ID : MRU_ 432809 | Date : Dec, 2025 | Pages : 246 | Region : Global | Publisher : MRU

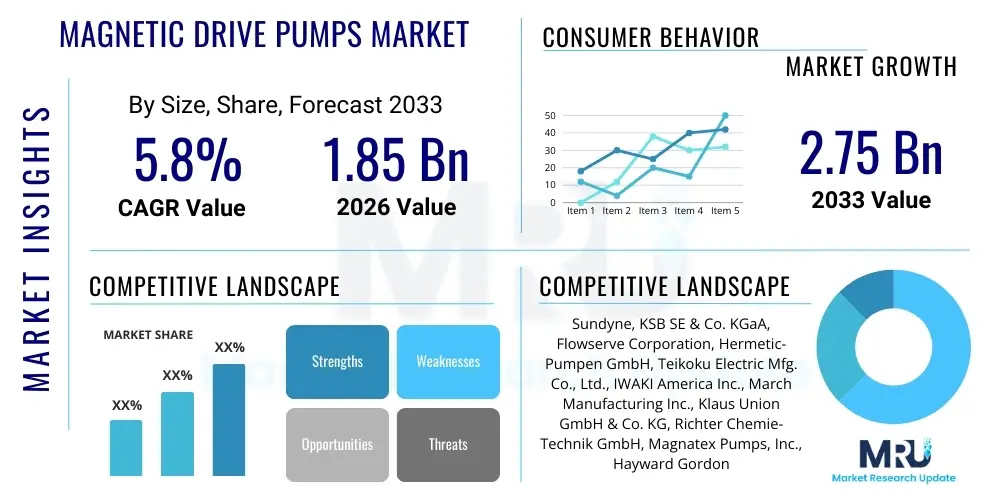

The Magnetic Drive Pumps Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 5.8% between 2026 and 2033. The market is estimated at USD 1.85 Billion in 2026 and is projected to reach USD 2.75 Billion by the end of the forecast period in 2033.

Magnetic drive pumps, often referred to as mag-drive pumps, represent a critical segment of the industrial fluid handling equipment market, primarily utilized for transferring hazardous, corrosive, high-purity, or environmentally sensitive liquids. Unlike conventional centrifugal pumps that use a mechanical seal to prevent leakage around the shaft, magnetic drive pumps employ a hermetically sealed system. This seal-less design uses powerful magnets to transmit torque from the external motor to the internal impeller, completely eliminating the risk of leakage associated with mechanical seals. This inherent safety feature positions them as the preferred solution in industries where fugitive emissions and operational integrity are paramount, such as chemical processing, petrochemical refining, and pharmaceutical manufacturing.

The product portfolio encompasses various designs, including centrifugal, positive displacement, and turbine configurations, tailored to meet diverse flow rates and pressure requirements. Major applications span across critical industrial processes, including acid transfer, solvent circulation, handling highly volatile organic compounds (VOCs), and managing cryogenic liquids. The core benefits driving their adoption include enhanced operational safety due to zero leakage, reduced maintenance costs stemming from the absence of frequently failing mechanical seals, and superior compliance with stringent environmental regulations suchations as the Environmental Protection Agency (EPA) standards regarding hazardous air pollutants. The increasing global emphasis on worker safety and environmental protection directly fuels the demand for these technologically advanced pumping solutions.

Key driving factors propelling the market growth involve the rapid expansion of the chemical and pharmaceutical industries, particularly in emerging economies, which necessitate reliable and safe fluid transfer infrastructure. Furthermore, the mandatory implementation of leak prevention protocols across hazardous manufacturing sites is pushing end-users away from traditional sealed pumps. Technological advancements in magnetic materials, such as high-strength neodymium magnets, have improved pump efficiency and extended operating limits regarding pressure and temperature. The adoption of smart pumping systems incorporating condition monitoring and predictive maintenance features also contributes significantly to market expansion by offering higher reliability and uptime.

