ID : MRU_ 432814 | Date : Dec, 2025 | Pages : 245 | Region : Global | Publisher : MRU

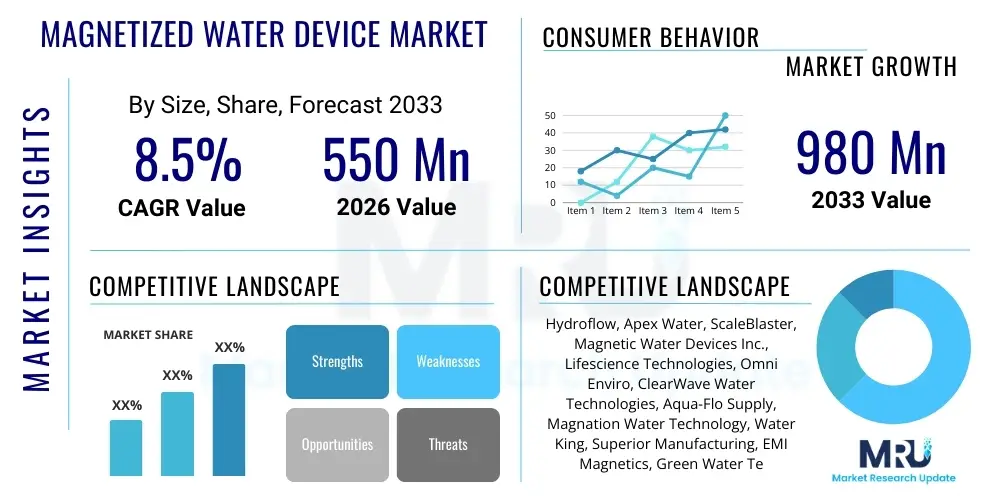

The Magnetized Water Device Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 8.5% between 2026 and 2033. The market is estimated at USD 550 million in 2026 and is projected to reach USD 980 million by the end of the forecast period in 2033.

The accelerated growth trajectory of the magnetized water device market is fundamentally driven by the escalating global concern over water quality and the imperative need for sustainable, chemical-free water treatment solutions across industrial and agricultural sectors. Market expansion is particularly pronounced in regions experiencing severe water stress and reliance on hard water sources, necessitating effective, non-invasive methods for scale prevention in critical infrastructure such as boilers, cooling towers, and heat exchangers. Furthermore, the increasing awareness regarding the environmental impact and operational costs associated with traditional chemical-based descaling methods acts as a significant catalyst, prompting industries to explore and adopt magnetic water conditioning systems as a viable, long-term alternative.

Technological advancements, specifically in the development of sophisticated electromagnetic devices that offer adjustable field strength and superior performance compared to traditional permanent magnets, are crucial factors bolstering market valuation. These advanced systems provide measurable improvements in efficiency, especially in high-flow and high-temperature industrial environments where scaling is rapid and detrimental. Concurrently, the burgeoning residential segment, fueled by growing health consciousness and demand for softened water without salt or chemical additives, contributes meaningfully to the overall market size. This convergence of industrial necessity, environmental sustainability mandates, and consumer wellness trends positions the market for robust financial expansion through 2033, translating into significant revenue opportunities for manufacturers specializing in durable and highly efficient magnetic water treatment technologies.

The Magnetized Water Device Market encompasses technologies designed to alter the physical properties of water by exposing it to powerful magnetic fields, primarily aiming to reduce the formation of mineral scale (calcium carbonate, magnesium salts) in piping and equipment without resorting to chemical additives. These devices, categorized generally into permanent magnet systems and electromagnetic systems, induce physical changes in dissolved minerals, changing their crystal structure from sharp, clinging calcite to soft, non-adhering aragonite, which passes easily through the system. Major applications span across industrial water treatment, where they maintain efficiency in cooling and heating systems; agriculture, where enhanced water absorption potentially boosts crop yields; and residential use, addressing hard water issues for improved appliance longevity and personal care.

The principal benefits driving the adoption of magnetized water devices include substantial reduction in equipment maintenance costs by minimizing downtime related to descaling, prolonged lifespan of water-handling infrastructure, and significant environmental advantages stemming from the elimination of harmful chemicals and salts typically used in conventional softening processes. In the industrial context, the devices support energy efficiency by preventing the insulating effect of scale buildup on heat transfer surfaces, resulting in lower operational expenses. For agricultural operations, research suggests potential improvements in soil permeability and nutrient uptake, positioning these devices as a critical component in sustainable irrigation management, particularly in drought-prone areas or regions utilizing brackish water sources.

