ID : MRU_ 434452 | Date : Dec, 2025 | Pages : 246 | Region : Global | Publisher : MRU

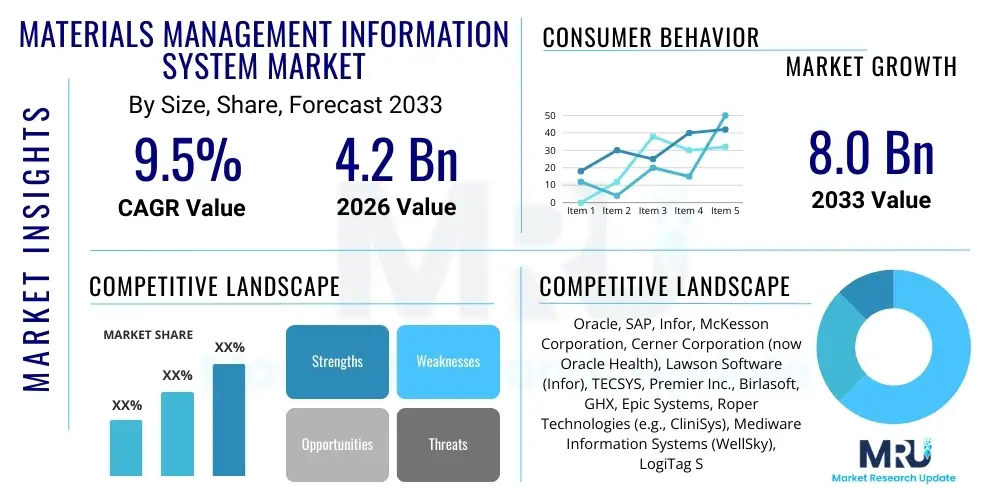

The Materials Management Information System Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 9.5% between 2026 and 2033. The market is estimated at USD 4.2 Billion in 2026 and is projected to reach USD 8.0 Billion by the end of the forecast period in 2033.

The Materials Management Information System (MMIS) Market encompasses software solutions designed to manage the comprehensive lifecycle of materials, including procurement, inventory management, storage, usage tracking, and disposal, primarily within complex operational environments such as healthcare institutions, manufacturing facilities, and large logistics networks. These systems automate critical supply chain functions, providing real-time visibility into inventory levels, reducing operational costs, minimizing waste, and ensuring compliance with regulatory standards. MMIS solutions are foundational to operational efficiency, integrating seamlessly with Enterprise Resource Planning (ERP) systems and Electronic Health Records (EHR) in the healthcare sector, allowing organizations to optimize capital expenditure and improve service delivery quality by preventing stockouts or obsolescence. The core objective of deploying MMIS is to transform decentralized, manual processes into centralized, data-driven material flow management.

Major applications of MMIS span across several high-stakes industries where precise material control is paramount. In the healthcare sector, MMIS is essential for managing critical supplies, pharmaceuticals, surgical instruments, and high-value medical devices, directly impacting patient safety and financial sustainability. In manufacturing and logistics, these systems are deployed to optimize raw material flow, track components through production stages, manage finished goods inventory, and streamline distribution logistics. Key benefits derived from robust MMIS implementation include significant cost reduction through optimized purchasing and decreased carrying costs, enhanced operational productivity due to streamlined workflows, and superior financial accountability resulting from accurate consumption data and audit trails. Furthermore, the modern iteration of MMIS often incorporates predictive analytics and mobile capabilities, ensuring that purchasing decisions are based on forecasted demand rather than historical averages, thus driving proactive supply chain resilience.

The market growth is fundamentally driven by the accelerating demand for digital transformation across industries, particularly the shift towards integrated supply chain visibility and automated inventory replenishment mechanisms. Organizations are increasingly recognizing that material costs often constitute a substantial portion of their operating budgets, making efficient management an imperative for profitability. The proliferation of complex, global supply chains necessitates sophisticated tracking tools to mitigate risks associated with geopolitical instability and unforeseen disruptions. Additionally, the stringent regulatory environment in sectors like healthcare, which requires meticulous tracking of materials for patient safety and compliance (e.g., Unique Device Identification or UDI), strongly compels the adoption of advanced MMIS solutions. These driving factors, coupled with technological advancements like cloud deployment and IoT integration, ensure sustained market expansion over the forecast period.

