ID : MRU_ 434636 | Date : Dec, 2025 | Pages : 248 | Region : Global | Publisher : MRU

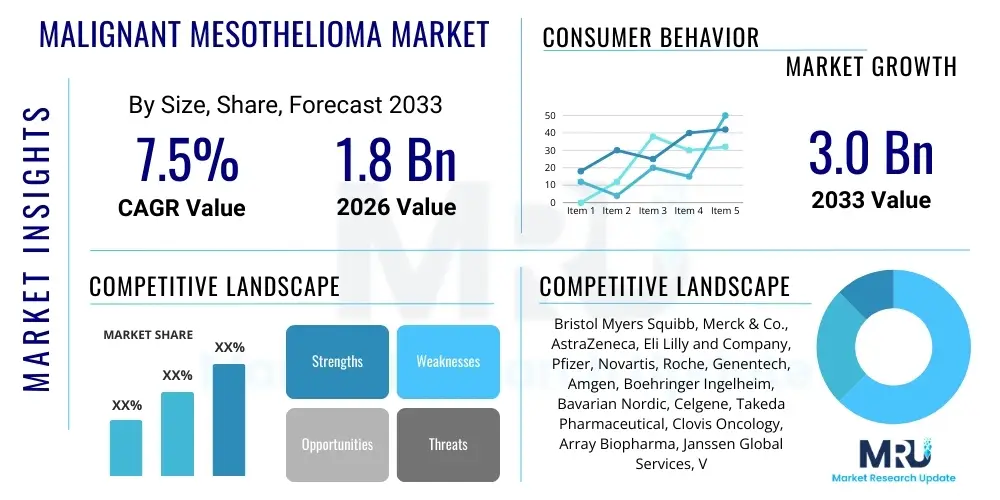

The Malignant Mesothelioma Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 7.5% between 2026 and 2033. The market is estimated at USD 1.8 Billion in 2026 and is projected to reach USD 3.0 Billion by the end of the forecast period in 2033.

The Malignant Mesothelioma Market encompasses the global landscape of diagnostics, therapeutics, and surgical interventions aimed at treating this aggressive cancer primarily linked to asbestos exposure. Malignant Mesothelioma (MM) is characterized by tumors arising from the mesothelium, the protective lining covering most internal organs, most commonly affecting the pleura (lining of the lungs). The complexity and poor prognosis associated with MM necessitate continuous research and development into novel treatment modalities, driving significant market activity across oncology and biopharmaceutical sectors. Key market participants include pharmaceutical companies focused on developing next-generation chemotherapy combinations, immunotherapies, and targeted therapies, alongside medical device manufacturers providing advanced surgical and radiation equipment.

Major applications of market solutions center around extending patient survival and improving quality of life. Traditional treatment regimens include multimodal approaches involving surgery (such as pleurectomy/decortication or extrapleural pneumonectomy), platinum-based chemotherapy (like cisplatin and pemetrexed), and radiation therapy. However, recent scientific breakthroughs have positioned immunotherapy, particularly checkpoint inhibitors, as foundational elements in the treatment algorithm, offering substantial benefits in previously refractory cases. These advances have led to a noticeable shift in clinical practice guidelines and expenditure, bolstering market growth.

The primary driving factors propelling the market forward include the increasing global incidence of mesothelioma due to historical asbestos exposure peaking decades ago, the rising geriatric population which is more susceptible to cancer, and robust governmental and private funding allocated to oncology research. Furthermore, the expiration of patents for established drug regimens is paving the way for generic competition, potentially improving access, while the high unmet medical need associated with MM continues to incentivize pharmaceutical innovation in precision medicine and personalized oncology.

The Malignant Mesothelioma Market is experiencing a transformative period, primarily driven by the success of immune-oncology agents and increasing sophistication in diagnostic tools, particularly liquid biopsies and advanced imaging. Business trends highlight strategic partnerships between biotech startups focusing on novel targets (like anti-mesothelin therapies) and large pharmaceutical companies seeking to diversify their oncology portfolios. Venture capital investment remains robust in clinical-stage companies demonstrating positive data in Phase II and Phase III trials for late-stage mesothelioma. Furthermore, the market is characterized by intense competition to establish first-line superiority, shifting away from standard cytotoxic combinations towards immunotherapy monotherapy or combination regimens, which command premium pricing and drive overall market revenue expansion.