The Magnetic Drive Pumps Market is poised for stable growth, underpinned by the increasing necessity for seal-less technology in sensitive industrial applications. Business trends indicate a strong shift towards highly customized and modular pump systems that can handle extreme conditions, including high system pressures and temperature excursions, while maintaining zero emissions. Strategic mergers, acquisitions, and partnerships focused on integrating advanced materials science—such as non-metallic linings (e.g., PTFE, PFA) for highly corrosive fluids—are prominent among key market participants. Furthermore, the trend toward pump standardization and digitalization, including the incorporation of sensors for real-time performance monitoring and connectivity, is defining the competitive landscape. Efficiency and total cost of ownership (TCO) remain primary purchasing criteria, compelling manufacturers to innovate in motor efficiency and bearing durability.

Regionally, Asia Pacific is anticipated to exhibit the highest growth rate, driven by massive investments in new chemical processing plants, establishment of large-scale pharmaceutical manufacturing hubs, and stringent implementation of environmental mandates, particularly in China and India. North America and Europe, while being mature markets, maintain significant market share due to the widespread presence of established petrochemical and specialty chemical industries, coupled with strict regulatory oversight, which necessitates continuous upgrades to seal-less technology. The Middle East and Africa are witnessing gradual growth, primarily fueled by expansion in oil and gas midstream activities and related refining operations where API 685 compliant magnetic drive pumps are critical for safety and operational integrity.

Segment trends reveal that the centrifugal pump type dominates the market due to its wide range of applications, ease of manufacturing, and cost-effectiveness for high-flow, low-head requirements. However, positive displacement magnetic drive pumps are gaining traction in metering and dosing applications where precision and low-pulsation flow are necessary. In terms of end-user sectors, the chemical processing industry remains the largest consumer, driven by the sheer volume and hazardous nature of the fluids handled. Material segmentation shows a growing preference for exotic alloys and reinforced plastics, enabling pumps to handle ultra-corrosive mixtures that standard metallic pumps cannot manage effectively, thereby expanding the applicability of magnetic drive technology in niche segments.

User queries regarding the impact of Artificial Intelligence (AI) on the Magnetic Drive Pumps Market predominantly center on predictive maintenance, operational efficiency improvements, and design optimization. Users are keen to understand how AI algorithms can leverage real-time sensor data (vibration, temperature, pressure, power consumption) to predict impending pump failures, particularly bearing wear or dry running conditions, which are common failure modes in mag-drive systems. Concerns also revolve around the cost and complexity of integrating AI-powered condition monitoring into existing pump infrastructure (retrofitting) and the standardization of data protocols for effective machine learning application. The overarching expectation is that AI will minimize unscheduled downtime and optimize energy consumption by controlling variable speed drives (VSDs) based on process demand fluctuations, transforming maintenance from reactive to prescriptive, thus maximizing the TCO of these high-value assets.

The market trajectory for magnetic drive pumps is profoundly shaped by a confluence of driving factors (D), inherent restraints (R), and emerging opportunities (O), which together constitute the impact forces governing investment and adoption. The primary driver is the stringent global regulatory landscape, specifically environmental mandates aimed at reducing volatile organic compound (VOC) emissions and toxic fluid leakage in chemical and petrochemical facilities. The mandate for zero-leakage pumping solutions provides a non-negotiable incentive for industries to upgrade to magnetic drive technology, which inherently meets these compliance requirements by eliminating mechanical seals. Another significant driver is the reduction in long-term operational expenditure; although the initial capital cost of a magnetic drive pump is higher, the substantial decrease in maintenance costs associated with seal failure, leakage cleanup, and lost production time validates the investment over the pump's lifecycle.

However, the market faces notable restraints. The initial high capital expenditure remains a significant barrier, particularly for small and medium-sized enterprises (SMEs) in developing regions that might opt for cheaper, traditional sealed pumps despite the long-term risks. Technical limitations also present challenges; magnetic drive pumps are susceptible to damage from dry running, as the fluid itself often lubricates the internal bearings. Moreover, operation at very high viscosities or temperatures can lead to magnetic coupling slippage or demagnetization, limiting their applicability in certain extreme process environments. These technical constraints necessitate highly specialized material selection and careful operational training, adding complexity to deployment and management.

