ID : MRU_ 431892 | Date : Dec, 2025 | Pages : 246 | Region : Global | Publisher : MRU

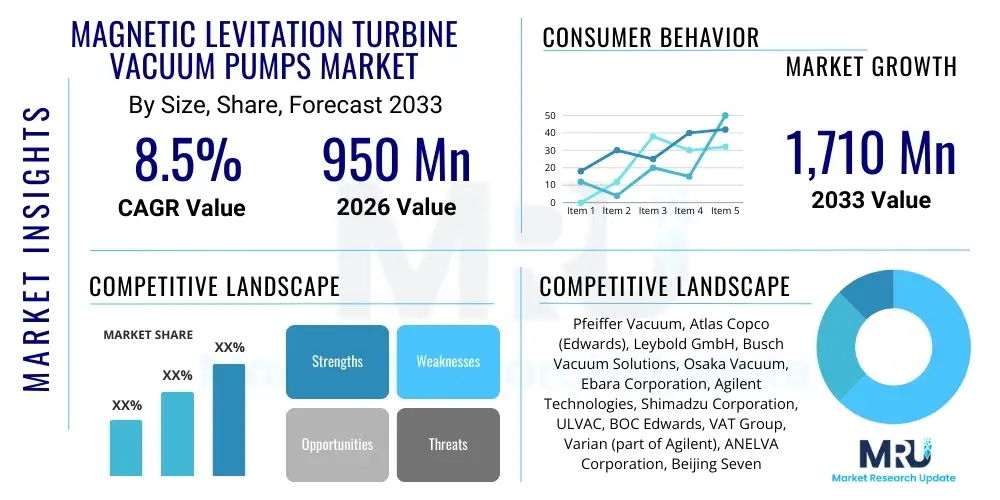

The Magnetic Levitation Turbine Vacuum Pumps Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 8.5% between 2026 and 2033. The market is estimated at USD 950 million in 2026 and is projected to reach USD 1,710 million by the end of the forecast period in 2033.

The Magnetic Levitation Turbine Vacuum Pumps Market encompasses high-performance vacuum generation equipment utilized primarily in environments demanding ultra-clean, high-vacuum, or ultra-high vacuum conditions. These pumps operate using magnetic bearings instead of traditional mechanical bearings, eliminating friction, minimizing contamination risk from lubricating oils, and providing significantly enhanced rotational speeds and operational longevity. This technology is foundational for industries where particulate contamination and hydrocarbon backstreaming are detrimental to process yield and product quality, distinguishing them as critical components in advanced manufacturing and research.

Magnetic levitation turbopumps are complex systems comprising a high-speed rotor suspended by active magnetic fields, integrated with sophisticated controllers that manage stability and speed. Their main function is to draw down vacuum chambers to extremely low pressures, essential for processes such as physical vapor deposition (PVD), chemical vapor deposition (CVD), etching, and ion implantation. Major applications span the semiconductor industry, particularly in the fabrication of advanced microprocessors and memory chips, as well as in the production of flat panel displays (FPDs), solar cells, and sophisticated research laboratories involving high-energy physics and analytical instrumentation.

The core benefits driving market adoption include unparalleled cleanliness due to the absence of mechanical wear and lubricants, leading to zero particle generation within the vacuum environment. Furthermore, these pumps offer lower vibration levels, improved energy efficiency at high rotational speeds, and substantially reduced maintenance requirements compared to conventional pumps. Key driving factors include the persistent scaling down of semiconductor geometries (Moore's Law), the global expansion of OLED and MicroLED display manufacturing, and the accelerating demand for advanced scientific research infrastructure requiring precise, stable vacuum conditions for complex experiments.

The global Magnetic Levitation Turbine Vacuum Pumps Market is experiencing robust growth fueled primarily by irreversible trends toward miniaturization and purity in the electronics and manufacturing sectors. Business trends highlight strategic partnerships between pump manufacturers and equipment suppliers (OEMs) in the semiconductor and FPD domains to integrate bespoke vacuum solutions early in the equipment design cycle. There is a strong movement towards developing intelligent vacuum systems featuring integrated sensors, predictive maintenance capabilities, and remote diagnostic tools, optimizing uptime and reducing total cost of ownership (TCO). Companies are also investing heavily in increasing pumping speeds and improving energy efficiency to meet rigorous industrial standards, especially in power-intensive fabrication plants.