Regionally, North America maintains the dominant market share, attributed to advanced healthcare infrastructure, high awareness among clinicians, substantial research and development expenditure, and favorable reimbursement policies for expensive biologic therapies. However, the Asia Pacific (APAC) region is projected to register the fastest growth rate due to improving healthcare access, increasing awareness in densely populated countries, and a large patient pool, particularly in industrializing economies where historical asbestos use was prevalent. European markets demonstrate stability, with regulatory bodies increasingly streamlining approval processes for orphan drugs targeting rare cancers like MM, thereby accelerating market penetration.

Segment trends indicate that the Immunotherapy segment is poised for the highest growth, gradually replacing or complementing traditional chemotherapy as the cornerstone of care. Within the end-user segmentation, specialized Cancer Centers and Academic Research Institutes are crucial for administering complex, state-of-the-art treatments and clinical trials. Technological advancements in diagnostic tools that allow for earlier detection and precise molecular profiling are also gaining prominence, enabling tailored treatment selection and significantly impacting patient outcomes, thus influencing purchasing patterns within institutional settings.

Users frequently inquire about AI's potential to revolutionize the often-delayed diagnosis of Malignant Mesothelioma (MM), considering its non-specific initial symptoms and long latency period. Key questions revolve around how Artificial Intelligence can enhance the interpretation of complex radiological scans (CT, MRI, PET) and histopathological slides to detect subtle signs of pleural thickening or nodules earlier than human counterparts. There is also significant user interest in AI-driven drug discovery, specifically concerning the identification of novel drug targets, prediction of patient response to existing treatments (especially complex immunochemotherapy combinations), and optimization of clinical trial design for rare populations. The primary themes summarized include using AI for precision oncology tailoring, improving diagnostic accuracy to overcome the latency challenge, and accelerating the development pipeline for treatments where therapeutic options are currently limited.

AI's application extends beyond mere diagnosis into prognostic modeling and treatment sequencing. Machine learning algorithms, trained on vast datasets of genomic, clinical, and pathological information, are becoming indispensable in predicting which MM subtype (epithelioid, sarcomatoid, or biphasic) is likely to respond best to a specific combination of immunotherapies or targeted agents. This capability enhances clinical decision-making, minimizing resource wastage associated with ineffective treatments and significantly improving the patient's therapeutic journey. Moreover, AI systems are being integrated into hospital workflow management to assist in trial matching and monitoring patient adherence and toxicity profiles in real-time, ushering in an era of truly personalized care for this difficult-to-treat malignancy.

The market dynamics for Malignant Mesothelioma are governed by a complex interplay of Drivers, Restraints, and Opportunities (DRO) that collectively shape market trajectory and impact forces. The most prominent driver is the prolonged latency period of asbestos exposure, ensuring a steady, though geographically variable, stream of new diagnoses globally, often decades after initial exposure. Coupled with this, the rapid innovation cycle within oncology, particularly the advent of successful immunotherapy regimens like pembrolizumab and nivolumab in combination, provides crucial growth momentum. These immunotherapies, offering significant survival advantages over standard chemotherapy, command high pricing and drive market value despite the relatively low patient incidence compared to other common cancers. Furthermore, global initiatives aimed at early detection and improved screening methodologies, even for high-risk populations, contribute positively to the market size.

Conversely, significant restraints hinder market expansion. The exceedingly high cost of novel biologic therapies places substantial pressure on healthcare systems and limits accessibility, particularly in developing economies. Furthermore, the inherent complexities of diagnosing MM, often mistaken for more common lung ailments, lead to delayed staging and poor patient prognosis, limiting the effectiveness of expensive, early-stage treatments. Toxicities associated with intensive multimodal therapies, including radical surgery and high-dose chemotherapy or radiation, also restrain widespread adoption, prompting clinicians and patients to seek palliative rather than curative treatments in many advanced cases. The small patient population also renders clinical trials expensive and difficult to enroll, slowing the pace of novel drug approvals.