Opportunities for market expansion are largely driven by material science innovation and the integration of smart technologies. The development of advanced, highly inert internal bearing materials, such as reaction-bonded silicon carbide (RBSiC) or proprietary ceramics, mitigates the risks associated with dry-running incidents and extends pump life. Furthermore, the expansion of niche end-user segments, such as the handling of supercritical CO2 in carbon capture technology and specialized fluids in high-tech battery manufacturing, presents new, high-growth application areas. The increasing adoption of the Industrial Internet of Things (IIoT) facilitates the integration of advanced sensors and real-time diagnostics, enhancing the pump's reliability and allowing for proactive intervention, which significantly strengthens the value proposition of mag-drive systems over conventional alternatives.

The Magnetic Drive Pumps Market is extensively segmented based on pump type, material of construction, capacity, and end-user industry, enabling manufacturers to address highly specific industrial requirements. This segmentation highlights the diversity of applications and the specialized nature of the fluids being handled globally. The centrifugal segment dominates due to its suitability for high-flow, low-pressure applications common in bulk chemical transfer, while materials segmentation reflects the necessity of chemical compatibility, driving the use of non-metallic options like fluoropolymers for aggressively corrosive media. The following list details the core segmentation structure analyzed in the market research report.

The value chain for magnetic drive pumps begins with upstream activities focused on securing high-quality, specialized raw materials and components, which are crucial for the integrity and performance of seal-less systems. This includes the sourcing of powerful permanent magnets (typically rare-earth alloys like Neodymium-Iron-Boron or Samarium Cobalt), high-strength, chemically resistant housing materials (exotic alloys or fluoropolymer liners), and advanced bearing and thrust materials (Silicon Carbide, ceramic compounds). The performance of the final pump is highly dependent on the precision manufacturing of these internal components, especially the containment shell and magnetic couplings. Key upstream challenges include volatile pricing and supply chain concentration of rare-earth magnetic materials, requiring manufacturers to maintain diversified sourcing strategies and robust inventory management.

The midstream phase involves core manufacturing, assembly, and testing. Manufacturers focus on highly specialized engineering processes to ensure tight tolerances are met, which is critical for preventing magnetic decoupling and minimizing frictional heat generation in the containment area. Research and development activities in this phase are continuous, aiming to improve hydraulic efficiency, increase maximum operating temperatures and pressures, and develop modular designs that simplify maintenance. Downstream analysis focuses heavily on distribution and post-sale services. Given the technical complexity and safety-critical nature of magnetic drive pumps, specialized distribution channels are preferred. These channels often involve highly trained distributors or value-added resellers who can offer expert consultation on fluid compatibility, system integration, and regulatory compliance.

Distribution channels for magnetic drive pumps are broadly categorized into direct sales and indirect sales. Direct sales are typically employed for large, custom projects involving major petrochemical or chemical complexes, where manufacturers engage directly with EPC contractors or end-users to provide bespoke solutions and long-term service agreements. Indirect distribution utilizes regional distributors who maintain local inventory, offer immediate technical support, and handle sales to smaller industrial clients and maintenance, repair, and overhaul (MRO) markets. The importance of the after-market service—including repair kits, spare parts inventory, and rapid technical support—cannot be overstated, as uptime is critical for end-users. The distribution network must be capable of providing rapid access to specialized internal components (bearings, coupling magnets, and containment shells) that require specific expertise for installation, maintaining the pump’s zero-leakage integrity.

The potential customers and end-users of magnetic drive pumps are overwhelmingly concentrated in industries where the handling of hazardous, volatile, or highly corrosive fluids is routine, and regulatory compliance regarding emissions is strictly enforced. The largest segments include the chemical processing industry, encompassing basic chemicals, specialty chemicals, and fine chemicals manufacturers who rely on seal-less pumps for transferring acids, bases, solvents, and polymerization agents without leakage. The pharmaceutical and biotechnology sectors are also crucial buyers, utilizing these pumps for high-purity applications, sterile fluid transfer, and metering of costly or highly potent active pharmaceutical ingredients (APIs), where contamination and leakage are unacceptable risks to both product integrity and worker safety.