Regionally, the market is heavily dominated by the Asia Pacific (APAC), particularly driven by substantial capital expenditure in semiconductor foundries in Taiwan, South Korea, China, and Japan. These nations are leading global production in logic chips, memory, and advanced display technologies, making them the largest consumers of high-capacity magnetic levitation pumps. North America and Europe remain crucial markets, driven by specialized R&D, aerospace, and the niche market of advanced analytical instruments, with regulatory mandates regarding process cleanliness and energy consumption further supporting technological advancements in these regions.

Segmentation trends indicate that the High Capacity segment, primarily utilized in large-scale semiconductor etching and deposition tools, commands the largest revenue share and is projected to exhibit the highest CAGR due to new fab constructions globally. In terms of application, Semiconductor Manufacturing is the unequivocal leader, dictating the technology roadmap for pump manufacturers. However, the Solar/Photovoltaic segment, driven by the shift towards high-efficiency thin-film solar technologies, and the Industrial Coating segment, focusing on protective and functional coatings for electric vehicle components and architectural glass, are emerging as significant secondary growth vectors.

Common user questions regarding AI's impact on the Magnetic Levitation Turbine Vacuum Pumps Market often revolve around operational efficiency, maintenance prediction, and system longevity. Users inquire whether AI can accurately predict bearing failures, optimize pump parameters in real-time based on fluctuating process loads, and reduce energy consumption without compromising vacuum quality. Key concerns focus on data security, the required infrastructure for edge computing in cleanroom environments, and the reliability of AI algorithms in interpreting complex vibration and temperature signatures unique to magnetic levitation technology. Overall, the expectation is that AI will transform these high-precision pumps from passive components into active, self-monitoring systems, offering superior uptime and maximizing the efficiency of associated capital equipment in high-value manufacturing processes like semiconductor lithography and deposition.

The market dynamics are governed by a complex interplay of technological necessity, high capital expenditure, and volatile global manufacturing cycles. Magnetic levitation technology addresses fundamental industry needs for extreme cleanliness and stability, acting as a primary driver. However, the sophisticated nature of these pumps contributes to high upfront costs and dependency on highly specialized supply chains, presenting significant restraints. The persistent global effort to expand advanced electronics manufacturing and develop cutting-edge materials offers continuous opportunities for market penetration and application diversification, ensuring sustained long-term growth.

Key impact forces include the increasing global capital investment in 300mm and 450mm semiconductor wafer fabrication plants, which rely exclusively on advanced dry pump technology. The shift toward complex 3D NAND and Gate-All-Around (GAA) transistor structures necessitates more frequent and intricate vacuum processes, driving demand for higher capacity, more robust pumps. Furthermore, strict environmental regulations worldwide are phasing out older, less efficient pump technologies, indirectly favoring the adoption of energy-efficient, oil-free magnetic levitation solutions that minimize environmental footprint and hazardous waste.

The competitive environment is characterized by intense R&D focusing on speed, bearing stability, and corrosion resistance, particularly for handling aggressive process gases used in etching and cleaning processes. Strategic acquisitions and intellectual property protection play a crucial role, as market leaders seek to consolidate expertise and secure patented technologies related to magnetic bearing control systems and complex molecular drag stages. The overall market momentum is strong, driven by the non-negotiable requirement for zero contamination in high-value manufacturing, which outweighs the restraint of high initial procurement costs for major industry players.

The Magnetic Levitation Turbine Vacuum Pumps Market is systematically segmented primarily based on capacity, which directly correlates with the pump's application size and the required process throughput, and by end-user application, reflecting the varying operational demands across different high-technology sectors. Capacity segmentation—Small, Medium, and High—allows manufacturers to tailor products for specific equipment needs, from small analytical instruments requiring high ultimate vacuum but low throughput (Small Capacity) to major production tools like large deposition and etching chambers demanding massive gas handling capabilities (High Capacity).