The Materials Management Information System Market is experiencing rapid structural evolution driven by robust business trends centered on cloud adoption, modular flexibility, and the integration of advanced analytics. Business trends highlight a strong movement away from monolithic, on-premise systems toward flexible, subscription-based Software-as-a-Service (SaaS) models, offering scalability, reduced upfront capital expenditure, and easier maintenance, particularly appealing to mid-sized enterprises and sprawling hospital networks. Furthermore, the competitive landscape is shifting toward specialized solutions that cater specifically to the nuances of industries such as healthcare (e.g., surgical tray tracking) or specialized manufacturing (e.g., hazardous materials management), necessitating vendor investment in deep vertical expertise. Strategic partnerships between core MMIS providers and specialized logistics and supply chain firms are also becoming common, aiming to offer end-to-end, integrated solutions that cover everything from supplier onboarding to last-mile delivery tracking, thereby enhancing the overall value proposition for end-users seeking comprehensive operational control and risk mitigation across complex value chains.

Regionally, North America maintains its dominance due to high digital maturity, significant investment in healthcare infrastructure digitization, and the presence of major technology providers and early adopters of sophisticated supply chain technologies. However, the Asia Pacific (APAC) region is projected to exhibit the highest growth rate, fueled by rapid industrialization, increasing governmental focus on improving public healthcare logistics, and substantial infrastructure investment in emerging economies like India and China, which are modernizing their outdated supply chain frameworks. European growth is steady, largely driven by regulatory compliance requirements, such as the Medical Device Regulation (MDR), and a strong push toward creating resilient, localized supply chains following recent global disruptions. Latin America and the Middle East & Africa (MEA) are also showing promising acceleration, primarily focused on adopting cloud-based solutions to leapfrog traditional infrastructural limitations and rapidly improve inventory control within burgeoning manufacturing and healthcare sectors.

Segment trends indicate that the Software component, particularly cloud-based platforms, will retain the largest market share, reflecting ongoing digital transformation efforts. Within deployment models, the SaaS segment is expected to outpace traditional on-premise deployments due to its inherent advantages in accessibility and scalability. The healthcare end-user segment, comprising hospitals, clinics, and pharmaceutical companies, will remain the primary market driver, given the critical nature of managing medical supplies, coupled with intense regulatory scrutiny and the significant financial impact of inefficient inventory practices in this sector. However, the manufacturing segment, specifically high-tech and automotive manufacturing, is also showing robust demand for MMIS solutions that integrate seamlessly with Industry 4.0 initiatives, utilizing IoT and predictive maintenance features to manage complex Bill of Materials (BOM) and ensure JIT (Just-in-Time) inventory delivery, thereby minimizing carrying costs and maximizing production uptime, showcasing diverse application growth.

The integration of Artificial Intelligence (AI) and Machine Learning (ML) into Materials Management Information Systems is addressing user expectations for enhanced efficiency, predictive capabilities, and proactive risk mitigation, transforming the traditional role of inventory tracking into a strategic forecasting function. Users frequently inquire about AI's ability to accurately predict demand fluctuations, optimize complex stocking locations, and automatically identify and address potential supply chain disruptions before they materially impact operations. The key themes revolve around achieving true 'intelligent inventory' management—moving beyond reactive replenishment based on reorder points to a system that dynamically adjusts stock levels, identifies optimal purchasing windows, and minimizes bullwhip effects across the supply network. Furthermore, significant user interest focuses on AI’s role in automating compliance reporting and invoice reconciliation, reducing manual errors and labor costs associated with administrative tasks within materials management, leading to improved overall resource utilization and operational clarity in highly regulated industries like pharmaceutical production and hospital administration.

Concerns often center on data privacy, the requirement for high-quality, normalized historical data to train accurate ML models, and the complexity of integrating advanced AI modules with legacy MMIS infrastructure. Organizations are seeking clear pathways and documented return-on-investment (ROI) figures for AI-driven materials management enhancements. Expectations are high regarding the use of Natural Language Processing (NLP) to analyze unstructured data from supplier contracts and market news to assess geopolitical or natural disaster risks impacting sourcing, creating a more resilient and responsive supply chain ecosystem. The deployment of AI-powered Robotic Process Automation (RPA) tools is specifically anticipated to revolutionize the warehouse environment, automating routine inventory counting, cycle checking, and documentation processes, thereby freeing up human resources for strategic oversight and complex problem-solving rather than routine data entry and verification tasks, substantially raising the productivity ceiling of existing MMIS deployments.