Opportunities in the market primarily reside in the development of combination therapies that target multiple resistance mechanisms simultaneously, moving beyond PD-1/PD-L1 inhibition to include novel checkpoint targets or cellular therapies (e.g., CAR T-cell therapy targeting mesothelin). The growing acceptance and integration of multimodal treatment planning, involving specialized surgical oncology and radiation technologies (like Intensity-Modulated Radiation Therapy or IMRT), represent critical commercial avenues. Moreover, significant potential exists in emerging biomarkers and liquid biopsy technologies that can monitor disease progression or recurrence non-invasively, providing new revenue streams in the diagnostic segment and enabling real-time therapeutic adjustments.

The Malignant Mesothelioma market segmentation provides a granular view of revenue distribution across treatment types, disease types, and end-user settings, reflecting where current therapeutic expenditure is concentrated and where future investment is anticipated. Treatment modalities are rapidly evolving, moving from cytotoxic dominance to immune-oncology leadership. Disease type segmentation confirms that Pleural Mesothelioma, given its prevalence (approximately 80-90% of all cases), constitutes the largest market share, though peritoneal and other rare forms offer unique challenges and niche market potential for specialized treatments. The end-user segment underscores the criticality of specialized oncology centers in administering these complex, high-cost treatments.

The value chain for the Malignant Mesothelioma market is highly specialized, beginning with the upstream discovery and development phase characterized by significant R&D investments by biopharmaceutical companies and academic institutions. This stage involves identifying novel targets (like mesothelin, PD-L1, or FAK pathways) and synthesizing complex biologic agents or small molecule inhibitors. Due to the orphan drug nature of MM, these R&D efforts often benefit from regulatory incentives, which accelerate the path to clinical trials. Intellectual property protection at this stage is crucial, ensuring monopolistic pricing power upon market entry, especially for innovative immunotherapies.

The midstream phase involves manufacturing, complex logistics, and distribution. Manufacturing of biologic drugs, particularly monoclonal antibodies used in immunotherapy, is a sophisticated and highly regulated process requiring specialized facilities and stringent quality control. Distribution channels are predominantly indirect, utilizing established pharmaceutical wholesalers and distributors to reach end-users. Given the stability requirements for many biologicals (cold chain logistics), the distribution network must be robust and certified. Direct distribution, although less common, is sometimes employed by manufacturers for specific high-value devices or specialized hospital accounts.

The downstream segment centers on patient access, treatment administration, and post-treatment monitoring. Key players here are the healthcare providers (Hospitals and Cancer Centers) who administer the therapies, often within multidisciplinary tumor boards. Payer organizations (governments, private insurers) play a critical role in determining patient access through coverage and reimbursement policies, significantly influencing product utilization rates. The complexity of MM treatment means patients are high-cost, high-touch consumers, requiring extensive supportive care and follow-up using diagnostic tools for recurrence monitoring, thus sustaining the revenue stream for providers and diagnostic companies alike.

The primary end-users and potential customers in the Malignant Mesothelioma market are highly sophisticated institutional entities specializing in complex oncology care. These include large, tertiary care hospitals and globally recognized comprehensive cancer centers, such as the Memorial Sloan Kettering Cancer Center or MD Anderson Cancer Center. These institutions are the core purchasers of premium-priced therapeutics (immunotherapy and targeted drugs), advanced surgical instruments, and state-of-the-art radiation oncology equipment. Their patient populations often participate in clinical trials, positioning them at the forefront of adopting emerging treatment protocols, making them critical targets for market penetration by pharmaceutical companies and device manufacturers.

Beyond the major academic centers, specialty private oncology clinics and community hospitals with established oncology departments represent a significant and expanding customer base, particularly in developed markets. While they may not handle the most radical surgical procedures, they are increasingly administering standard-of-care systemic treatments, including combination chemotherapy and established immunotherapies, especially as patent expirations make some biologics more accessible. These clinics prioritize treatments that offer high efficacy, manageable toxicity profiles, and strong payer reimbursement, focusing on maximizing patient throughput and outcome quality within defined protocols.