Application segmentation highlights the critical dependency of the market on the semiconductor sector, which drives volume and technological innovation due to its unparalleled demands for process control and particle reduction. However, diversification into related high-vacuum applications, such as solar cell production (requiring large-area uniformity) and specialized R&D (demanding stability and deep vacuum), ensures market resilience against cyclical downturns in any single industry. The structure of the segmentation reflects the technological specificity of the product, where customization is often necessary to meet corrosive gas resistance or specific vibration dampening requirements of the end application.

The convergence of advanced packaging techniques and the emergence of new materials in consumer electronics continue to necessitate specific pump characteristics, driving growth in highly customized sub-segments. Manufacturers are increasingly focusing on modular design concepts to allow quick adaptation to different process requirements, thereby maximizing inventory flexibility and reducing lead times for complex systems. This strategic approach reinforces the prominence of the High Capacity and Semiconductor Manufacturing segments as market revenue pillars while fostering specialized growth in niche application areas.

The value chain for Magnetic Levitation Turbine Vacuum Pumps is intensely specialized and technologically focused, beginning with upstream activities centered on the procurement and fabrication of highly precise components. Upstream analysis involves sourcing rare earth magnets, high-speed motor components, sophisticated control electronics (DSP chips for magnetic bearing control), and specialized corrosion-resistant materials (e.g., specific aluminum alloys or high-grade stainless steel). The complexity of manufacturing and assembly, particularly the precise balancing of the high-speed rotor and the calibration of the magnetic bearing control unit, dictates that the key value capture occurs at the manufacturing stage, where proprietary intellectual property related to bearing stability and pumping efficiency is housed.

The distribution channel is predominantly managed through a blend of direct and indirect methods. Direct sales are crucial for major Original Equipment Manufacturers (OEMs) in the semiconductor industry, such as Applied Materials or Lam Research, where pumps are incorporated directly into multi-million dollar capital equipment. This allows manufacturers to provide customized integration, immediate technical support, and long-term service contracts. Indirect channels, involving specialized distributors and regional sales representatives, are often utilized for serving smaller end-users, R&D facilities, and maintenance/replacement markets, offering broader geographic reach and local technical assistance.

Downstream analysis focuses heavily on the post-sales service and maintenance ecosystem, which is a significant revenue driver due to the high cost and complexity of these pumps. Lifetime service contracts, overhaul, repair, and remote diagnostics are essential components of the downstream value chain, ensuring prolonged operational life and maximum uptime in critical applications. The end-users, primarily semiconductor fabs and FPD plants, view the pump not merely as a component but as a vital system that determines process yield, making long-term technical partnership with the manufacturer a critical factor in purchasing decisions.

The primary customers for Magnetic Levitation Turbine Vacuum Pumps are large-scale industrial entities and research institutions requiring controlled, ultra-clean vacuum environments. Semiconductor manufacturers, including leading foundries (e.g., TSMC, Samsung, Intel) and specialized equipment providers (e.g., TEL, ASML), constitute the most significant customer segment due to the pumps' indispensable role in highly sensitive processes like dry etching, advanced lithography, and metal deposition. These customers demand the highest reliability, exceptional cleanliness (zero hydrocarbon contamination), and pumps capable of resisting highly aggressive process chemistries.

A second major customer base includes manufacturers in the Flat Panel Display (FPD) and Solar/Photovoltaic (PV) industries. FPD companies, especially those producing large-area OLED panels, require high-capacity pumps for large deposition chambers to ensure uniform thin-film characteristics across massive substrates. Similarly, thin-film solar manufacturers depend on magnetic levitation pumps to maintain stable, contamination-free PVD and PECVD processes critical for cell efficiency and longevity. These sectors prioritize high throughput and robust performance over prolonged production cycles.