Overall, AI is expected to transition MMIS from a system of record to a system of intelligence. By leveraging complex algorithms, AI can analyze vast datasets—including consumption rates, seasonal variations, clinical procedure schedules (in healthcare), and macroeconomic indicators—to generate highly accurate demand forecasts, significantly reducing both overstocking (and associated obsolescence costs) and critical shortages. This shift provides materials managers with prescriptive insights rather than just descriptive reports, enabling them to make timely, data-backed decisions concerning supplier selection, contract negotiations, and dynamic pricing strategies. The foundational influence of AI is therefore positioned to maximize inventory capital efficiency and provide a crucial competitive advantage to organizations that successfully adopt these intelligent features, driving the next phase of advanced MMIS market evolution.

The Materials Management Information System Market is propelled by several strong drivers, counterbalanced by persistent restraints, and offers significant emerging opportunities, all shaped by core impact forces influencing supply chain resilience and cost management imperatives. A primary driver is the pervasive need across critical industries, particularly healthcare and complex manufacturing, for enhanced inventory visibility and precision. In healthcare, the necessity to manage high-cost specialty medical supplies and implants requires real-time tracking from dock to patient bedside to ensure both financial accountability and patient safety compliance, making sophisticated MMIS essential infrastructure. Furthermore, the global push towards digitalizing core business functions and integrating supply chain data across disparate organizational systems strongly mandates the adoption of advanced, interoperable MMIS platforms capable of feeding accurate data into higher-level ERP and financial planning systems, thereby generating significant momentum for market expansion.

However, the market faces considerable restraints that temper the speed of adoption, particularly the substantial initial investment costs associated with implementing complex MMIS software, including integration fees, hardware upgrades, and extensive training requirements for staff. Many potential users, especially smaller healthcare facilities or mid-market manufacturing companies, struggle with the capital outlay and the long transition period necessary for system migration, often leading to prolonged decision cycles. Furthermore, interoperability challenges persist, as integrating a new MMIS with existing, often decades-old legacy ERP and clinical systems can be technically arduous and fraught with data migration risks, posing a significant barrier. The requirement for specialized IT talent to manage, maintain, and optimize these systems also presents a workforce constraint, particularly in developing regions where skilled labor in sophisticated supply chain IT is scarce, leading to slower deployment rates than technology availability might suggest.

The most compelling opportunities for market growth lie in the rapid proliferation of cloud-based deployment models and the subsequent emergence of advanced analytical features, offering scalability and lower total cost of ownership (TCO) that appeal to a broader range of enterprises globally. Furthermore, the growing adoption of Internet of Things (IoT) technologies and RFID/Barcode scanning within materials management creates opportunities for MMIS vendors to offer advanced asset tracking and automated replenishment functionalities, moving systems closer to a truly automated, zero-touch inventory environment. The impact forces shaping the market are centered on cost pressures, demanding efficiency and waste reduction, and the imperative for supply chain resilience, especially following the disruptions caused by global events. These forces push organizations towards robust, predictive MMIS solutions that not only manage existing inventory but also forecast future requirements and assess risk in real-time, fundamentally shifting MMIS from an administrative tool to a strategic asset for achieving operational excellence and maintaining competitive advantage in volatile markets.

The Materials Management Information System Market is comprehensively segmented across several dimensions, including Component, Deployment Model, Application, and End-User, providing a nuanced view of where market investments and technological adoption are concentrated. Understanding these segments is crucial for strategic planning, as different industries and organizations prioritize distinct feature sets. For instance, the separation of the market into Software and Services components reflects the complex requirement for not only the foundational platform but also ongoing implementation, integration, training, and maintenance support, which often constitutes a significant portion of the total contract value, especially for large, customized enterprise deployments spanning multiple regional facilities.