Another significant customer base resides within the oil and gas industry, particularly in downstream refining and midstream gas processing, where magnetic drive pumps, often compliant with the demanding API 685 standard, are essential for handling hazardous hydrocarbons, liquefied gases, and high-temperature thermal fluids. These pumps are favored in applications involving highly toxic or flammable fluids like hydrogen sulfide or benzene, where a containment shell offers far superior safety margins compared to mechanical seals. Furthermore, general industrial applications, including surface finishing, semiconductor manufacturing (for high-purity chemical distribution), and nuclear power generation, represent growing segments, driven by the need for reliable containment of aggressive media or highly sensitive cooling loops.

The purchasing decision among these end-users is driven by factors beyond initial cost, focusing heavily on reliability, mean time between failures (MTBF), compliance assurance, and ease of maintenance access, which is often challenging in complex industrial layouts. Key buying personas include plant managers, maintenance engineers, and process safety directors who prioritize long-term system integrity over upfront capital investment. As environmental, social, and governance (ESG) criteria become increasingly relevant, companies dedicated to sustainability are rapidly transitioning their fleets to magnetic drive technology to reduce operational risks and minimize their environmental footprint, positioning them as prime future buyers.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 1.85 Billion |

| Market Forecast in 2033 | USD 2.75 Billion |

| Growth Rate | 5.8% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Sundyne, KSB SE & Co. KGaA, Flowserve Corporation, Hermetic-Pumpen GmbH, Teikoku Electric Mfg. Co., Ltd., IWAKI America Inc., March Manufacturing Inc., Klaus Union GmbH & Co. KG, Richter Chemie-Technik GmbH, Magnatex Pumps, Inc., Hayward Gordon Ltd., HMD Kontro, Cornell Pump Company, Verder International B.V., Finish Thompson Inc., Ruhrpumpen Inc., CDR Pompe S.p.A., Nikkiso Co., Ltd., Tuthill Corporation, Sulzer Ltd. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The core technological evolution in the magnetic drive pumps market revolves around maximizing efficiency, extending operational lifespan, and broadening the fluid handling envelope, particularly concerning high temperatures, high pressures, and corrosive environments. A critical area of advancement involves internal bearing technology. The traditional reliance on carbon graphite or PTFE bearings is being superseded by highly durable, wear-resistant materials like Alpha-Sintered Silicon Carbide (SiC) and proprietary advanced ceramics. These materials offer superior chemical inertness and enhanced resistance to frictional wear, significantly mitigating the risk of dry-running damage—a primary failure mode. The move towards specialized silicon carbide compounds that can handle temperature fluctuations and high system pressures is essential for meeting the requirements of API 685 standards prevalent in the oil and gas sector.

Another major technological trend is the continuous improvement in magnetic coupling design and material strength. Modern magnetic drive pumps utilize powerful rare-earth magnets (Neodymium or Samarium Cobalt) encapsulated within highly optimized containment shells. Engineers are focusing on maximizing the magnetic coupling efficiency (the torque transmission capability) while minimizing eddy current losses within the metal containment shell, which generates unwanted heat and reduces pump efficiency. The introduction of non-metallic containment shells, often made from engineered thermoplastics or composites, is a key innovation for handling highly aggressive fluids, as it eliminates eddy current losses entirely, though these shells are typically limited to lower pressure applications.

Furthermore, the integration of smart technologies, aligning with the principles of Industry 4.0, is rapidly defining the current technology landscape. This includes embedding non-contact sensors directly into the pump housing to monitor critical parameters such as vibration, temperature of the internal fluid and bearings, and power consumption. These sensors feed data to integrated monitoring systems that can detect early signs of cavitation, thrust bearing wear, or magnetic slippage. The use of Variable Speed Drives (VSDs) is also crucial, allowing the pump speed to be precisely matched to the current process requirements, optimizing energy usage and extending component life, thereby offering a significant competitive advantage in terms of operational flexibility and total energy efficiency.

The regional market dynamics for magnetic drive pumps are highly heterogeneous, reflecting varying levels of industrial development, regulatory rigor, and capital investment in infrastructure across the globe. North America maintains a strong position, driven by the mature petrochemical industry and rigorous enforcement of environmental regulations by agencies like the EPA, which necessitates zero-emission technology upgrades. The U.S. remains the largest market in the region, characterized by continuous investment in specialty chemical manufacturing and advanced pharmaceutical production. European markets, particularly Germany, the UK, and France, exhibit stable growth, fueled by the strong presence of chemical manufacturing hubs (e.g., the German chemical industry) and ambitious EU directives focusing on industrial decarbonization and occupational safety, driving demand for premium, highly efficient magnetic drive solutions.