Niche but high-value customers include national laboratories, university research centers, and specialized industrial coaters. These R&D organizations utilize these pumps for high-energy physics experiments (synchrotrons, particle accelerators), complex analytical instrumentation (high-resolution mass spectrometers), and aerospace material research. While their volume demand is lower, their requirement for absolute vacuum stability and precise control pushes the boundaries of current pump technology, often leading to specialized, customized purchasing agreements and long-term technological collaboration.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 950 million |

| Market Forecast in 2033 | USD 1,710 million |

| Growth Rate | 8.5% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Pfeiffer Vacuum, Atlas Copco (Edwards), Leybold GmbH, Busch Vacuum Solutions, Osaka Vacuum, Ebara Corporation, Agilent Technologies, Shimadzu Corporation, ULVAC, BOC Edwards, VAT Group, Varian (part of Agilent), ANELVA Corporation, Beijing Sevenstar Huachuang Electronic Co., Ltd., Turbo Vacuum Technologies, VSR Technologies, Fushun Vacuum Technology, Vactech Co., Ltd., Precision Plus Vacuum Parts, Adixen (Pfeiffer Vacuum) |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological core of the magnetic levitation turbine vacuum pump market lies in the sophisticated integration of high-speed electromechanics and precise digital control systems. Central to this technology is the Active Magnetic Bearing (AMB) system, which uses electromagnets and real-time electronic feedback loops to levitate the rotor shaft, eliminating mechanical contact and thereby achieving lubrication-free, ultra-clean operation. Continuous advancements focus on enhancing the stiffness and damping capabilities of these bearings to ensure stable operation even under high rotational speeds (up to 90,000 RPM) and during periods of high vibration or uneven gas loading, which is critical in dynamic vacuum applications like etching and plasma processing.

Another crucial technological focus involves optimizing the pump's vacuum stage, which typically combines turbomolecular stages with multiple compression stages, often including specialized molecular drag or regenerative stages (such as Holweck or Siegbahn stages). Manufacturers are leveraging Computational Fluid Dynamics (CFD) modeling to refine blade and groove geometries, maximizing pumping efficiency and compression ratio, especially for light gases like hydrogen and helium, which are notoriously difficult to pump. The incorporation of robust materials, such as ceramic coatings and specialized alloys, is also critical for pumps intended to handle highly corrosive process gases prevalent in advanced semiconductor fabrication.

The trend towards "smart" vacuum systems represents a significant shift, integrating advanced digital controllers capable of sophisticated diagnostic monitoring. Modern pumps feature integrated sensors that track vibration, temperature, current, and rotor displacement. These data are processed in real-time to allow for condition-based monitoring, remote diagnostics, and the implementation of AI-driven predictive maintenance routines. Furthermore, the communication protocols are being standardized to ensure seamless integration with the factory automation systems (e.g., through Ethernet/IP or OPC UA), enabling centralized control and enhanced data exchange necessary for Industry 4.0 environments.

The primary advantage is the elimination of mechanical bearings and lubricating oil, which prevents hydrocarbon backstreaming and particle generation, ensuring an ultra-clean vacuum environment critical for semiconductor and high-purity processes.

Semiconductor Manufacturing is the dominant application segment. Its continuous push for smaller feature sizes (miniaturization) and complex 3D structures dictates the need for higher pumping speeds, enhanced corrosion resistance, and zero contamination, driving all major technological advancements.

Magnetic levitation pumps require significantly less routine maintenance than mechanical pumps, often only needing periodic health checks and eventual full overhaul (rotor balancing, bearing replacement) every 3 to 5 years, leading to a longer operational lifespan and higher mean time between failures (MTBF).

AI integration reduces operational cost significantly by enabling predictive maintenance, minimizing unplanned downtime, and optimizing energy consumption by dynamically adjusting pump parameters based on real-time process gas load requirements, maximizing system efficiency.

Yes, for high-value manufacturing like semiconductor fabrication, the initial high cost is justified by the massive reduction in contamination-related yield losses, superior uptime, and avoidance of catastrophic failure associated with less reliable pump technologies.

The technological evolution within the Magnetic Levitation Turbine Vacuum Pumps Market is inextricably linked to the demanding specifications of the microelectronics industry. As semiconductor processes migrate to 3nm and beyond, the tolerance for particulate matter and residual gases approaches zero, making the oil-free, contact-free operation of magnetic levitation pumps mandatory. Manufacturers are focusing substantial R&D expenditure on developing controllers that can manage highly unbalanced loads caused by aggressive process etching, ensuring rotor stability throughout the operational cycle. This involves complex algorithms that actively adjust the magnetic field strength in multiple axes based on instantaneous sensor feedback, a capability that defines the quality and reliability of a modern turbopump system. The integration of advanced communication standards, such as SEMI standards for factory automation, is no longer optional but a baseline requirement for market entry, reflecting the pumps' role as intelligent nodes within the larger fabrication ecosystem. Furthermore, environmental pressures are driving innovation in pump exhaust management, requiring pumps that can efficiently handle corrosive byproducts while maintaining environmental compliance, thus indirectly promoting the adoption of dry, oil-free designs.