The segmentation by Deployment Model—On-premise versus Cloud/SaaS—is perhaps the most indicative of the market's technological trajectory. While traditional on-premise solutions still serve legacy systems and highly regulated environments requiring absolute data control, the overwhelming trend favors cloud-based SaaS models. This preference is driven by the inherent benefits of cloud infrastructure, including accelerated deployment, automatic updates, reduced reliance on in-house IT infrastructure, and significantly improved scalability and accessibility, which is vital for multinational corporations and expansive healthcare networks that require real-time data synchronization across geographically dispersed locations and diverse business units.

Furthermore, segmenting the market by End-User clearly highlights the critical role of MMIS in the healthcare sector, which leads in adoption due to intense pressures to manage medical supply costs and regulatory mandates regarding traceability. Within this segment, hospitals and large integrated delivery networks (IDNs) represent the largest sub-segment, utilizing MMIS for everything from general consumables to high-value capital equipment. Concurrently, the robust growth in the manufacturing sector—particularly automotive, electronics, and aerospace—is driven by the need for MMIS to support complex, multi-tiered supply chains, integrate with Manufacturing Execution Systems (MES), and facilitate highly accurate JIT inventory strategies, thereby ensuring materials are available precisely when production lines require them, minimizing downtime and inventory carrying costs simultaneously.

The value chain for the Materials Management Information System Market begins with the upstream activities dominated by core technology providers and independent software vendors (ISVs) responsible for the research, development, and coding of the foundational MMIS platform and subsequent modular enhancements. This upstream phase involves significant intellectual property investment in developing specialized inventory algorithms, user interface/experience (UI/UX) design, and ensuring seamless API connectivity for integration purposes. Key upstream players include major ERP system manufacturers (like SAP and Oracle) who offer MMIS modules, alongside specialized niche MMIS vendors focused purely on specific vertical requirements, such as those tailored exclusively for surgical supply management or high-tech component tracking, differentiating themselves through industry-specific functionalities and robust security features appropriate for the data sensitivity of their chosen sector.

Moving downstream, the value chain shifts focus to implementation, integration, and distribution, where system integrators, third-party consulting firms, and Value-Added Resellers (VARs) play a crucial role. These downstream actors are responsible for customizing the core software to meet specific end-user operational requirements, migrating historical data, configuring the system interfaces with existing finance and operational software, and providing the intensive user training required for successful adoption. Distribution channels are primarily bifurcated into direct sales models, where large vendors handle enterprise deals and implementation internally, and indirect channels, utilizing channel partners, regional resellers, and managed service providers (MSPs). Indirect distribution is particularly crucial in reaching Small and Medium Enterprises (SMEs) and penetrating diverse international markets where local expertise in regulatory compliance and regional business practices is essential for successful deployment and ongoing support, necessitating strong local partnerships.

The service component within the value chain is increasingly significant, especially for cloud-based MMIS. Post-deployment support, regular software updates, system optimization consulting, and cloud hosting services ensure the longevity and effectiveness of the MMIS solution. For end-users, the value derived is maximized when the MMIS effectively integrates with operational hardware, such as RFID readers, barcode scanners, IoT sensors, and automated dispensing units. The complete chain, therefore, links advanced software development (upstream) through complex system integration and sales (distribution) to continuous service and maintenance (downstream), ultimately delivering tangible value by reducing materials waste, optimizing working capital, and ensuring critical supply availability across the end-user's entire operational footprint, thereby transforming raw software into a strategic business enabler for global supply chain optimization.

The primary potential customers and end-users of Materials Management Information Systems are organizations with high volumes of material turnover, complex inventory requirements, and stringent regulatory or quality control needs where material flow directly impacts service delivery or product quality. The largest and most demanding segment is Healthcare Providers, encompassing large Integrated Delivery Networks (IDNs), acute care hospitals, specialized surgical centers, and long-term care facilities. These entities rely on MMIS to manage thousands of distinct medical items, pharmaceuticals, and perishable supplies, where inventory inaccuracy can lead not only to significant financial losses but also life-critical shortages. Hospitals are increasingly focusing on point-of-use inventory management systems integrated with the MMIS to track supplies consumed during procedures, ensuring accurate patient billing and automated replenishment triggers directly linked to clinical usage.