Asia Pacific (APAC) is projected to be the fastest-growing region throughout the forecast period. This accelerated growth is primarily attributed to rapid industrialization, large-scale capacity expansion in the chemical, water treatment, and food processing sectors across China, India, and Southeast Asian nations. Governments in these regions are increasingly adopting and enforcing stricter pollution control norms, pushing local manufacturers towards advanced pumping technologies. Investments in greenfield chemical plants and pharmaceutical formulation facilities are consistently choosing magnetic drive pumps over traditional alternatives to ensure compliance from the outset. Japan and South Korea contribute significantly through their advanced semiconductor and high-tech manufacturing sectors, demanding ultra-high-purity chemical handling capabilities.

Latin America and the Middle East and Africa (MEA) represent emerging opportunities. In MEA, market growth is intrinsically linked to the expansion of oil and gas exploration, refining capacity upgrades, and related downstream chemical conversion projects, particularly in Saudi Arabia and the UAE, where API 685 compliance is often mandatory for high-hazard applications. Latin America, led by Brazil and Mexico, shows potential driven by agricultural chemical production and expanding pharmaceutical manufacturing bases, although economic volatility and dependence on commodity prices can sometimes slow capital expenditure on industrial equipment upgrades. Overall, the market remains globally competitive, with regional success dependent on localization strategies, particularly establishing robust service and spare parts networks to support complex installations.

The primary advantage is the seal-less design, which eliminates leakage and fugitive emissions entirely. This feature is critical for handling hazardous, toxic, or highly valuable fluids, ensuring superior environmental compliance, enhancing worker safety, and drastically reducing maintenance costs associated with mechanical seal failure and system downtime.

The chemical processing industry is the largest consumer due to the volume and corrosive nature of the fluids handled. Other major consuming sectors include the oil and gas industry (especially refining and hazardous gas handling), pharmaceutical manufacturing (for high-purity and sterile applications), and specialized industries like semiconductor manufacturing and nuclear power.

The main risk is damage caused by dry running or inadequate lubrication, as the pumped fluid often lubricates the internal bearings (typically Silicon Carbide). If fluid flow is interrupted, excessive friction can lead to rapid bearing overheating and catastrophic failure. Overcoming this risk requires proper operational protocols, external flush systems, and condition monitoring technology.

Industry 4.0 significantly impacts the market through the integration of IIoT sensors and AI. This allows for real-time condition monitoring, predictive maintenance forecasting, and remote diagnostics. This digitalization maximizes pump uptime, optimizes energy consumption via VSD control, and provides actionable data for prescriptive maintenance strategies, improving overall operational efficiency.

Key material developments focus on advanced internal components, specifically specialized ceramics like Alpha-Sintered Silicon Carbide for bearings, which enhance resistance to wear and thermal shock. Additionally, the increasing use of non-metallic materials (e.g., PFA, PVDF lining) for pump casings allows for the safe and efficient handling of extremely aggressive acids and ultra-high-purity media, broadening application scope.

While the initial capital cost is higher, the total lifecycle cost is lower due to increased Mean Time Between Failures (MTBF). By eliminating the mechanical seal—the most frequent point of failure in conventional pumps—magnetic drive pumps can operate reliably for significantly longer periods, often achieving several years of continuous, zero-maintenance service under ideal conditions, compared to mechanical seals requiring frequent servicing.

Magnetic drive pumps are generally less efficient and face technical constraints when handling very high-viscosity liquids compared to positive displacement pumps. High viscosity can cause excessive heat generation (due to viscous drag within the containment shell) and potentially lead to magnetic coupling slippage. Specialized, high-torque mag-drive designs or mag-drive gear pumps are often used for medium-viscosity applications, but limits apply.

API 685 (Centrifugal Pumps for Refinery Services, Sealless) specifically standardizes the design, construction, testing, and documentation requirements for sealless magnetic drive pumps used in critical petrochemical and refinery services. Compliance with this rigorous standard is often mandatory in the oil and gas sector, directly driving demand for high-specification magnetic drive pumps manufactured by certified companies.

