPD) and photovoltaic industries in China significantly contributes to APAC’s leading consumption share. The region is characterized by high-volume, high-throughput manufacturing, necessitating reliable 24/7 vacuum performance.

North America (NA) and Europe: North America and Europe serve as critical hubs for innovation, high-value scientific research, and specialized manufacturing, contributing substantially to market revenue despite lower volume compared to APAC. North America, driven by the concentration of leading scientific institutions, aerospace manufacturing, and advanced materials R&D, shows steady demand for high-performance pumps used in fusion research and specialized analytical instruments (e.g., mass spectrometry). European demand is anchored by Germany's strong industrial base, specifically in high-precision automotive component coatings, R&D in quantum technologies, and established scientific infrastructure. Both regions exhibit mature markets, with demand focused on replacing aging equipment and upgrading systems to leverage AI-enabled predictive maintenance features.

Emerging Markets (MEA & LATAM): The Middle East and Africa (MEA) and Latin America (LATAM) currently hold smaller market shares, but represent significant long-term growth opportunities. Growth in these regions is primarily linked to government initiatives aimed at establishing regional R&D centers, expanding educational institutions, and initial investments in local electronics assembly or solar energy production facilities. Adoption is slower due to high import costs and less developed local service infrastructure, yet the long-term potential remains strong as these regions diversify their economies into high-technology sectors. Strategic market entry in these regions often involves establishing partnerships with local distributors to handle complex installation and maintenance requirements.

The primary advantage is the elimination of mechanical friction and oil lubrication through magnetic levitation, resulting in ultra-clean, contamination-free vacuum environments essential for advanced semiconductor processes (EUV, 3D NAND), zero particle generation, and extremely low vibration levels.

The market is segmented into Low, Medium, and High-Speed pumps (measured in Liters per second). This segmentation dictates suitability for different chamber sizes and gas load requirements, with High-Speed pumps (3,500 L/s and above) typically used for large-volume industrial deposition and etching systems.

Asia Pacific (APAC), particularly driven by China, Taiwan, and South Korea, dominates consumption. This is due to the concentration of major global semiconductor foundries and memory chip manufacturers, who require high volumes of maglev pumps for their continuous, large-scale fabrication line expansion.

The principal restraints include the significantly high initial capital investment required for magnetic bearing technology compared to traditional pumps, coupled with the necessity for highly specialized, proprietary maintenance and service procedures that can lead to vendor dependence.

AI is integrated through advanced monitoring and diagnostics to facilitate predictive maintenance. Machine learning algorithms analyze real-time operational data (vibration, temperature) to forecast potential mechanical failure, thereby maximizing pump uptime, optimizing energy usage, and reducing unexpected downtime in critical production environments.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.