Geographic expansion remains a key strategic pillar for market leaders. While APAC dominates consumption, manufacturers are establishing localized service centers and specialized repair facilities closer to major fabrication clusters globally. This strategy aims to reduce the high costs and logistical complexity associated with shipping large, sensitive equipment internationally for service. The push toward regional self-sufficiency in semiconductor production, visible across North America and Europe, mandates that vacuum suppliers increase their local presence and responsiveness. This regional dynamic is creating localized competition and fostering the development of specialized service providers trained specifically on magnetic bearing technology, thereby enhancing the overall value proposition for end-users seeking robust service level agreements (SLAs).

The segmentation by capacity reflects the diversity of vacuum requirements across industries. The High Capacity segment (over 2,000 L/s) is characterized by intense price competition and technology benchmarking, as these pumps are typically purchased in large volumes for new fabs. Conversely, the Small Capacity segment (under 500 L/s) caters more to high-precision analytical instruments and niche research setups, where stability, ultimate vacuum, and small footprint are prioritized over raw throughput. Companies specializing in the medium capacity range often focus on versatility, designing modular pumps suitable for applications ranging from smaller R&D cluster tools to specialized industrial coating machines. This strategic differentiation allows manufacturers to maintain profitability across the entire product spectrum, balancing high-volume contracts with high-margin, specialized product sales.

Investment cycles in the Flat Panel Display (FPD) market, particularly in OLED and MicroLED technologies, significantly influence demand. FPD manufacturing utilizes deposition processes that require large, specialized vacuum chambers. Magnetic levitation pumps are crucial here because they prevent defects on large glass substrates, maximizing yield on high-value displays. As panel sizes increase and resolutions improve, the necessity for flawless vacuum conditions only escalates, reinforcing the essential nature of magnetic levitation technology in this sector. Similarly, the growing application of vacuum coating processes in electric vehicle (EV) battery manufacturing, specifically for electrode material deposition and separator production, is opening up new, high-volume opportunities for specialized dry vacuum systems capable of handling low vapor pressure materials and demanding inert environments.

The supply chain is highly consolidated, with a handful of key players holding proprietary patents essential for magnetic bearing controls and rotor design. This consolidation results in high barriers to entry, protecting existing market leaders and ensuring that technological advancements are incremental but highly impactful. Furthermore, the regulatory landscape regarding environmental and safety standards, particularly concerning pump exhaust handling and energy consumption in high-volume manufacturing environments, continually pushes manufacturers toward more efficient and compliant magnetic levitation designs. This regulatory pressure acts as a perpetual forcing function for innovation, ensuring that older, less efficient technologies are systematically replaced, favoring the sustained growth of the oil-free, high-performance segment.

Future market growth is also predicted to stem from advanced manufacturing techniques like additive manufacturing (3D printing) of reactive metals. These processes often require inert gas or high vacuum environments to prevent material oxidation and ensure structural integrity. Magnetic levitation pumps, offering reliable deep vacuum capabilities without risk of contamination, are becoming the preferred solution for industrial-scale metal additive manufacturing systems, representing a robust, albeit specialized, vertical market expansion opportunity. The ability to integrate these pumps with sophisticated process monitoring software further enhances their value proposition in these highly regulated, high-precision manufacturing fields.

The competitive dynamics are driven not just by raw performance metrics like pumping speed (L/s) but increasingly by peripheral features such as acoustic signature management and vibration isolation. In ultra-precise metrology and lithography tools, even minor vibrations transmitted through the vacuum system can compromise resolution and quality. Consequently, advanced magnetic levitation systems now feature complex active vibration cancellation technologies, positioning them as premium components that contribute directly to the sub-nanometer precision required in next-generation manufacturing tools. This focus on ancillary performance indicators reinforces the pumps' status as highly engineered capital equipment rather than simple consumables.