Driving factors underpinning the market's trajectory involve stringent global regulatory frameworks pushing for sustainable water management practices and mandates restricting chemical discharge in industrial wastewater. The persistent challenge of water scarcity in developing and developed nations necessitates technologies that optimize water use and minimize waste, which magnetic conditioning facilitates by improving water quality for reuse applications. Furthermore, heightened operational cost pressures on businesses incentivize the adoption of solutions that yield rapid returns on investment through reduced energy consumption and decreased reliance on expensive chemical inhibitors, thereby solidifying the market's foundation for sustainable long-term growth and widespread industrial application integration.

The executive outlook for the Magnetized Water Device Market highlights strong integration trends towards smart water management systems and advanced materials utilization. Business trends show a strategic shift among manufacturers toward offering comprehensive monitoring and validation services alongside the hardware, addressing long-standing market skepticism regarding efficacy through demonstrable performance metrics integrated via IIoT platforms. Consolidation among smaller, specialized technology providers by large industrial water treatment conglomerates is accelerating, aiming to integrate magnetic conditioning solutions into broader, multi-technology water hygiene portfolios. This market maturation involves increased investment in rigorous third-party testing and standardization protocols, enhancing consumer and industrial confidence in magnetic water treatment as a reliable scale mitigation strategy.

Regionally, Asia Pacific (APAC) stands out as the primary engine of growth, capitalizing on massive industrial expansion, particularly in manufacturing, power generation, and chemical processing sectors requiring high-volume water recycling and scale control. North America and Europe, while having established markets, exhibit mature growth driven by the residential wellness segment and strict environmental mandates compelling industries to adopt zero-chemical water conditioning methods, promoting retrofitting of existing infrastructure. Latin America and the Middle East and Africa (MEA) represent emerging high-potential regions, primarily driven by agricultural needs—where magnetic water treatment is applied to improve irrigation efficiency under challenging hard water or saline conditions—and by rapid urbanization demanding efficient municipal water distribution maintenance.

Segmentation trends indicate a strong preference for high-power electromagnetic devices in critical industrial applications due to their controllability, adjustability, and superior scale inhibition capability in dynamic environments, contrasting with the dominance of simpler, lower-cost permanent magnet systems in the residential and small-scale commercial sectors. The industrial segment, encompassing HVAC, process heating, and utility management, maintains the largest market share by value, though the agriculture segment is projected to exhibit the highest CAGR due to rapid technological adoption necessitated by resource scarcity. Distribution channels are increasingly diversifying, with online retail platforms facilitating access for residential consumers, while complex industrial systems rely heavily on direct sales and specialized engineering consultancies for installation and calibration.

User queries regarding the intersection of Artificial Intelligence (AI) and the Magnetized Water Device Market primarily center on the validation of device efficacy, the integration of these systems into smart industrial ecosystems (IIoT), and the optimization of magnetic field parameters for variable water chemistries. Users are keenly interested in how AI can move magnetic conditioning beyond anecdotal evidence to become a scientifically verifiable, performance-guaranteed solution. Key concerns revolve around predictive maintenance—determining the remaining lifespan and optimal cleaning schedules for industrial infrastructure based on real-time scaling rates—and using machine learning algorithms to correlate magnetic field adjustments with specific chemical signatures (TDS, hardness, pH) to maximize the antiscaling effect, ensuring the technology performs optimally across diverse operational parameters without manual intervention.

The adoption of AI and machine learning is revolutionizing the functionality of high-end electromagnetic water treatment systems. AI algorithms are essential for analyzing sensor data streams related to water flow rates, temperature, pressure, and instantaneous mineral concentration. By processing this complex, multi-dimensional data, AI enables the predictive adjustment of the electromagnetic field frequency and intensity in real-time. This dynamic tuning ensures that the magnetic conditioning effect remains optimized, compensating for fluctuations in industrial input water quality or operational load, thereby significantly improving overall scale prevention reliability and delivering quantifiable performance metrics that address historical market skepticism concerning inconsistent results. This transition toward AI-driven, self-optimizing devices is pivotal for broader industrial acceptance.