Another major buying segment is the Pharmaceutical and Biotechnology industry, which requires MMIS solutions capable of handling strict regulatory compliance (e.g., FDA requirements, serialization, and cold chain logistics) related to raw materials, in-process goods, and finished drug products. For these highly regulated buyers, MMIS functionality must extend beyond basic inventory counts to include detailed batch tracking, expiry date management, quality assurance hold processes, and audit trail generation, making the selection criteria highly specific and focused on compliance features. The need for precise tracking is compounded by the global nature of pharmaceutical production and distribution, necessitating robust systems that can handle multiple currencies, regulatory frameworks, and complex international shipping logistics, often utilizing advanced technologies like blockchain for enhanced traceability and tamper resistance throughout the entire cold chain.

Furthermore, the Manufacturing and Industrial sector represents a vast and growing customer base, specifically within high-value segments like Automotive, Aerospace, and Electronics production, where Just-in-Time (JIT) and high-mix, low-volume production strategies dominate. These customers require MMIS solutions that interface directly with sophisticated production scheduling systems and shop floor controls. Their focus is on ensuring a continuous, optimized flow of raw materials and sub-components to prevent costly production line stoppages, requiring highly accurate inventory forecasting, supplier relationship management integration, and sometimes vendor-managed inventory (VMI) capabilities facilitated by the MMIS platform. The convergence of industrial IoT (IIoT) sensors and MMIS data streams is making systems increasingly attractive to these manufacturers seeking true Industry 4.0 operational efficiency.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 4.2 Billion |

| Market Forecast in 2033 | USD 8.0 Billion |

| Growth Rate | CAGR 9.5% |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Oracle, SAP, Infor, McKesson Corporation, Cerner Corporation (now Oracle Health), Lawson Software (Infor), TECSYS, Premier Inc., Birlasoft, GHX, Epic Systems, Roper Technologies (e.g., CliniSys), Mediware Information Systems (WellSky), LogiTag Systems, Zocdoc, CompuGroup Medical, Allscripts Healthcare Solutions (now Veradigm), Plex Systems. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological landscape of the Materials Management Information System market is rapidly evolving, moving beyond simple transactional processing to incorporate sophisticated, real-time data capture and analytical capabilities crucial for modern supply chain management. Cloud computing stands as the most critical technology, fundamentally redefining deployment and accessibility. The shift to Software-as-a-Service (SaaS) models allows organizations to access advanced MMIS functionalities without heavy upfront infrastructure investment, enabling faster deployment and ensuring automatic, centralized software updates. This model enhances data accessibility across multi-site operations and facilitates easier integration with other cloud-based enterprise applications, fostering a highly collaborative and data-synchronized supply chain ecosystem crucial for efficient material flow and vendor management across global networks.

Furthermore, the physical tracking and visibility layer of MMIS is being revolutionized by the widespread adoption of identification and location technologies, primarily Radio Frequency Identification (RFID) and advanced Internet of Things (IoT) sensors. RFID technology, particularly passive UHF RFID tags, enables high-speed, automated inventory counts without line-of-sight scanning, drastically improving inventory accuracy and reducing labor time in large warehouses or surgical supply rooms. IoT sensors are crucial for monitoring condition-sensitive materials, such as pharmaceuticals requiring strict temperature control (cold chain monitoring), automatically feeding real-time environmental data directly into the MMIS. This technological synergy allows the system to trigger alerts or implement corrective actions proactively, ensuring material integrity and compliance with stringent quality and safety standards, especially vital in sectors like food, pharma, and specialized medical device handling where product integrity is non-negotiable.

Finally, emerging technologies such as Artificial Intelligence (AI), Machine Learning (ML), and Blockchain are positioned to be significant future differentiators in the MMIS space. AI/ML algorithms are being integrated to power predictive analytics, enabling systems to forecast demand with greater accuracy, optimize procurement timing, and identify potential fraud or anomalies in inventory consumption patterns, transforming materials management from a reactive to a prescriptive function. Blockchain technology, although still nascent in widespread MMIS application, offers the potential for creating highly secure, immutable, and transparent audit trails for material provenance, crucial for high-value items, regulatory compliance, and anti-counterfeiting efforts in complex, multi-party supply chains. The convergence of these advanced digital tools ensures that the modern MMIS is not merely an inventory tracker but a strategic, intelligent engine driving operational efficiency and comprehensive supply chain risk mitigation.