Magnetic coupling slippage occurs when the torque demanded by the pump exceeds the maximum torque capacity that the magnetic coupling can transmit. This causes the driven magnets (impeller assembly) to lag behind the driving magnets (motor side), leading to a reduction in flow/head and significant heat generation within the coupling area due to eddy currents, potentially resulting in demagnetization or pump failure.

Advanced materials, particularly high-temperature Samarium Cobalt magnets, are used instead of Neodymium magnets, which lose strength above 150°C. Furthermore, materials used for the containment shell (e.g., Titanium or special high-nickel alloys) and internal bearings must maintain structural integrity and low thermal expansion at elevated temperatures, allowing the pump to handle fluids up to 400°C in specialized configurations.

Metallic magnetic drive pumps, typically made from stainless steel or exotic alloys like Hastelloy, are designed for high-pressure, high-temperature, and moderate corrosion environments, often complying with API 685 standards. Non-metallic pumps, lined with fluoropolymers (like PTFE or PFA), are used for aggressively corrosive applications (e.g., concentrated acids) at lower pressures and temperatures, offering superior chemical resistance where metallic alloys would fail.

Optimization is achieved through better hydraulic designs, reducing internal friction losses, and minimizing heat generation from eddy currents. Using non-metallic containment shells eliminates eddy current heat entirely, while integrating high-efficiency permanent magnet synchronous motors (PMSM) and VSDs ensures the pump operates at its most efficient duty point corresponding to real-time process demand.

API 685 is highly significant as it provides a standardized, rigorous framework specifically for sealless pumps, which are vital in the petrochemical sector. Compliance assures end-users of high reliability, safety, and interchangeability. This standard drives innovation towards high-pressure, high-temperature capabilities and robust bearing systems, setting the benchmark for premium industrial magnetic drive pumps.

A key challenge is the lack of universal standards for integrating monitoring sensors and data protocols across different vendors, complicating the adoption of centralized AI/IIoT platforms. Additionally, standardizing internal components, especially bearings and containment shells, can be difficult due to proprietary material science and design necessary to manage diverse chemical compatibility and pressure requirements.

EV battery production creates significant new demand for magnetic drive pumps, particularly for handling aggressive electrolyte precursors and solvents used in battery manufacturing processes (e.g., lithium salts, NMP). These applications require ultra-high purity, zero-leakage conditions, and precise flow control, making magnetic drive positive displacement pumps essential components in these advanced facilities.

Unlike mechanical sealed pumps that require routine seal replacement (often annually or semi-annually), magnetic drive pumps typically operate maintenance-free for extended periods. Maintenance is primarily preventative, focusing on bearing checks or system monitoring. Complete overhaul intervals can stretch to five years or more, drastically reducing operational interventions and associated costs.

Manufacturers utilize advanced thermoplastics and fluoropolymers (such as PFA and PTFE lining) known for their near-universal chemical inertness. The selection involves rigorous material testing to ensure that all wetted internal components—including the casing, impeller, and containment shell—can withstand aggressive chemicals and high temperatures without degradation, preventing fluid contamination or structural failure.

Although magnetic drive pumps eliminate the primary seal leakage path, secondary containment involves an additional layer of protection, often a double-walled casing or an external monitoring chamber, designed to capture or detect any breach of the primary containment shell. This system provides an added safety barrier in applications handling highly lethal or explosive materials, fulfilling the highest regulatory safety requirements.

In very high-head (high-pressure differential) applications, magnetic drive pumps require extremely robust containment shells to withstand high system pressures. This often necessitates thicker metallic shells, which increases the air gap between the magnets, potentially weakening the magnetic coupling and increasing eddy current losses, thereby reducing efficiency compared to some sealed, high-pressure pumps.

While magnetic drive pumps have a higher initial capital investment (CapEx), their TCO is generally lower than that of sealed pumps over a 5-to-10-year operational period. This reduction is driven by minimal maintenance expenditure (reduced spare parts, labor), elimination of hazardous leakage cleanup costs, and often superior energy efficiency due to optimized pump designs and VSD integration.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.