Moreover, AI contributes significantly to the operational efficiency and commercial viability of these devices through advanced monitoring and diagnostics. Machine learning models can be trained on extensive datasets covering various water sources and scaling types, allowing them to accurately predict future scaling potential and schedule proactive, minimal intervention maintenance cycles, transitioning the industry from reactive descaling to preventive management. For manufacturers, AI assists in optimizing product design and calibration by simulating complex fluid dynamics and magnetic interactions, accelerating the development of highly customized and effective solutions tailored to specific client needs, thus integrating the magnetized water device market fully into the paradigm of Industry 4.0 and advanced asset management.

The magnetized water device market is propelled by key Drivers such as the increasing global emphasis on sustainable water usage, stringent environmental regulations limiting chemical discharge, and the rising cost of energy, making scale prevention critical for efficiency gains in thermal processes. Opportunities are vast, particularly in emerging economies with rapidly expanding industrial bases and large agricultural sectors grappling with hard water issues; miniaturization and integration into smart home systems also present lucrative expansion paths in the residential segment. Restraints include the persistent lack of universal, standardized, and independent scientific validation for the technology's effectiveness across all conditions, high upfront capital expenditure for advanced electromagnetic systems, and strong competition from established chemical and physical water treatment methods, necessitating aggressive market education and verifiable performance data to overcome skepticism.

Impact Forces analysis reveals a competitive landscape governed by low to moderate supplier power, as raw materials (especially Neodymium magnets and specialized electronic components) are largely commoditized, although expertise in complex electromagnetic system design elevates the power of key technology leaders. Buyer power is moderate to high, particularly in industrial sectors, due to the availability of substitutes (chemical inhibitors, reverse osmosis) and the requirement for substantial proof-of-concept before large-scale adoption, demanding competitive pricing and guaranteed efficacy from device manufacturers. The threat of new entrants is moderate; while permanent magnet systems are easy to manufacture, the complexity and intellectual property surrounding high-performance electromagnetic and AI-integrated systems pose significant barriers to entry for unspecialized competitors, focusing rivalry intensely among existing, established players.

The greatest challenge remains regulatory uncertainty; while sustainability goals favor non-chemical solutions, the absence of standardized testing protocols across major industrialized nations hinders rapid market penetration. Overcoming this requires concerted industry effort to collaborate with regulatory bodies and academic institutions to establish clear performance benchmarks. Strategic focus on large-scale industrial customers, demonstrating verifiable reductions in operational costs (fuel consumption, maintenance labor, chemical purchase) through robust data collection, is essential. The increasing integration of IoT capabilities addresses the restraint of performance ambiguity, transforming these devices into data-generating assets crucial for modern industrial facility management and reinforcing their competitive position against conventional water treatment modalities.

The Magnetized Water Device Market is comprehensively segmented based on three primary dimensions: the Type of magnetic technology utilized, the Application industry served, and the Distribution Channel through which the products reach the end-user. This segmentation is crucial for understanding the diverse demands and technical specifications required across different market verticals. Technological segmentation highlights the fundamental distinction between passive permanent magnet systems, which require no external power and are favored for simple applications, and active electromagnetic systems, which provide controllable field strength necessary for complex, high-flow industrial settings. Application segmentation differentiates the high-value industrial needs (e.g., cooling towers, heat exchangers) from the high-volume, cost-sensitive agricultural and residential sectors, each presenting unique scaling challenges and requiring tailored device designs and material specifications.

The industrial application segment holds the dominant share globally, driven by the critical need to maintain operational efficiency and comply with strict environmental mandates concerning chemical discharge. Within the industrial sub-segments, HVAC and boiler systems represent particularly high-growth areas due to the direct correlation between scale buildup and drastic energy efficiency losses. Meanwhile, the agricultural sector, especially large-scale farming and horticulture, is rapidly adopting these devices to mitigate the effects of hard or saline irrigation water on soil structure and crop development, showcasing the highest projected CAGR. Distribution channel analysis confirms that industrial clients rely predominantly on direct sales and specialized system integrators, demanding bespoke solutions and technical support, whereas the mass market residential segment is increasingly reliant on e-commerce and specialized retail channels for ease of access and installation.

The value chain for the Magnetized Water Device Market commences with upstream activities centered on the procurement and processing of highly specialized raw materials, primarily focusing on rare-earth magnets (such as Neodymium Iron Boron, NdFeB) and high-quality conductive materials for coils in electromagnetic systems. Manufacturing involves precision engineering, integrating magnetic components with durable housing materials (stainless steel, specialized polymers) capable of withstanding high pressure and varying temperatures, alongside sophisticated electronics assembly for active devices incorporating microprocessors and sensors. Critical value addition occurs at the design and R&D stage, where manufacturers focus on optimizing magnetic field geometry and flux density to maximize water conditioning efficiency, often requiring specialized simulation software and rigorous laboratory testing to validate performance claims, forming the foundation of product quality and intellectual property.