Regional dynamics play a crucial role in shaping the Materials Management Information System Market, reflecting variations in digital readiness, regulatory pressures, and investment priorities across major economic zones. North America currently dominates the global market share, largely attributed to the high sophistication of its healthcare and manufacturing sectors, coupled with substantial early investments in enterprise software and digitalization initiatives. The United States, in particular, drives adoption due to the presence of major technology vendors, robust economic growth necessitating optimized supply chain logistics, and the increasing pressure on healthcare systems to curb expenditures by implementing precise inventory control and supply utilization monitoring systems. Regulatory mandates and financial incentives favoring EHR and supply chain digitalization further accelerate MMIS penetration across Integrated Delivery Networks (IDNs) and large hospital groups seeking operational transparency.

Europe represents a mature market, demonstrating steady and substantial growth, primarily driven by stringent quality and traceability regulations, such as the EU Medical Device Regulation (MDR) and general industrial safety standards. These regulatory frameworks necessitate highly capable MMIS solutions to maintain comprehensive audit trails and device identification records throughout the supply chain. Adoption rates are high across Western European economies, focusing particularly on optimizing warehouse operations and achieving supply chain resilience. The market dynamic in Europe is also characterized by a strong demand for MMIS solutions that are easily scalable across multinational operations, catering to pan-European enterprises seeking harmonized material management practices across diverse national healthcare and industrial systems, often favoring vendors that offer multi-language and multi-currency support, while increasingly prioritizing data sovereignty considerations in cloud deployments.

The Asia Pacific (APAC) region is projected to be the fastest-growing market, experiencing explosive growth fueled by rapid industrialization, massive government investment in modernizing public health infrastructure, and the expansion of the manufacturing base, especially in China, India, and Southeast Asia. As these economies mature, organizations are moving away from manual and fragmented inventory management methods towards integrated, cloud-based MMIS platforms to achieve global competitiveness and efficiency. While initial adoption may prioritize basic inventory and procurement functionalities, the long-term trend indicates a rapid leapfrogging toward advanced solutions utilizing IoT and AI to manage burgeoning and complex supply chains that are critical to serving both domestic populations and global export markets. Furthermore, the Middle East and Africa (MEA) and Latin America are showing strong momentum, primarily focusing on cloud MMIS adoption to rapidly address fundamental challenges in inventory accuracy, reduce stock pilferage, and improve transparency in pharmaceutical supply chains, benefiting from the lower infrastructure requirements of SaaS solutions.

The primary function of an MMIS in healthcare is to manage the entire lifecycle of medical supplies, pharmaceuticals, and high-value equipment, ensuring optimal inventory levels, accurate tracking from procurement to patient use, reduced stockouts, and compliance with patient safety and financial regulations (e.g., UDI tracking and accurate billing). It acts as the backbone for supply chain efficiency.

Cloud deployment (SaaS) significantly reduces the TCO of MMIS by eliminating the need for large upfront capital expenditures on hardware and infrastructure, minimizing associated IT maintenance costs, and providing automatic software updates. This model generally results in a predictable, lower operational expenditure (OpEx) compared to traditional on-premise systems.

The most critical integration is with RFID and IoT sensors. RFID enables hands-free, high-speed inventory counting and tracking, drastically improving accuracy. IoT integration allows for real-time monitoring of critical conditions, such as temperature (cold chain), ensuring the integrity and compliance of sensitive materials like vaccines and specialized medical devices.

Key implementation challenges include the complexity of integrating the new MMIS with existing legacy ERP, financial, and clinical systems; the significant initial financial investment required for customization and training; and the necessity of ensuring high-quality, normalized historical data migration to prevent early operational errors and guarantee reliable system performance.

AI transforms materials management by enabling predictive analytics for highly accurate demand forecasting, optimizing complex stocking strategies based on usage patterns, and automating procurement decisions. This shift moves organizations away from reactive inventory replenishment toward proactive, intelligent supply chain planning, maximizing working capital efficiency and mitigating shortage risks.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.