The overall structure of the market, characterized by high technological specialization, demanding customer requirements, and significant integration challenges with OEM equipment, ensures that only well-capitalized firms with strong intellectual property and extensive service networks can compete effectively. Pricing strategies often involve complex total cost of ownership (TCO) models, where the initial high procurement cost is offset by exceptionally long MTBF, reduced maintenance labor, and the mitigation of yield loss risks, making the investment decision a calculation based on long-term process reliability and throughput maximization. This strategic approach ensures the magnetic levitation segment remains the gold standard for critical vacuum applications globally.

The influence of AI in reducing total ownership costs is a transformative element. By constantly monitoring internal pump conditions and external process parameters, AI algorithms can pre-emptively flag maintenance needs, optimizing service intervals precisely before critical component degradation occurs. This shift from time-based maintenance to condition-based maintenance maximizes the productive life of the asset while minimizing unexpected operational halts. Furthermore, in applications involving corrosive gases, AI can monitor coating wear rates and predict the necessary timing for rotor chamber cleaning or replacement, thereby significantly extending the service life of internal components and preserving the pump's compression ratio and speed integrity over extended operational periods.

The role of advanced materials science cannot be overstated in this market. Continuous innovation in high-strength, lightweight rotor materials allows for higher rotational speeds and improved energy storage characteristics, crucial for ride-through capabilities during power fluctuations. Similarly, improvements in magnet materials and power electronics components enhance the efficiency of the magnetic bearing control system, reducing heat generation and improving stability under extreme operating conditions. These incremental but vital material advancements are fundamental to achieving the next generation of performance benchmarks required by leading-edge semiconductor lithography and deposition equipment, confirming the market's dependence on deep material expertise alongside digital control engineering.

The competitive landscape is marked by a clear differentiation between full-spectrum providers, who offer integrated vacuum solutions (including magnetic levitation pumps, dry backing pumps, and abatement systems), and specialized component manufacturers. Major players like Pfeiffer Vacuum and Atlas Copco (Edwards/Leybold) leverage their broad product portfolios and global service reach to dominate the market, offering comprehensive packages tailored for large-scale fabs. Smaller, more specialized companies often focus on niche applications, such as high-temperature or extreme-corrosion environments, where specific engineering customizations provide a competitive edge. Strategic mergers and acquisitions are common as large firms seek to assimilate specialized technologies and strengthen their patent portfolios, further consolidating market expertise and reducing fragmentation.

The long-term trajectory of the market is heavily influenced by global geopolitical factors affecting the semiconductor supply chain. As nations prioritize domestic manufacturing resilience, the demand for localized installation, service, and spare parts availability increases. This creates logistical complexities for global suppliers but also opportunities for local joint ventures and expanded regional production facilities. The strategic nature of magnetic levitation pump technology, deemed essential capital equipment for national technological competitiveness, positions the market for consistent, mandated investment regardless of short-term economic fluctuations in other industrial sectors. The focus remains on reliability, purity, and long-term performance guarantees.

The expansion into ultra-high vacuum (UHV) applications, necessary for advanced scientific instruments and next-generation particle accelerators, represents a high-technology frontier. Achieving and maintaining pressures below 10-10 mbar requires exceptionally precise control over internal pump temperatures and gas residual profiles. Magnetic levitation technology excels in this area due to its ability to operate without internal mechanical friction heat, which could otherwise limit ultimate vacuum levels. Development efforts in this segment are focused on integrating specialized cryogenic or getter stages alongside the turbomolecular pump to maximize capture efficiency of residual light gases, pushing the boundaries of accessible vacuum environments for fundamental research.

In conclusion, the Magnetic Levitation Turbine Vacuum Pumps Market is a high-growth, high-value sector defined by technological intensity and stringent performance requirements set by the global microelectronics industry. The market's structural drivers—zero tolerance for contamination, demand for high reliability, and relentless pursuit of miniaturization—ensure sustained investment in magnetic levitation technology. The adoption of smart, AI-integrated systems further enhances their value proposition, cementing their status as indispensable tools for 21st-century advanced manufacturing and scientific research.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.