A crucial, though often indirect, customer group includes governmental and private health insurance payers. Their policies determine the financial viability of market products. For orphan drugs like those treating MM, demonstrating superior efficacy and cost-effectiveness (value-based evidence) is essential to secure favorable coverage decisions. Ultimately, while the patient receives the drug, the economic purchasing power rests predominantly with the institutional buyers and the reimbursement entities that authorize payment for high-cost therapies and prolonged hospital stays associated with treatment.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 1.8 Billion |

| Market Forecast in 2033 | USD 3.0 Billion |

| Growth Rate | 7.5% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Bristol Myers Squibb, Merck & Co., AstraZeneca, Eli Lilly and Company, Pfizer, Novartis, Roche, Genentech, Amgen, Boehringer Ingelheim, Bavarian Nordic, Celgene, Takeda Pharmaceutical, Clovis Oncology, Array Biopharma, Janssen Global Services, Viatris, GSK. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technology landscape in the Malignant Mesothelioma market is rapidly evolving, driven by the need for more precise diagnostics and less toxic, more efficacious treatments. A cornerstone of modern MM management is advanced radiation oncology technology. Technologies such as Intensity-Modulated Radiation Therapy (IMRT) and Stereotactic Body Radiation Therapy (SBRT) are crucial for delivering highly conformal doses to the tumor while sparing critical surrounding structures like the lungs and heart, a necessity given the proximity of pleural tumors to sensitive organs. Furthermore, the integration of 4D imaging and motion management systems allows for precise targeting, mitigating the effects of respiratory movement during treatment, thereby improving local control rates significantly.

On the diagnostic front, the adoption of liquid biopsy technologies is poised to be transformative. Unlike invasive tissue biopsies, liquid biopsies enable non-invasive molecular profiling by analyzing circulating tumor cells (CTCs) or circulating tumor DNA (ctDNA) in the blood. This technology is vital in MM for monitoring minimal residual disease after surgery, detecting early recurrence, and tracking acquired resistance mutations in real-time. This capability allows oncologists to adjust systemic therapy promptly and provides crucial prognostic information. Furthermore, advanced immunohistochemistry and genomic sequencing techniques (Next-Generation Sequencing, NGS) are essential for precisely subtyping the tumor (epithelioid vs. sarcomatoid) and identifying actionable mutations that guide the use of targeted therapies, optimizing patient selection.

In the therapeutic arena, drug manufacturing technologies are critical, particularly for complex biologics like monoclonal antibodies and cellular therapies. Advanced biotechnology platforms are necessary for scalable, consistent production of high-quality immunotherapies, ensuring global supply stability. The emerging focus on regional and localized delivery methods, such as hyperthermic intrathoracic chemotherapy (HITHOC) or pressurized intraperitoneal aerosol chemotherapy (PIPAC) for peritoneal mesothelioma, relies on specialized delivery systems and perfusion technologies. These localized therapies aim to maximize drug concentration at the tumor site while minimizing systemic toxicity, representing a crucial technological advancement for improving outcomes in specific MM subsets.

The current dominant treatment approach is multimodal, increasingly centered around Immunotherapy, specifically checkpoint inhibitors (e.g., anti-PD-1 agents) often used in combination with standard chemotherapy (platinum and pemetrexed). This combination has demonstrated superior overall survival rates compared to chemotherapy alone in first-line settings.

The market size is directly influenced by historical asbestos exposure due to the long latency period (20 to 50 years) before cancer manifestation. This guarantees a sustained influx of new diagnoses globally for the foreseeable future, particularly in regions that experienced heavy industrial asbestos use in the mid-20th century, ensuring continued demand for treatment solutions.

Key diagnostic advancements include high-resolution medical imaging integrated with Artificial Intelligence (AI) for earlier detection of pleural plaques and subtle tumors, alongside the increasing adoption of liquid biopsy techniques (ctDNA analysis) for non-invasive molecular profiling, monitoring recurrence, and detecting treatment resistance.

The Asia Pacific (APAC) region is projected to exhibit the highest Compound Annual Growth Rate (CAGR). This growth is fueled by expanding healthcare infrastructure, rising health expenditure, and a large patient pool resulting from significant historical asbestos exposure during industrial expansion in countries like China and India.

Given that Malignant Mesothelioma is a rare disease, many novel therapeutics receive Orphan Drug Designation (ODD) from regulatory bodies like the FDA and EMA. ODD provides pharmaceutical companies with incentives, including market exclusivity, tax credits, and streamlined approval processes, which are critical for justifying the high R&D costs associated with developing treatments for a small patient population.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.