Downstream activities involve specialized distribution channels tailored to the end-user segment. For the large industrial segment, the distribution is characterized by direct sales models, utilizing specialized engineering sales teams that provide extensive pre-sales consultation, system customization, and post-installation technical support, often requiring integration into existing complex industrial plumbing and control systems. This indirect channel leverages system integrators and HVAC contractors who act as intermediaries, embedding magnetic devices within larger plant maintenance contracts. Conversely, the residential and small commercial sectors rely more on indirect distribution through large retail chains, hardware stores, and burgeoning e-commerce platforms, emphasizing simple installation instructions and consumer warranties, where logistics and inventory management become critical components of efficiency.

The efficiency of the value chain is significantly influenced by the efficacy of the after-sales service and validation process. Given the inherent skepticism surrounding the efficacy of magnetic water treatment, downstream success hinges on continuous performance monitoring, especially for industrial installations. Service providers often offer data logging and analytical services to demonstrate measurable scale reduction and energy savings, translating product features into clear operational benefits. This focus on verifiable results strengthens the direct channel relationship and contributes to repeat business. Overall, the value chain is complex, requiring high-precision manufacturing upstream and specialized, application-specific technical expertise downstream to successfully penetrate and sustain market share across diverse industrial, agricultural, and residential customer bases.

Potential customers for the Magnetized Water Device Market span a broad spectrum of industries and consumer groups, united by the common need to mitigate the detrimental effects of hard water scaling, erosion, and biological fouling without relying heavily on traditional chemical treatments. The primary target segment comprises large industrial facilities, including power generation plants, petrochemical refineries, manufacturing sites, and large commercial HVAC operators (hotels, corporate campuses), where water cooling towers, boilers, and heat exchangers are fundamental to operation. These institutional buyers are motivated by the imperative to reduce energy costs associated with insulating scale layers, minimize equipment downtime for maintenance, and comply with strict environmental regulations limiting chemical discharge into municipal waste streams, seeking robust, high-capacity electromagnetic systems offering measurable ROI through enhanced thermal efficiency and reduced chemical expenditure.

The agricultural sector represents a high-growth customer base, particularly in regions facing water scarcity or utilizing brackish/hard groundwater for irrigation. Large commercial farms, vineyards, and greenhouse operators are seeking magnetic conditioning solutions to improve soil permeability, enhance water absorption efficiency by plants, and prevent scaling in drip irrigation lines and nozzles, which are easily clogged by mineral deposits. This customer group values durability, ease of installation, and proven efficacy in increasing crop yields or mitigating the negative effects of salinity, often adopting medium-sized permanent magnet devices or smaller, specialized electromagnetic units integrated into pump systems. The economic incentive here is directly tied to operational longevity and crop productivity, making them sensitive to both performance and affordability in irrigation infrastructure maintenance.

Finally, the residential market segment constitutes a large volume of potential buyers, consisting primarily of homeowners living in areas characterized by high water hardness, who seek soft water benefits for personal comfort and appliance protection. These consumers prioritize simple, non-salt-based water softening alternatives to protect expensive assets like water heaters, washing machines, and plumbing fixtures from premature wear and efficiency loss caused by limescale buildup. The residential buyers typically purchase easy-to-install, entry-level permanent magnet devices through retail or online channels, motivated by health consciousness (avoiding salt intake associated with traditional softeners) and the desire for hassle-free maintenance, providing a consistent demand driver for standardized, mass-produced magnetic conditioning units.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 550 Million |

| Market Forecast in 2033 | USD 980 Million |

| Growth Rate | CAGR 8.5% |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Hydroflow, Apex Water, ScaleBlaster, Magnetic Water Devices Inc., Lifescience Technologies, Omni Enviro, ClearWave Water Technologies, Aqua-Flo Supply, Magnation Water Technology, Water King, Superior Manufacturing, EMI Magnetics, Green Water Technologies, Cascade Water Systems, Ionization Technology Solutions, GMX International, VRT Water, Watts Water Technologies (Select Offerings), Pura-Sys, Global Treatment Solutions |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technology landscape for magnetized water devices is characterized by a dichotomy between static and dynamic magnetic field generation methods, coupled with increasing sophistication in sensor integration and control electronics. Static devices predominantly rely on high-grade rare-earth magnets, notably Neodymium Iron Boron (NdFeB), which offers superior residual magnetism and coercivity compared to older Ferrite magnets, allowing for compact, powerful, and maintenance-free permanent magnet systems. The key technological focus here lies in optimizing the magnet arrangement (e.g., opposing poles, specific flow paths) and housing material design to ensure maximum magnetic field penetration and uniform exposure across the water flow, maximizing the conditioning effect while maintaining hydraulic integrity under high-pressure conditions typical of industrial piping systems.

Conversely, the leading technological advancements are concentrated within dynamic or active systems, utilizing pulsed electromagnetic fields (PEMF). These systems employ conductive coils powered by microprocessors to generate magnetic fields that are variable in intensity, frequency, and waveform. The critical innovation in this segment is the development of sophisticated control algorithms that allow the device to dynamically adjust the field parameters in real-time based on input from integrated sensors monitoring water flow, temperature, and hardness levels. This intelligent adjustment capability ensures that the device provides optimal scale mitigation performance regardless of rapid changes in water quality or operational load, directly addressing the variability and inconsistency historically associated with passive magnetic devices, thus increasing operational reliability in mission-critical applications.

Furthermore, the integration of digital technology, encompassing smart monitoring systems and IoT connectivity, is transforming the technological landscape. Modern magnetized water devices often include conductivity probes and pressure sensors that transmit data wirelessly to cloud platforms, enabling remote diagnostics, performance tracking, and the application of machine learning for predictive maintenance. This shift transforms the device from a simple physical treatment unit into a data-generating asset, providing verifiable proof of efficacy and supporting proactive asset management strategies for industrial clients. The ongoing research focuses on exploring alternative magnetization techniques, such as induced high-frequency resonance or electro-chemical hybridization, aiming to broaden the spectrum of minerals affected and enhance the overall longevity and effectiveness of the conditioning effect on highly complex water chemistries.

Magnetized water devices prevent scale by exposing water to strong magnetic fields, which alters the charge and crystal structure of dissolved hard minerals like calcium carbonate (calcite). This alteration causes the minerals to transform into a softer, non-adhering crystalline structure called aragonite. Aragonite remains suspended in the water and is flushed out of the system, preventing hard, insulating scale from accumulating on pipes, heating elements, and critical industrial surfaces, thereby maintaining system efficiency without the use of chemical softeners.

While the market has historically faced skepticism, recent independent scientific studies and rigorous industrial field trials, particularly involving advanced electromagnetic systems, have provided increasing evidence of measurable scale reduction and efficiency improvements under specific operational conditions. Efficacy often depends heavily on factors like magnetic field strength, flow rate, water chemistry, and precise device calibration. Reputable manufacturers now focus on providing verified performance data and third-party certifications tailored to specific industrial applications to substantiate their efficacy claims.

Permanent magnet devices utilize static rare-earth magnets (like Neodymium) and require no external power, offering a cost-effective, low-maintenance solution primarily suitable for residential and small commercial applications with consistent flow. Electromagnetic devices, conversely, are active systems that use electricity to generate dynamic, pulsed magnetic fields. These systems offer controllable field intensity and frequency, enabling real-time adjustment based on water parameters, making them superior for large-scale industrial applications where high flow rates and fluctuating water quality demand optimized, high-performance scale mitigation.

Magnetized water devices are renowned for their low maintenance requirements and long lifespan. Permanent magnet devices have a theoretical lifespan exceeding 50 years, often requiring no maintenance as the magnets do not degrade significantly over time. Electromagnetic devices typically have a lifespan determined by their electronic components (usually 10 to 20 years); maintenance primarily involves checking power supply integrity and ensuring sensor calibration, with no physical component replacement necessary for the magnetic conditioning function itself, resulting in significantly reduced operational expenditure compared to chemical treatment systems.

The Industrial application segment holds the largest market share by value due to the high cost and complexity of the systems required for large-scale operations, such as cooling towers, boilers, and heat exchangers in power generation and manufacturing sectors. These industries prioritize maintaining thermal efficiency and minimizing downtime caused by scale, leading to the adoption of expensive, high-capacity, and technologically advanced electromagnetic systems. The financial savings realized through reduced energy consumption and lower chemical purchase costs solidify the industrial sector's dominance in market valuation.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.